60%+ returns in 2025: Here’s how AI-powered stock investing has changed the game

Introduction & Market Context

BBVA Argentina (NYSE:BBAR) presented its third-quarter 2025 results on November 26, revealing a significant decline in profitability despite growth in both loans and deposits. The bank’s stock closed up 5.56% at $14.38 following the presentation, suggesting investors may be focusing on market share gains and digital transformation progress rather than the immediate earnings challenges.

The results come amid a complex economic environment in Argentina, with the bank facing rising loan delinquencies and increased provisioning needs. Despite these headwinds, BBVA Argentina maintained its market share growth trajectory, with private deposits market share crossing the 10% threshold.

Quarterly Performance Highlights

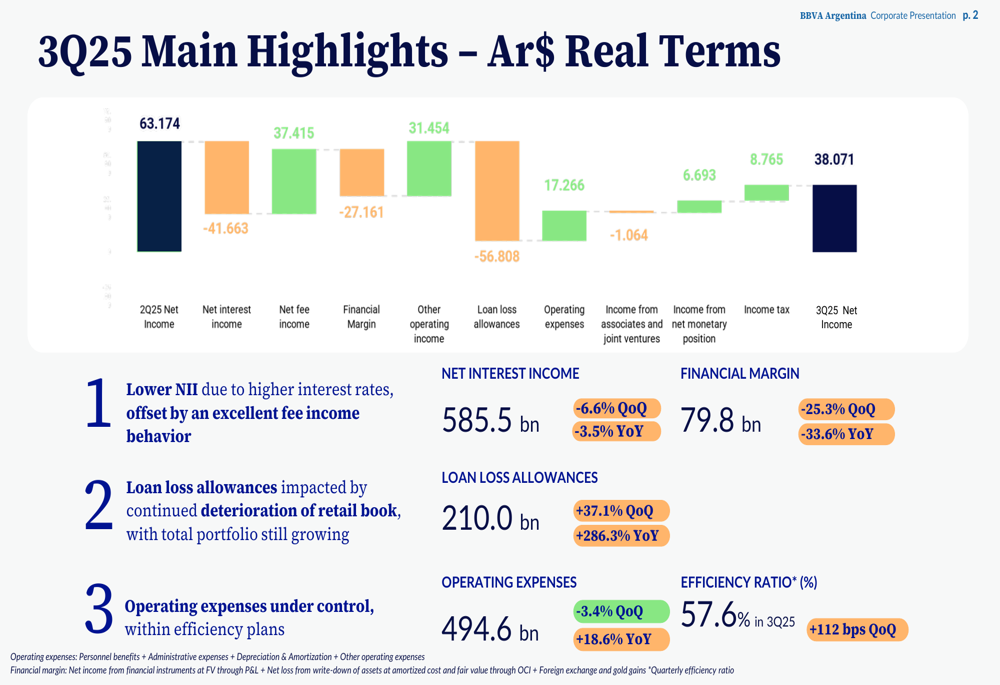

BBVA Argentina reported net income of AR$ 38.1 billion for Q3 2025, representing a steep 40% year-over-year decline and a 46% drop from the previous quarter. This performance resulted in an EPS of $0.5049, missing analyst forecasts of $0.6 by 15.85%.

The bank’s profitability metrics showed a concerning downward trend, with return on assets (ROA) falling to 1.2% quarterly (0.7% annualized) and return on equity (ROE) dropping to 8.0% quarterly, with an annualized figure turning negative at -4.7%.

As shown in the following chart of profitability indicators, the bank has experienced a consistent decline in earnings over the past year:

Net interest income decreased to AR$ 585.5 billion, down 6.6% quarter-over-quarter and 3.5% year-over-year. The bank attributed this decline to higher interest rates, though it was partially offset by strong fee income performance. Operating expenses showed improvement, decreasing 3.4% quarter-over-quarter to AR$ 494.6 billion, reflecting the company’s focus on cost control.

The following waterfall chart illustrates the main drivers behind the quarterly performance decline:

The efficiency ratio deteriorated slightly to 57.6% in Q3 2025, up 112 basis points from the previous quarter. However, the fees-to-expenses ratio showed significant improvement, reaching 37.3% in Q3 2025 compared to 26.3% in the previous quarter, indicating the bank’s success in generating non-interest income to offset expenses.

Asset Quality and Risk Management

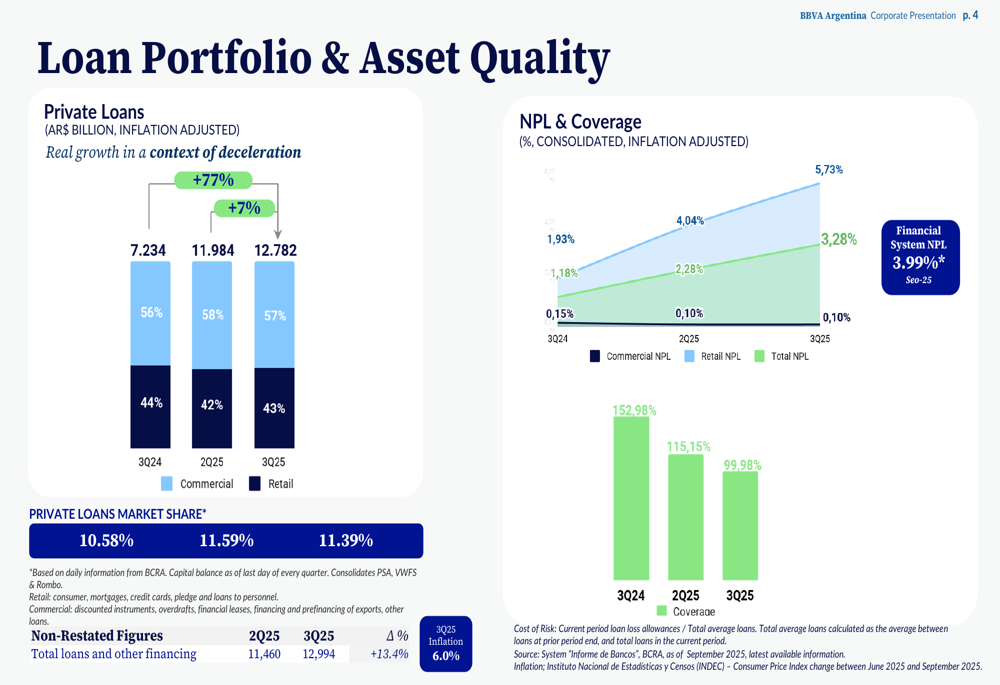

A key concern emerging from the presentation was the deterioration in asset quality. Loan loss allowances surged to AR$ 210.0 billion, representing a 37.1% increase quarter-over-quarter and a dramatic 286.3% rise year-over-year. This significant increase reflects ongoing challenges in the retail loan book.

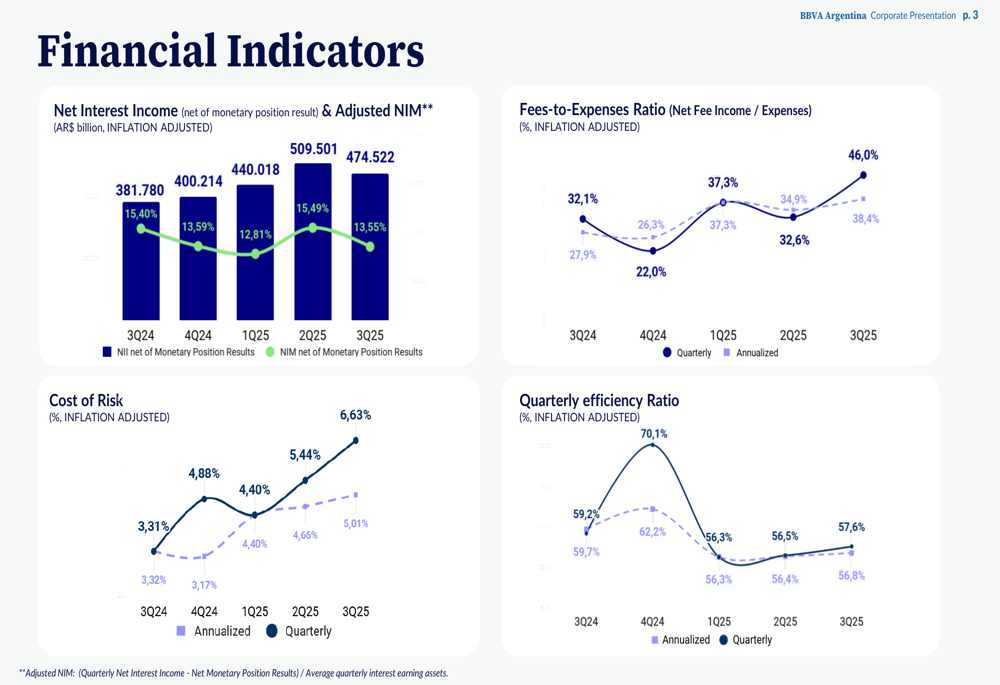

The cost of risk continued its upward trajectory, reaching 5.01% in Q3 2025, up from 4.40% in the previous quarter and 3.31% a year earlier. This trend suggests increasing pressure on the bank’s loan portfolio quality.

As illustrated in the following chart, key financial indicators show mixed performance, with cost of risk being a particular area of concern:

The non-performing loan (NPL) ratio nearly doubled to 2.28% in Q3 2025 from 1.18% in Q2 2025, while the coverage ratio declined to 99.98% from 115.15% in the previous quarter. This combination of rising delinquencies and lower coverage could signal potential challenges ahead if the trend continues.

The loan portfolio composition and asset quality metrics are visualized in the following chart:

Liquidity, Capital Position, and Market Share

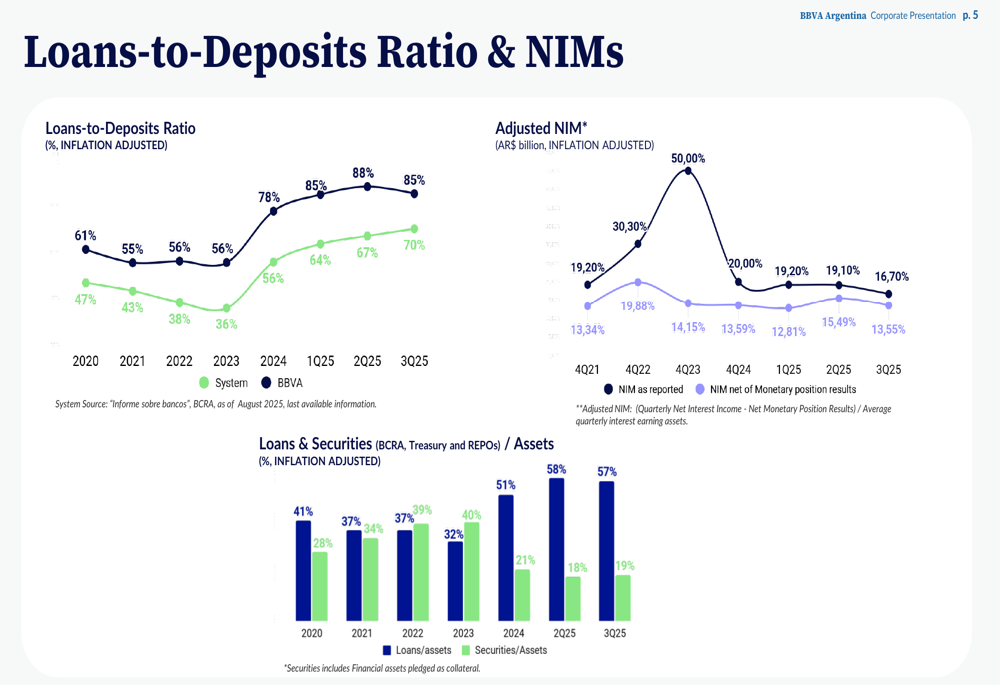

BBVA Argentina’s loans-to-deposits ratio stood at 85% in Q3 2025, slightly down from 88% in the previous quarter but significantly higher than the 61% reported in 2020. This indicates the bank is deploying more of its deposit base into lending activities, potentially improving net interest margins but also increasing risk exposure.

The bank’s capital ratio continued its downward trend, reaching 16.70% in Q3 2025 compared to 18.40% in the previous quarter. While still well above regulatory requirements, this declining trend bears watching, especially given the challenging economic environment.

The following chart illustrates the evolution of the bank’s loans-to-deposits ratio and net interest margins:

On a positive note, BBVA Argentina continued to gain market share in both loans and deposits. Private deposits market share increased to 10.09% in Q3 2025 from 9.65% in the previous quarter and 8.53% a year earlier. Similarly, private loans market share stood at 11.39%, slightly down from 11.59% in Q2 but still higher than the 10.58% reported a year ago.

The composition of deposits and capital requirements are shown in the following chart:

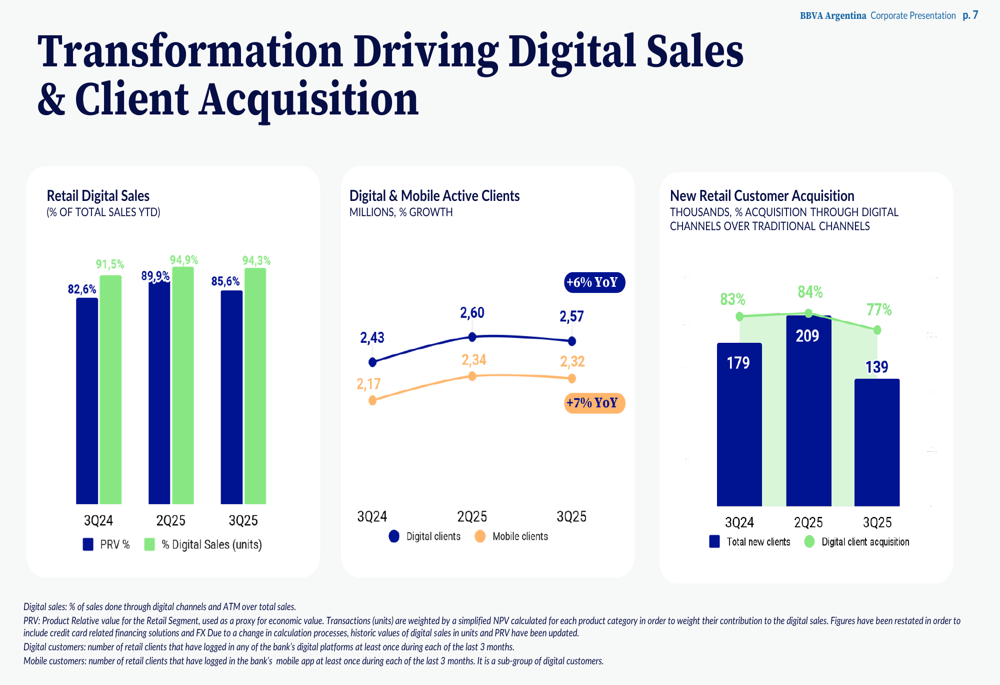

Digital Transformation Progress

A bright spot in BBVA Argentina’s presentation was the continued progress in digital transformation. The bank reported steady growth in digital sales, mobile active clients, and new customer acquisition through digital channels.

The digital transformation metrics provide a forward-looking indicator of the bank’s ability to compete effectively in an increasingly digital banking landscape while potentially reducing branch-related expenses over time.

As illustrated in the following chart, digital transformation is driving sales and client acquisition:

Forward Outlook

Despite the earnings miss and declining profitability, BBVA Argentina’s management maintains a positive outlook. According to the earnings call, the bank expects loan growth of 45-50% and deposit growth of 30-35% in real terms, suggesting confidence in continued business expansion despite economic challenges.

Management anticipates a capital ratio of around 17% by year-end and expects improvements in non-performing loans and cost of risk in 2026. CFO Carmen Morillo Arroyo expressed optimism about future performance, stating, "2026 will be better than this year, maybe not at a sustainable pace. The trend should go upwards."

However, investors should remain cautious given the significant deterioration in asset quality and rising cost of risk. The bank faces several challenges, including political uncertainty, restrictive monetary policy by the Central Bank, potential currency volatility, and maintaining growth in a competitive market with rising deposit rates.

BBVA Argentina’s ability to navigate these challenges while continuing its digital transformation and market share growth will be critical to its performance in the coming quarters.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.