Texas Roadhouse earnings missed by $0.05, revenue topped estimates

Introduction & Market Context

Blackstone Mortgage Trust (NYSE:BXMT) presented its second quarter 2025 results on July 30, showing signs of portfolio growth after previous contractions, continued progress on impaired loan resolutions, and further strategic shift away from office properties. The commercial mortgage REIT, which currently offers a 9.7% dividend yield, reported modest GAAP earnings while highlighting stronger distributable earnings before charge-offs.

The stock was trading down 0.83% in premarket activity at $19.21, reflecting cautious investor sentiment despite the company’s progress on strategic initiatives. BXMT shares have traded between $16.51 and $21.24 over the past 52 weeks.

Quarterly Performance Highlights

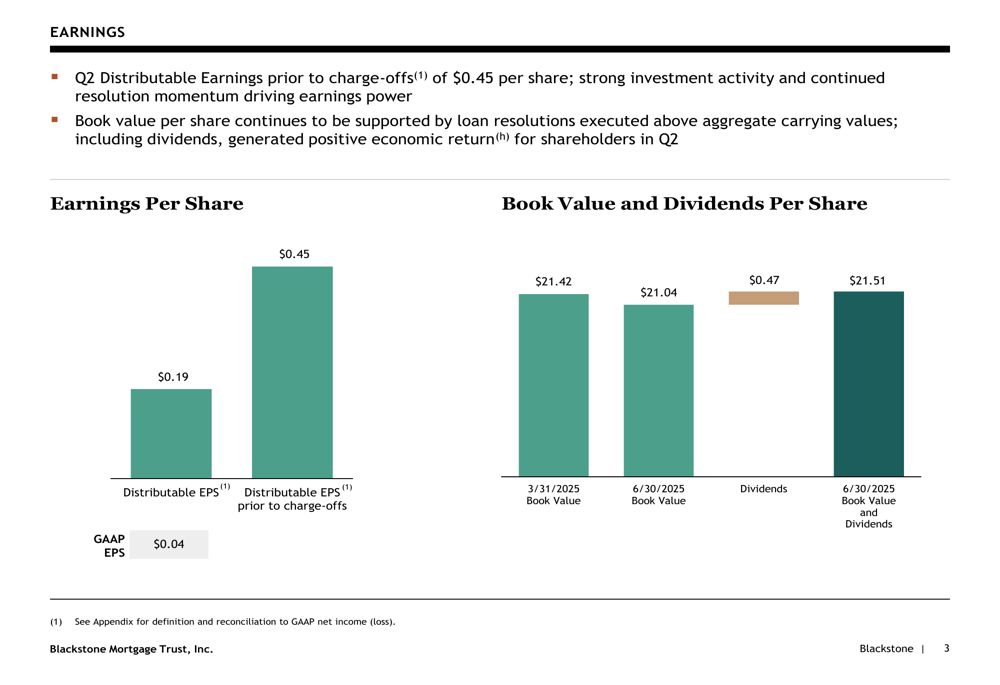

Blackstone Mortgage Trust reported GAAP earnings per share of $0.04 for Q2 2025, a significant improvement from the $(0.00) reported in Q1 and the $(0.35) from the same quarter last year. Distributable earnings came in at $0.19 per share, up from $0.17 in the previous quarter. Before charge-offs, distributable earnings reached $0.45 per share.

The company maintained its quarterly dividend at $0.47 per share, representing an annualized yield of 9.7% based on recent share prices. Book value per share stood at $21.04 as of June 30, 2025, which includes $4.39 per share of CECL reserves. This represents a slight decrease from the $21.42 reported at the end of Q1.

As shown in the following chart of earnings and book value performance:

Portfolio Strategy and Composition

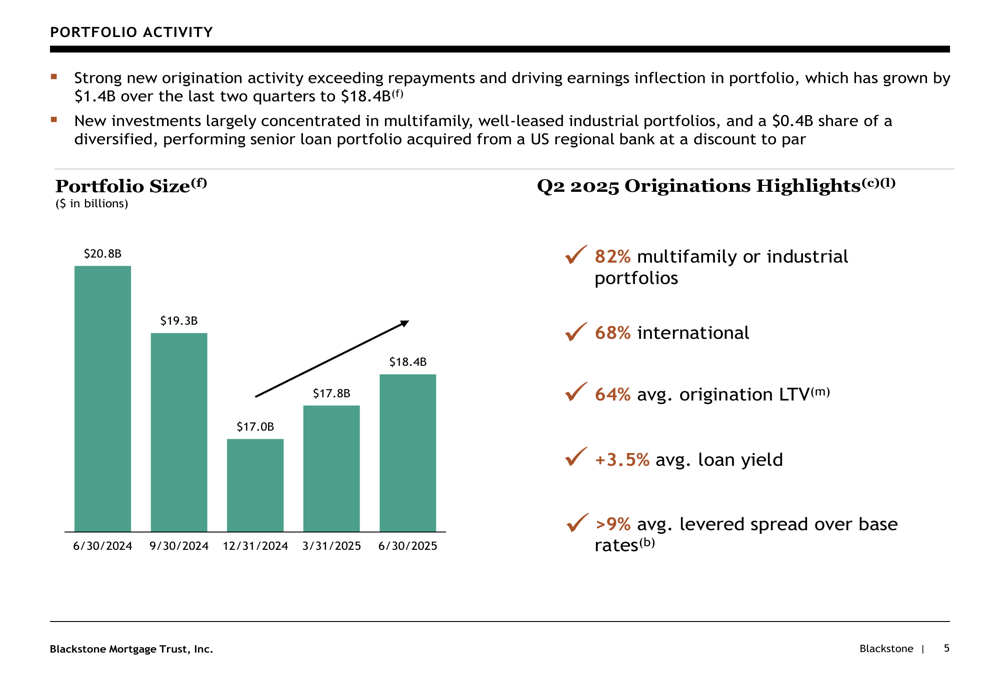

BXMT’s loan portfolio grew to $18.4 billion across 144 loans by quarter-end, representing an increase of $1.4 billion over the past two quarters. This growth follows a period of portfolio contraction, as the company had reduced its portfolio from $20.8 billion in June 2024 to $17.0 billion by December 2024.

The company originated $2.2 billion in new loans during Q2 while collecting $1.6 billion in repayments. Notably, 82% of new originations were secured by multifamily or diversified industrial portfolios, and 68% were sourced internationally. The company also acquired a $0.4 billion share of a performing senior loan portfolio from a U.S. regional bank at a discount to par, primarily concentrated in neighborhood retail, multifamily, and industrial sectors.

The portfolio growth trajectory and composition is illustrated in this chart:

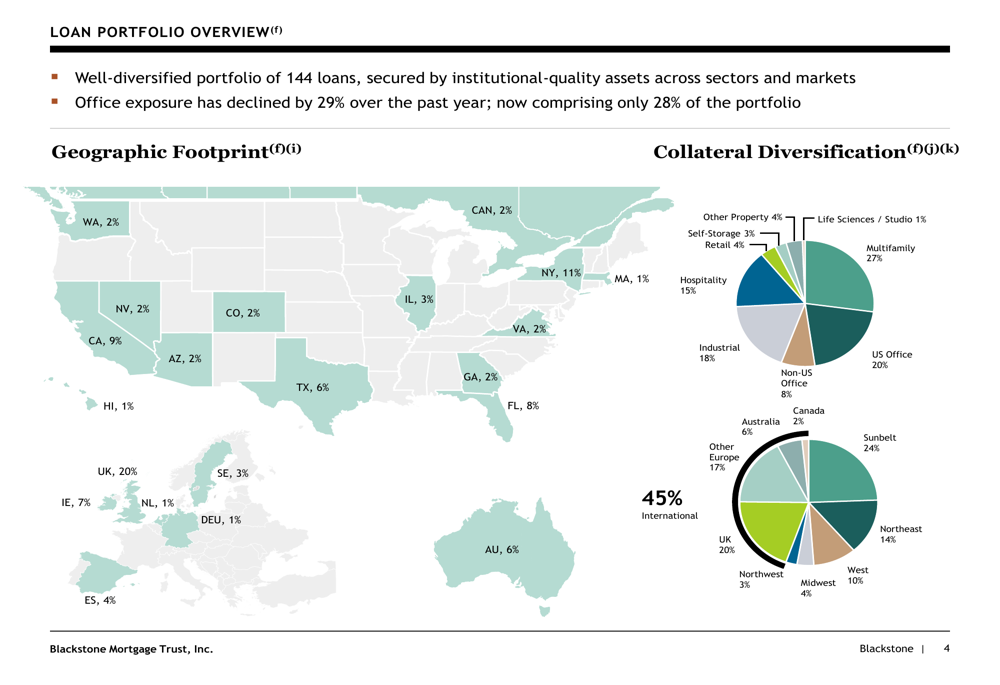

BXMT continues to diversify its portfolio both geographically and by property type. The company has reduced its office exposure from 36% to 28% of the loan portfolio over the past twelve months, with $0.3 billion of office repayments in Q2 alone. Meanwhile, multifamily properties now represent 27% of the portfolio, with industrial at 18%.

The geographic footprint shows significant international diversification, with 45% of loans outside the U.S. The United Kingdom (TADAWUL:4280) represents the largest international exposure at 20% of the portfolio.

The following image shows the detailed breakdown of the portfolio by geography and property type:

Credit Quality and Impaired Loan Resolution

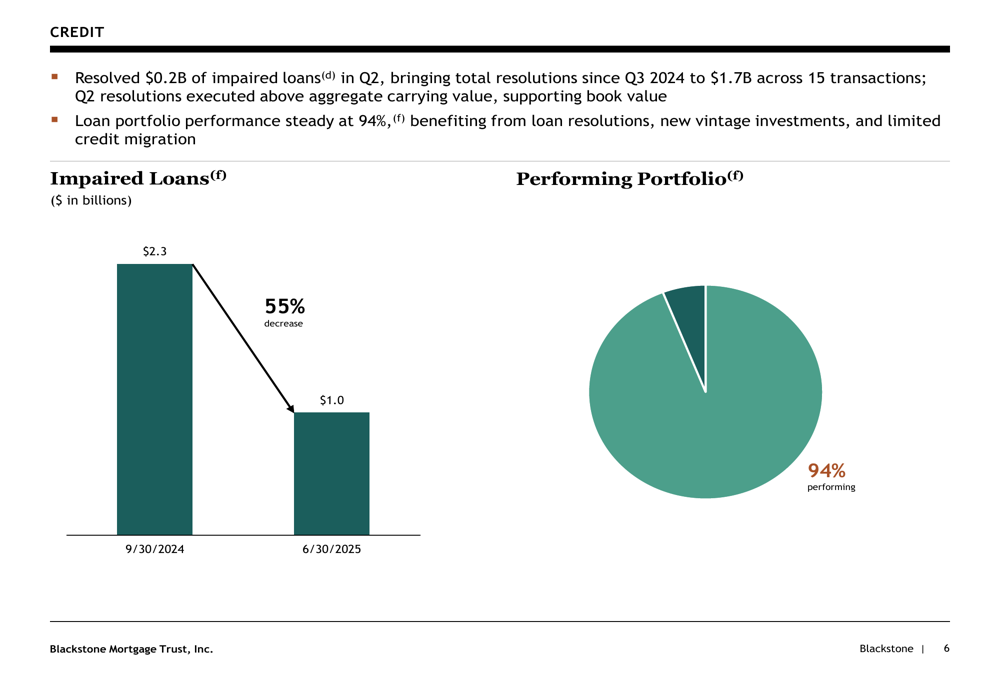

A key focus for BXMT has been resolving impaired loans, and the company reported continued progress in this area. During Q2, the company resolved $0.2 billion of impaired assets at values above their aggregate carrying value. Since Q3 2024, total resolutions have reached $1.7 billion, which is $69 million above aggregate carrying value and represents a 55% reduction in impaired loan balances from their peak.

The company’s CECL reserves remained stable quarter-over-quarter at $755 million, representing 3.8% of principal balance. Overall portfolio performance metrics were steady, with 94% of the portfolio performing and a weighted average risk rating of 3.1.

The following chart illustrates the company’s progress in reducing impaired loans:

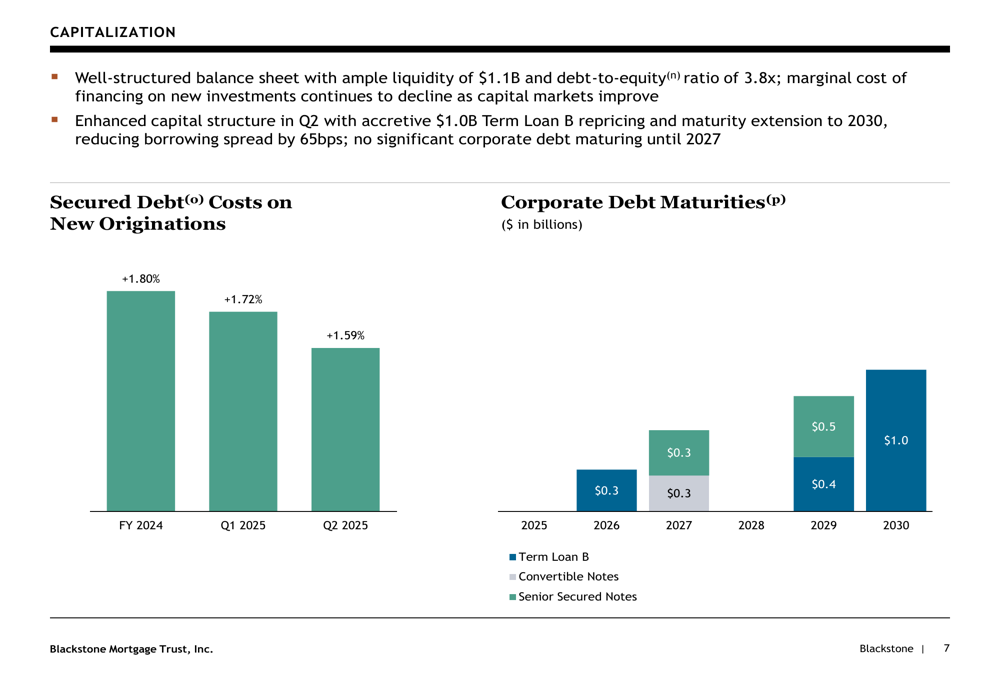

Balance Sheet and Liquidity

BXMT reported strong liquidity of $1.1 billion at quarter-end, supporting ongoing portfolio turnover. The company has total credit facility capacity of $19.1 billion across 14 bank counterparties, including over $7.0 billion undrawn.

During the quarter, BXMT enhanced its capital structure by repricing its $1.0 billion Term Loan B, reducing the spread by 65 basis points and extending the maturity to 2030. The company’s debt-to-equity ratio stands at 3.8x.

The marginal cost of financing on new investments continues to decline as capital markets improve. Secured debt costs on new originations decreased from 1.80% in fiscal year 2024 to 1.59% in Q2 2025.

The company’s debt maturity profile and financing costs are illustrated in the following chart:

Forward Outlook

While the presentation did not provide explicit forward guidance, BXMT’s strategic direction is clear from its recent activities. The company is focused on:

1. Continuing to grow its portfolio with an emphasis on multifamily and industrial assets

2. Further resolving impaired loans to strengthen the balance sheet

3. Maintaining geographic diversification with significant international exposure

4. Optimizing its capital structure to reduce financing costs

The company’s average leveraged spread over base rates exceeds 9%, providing a substantial margin to support its dividend. With the significant progress made in resolving impaired loans and the strategic shift in portfolio composition, BXMT appears positioned to continue its recovery from the challenges faced by commercial real estate lenders in recent years.

Investors will likely focus on the sustainability of the 9.7% dividend yield and the company’s ability to maintain book value as it continues to work through remaining credit issues while deploying capital into new opportunities.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.