LATAM Airlines pilots in Chile to begin strike at midnight Wednesday

Bandwidth Inc (NASDAQ:BAND) reported mixed third-quarter 2025 results on October 30, showing solid revenue growth but falling short of earnings expectations. The cloud communications provider saw its stock drop 6.2% following the announcement, despite initially positive pre-market trading.

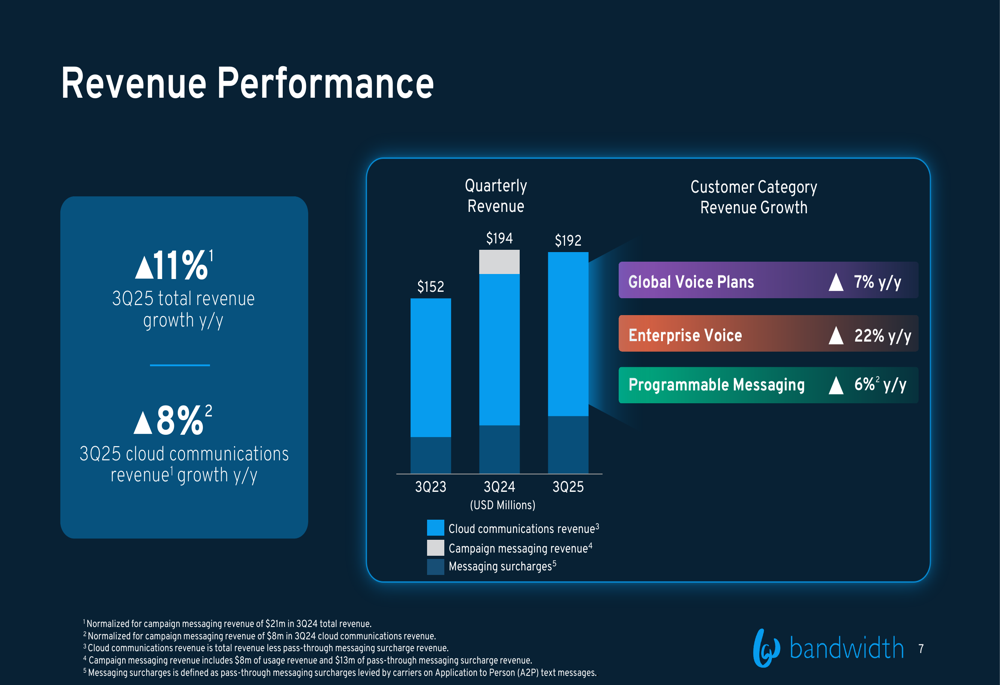

Quarterly Performance Highlights

Bandwidth delivered total revenue of $192 million for Q3 2025, representing an 11% year-over-year increase and exceeding analyst expectations of $189.91 million. However, the company posted earnings per share of $0.36, missing the forecasted $0.37.

Cloud communications revenue, which forms the core of Bandwidth’s business, grew 8% year-over-year to $142 million. The company maintained a non-GAAP gross margin of 58%, unchanged from the same quarter last year but improved from 55% in Q3 2023.

As shown in the following chart of quarterly revenue performance:

The company’s performance varied across its three main customer categories, with Enterprise Voice showing particularly strong momentum at 22% year-over-year growth. Global Voice Plans grew by 7%, while Programmable Messaging increased by 6%.

Customer Relationships and Loyalty

Bandwidth highlighted its strong customer relationships as a key business strength. The company maintains impressive retention metrics, including a name retention rate exceeding 99% and a net retention rate of 107% (excluding political campaign benefits).

The following slide illustrates these customer loyalty metrics:

The company’s customer base includes major technology and enterprise clients across various segments. Global Voice Plans customers include Microsoft, Google, Zoom, and Cisco, while Enterprise Voice serves companies like Uber, Southwest, and DocuSign.

As shown in this customer category breakdown:

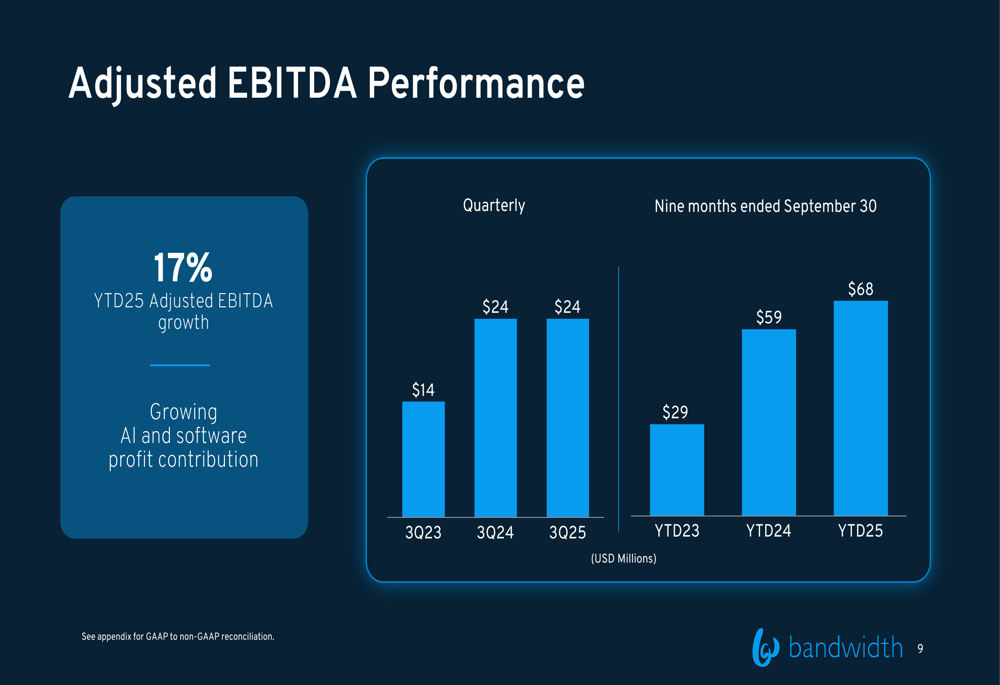

Financial Performance and Profitability

While quarterly revenue showed strong growth, Bandwidth’s adjusted EBITDA for Q3 2025 remained flat year-over-year at $24 million. However, on a year-to-date basis, adjusted EBITDA reached $68 million, representing a 17% increase over the same period in 2024.

The following chart illustrates this EBITDA performance:

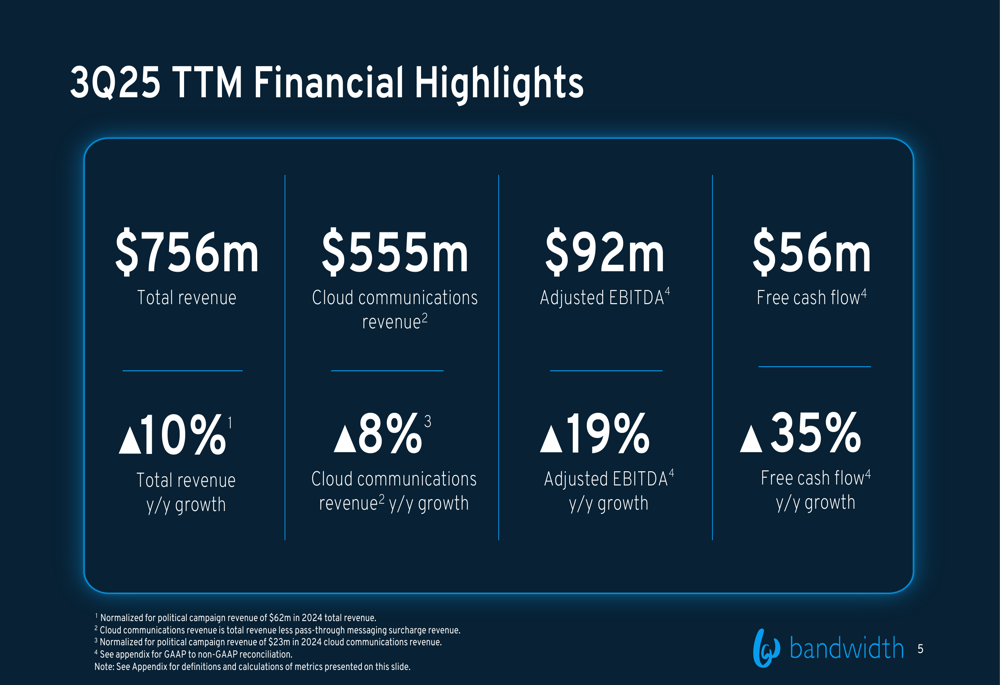

Free cash flow for the quarter was $13 million, slightly down from $14 million in Q3 2024. The company attributed this to "timing and network investments" according to its presentation. On a trailing twelve-month basis, however, free cash flow showed strong 35% year-over-year growth, reaching $56 million.

The company’s overall financial highlights for the trailing twelve months ending Q3 2025 show consistent growth across key metrics:

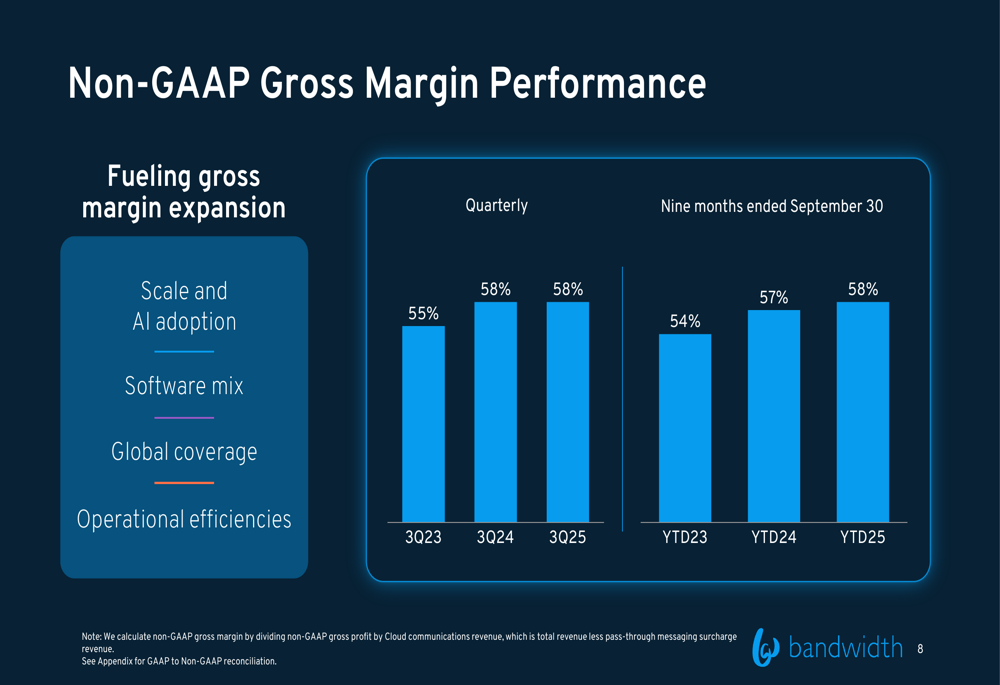

Strategic Focus on AI Integration

Bandwidth emphasized its growing focus on artificial intelligence throughout its presentation. The company noted that AI voice usage is increasing among its customers and that AI adoption is contributing to gross margin expansion.

"AI is not a standalone product for Bandwidth. It’s integrated throughout our cloud and embedded in the services our customers use every day," stated Daryl Raiford, CFO, according to the earnings call transcript.

The company’s non-GAAP gross margin performance has benefited from several factors, including scale and AI adoption:

Forward Guidance and Outlook

Bandwidth raised its full-year 2025 adjusted EBITDA guidance to a range of $89-$92 million. The company maintained its revenue guidance at $747-$760 million, representing approximately 10% year-over-year growth.

When adjusting for the expected cyclical reduction in political campaign messaging activity, the company projects 9-11% year-over-year revenue growth.

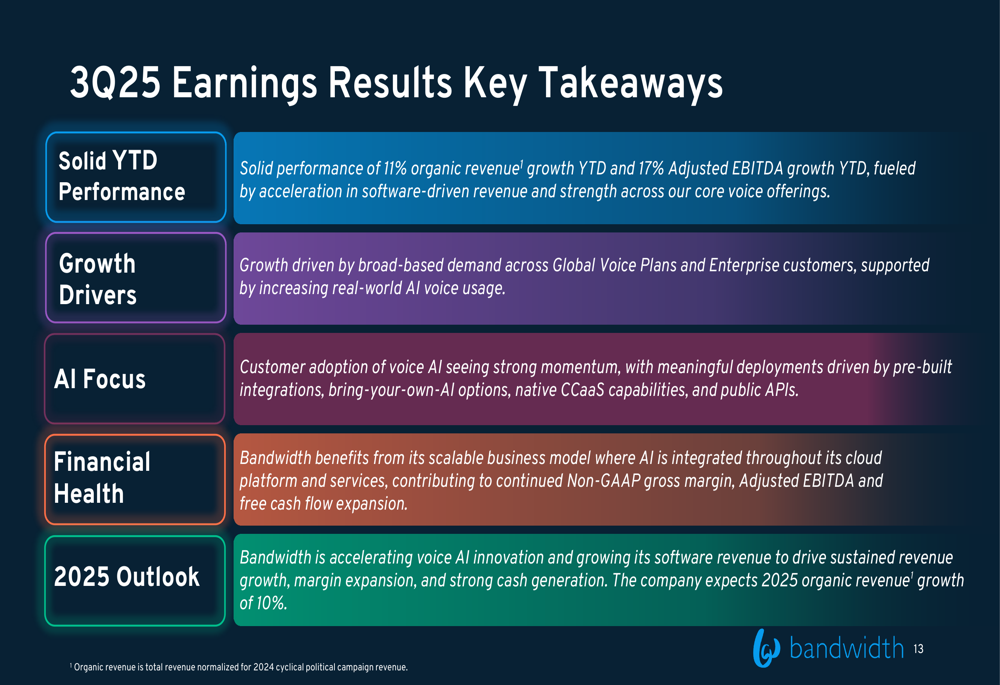

The key takeaways from Bandwidth’s Q3 2025 results highlight both achievements and ongoing strategic initiatives:

Market Context and Challenges

Despite the revenue beat and raised EBITDA guidance, Bandwidth’s stock declined 6.2% following the earnings release, with the price falling to $15.73 from the previous close of $16.77. This reaction suggests investors may have focused on the EPS miss and potentially on concerns about the slight decline in quarterly free cash flow.

The company faces several challenges, including intense competition in the AI and cloud communications space, which could pressure margins. Additionally, economic uncertainties may affect enterprise spending on communication solutions, while rapid technological advancements require continuous innovation and investment.

Nevertheless, Bandwidth’s strong customer retention metrics and growing enterprise voice segment indicate the company has established a solid foundation for future growth as it continues to integrate AI capabilities throughout its service offerings.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.