Berkshire Hathaway reveals $4.3 billion stake in Alphabet, cuts Apple

Introduction & Market Context

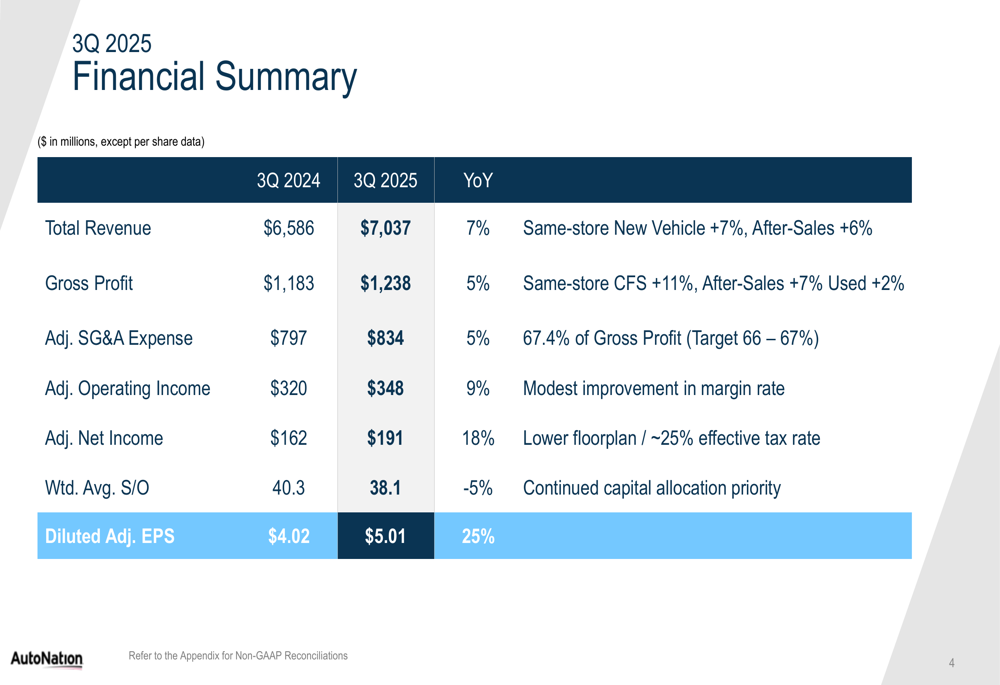

AutoNation Inc (NYSE:AN) released its third quarter 2025 earnings presentation on October 23, 2025, revealing strong financial performance despite facing market headwinds. The automotive retailer reported a 25% year-over-year increase in adjusted earnings per share, significantly outpacing revenue growth of 7%.

Despite the strong results that beat analyst expectations, AutoNation’s stock fell 3.33% in pre-market trading to $216.44, suggesting investors may have concerns about broader market conditions or margin pressures in certain segments.

Quarterly Performance Highlights

AutoNation delivered robust financial results across key metrics in Q3 2025. The company reported total revenue of $7.04 billion, up 7% from $6.59 billion in the same period last year, exceeding the forecast of $6.8 billion.

Adjusted net income reached $191 million, an 18% increase from $162 million in Q3 2024. This translated to diluted adjusted earnings per share of $5.01, up 25% from $4.02 a year ago and surpassing analyst expectations of $4.84.

The company’s ability to grow EPS at a faster rate than revenue highlights its operational efficiency and strategic capital allocation, including a 5% reduction in weighted average shares outstanding year-over-year.

As shown in the following financial summary from the presentation:

Segment Performance Analysis

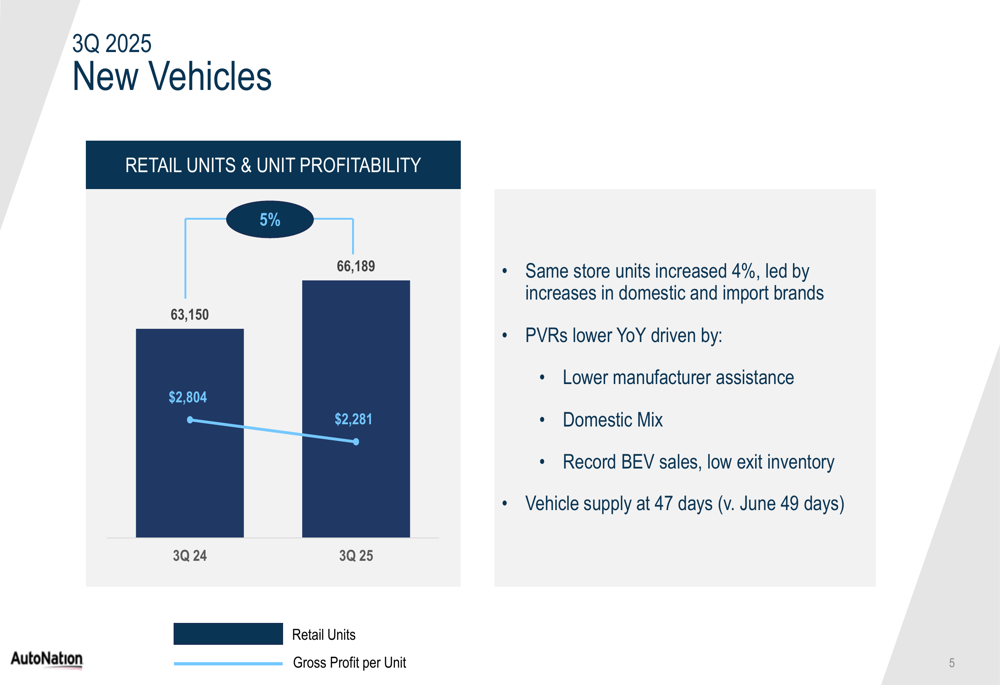

AutoNation’s new vehicle segment showed mixed results, with same-store unit sales increasing by 4%, led by double-digit growth in domestic brands and record battery electric vehicle (BEV) sales. However, gross profit per vehicle retailed (PVR) declined from $2,804 in Q3 2024 to $2,281 in Q3 2025, driven by lower manufacturer assistance, changing product mix, and low exit inventory.

The following chart illustrates this dynamic between volume growth and PVR pressure:

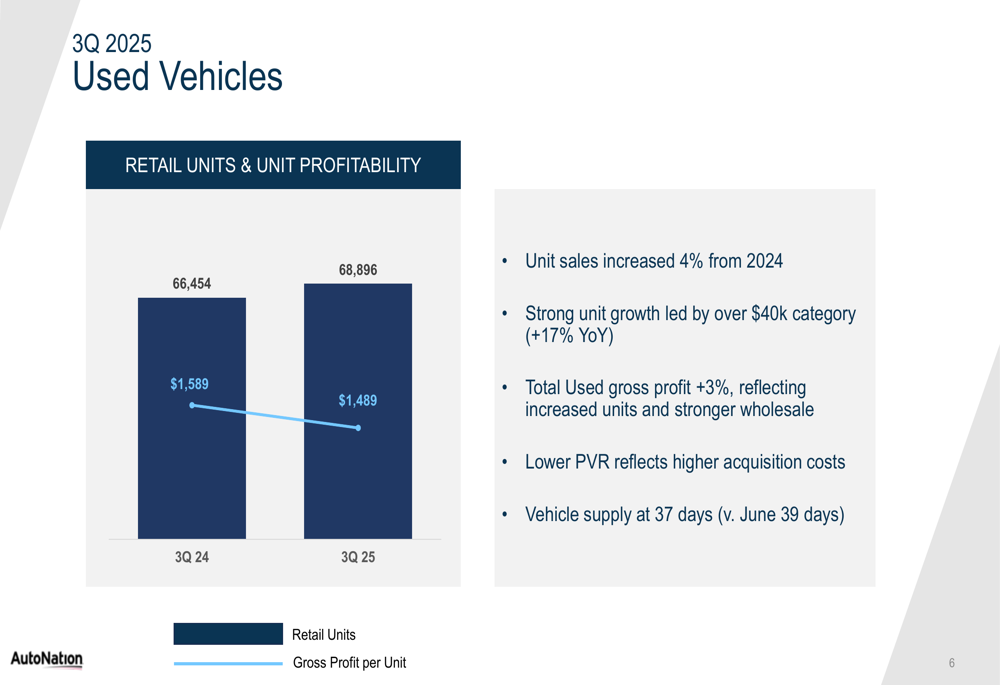

In the used vehicle segment, retail units increased by 4% year-over-year, with particularly strong growth in vehicles priced over $40,000, which saw a 17% increase. Total used vehicle gross profit grew 3%, benefiting from increased units and stronger wholesale performance, though PVR declined slightly from $1,589 to $1,489 due to higher acquisition costs.

The used vehicle performance metrics are detailed in this chart:

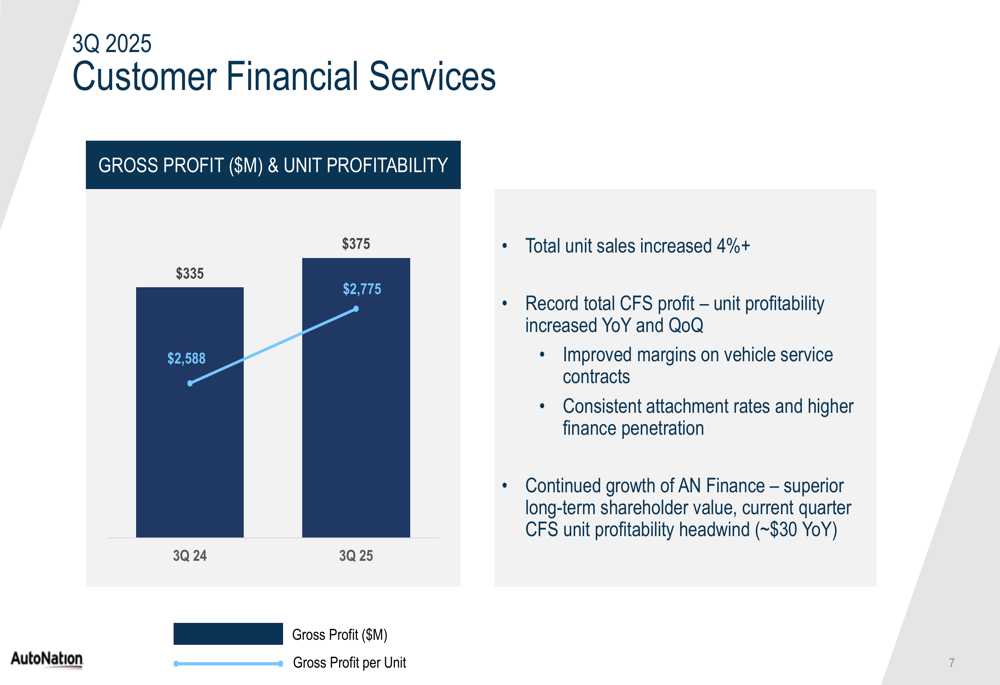

Customer Financial Services (CFS) was a standout performer, with gross profit increasing 11% on a same-store basis to $375 million. Unit profitability improved both year-over-year and quarter-over-quarter to $2,775 per unit, driven by improved margins on vehicle service contracts and higher finance penetration.

The following chart demonstrates the strong CFS performance:

After-sales operations also delivered solid results, with same-store revenue and gross profit growth of 6% and 7% respectively. Growth was led by customer pay, internal, and warranty services, supported by increased repair order count, higher value per repair order, and expanded technician headcount. The gross profit margin improved by 100 basis points to 48.7%.

AutoNation Finance Growth

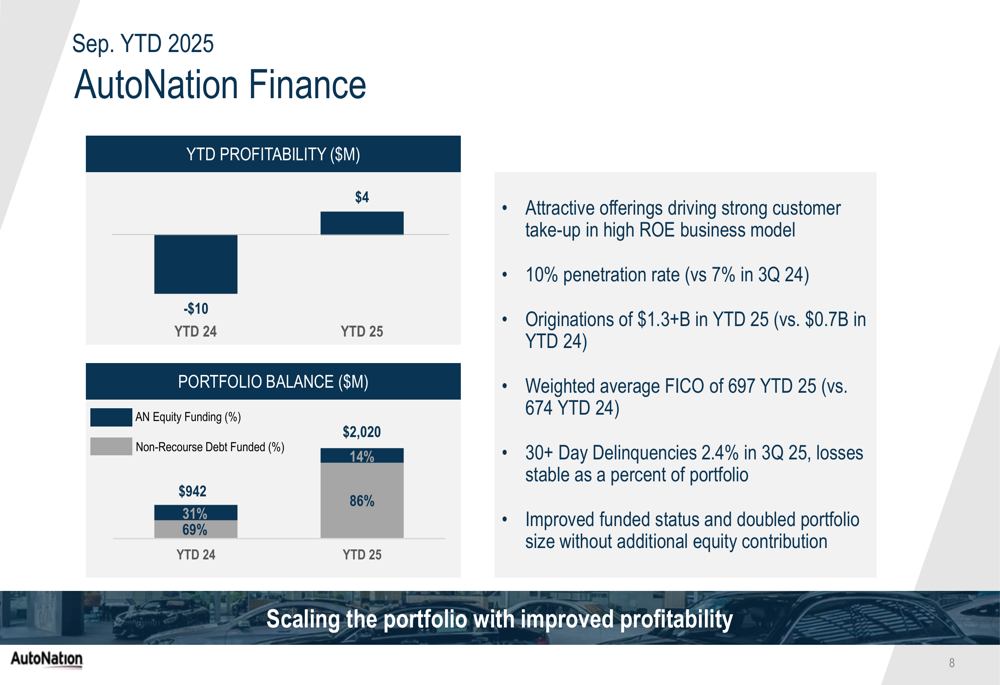

A notable highlight from the presentation was the significant growth and improved profitability of AutoNation Finance. The company’s captive finance arm has more than doubled its portfolio size year-over-year to over $2 billion, while turning profitable with year-to-date earnings of $4 million compared to a $10 million loss in the same period last year.

Customer penetration increased to 10% from 7% a year ago, with originations of over $1.3 billion year-to-date compared to $700 million in the prior year period. The credit quality of the portfolio has also improved, with the weighted average FICO score increasing to 697 from 674 last year, while 30+ day delinquencies remained low at 2.4%.

The company has also optimized its funding structure, reducing equity funding from 31% to 14% of the portfolio while increasing non-recourse debt funding to 86%, as illustrated in the following chart:

Capital Allocation & Cash Flow

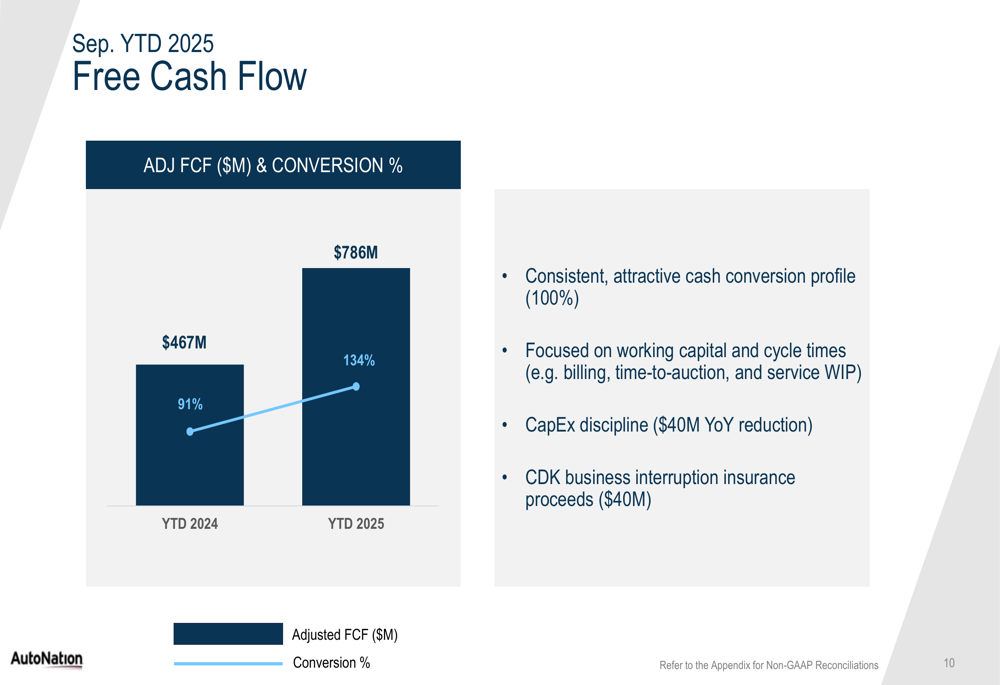

AutoNation demonstrated strong cash flow generation and disciplined capital allocation during the first nine months of 2025. Adjusted free cash flow reached $786 million, representing a 134% conversion rate of adjusted net income, a significant improvement from $467 million and 91% conversion in the same period last year.

This impressive cash flow performance was driven by focused working capital management, reduced capital expenditures, and $40 million in insurance proceeds related to a prior cybersecurity incident.

The following chart illustrates the company’s free cash flow performance:

The company deployed $1.01 billion in capital year-to-date, allocating $435 million to share repurchases at an average price of $183, $348 million to acquisitions, and $223 million to capital expenditures. This balanced approach to capital deployment reflects AutoNation’s commitment to returning value to shareholders while investing in strategic growth opportunities.

As shown in the capital allocation summary:

Forward-Looking Statements

Looking ahead, AutoNation emphasized its strong positioning in the evolving automotive landscape. The company maintains a healthy balance sheet with leverage of 2.35x, below the mid-point of its target range and improved from 2.45x at the end of 2024.

During the earnings call, CEO Mike Manley highlighted the company’s strong financial performance, stating, "We delivered 25% adjusted EPS growth, generated strong cash flow." The company expects an improved vehicle mix in Q4, with anticipated strength in the premium luxury segment.

However, investors should note potential challenges, including margin pressures from increased BEV and domestic vehicle sales, potential impacts from evolving tariffs, and economic conditions affecting consumer spending on vehicles.

Despite these challenges, AutoNation’s diversified business model, growing finance portfolio, and disciplined capital allocation strategy position the company to navigate the changing automotive retail environment effectively.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.