U.S. stock futures slip lower on waning rate cut bets; Applied Materials falls

Introduction & Market Context

Alkane Resources Ltd (ASX:ALK) presented its Q1 FY2026 earnings results on November 13, 2025, marking the first quarter to include contributions from its recently completed merger with Mandalay Resources. The merger, finalized on August 5, 2025, has transformed Alkane into a multi-mine producer with operations spanning Australia and Sweden.

The company reported a significant increase in production and revenue, though profitability declined amid rising costs. Alkane’s market capitalization now stands at A$1.5 billion, and the company was included in the ASX 300 index in September 2025, enhancing its visibility among institutional investors.

Quarterly Performance Highlights

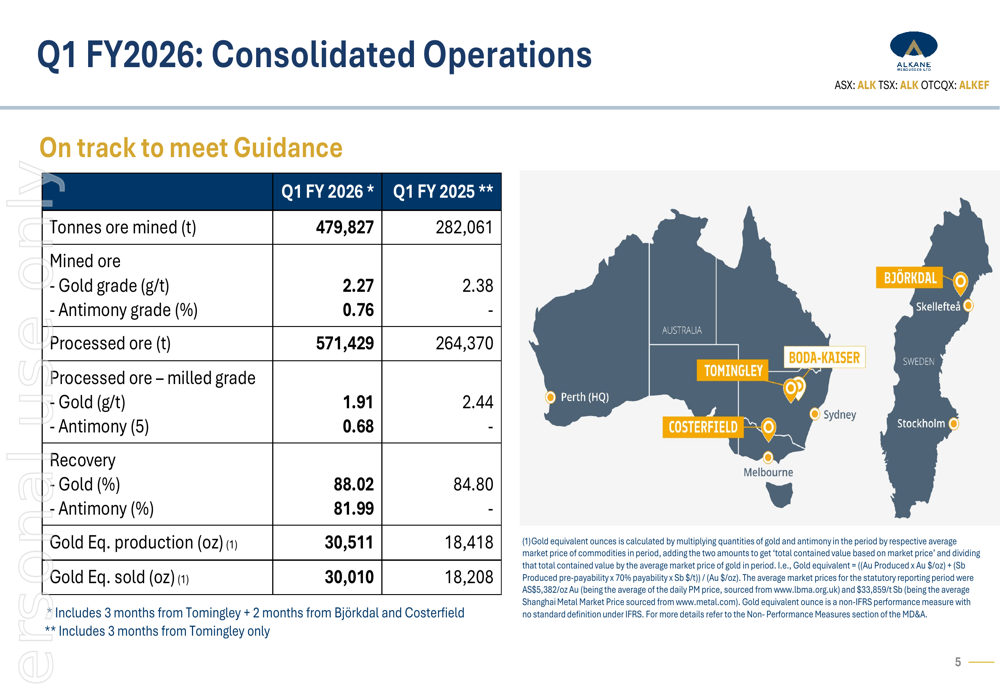

Alkane reported gold equivalent production of 30,511 ounces for Q1 FY2026, a 65.7% increase from 18,418 ounces in the same period last year. This substantial growth primarily reflects the addition of the Björkdal (Sweden) and Costerfield (Australia) mines to complement the existing Tomingley operation in Australia.

As shown in the consolidated operations data, mining volumes increased significantly year-over-year, though gold grades were slightly lower:

The Tomingley mine in Australia maintained stable production with 18,335 ounces of gold in Q1 FY2026, comparable to 18,418 ounces in Q1 FY2025 despite slightly lower grades. The newly acquired Björkdal and Costerfield operations contributed 5,987 ounces and 6,189 gold equivalent ounces, respectively, for the two months since the merger completion.

Detailed Financial Analysis

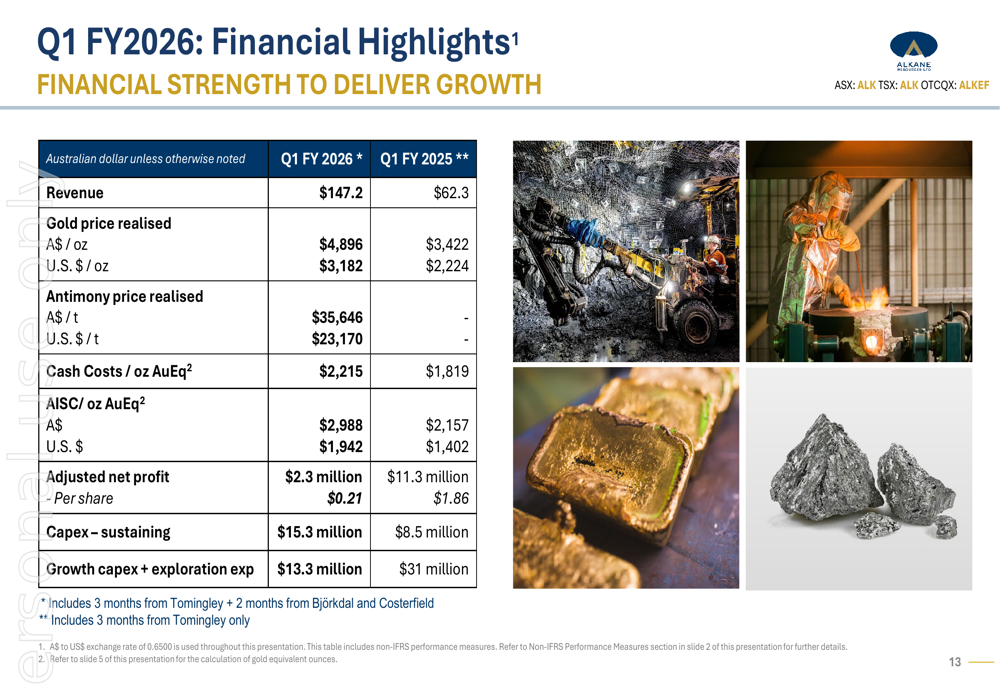

The company’s financial performance showed mixed results for the quarter. Revenue more than doubled to A$147.2 million from A$62.3 million in Q1 FY2025, driven by both increased production volumes and higher realized gold prices of A$4,896 per ounce (up from A$3,422 per ounce).

However, profitability declined substantially as costs increased:

Adjusted net profit fell to A$2.3 million in Q1 FY2026, down 79.6% from A$11.3 million in Q1 FY2025. All-in sustaining costs (AISC) rose to A$2,988 per gold equivalent ounce, a 38.5% increase from A$2,157 in the prior year period, reflecting industry-wide inflationary pressures and potentially integration costs following the merger.

Despite the profit decline, Alkane maintained a strong balance sheet with A$191 million in cash, bullion, and liquid investments at quarter-end, providing financial flexibility for future growth initiatives.

Strategic Initiatives & Growth Projects

Alkane outlined several strategic growth initiatives across its expanded portfolio. At Tomingley, the company is progressing with the Newell Highway Realignment to access the San Antonio open pits, while continuing underground mining at Roswell, Caloma 1, and Caloma 2. Exploration drilling is underway at the El Paso deposit, where significant gold intercepts have been reported.

The company’s most substantial growth opportunity is the Boda-Kaiser copper-gold project, which hosts a 14.7 million ounce gold equivalent resource. A scoping study completed in July 2024 demonstrated robust economics:

The study outlines a potential 20 million tonne per annum operation with a 17+ year mine life, producing approximately 159,000 ounces of gold and 35,000 tonnes of copper annually in the first five years. With an estimated pre-tax cash flow of A$8.2 billion and an internal rate of return of 36%, the project represents a significant long-term growth driver for Alkane.

Forward-Looking Statements

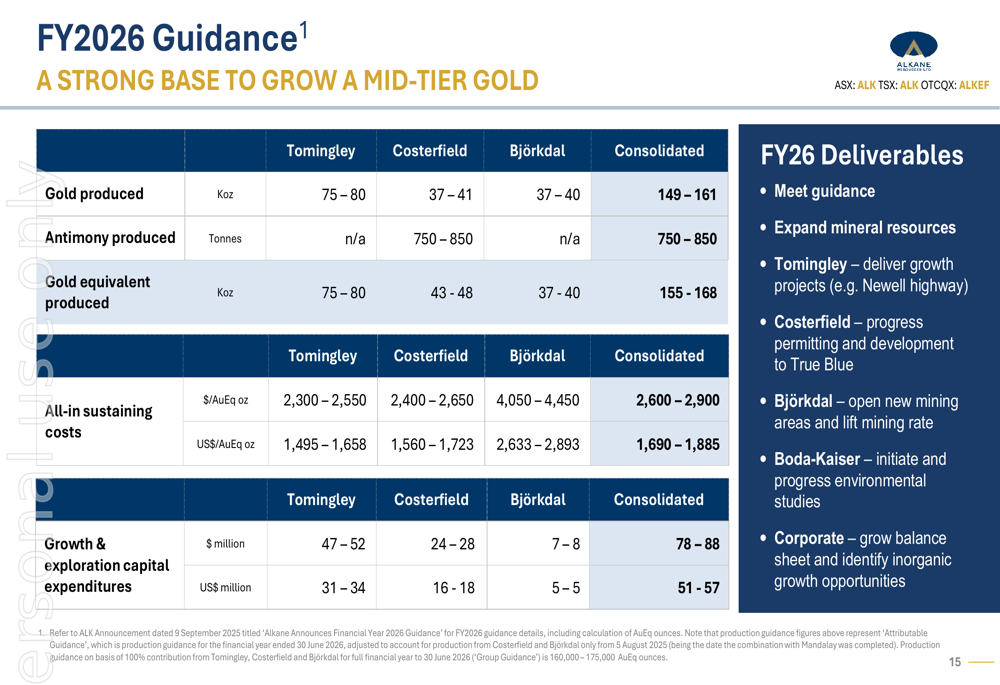

For FY2026, Alkane provided production guidance of 155,000-168,000 gold equivalent ounces at an AISC of A$2,600-2,900 per ounce. The company also plans to invest A$78-88 million in growth and exploration capital expenditures.

Management outlined key deliverables for FY2026, including expanding mineral resources, advancing growth projects at Tomingley, progressing permitting at Costerfield, lifting mining rates at Björkdal, and initiating environmental studies for the Boda-Kaiser project. The company also indicated it would seek inorganic growth opportunities to leverage its strengthened balance sheet.

"Our merger is delivering increased scale of operations, re-rating of the share price, stronger platform for growth, and new leadership," stated the company in its presentation, highlighting the strategic rationale behind the Mandalay Resources combination.

While the initial financial results show margin pressure, Alkane’s expanded production base, strong balance sheet, and significant growth projects position the company for potential long-term value creation as it works to optimize its newly expanded portfolio of assets.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.