Bitcoin price today: gains to $120k, near record high on U.S. regulatory cheer

Introduction & Market Context

Bridgewater Bancshares, Inc. (NASDAQ:BWB) released its first quarter 2025 earnings presentation on April 24, showcasing continued momentum following its acquisition of First Minnetonka City Bank in late 2024. The Minnesota-based bank reported solid financial performance with notable improvements in net interest margin and loan growth.

The company’s stock closed at $13.51 on April 23, 2025, up 4.89% for the day, and has shown resilience with trading well above its 52-week low of $10.52. The Q1 results represent the first full quarter since completing the First Minnetonka City Bank acquisition in December 2024.

Quarterly Performance Highlights

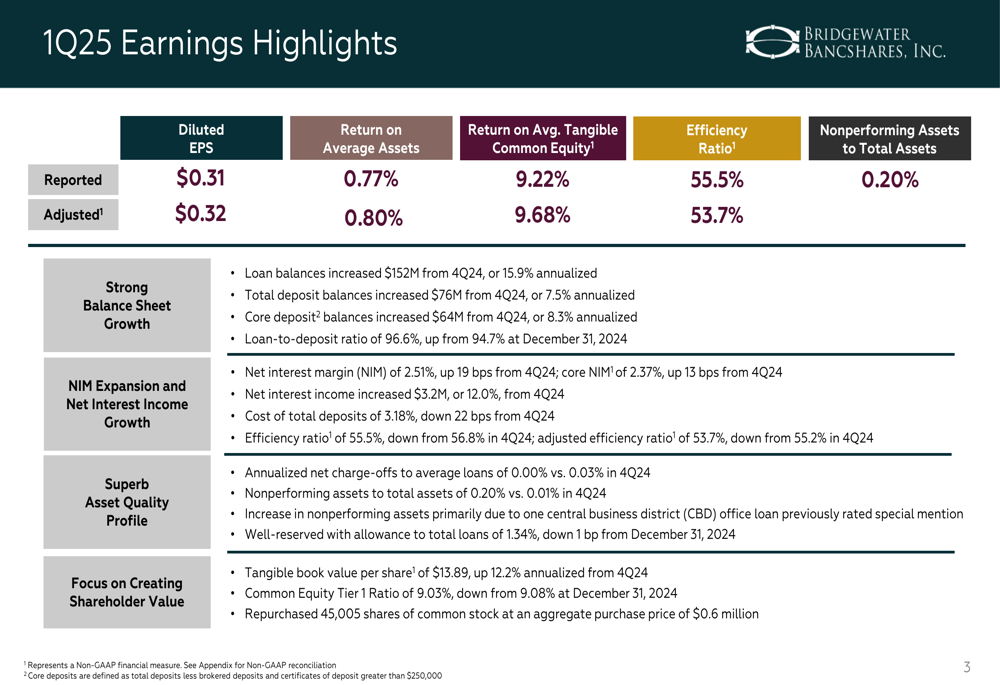

Bridgewater reported diluted earnings per share of $0.31 for Q1 2025, or $0.32 on an adjusted basis. This represents a sequential improvement from the $0.27 EPS reported in Q4 2024. Return on average assets came in at 0.77% (0.80% adjusted), while return on average tangible common equity reached 9.22% (9.68% adjusted).

As shown in the following comprehensive overview of the quarter’s performance:

The bank’s efficiency ratio improved to 55.5% (53.7% adjusted), outperforming the peer median of 60%. Asset quality remained excellent with nonperforming assets representing just 0.20% of total assets and zero net charge-offs during the quarter.

Detailed Financial Analysis

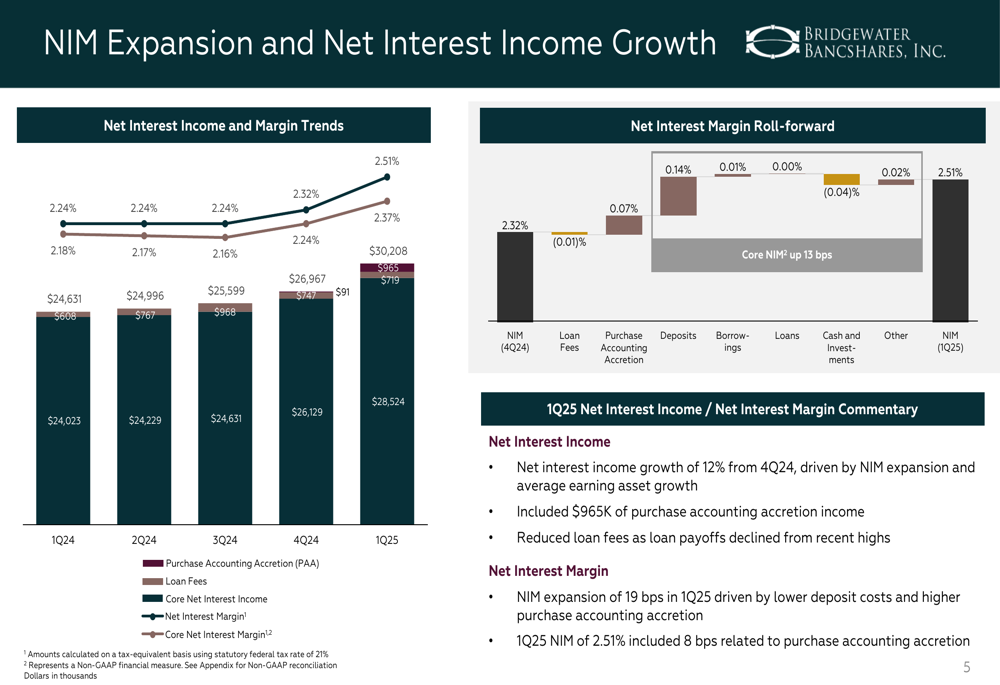

Net interest margin (NIM) expansion was a key driver of Bridgewater’s Q1 performance, increasing by 19 basis points from the previous quarter to 2.51%. This expansion contributed to net interest income growth of 12% from Q4 2024, which included $965,000 of purchase accounting accretion income related to the recent acquisition.

The following chart illustrates the NIM expansion and net interest income growth trends:

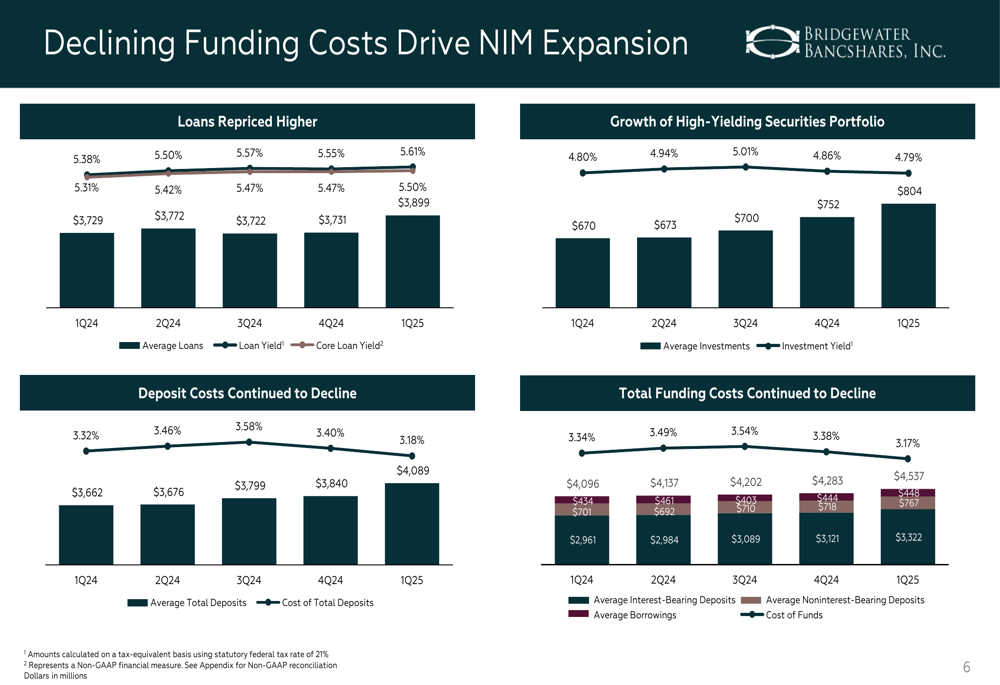

The margin improvement was primarily driven by declining funding costs, as shown in the detailed breakdown below:

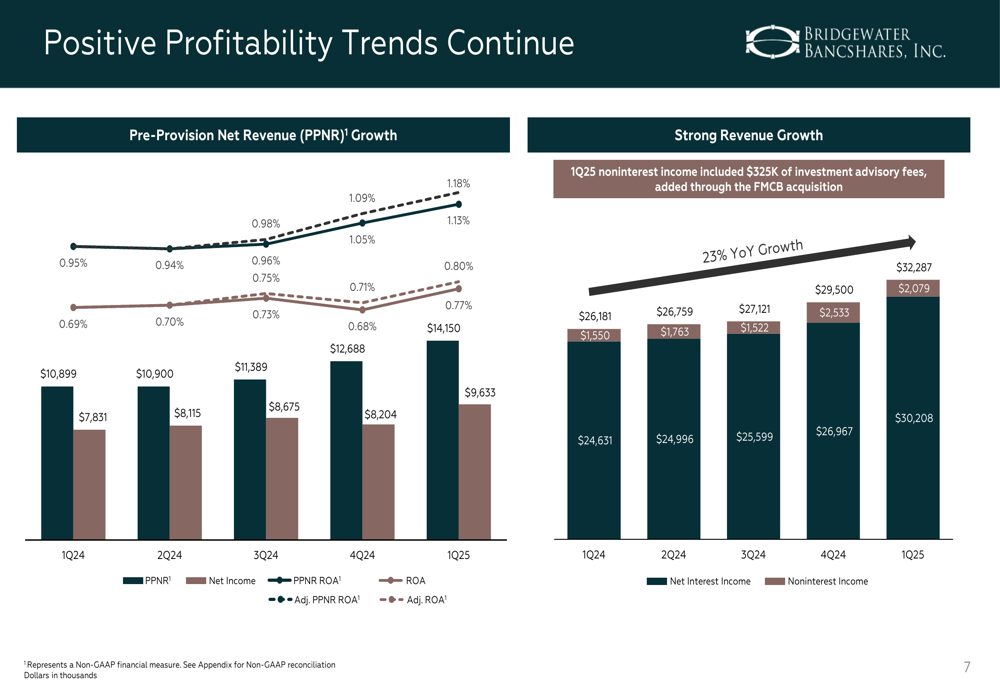

Bridgewater’s pre-provision net revenue (PPNR) grew to $14.15 million in Q1 2025, up from $10.90 million in Q1 2024, representing a 30% year-over-year increase. This growth was supported by strong revenue trends, with total revenue increasing by 23% compared to the same period last year.

The following chart demonstrates these positive profitability trends:

Balance Sheet Growth and Asset Quality

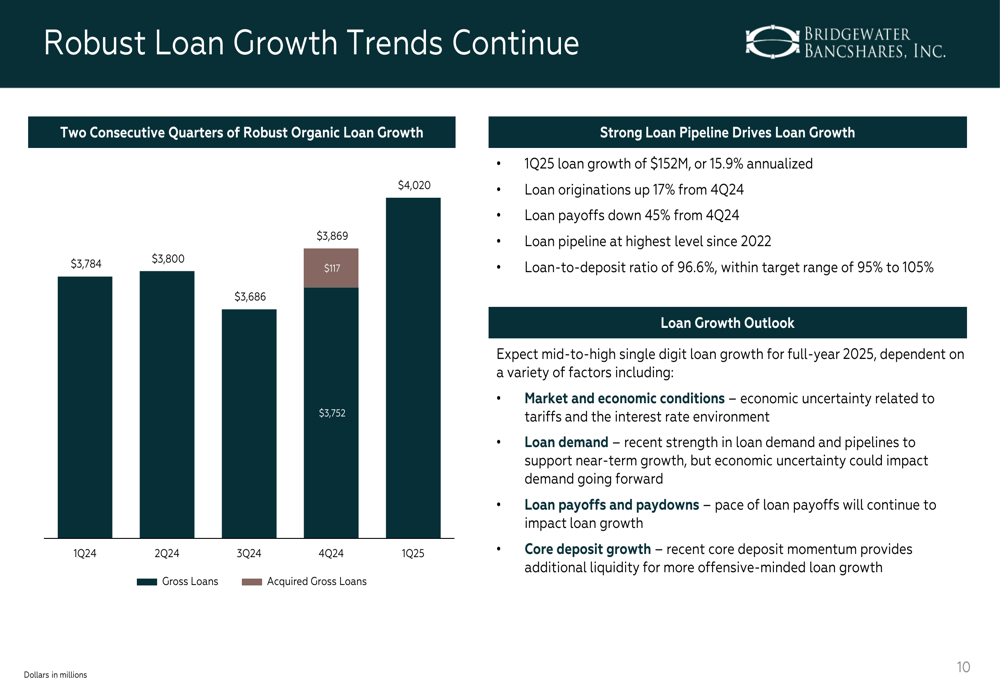

Loan growth remained robust with a $152 million increase from Q4 2024, representing a 15.9% annualized growth rate. This growth was driven by strong origination activity, which increased 17% from the previous quarter, while loan payoffs declined by 45%.

The bank’s loan portfolio growth trajectory is illustrated in the following chart:

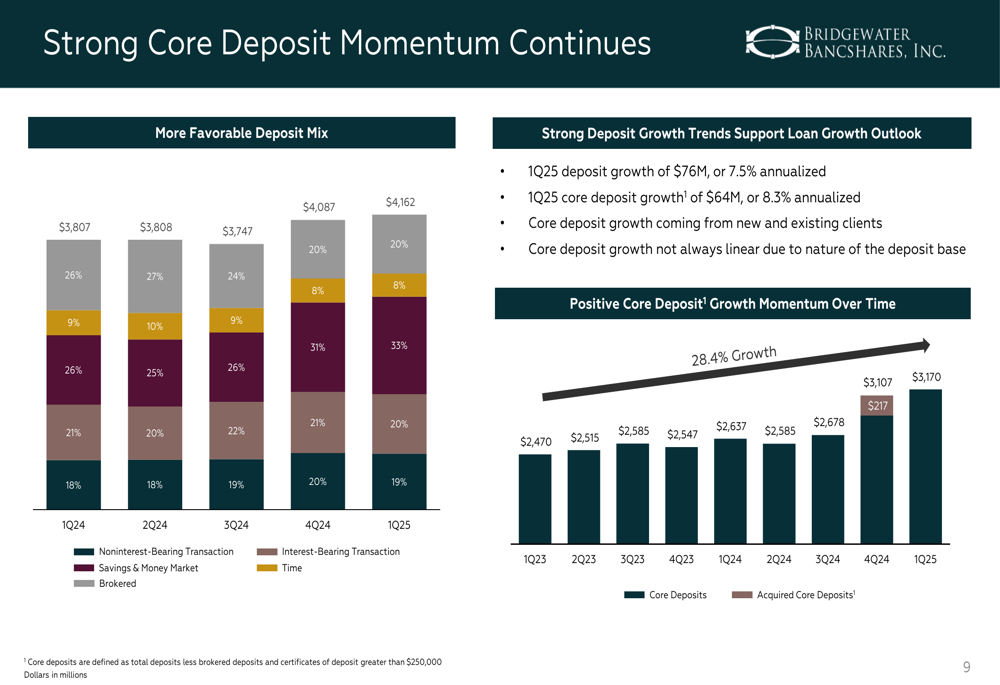

Deposit growth also remained strong with total deposits increasing by $76 million or 7.5% annualized in Q1 2025. Core deposits grew by $64 million or 8.3% annualized, coming from both new and existing clients. The bank maintained a loan-to-deposit ratio of 96.6%.

The deposit mix and growth trends are shown in the following visualization:

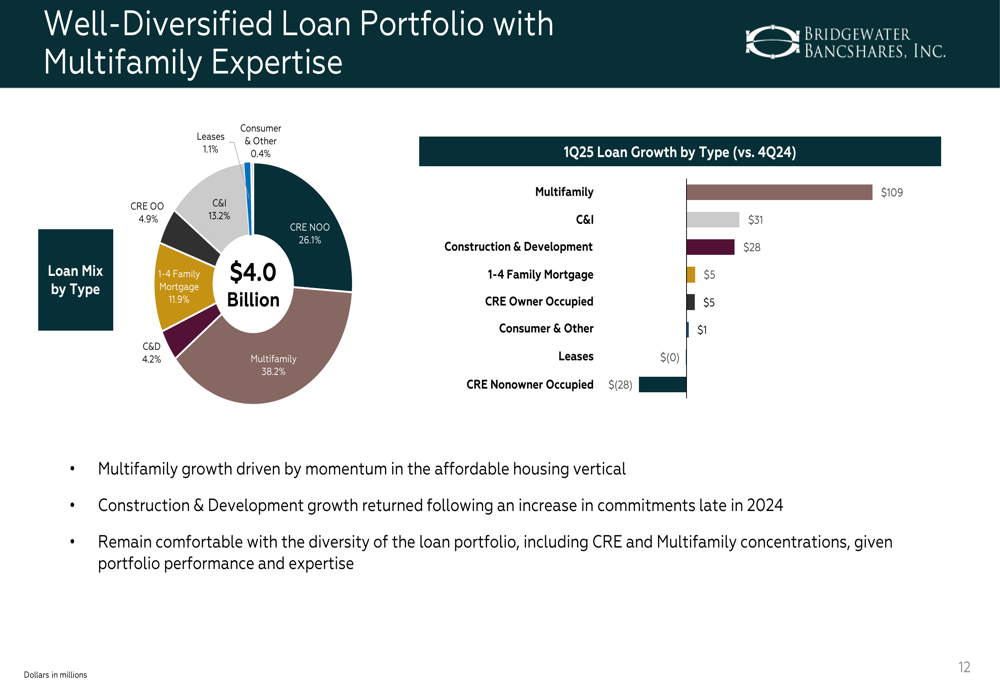

Bridgewater’s loan portfolio remains well-diversified with a focus on multifamily lending, which represents 38.2% of the total portfolio. The company highlighted its momentum in the affordable housing vertical as a key driver of multifamily growth.

The composition of the loan portfolio is detailed in this breakdown:

Asset quality metrics remained strong, with nonperforming assets at just 0.20% of total assets and no net charge-offs during the quarter. The allowance for credit losses stood at 1.34% of gross loans, providing adequate coverage for potential future losses.

Strategic Initiatives & Outlook

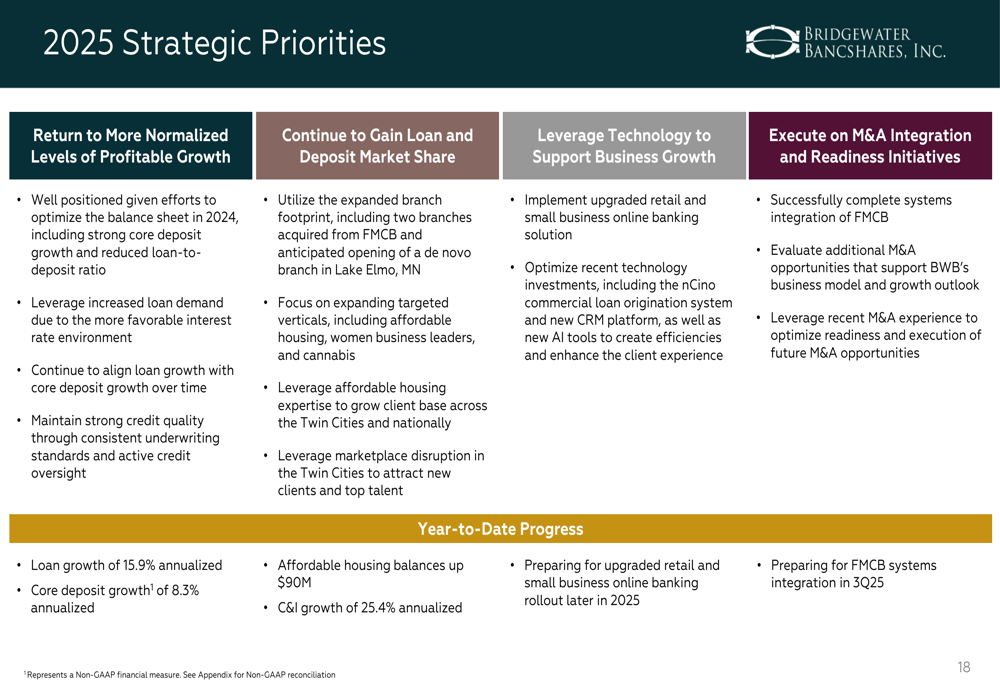

Bridgewater outlined its strategic priorities for 2025, focusing on normalized profitable growth, market share gains, technology implementation, and successful integration of the First Minnetonka City Bank acquisition.

The company’s strategic roadmap is detailed in the following overview:

For the remainder of 2025, Bridgewater expects mid-to-high single-digit loan growth, a slower pace of net interest margin expansion in Q2, and high-teen noninterest expense growth for the full year (excluding merger-related expenses). The bank plans to maintain stable capital levels while continuing to repurchase shares opportunistically.

Long-Term Performance and Shareholder Value

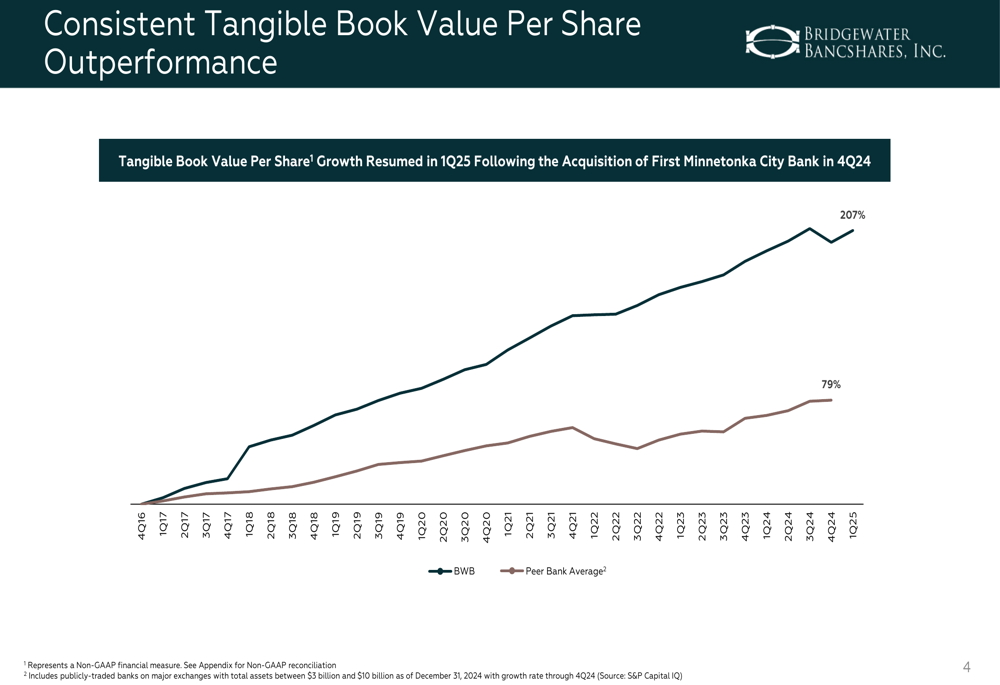

A notable achievement highlighted in the presentation is Bridgewater’s consistent outperformance in tangible book value per share growth compared to peers. Since 2016, the bank has grown tangible book value per share by 207%, significantly outpacing the peer bank average of 79%.

This long-term value creation trend is illustrated in the following chart:

Tangible book value per share reached $13.89 in Q1 2025, representing a 12.2% annualized increase. The company resumed tangible book value growth following the temporary impact of the First Minnetonka City Bank acquisition in Q4 2024.

Forward-Looking Statements

Bridgewater management expressed confidence in their ability to continue executing on their strategic priorities while navigating the current interest rate environment. The bank expects to leverage its expanded branch footprint from the recent acquisition to gain additional market share in both loans and deposits.

While the company anticipates continued growth and profitability improvements, it acknowledged that the pace of net interest margin expansion is likely to moderate in the coming quarters. The high-teen expense growth projection for 2025 reflects investments in technology and infrastructure to support future growth.

The bank’s capital allocation priorities remain focused on organic growth, with share repurchases continuing as a secondary use of capital. During Q1 2025, Bridgewater repurchased 45,005 shares of common stock, demonstrating its commitment to returning capital to shareholders while maintaining adequate capital levels for growth.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.