Bitcoin price today: gains to $120k, near record high on U.S. regulatory cheer

Introduction & Market Context

Amentum Holdings LLC (NYSE:AMTM) presented its Q2 FY25 earnings results on May 7, 2025, reporting modest growth across key financial metrics while announcing a strategic divestiture to strengthen its balance sheet. The company’s stock closed at $22.11 on May 6, trading well below its 52-week high of $34.50, with pre-market trading on the day of the presentation indicating a further decline of 2.58% to $21.54.

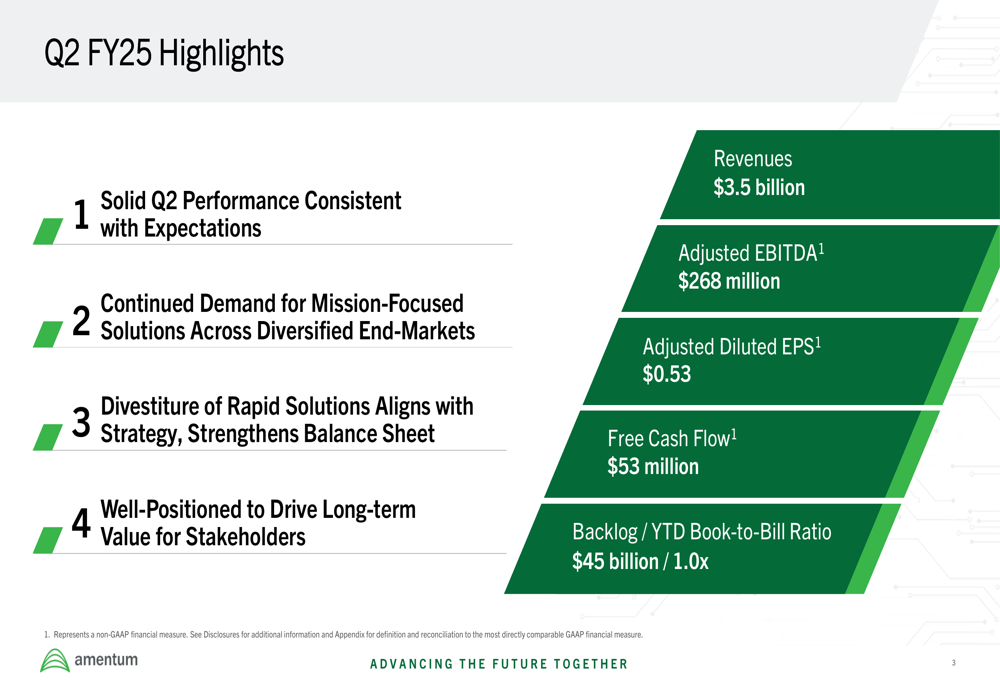

The defense and engineering services provider highlighted consistent performance in line with management expectations, supported by continued demand for its mission-focused solutions across diversified end-markets. The presentation emphasized Amentum’s position as a trusted partner with a capital-light business model and a global workforce of more than 53,000 employees.

Quarterly Performance Highlights

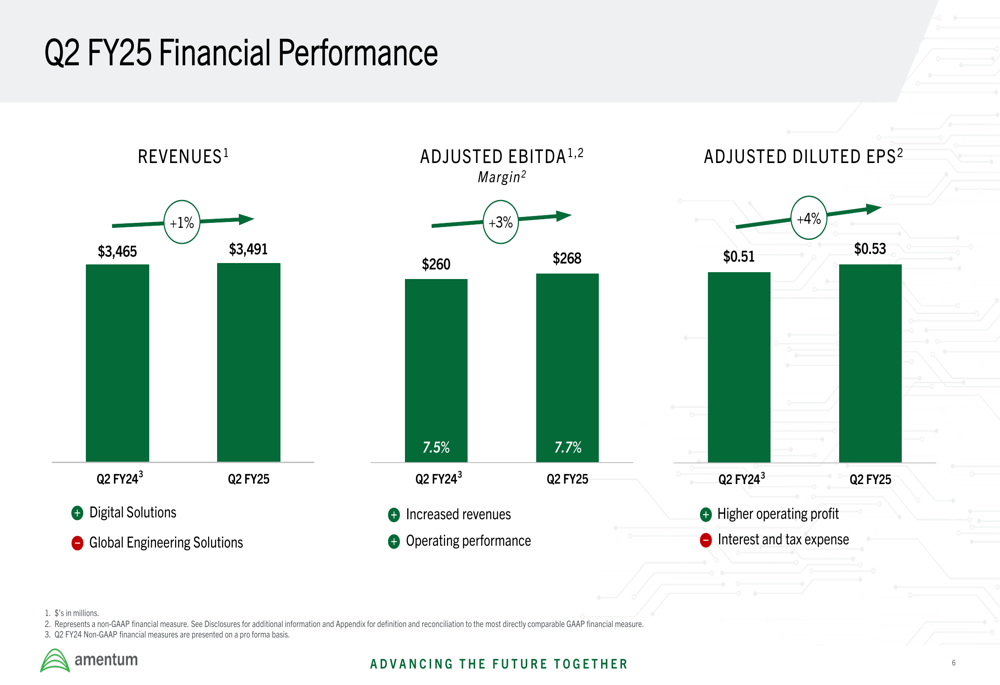

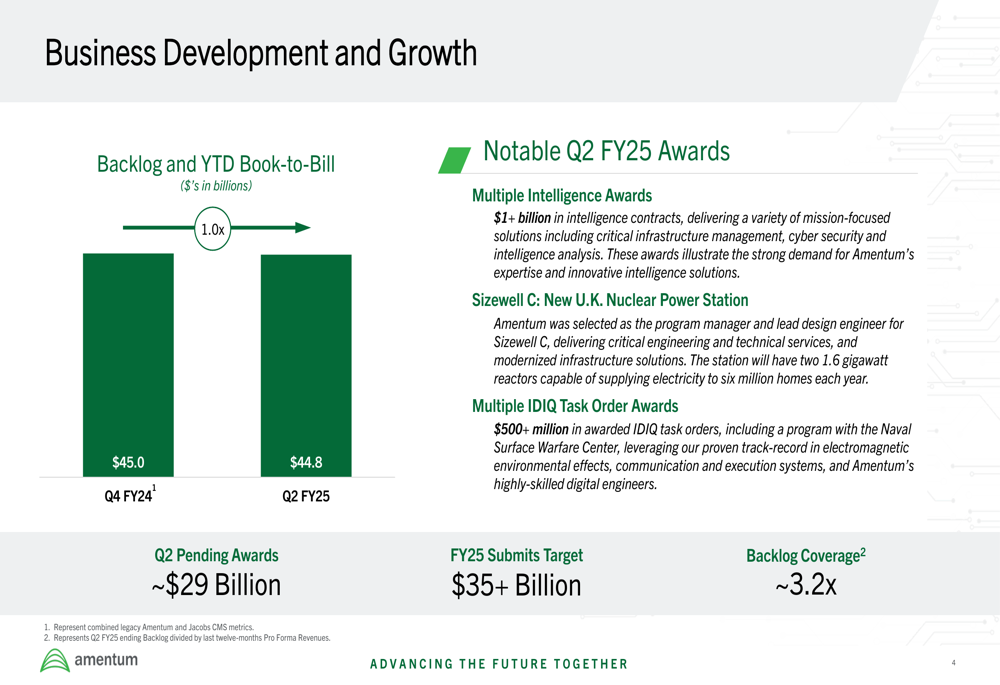

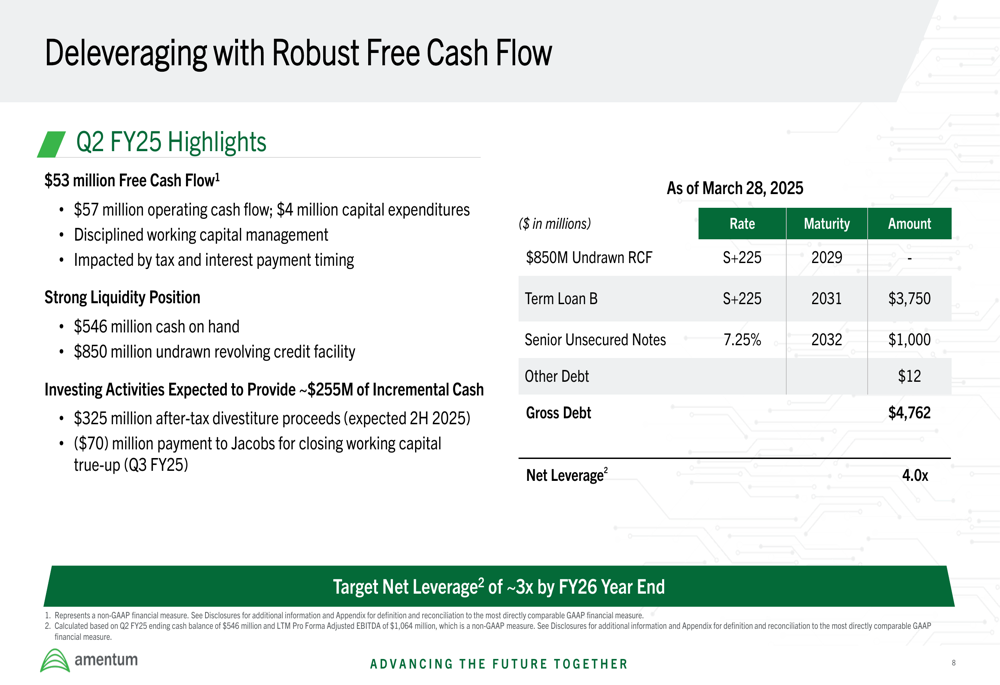

Amentum reported Q2 FY25 revenues of $3.5 billion, representing a 1% year-over-year increase on a pro forma basis. Adjusted EBITDA rose 3% to $268 million, while adjusted diluted EPS increased 4% to $0.53. Free cash flow for the quarter stood at $53 million, impacted by tax and interest payment timing according to management. The company maintained a solid backlog of $44.8 billion with a year-to-date book-to-bill ratio of 1.0x.

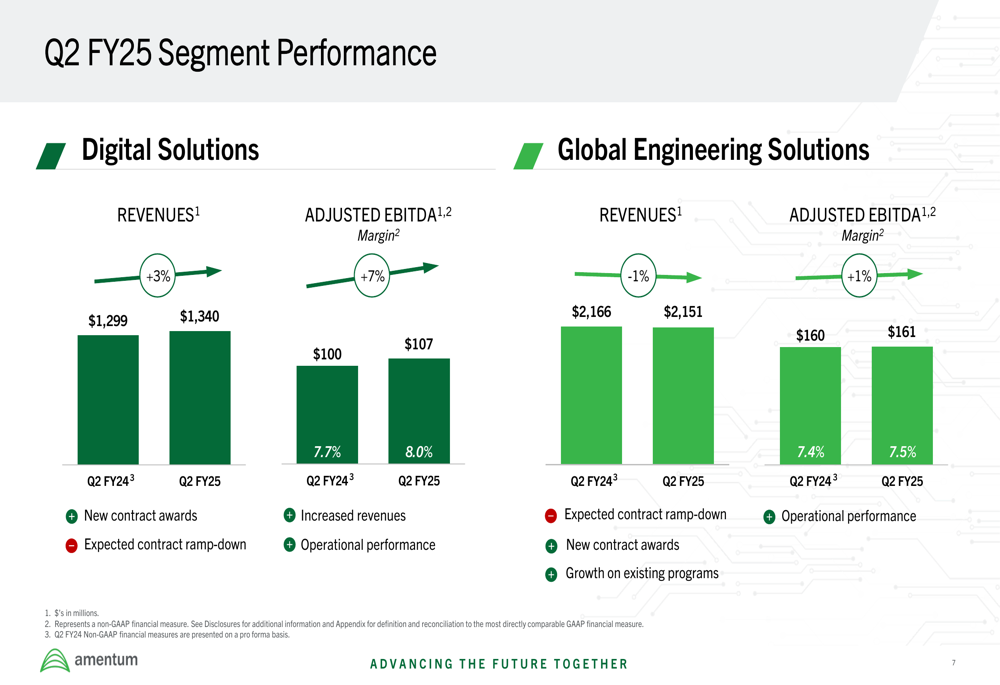

Performance varied across the company’s two main business segments. The Digital Solutions segment showed stronger growth, with revenues increasing 3% year-over-year to $1.34 billion and adjusted EBITDA rising 7% to $107 million. This segment achieved an adjusted EBITDA margin of 8.0%, benefiting from new contract awards and improved operational performance.

In contrast, the Global Engineering Solutions segment experienced a slight revenue decline of 1% year-over-year to $2.15 billion, while adjusted EBITDA increased 1% to $161 million. The segment posted an adjusted EBITDA margin of 7.5%, with management citing expected contract ramp-downs partially offset by new contract awards and growth on existing programs.

Strategic Initiatives

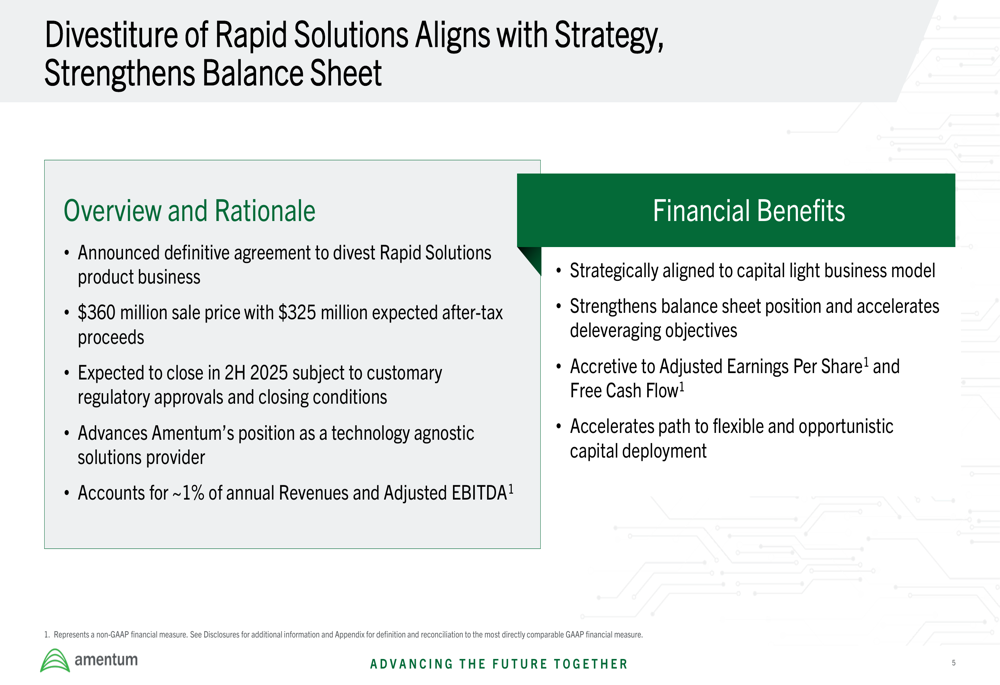

The most significant strategic development highlighted in the presentation was the announced divestiture of Amentum’s Rapid Solutions product business. The company has entered into a definitive agreement to sell this unit for $360 million, with expected after-tax proceeds of $325 million. The transaction is anticipated to close in the second half of 2025, subject to customary regulatory approvals and closing conditions.

Management emphasized that the divestiture aligns with Amentum’s positioning as a "technology agnostic solutions provider" and its capital-light business model. The Rapid Solutions business reportedly accounts for approximately 1% of annual revenues and adjusted EBITDA, suggesting minimal impact on the company’s core operations.

The presentation also highlighted several notable contract wins during the quarter, including multiple intelligence awards totaling over $1 billion, involvement in the Sizewell C nuclear power station project in the United Kingdom (TADAWUL:4280), and multiple IDIQ task order awards exceeding $500 million. The company reported pending awards of approximately $29 billion and a FY25 submits target of over $35 billion.

Balance Sheet & Deleveraging

Amentum emphasized its focus on deleveraging, with the Rapid Solutions divestiture playing a key role in this strategy. As of March 28, 2025, the company reported gross debt of $4.76 billion and a net leverage ratio of 4.0x. Management has set a target to reduce net leverage to approximately 3x by the end of FY26.

The company maintained a strong liquidity position with $546 million in cash on hand and an $850 million undrawn revolving credit facility. Management expects the Rapid Solutions divestiture to provide approximately $325 million in after-tax proceeds, partially offset by a $70 million payment to Jacobs for a closing working capital true-up in Q3 FY25, resulting in net incremental cash of approximately $255 million.

Outlook & Guidance

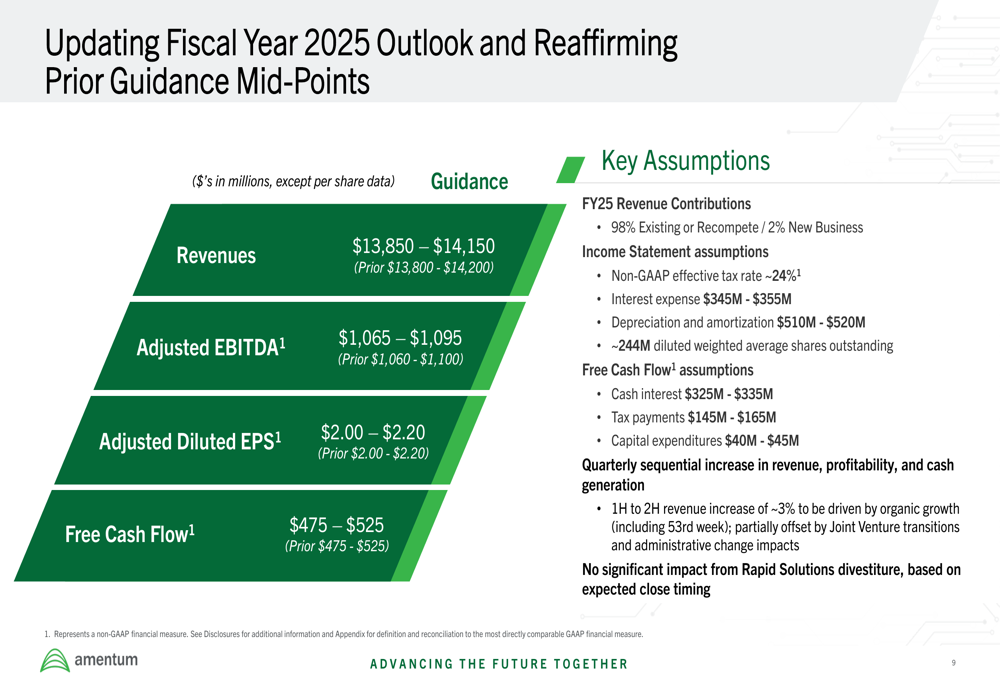

Amentum reaffirmed its fiscal year 2025 guidance while slightly narrowing the revenue range. The company now expects:

- Revenues of $13.85-14.15 billion (previously $13.8-14.2 billion)

- Adjusted EBITDA of $1.065-1.095 billion (previously $1.06-1.1 billion)

- Adjusted diluted EPS of $2.00-2.20 (unchanged)

- Free cash flow of $475-525 million (unchanged)

Management expects a quarterly sequential increase in revenue, profitability, and cash generation, with first half to second half revenue growth of approximately 3% driven by organic growth (including a 53rd week in the fiscal year), partially offset by joint venture transitions and administrative change impacts. The company noted that 98% of FY25 revenue is expected to come from existing or recompete business, with only 2% from new business.

Forward-Looking Statements

Looking beyond the current fiscal year, Amentum positioned itself as well-situated for long-term value creation, highlighting its differentiated scale, strong financial profile, and disciplined capital deployment strategy. Management emphasized the company’s full life cycle capabilities in growing markets and its capital-light business model as key advantages.

The presentation suggested that following the completion of the deleveraging initiative, Amentum would shift toward a more flexible and opportunistic capital deployment approach to drive sustained value creation for stakeholders. However, specific details on potential future acquisitions, share repurchases, or dividend policies were not provided.

In summary, Amentum’s Q2 FY25 presentation depicted a company with modest but steady growth, making strategic moves to strengthen its balance sheet while maintaining a solid backlog of business. The Rapid Solutions divestiture represents a significant step in the company’s deleveraging journey, with management expressing confidence in accelerating performance in the second half of the fiscal year.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.