Goldman Sachs expects Nvidia ’beat and raise,’ lifts price target to $240

Introduction & Market Context

Acast AB (STO:ACAST) presented its Q3 2025 results on October 30, showcasing strong growth and improved profitability that sent its stock soaring 24.13% to SEK 26.75, approaching its 52-week high. The podcast monetization company reported SEK 642 million in net sales, exceeding analyst expectations of SEK 606.5 million by 5.86%.

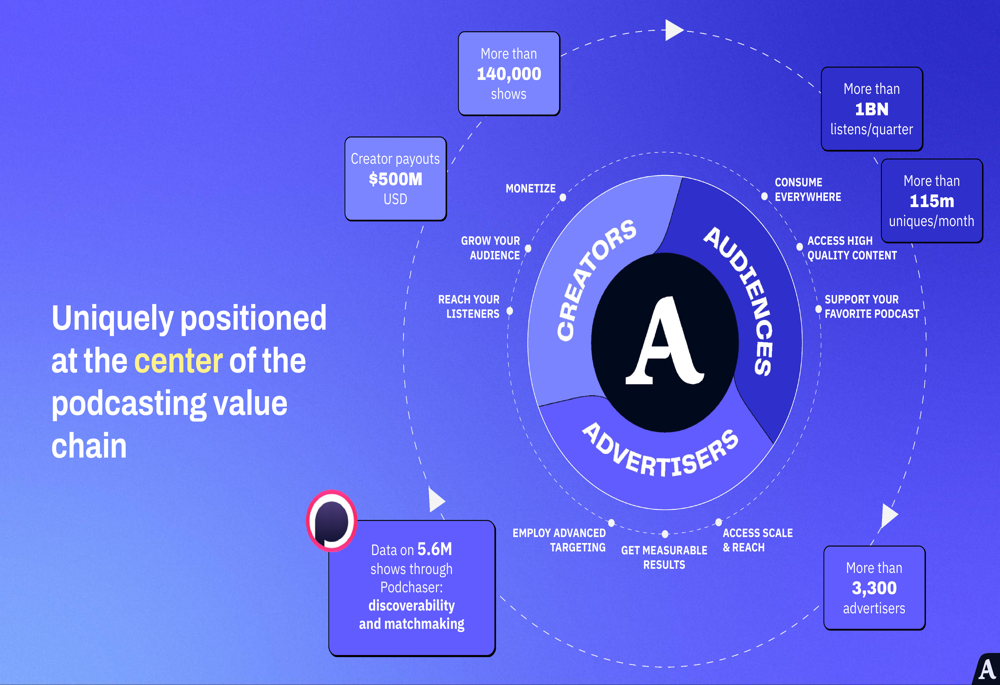

The company’s performance reflects its strengthening position in the global podcasting ecosystem, where it connects more than 140,000 shows with advertisers while serving over 115 million unique monthly listeners. With creator payouts reaching $500 million USD and quarterly listens exceeding 1 billion, Acast continues to capitalize on the growing but still undermonetized podcast advertising market.

Quarterly Performance Highlights

Acast delivered exceptional financial results in Q3 2025, with net sales growth of 35% year-over-year and an impressive 41% organic growth rate when adjusted for currency effects.

As shown in the following chart of quarterly net sales growth:

The company’s gross profit increased by 31% year-over-year to SEK 252 million, maintaining a solid gross margin of approximately 40% despite rapid expansion.

As illustrated in this gross profit and margin chart:

Profitability metrics showed notable improvement, with adjusted EBITDA margin reaching 6%, representing a 3 percentage point improvement year-over-year. The company also achieved a positive EBIT margin of 2%.

The following chart demonstrates this profitability uplift:

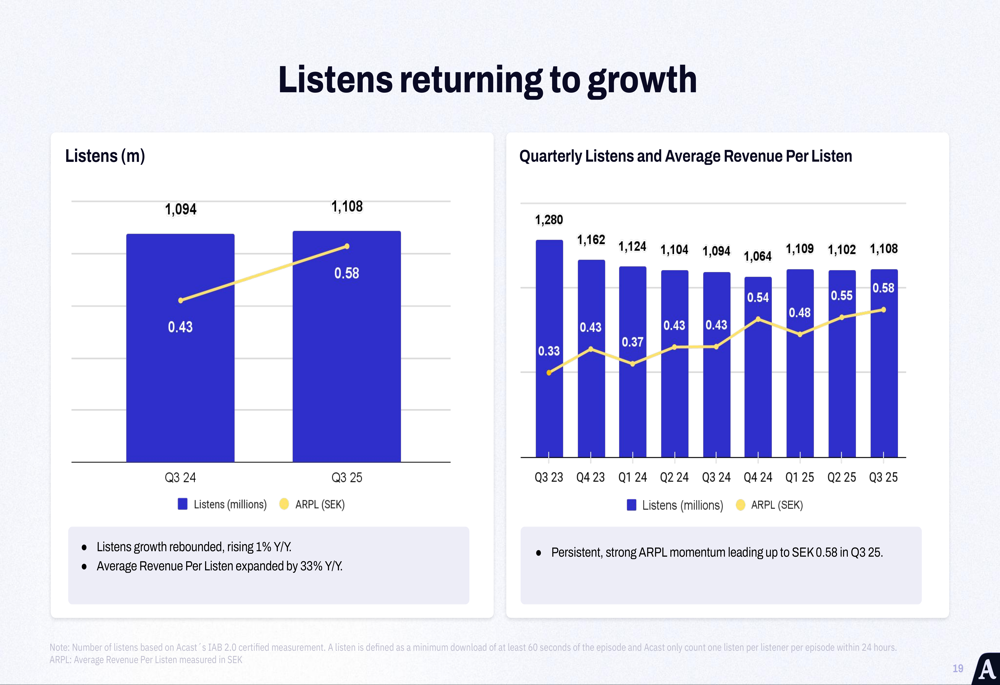

Listens returned to growth in Q3 2025, increasing 1% year-over-year to 1,108 million, while average revenue per listen (ARPL) continued its upward trajectory to SEK 0.58.

As shown in this chart tracking quarterly listens and ARPL:

Strategic Initiatives

During the quarter, Acast announced a strategic partnership with Magnite to expand its programmatic advertising capabilities. This collaboration aims to attract global demand, improve revenue potential for creators, enable unified campaign planning, and capitalize on omnichannel advertising trends.

The company also highlighted its unique position in the podcasting value chain, sitting at the center of the ecosystem connecting creators, audiences, and advertisers.

As illustrated in this ecosystem diagram:

Acast’s regional performance showed particular strength in Europe, which is fueling overall growth, while North America remains a significant growth opportunity given the company’s current 2-3% market share compared to its dominant positions in the UK (60-65%) and Sweden (45-50%).

CEO Greg Glenday emphasized the company’s strategic positioning during the earnings call: "We are riding a powerful secular tailwind where consumption already exists and the ad spend is playing catch-up."

Forward-Looking Statements

Acast updated its long-term financial targets during the presentation, now aiming for organic net sales growth (CAGR) exceeding 15% for the period 2025-2028, and targeting an operating profit (EBIT) margin of 10% by 2028.

The updated targets reflect management’s confidence in the company’s growth trajectory and operational leverage, as shown in this slide:

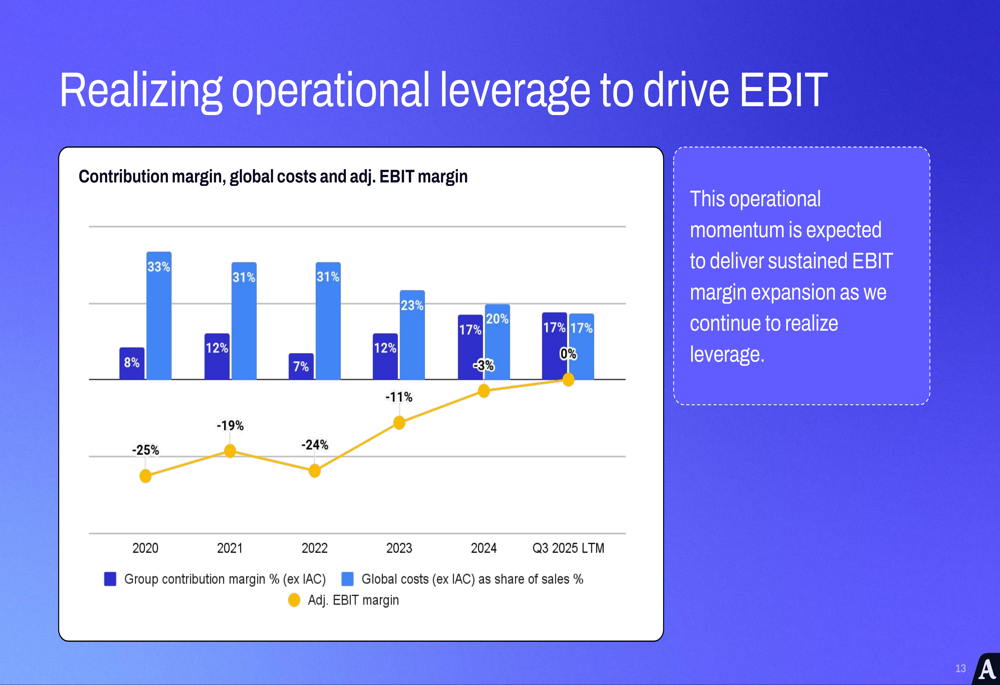

The path to achieving these targets includes leveraging Acast’s global scale, improving monetization, and expanding through omnichannel strategies. The company expects to benefit from increasing transaction volumes and greater utilization of low-touch sales channels, driving scalability and margin expansion.

As demonstrated in this operational leverage chart:

The company highlighted that its operational momentum is expected to deliver sustained EBIT margin expansion as it continues to realize leverage from its business model.

Competitive Industry Position

Acast maintains a unique position in the podcasting industry, working with a full spectrum of creators from major publishers like The Guardian and The Economist to niche shows with highly engaged audiences.

The company’s key takeaways from the quarter emphasize its strong organic growth, North America’s role as the primary engine for future expansion, continued profitability improvements, and confidence in meeting updated financial targets.

As summarized in this key takeaways slide:

With a cash position of SEK 548 million and improving cash flow from operations (SEK 20 million in Q3), Acast appears well-positioned to execute on its growth strategy while maintaining financial discipline.

Market reaction to the results was overwhelmingly positive, with the stock price jumping 24.13% following the announcement, reflecting investor confidence in both the quarterly performance and the company’s updated long-term targets. Acast’s stock is now trading just below its 52-week high of SEK 26.75, having delivered a remarkable 53.05% price return over the past six months.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.