Missed the webinar? Here are Investing.com’s top 10 stock picks for 2026

California Resources Corporation (NYSE:CRC) reported solid third-quarter 2025 results on November 5, demonstrating financial resilience despite lower commodity prices while advancing its strategic positioning in California's evolving energy landscape.

Quarterly Performance Highlights

California Resources delivered strong financial performance in Q3 2025, reporting adjusted EBITDAX of $338 million and free cash flow before working capital changes of $231 million. The company's earnings per share of $1.46 beat analyst expectations of $1.29 by 13.18%, although revenue of $855 million fell short of the $875.82 million forecast.

"California is entering a new era for locally produced energy, one defined by abundance, affordability, and sustainably produced solutions," said CEO Francisco Leon during the earnings call, emphasizing CRC's strategic role in the state's energy transition.

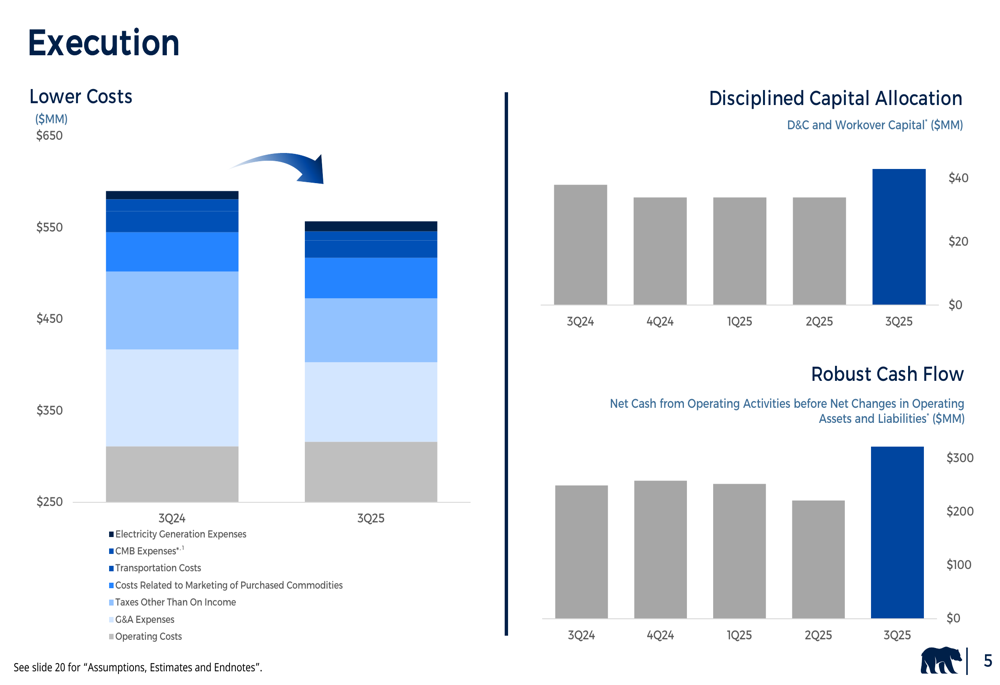

The company maintained production levels at 137 MBOE/D with 78% oil composition, while operating with just two rigs and deploying $43 million in drilling, completion, and workover capital.

As shown in the following chart, CRC has effectively managed costs while maintaining disciplined capital allocation:

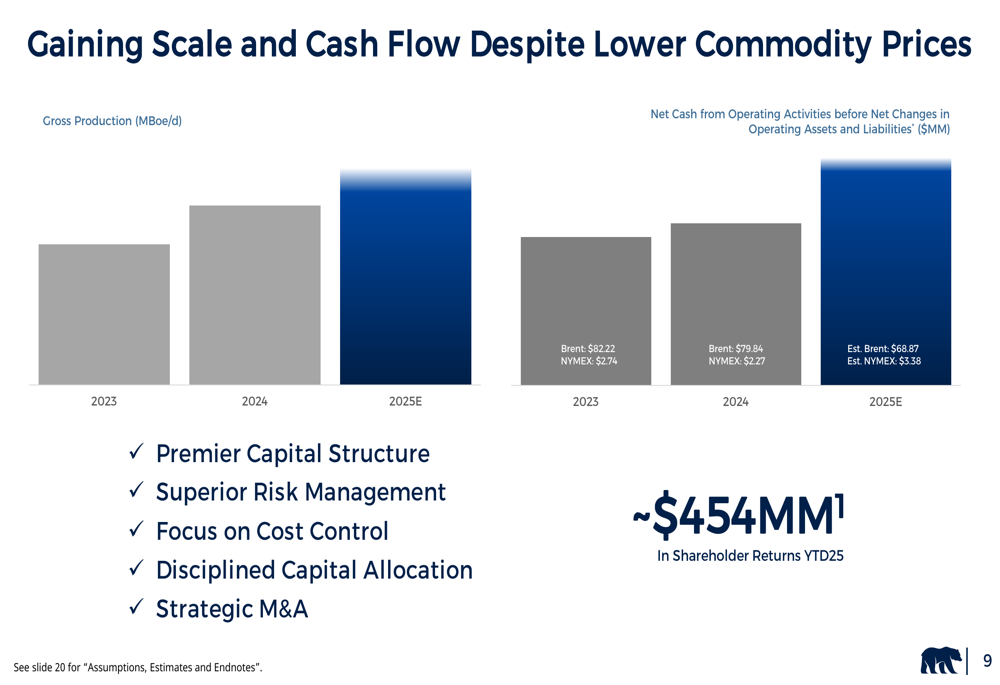

The company's focus on operational efficiency has enabled it to generate robust cash flow despite the challenging commodity price environment. Brent crude prices averaged $68.87 in 2025, significantly lower than the $79.84 average in 2024.

As illustrated in this production and cash flow comparison:

Strategic Initiatives

California Resources is positioning itself as "A Different Kind of Energy Company" with a three-pronged approach focused on higher cash flow, lower carbon emissions, and better outcomes for California. The company is capitalizing on an improving regulatory landscape following the Governor's signing of bills SB237/614 and AB1207 into law in Fall 2025.

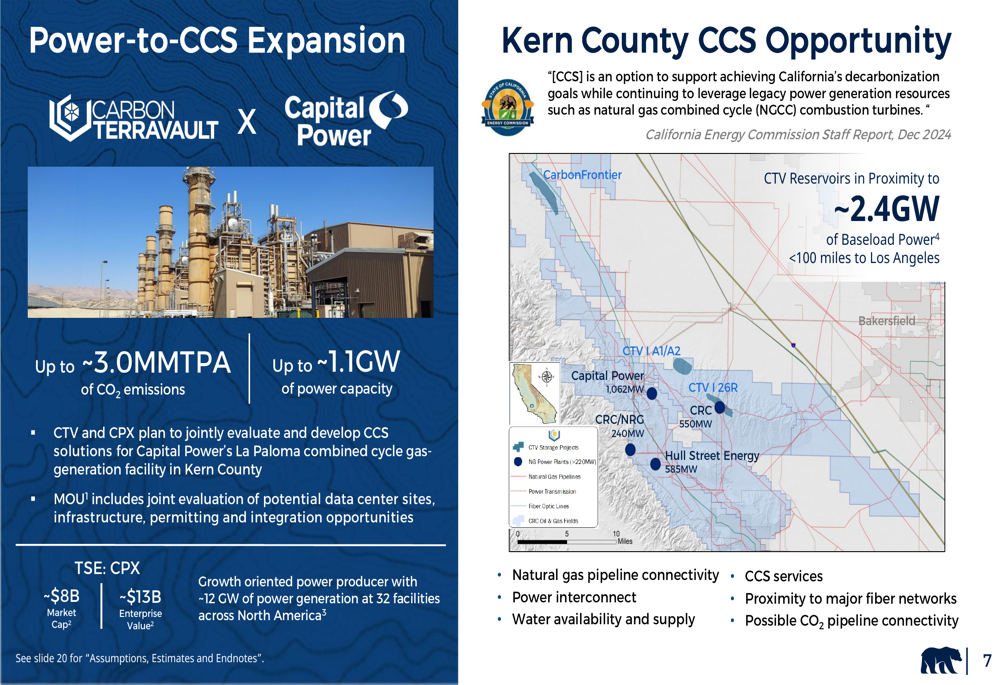

The company has made significant progress in its carbon capture and sequestration (CCS) initiatives. CRC received California's first EPA Class VI permits for underground CO2 injection and storage and is advancing its Elk Hills Cryogenic Gas Plant CCS project, which is on track to begin CO2 sequestration in early 2026.

A key strategic development is CRC's new memorandum of understanding with Capital Power for carbon capture:

This partnership aims to jointly evaluate and develop CCS solutions for Capital Power's La Paloma combined cycle gas-generation facility in Kern County, with potential for up to 3 million tonnes per annum (MMTPA) of CO2 emissions capture and up to 1.1GW of power capacity.

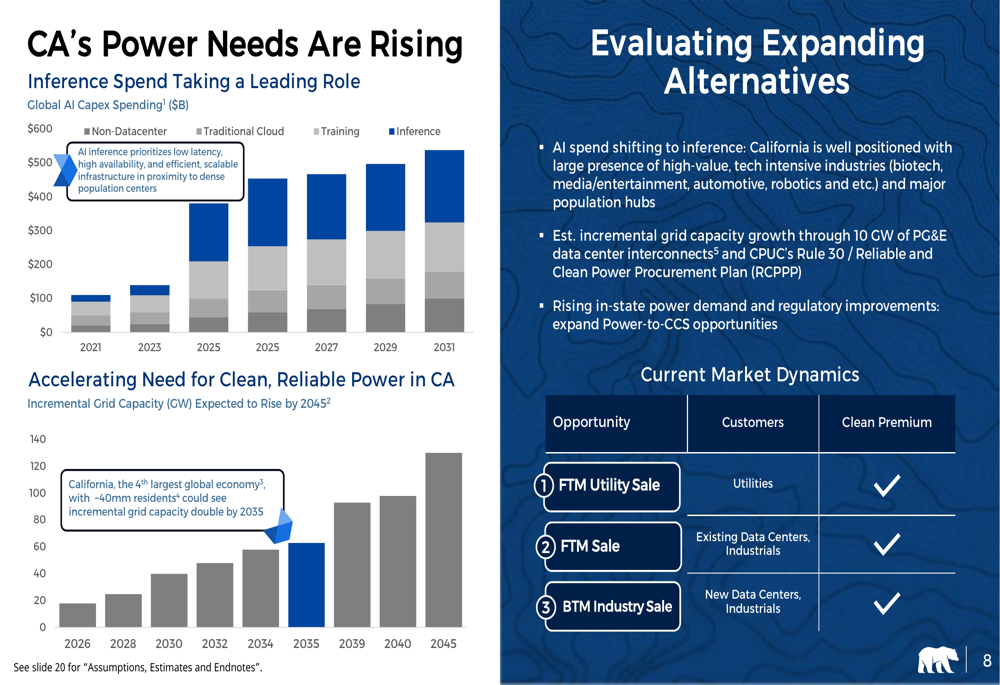

The company is also well-positioned to benefit from California's increasing power needs, particularly driven by AI infrastructure development:

Forward-Looking Statements

California Resources provided guidance for Q4 2025 and outlined its 2026 outlook, projecting continued operational efficiency and financial discipline:

For 2026, the company is targeting a shallower corporate PDP decline of 8-13%, reflecting the resilience of its reservoirs. CRC plans to operate four rigs with $280-$300 million allocated to drilling, completion, and workover capital.

A significant strategic development is CRC's pending merger with Berry Corporation (BRY), expected to close in Q1 2026. The company anticipates annual synergies of $80-$90 million within 12 months post-close. To refinance BRY's debt at closing, CRC has already raised $400 million in 2034 Senior Notes at 7.000%, which contributed to a ratings upgrade from Moody's to Ba3 and a positive outlook from Fitch.

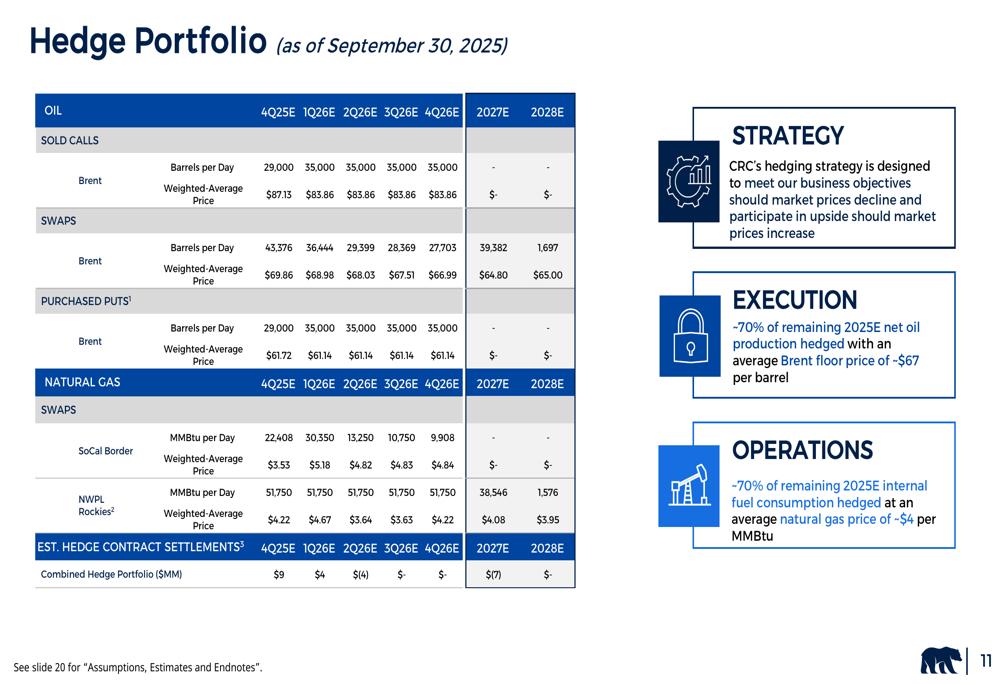

The company has also implemented a robust hedging strategy to protect against market volatility:

Approximately 70% of CRC's remaining 2025 net oil production is hedged with an average Brent floor price of around $67 per barrel, while 70% of its internal fuel consumption is hedged at an average natural gas price of approximately $4 per MMBtu.

Financial Position & Shareholder Returns

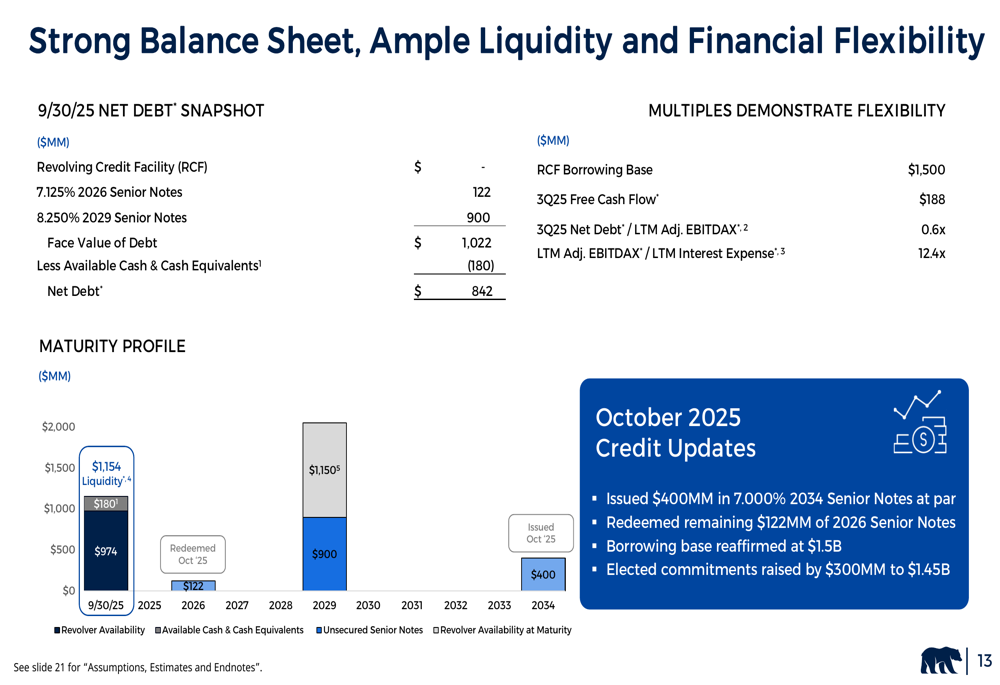

California Resources maintains a strong balance sheet with a net debt of $842 million as of September 30, 2025, resulting in a leverage ratio of 0.6x. The company has ample liquidity with a $1.5 billion revolving credit facility borrowing base and $180 million in cash and cash equivalents.

The financial flexibility is illustrated in the following slide:

In October 2025, CRC further strengthened its financial position by issuing $400 million in 7.000% 2034 Senior Notes at par and redeeming the remaining $122 million of 2026 Senior Notes. The company also had its borrowing base reaffirmed at $1.5 billion and increased its elected commitments by $300 million to $1.45 billion.

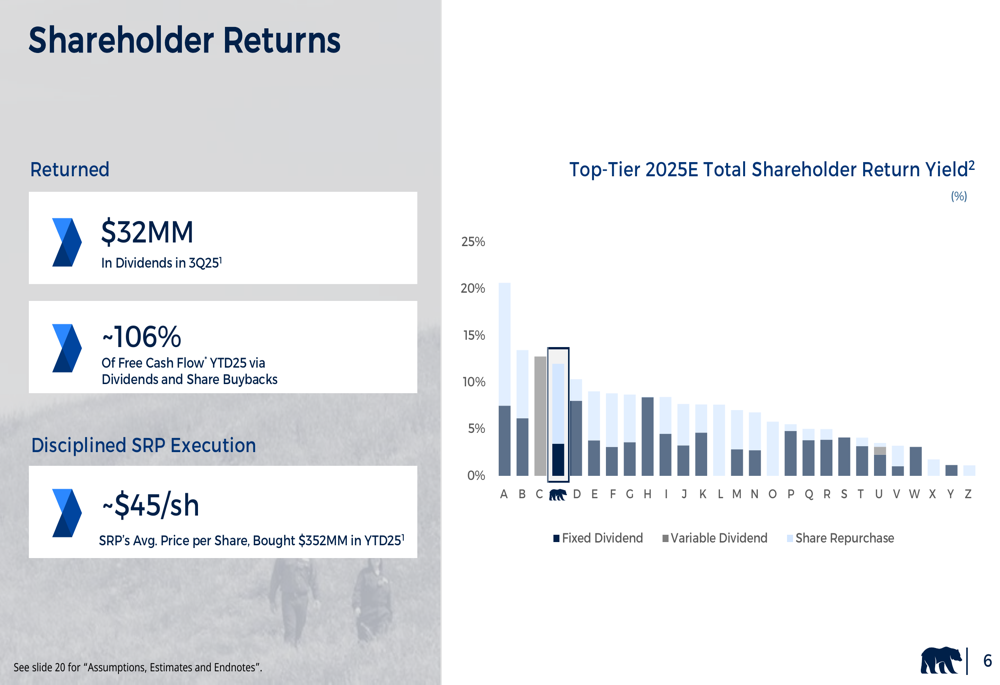

CRC continues to prioritize shareholder returns, returning $454 million to shareholders year-to-date through dividends and share buybacks. The company raised its dividend by 5% in Q3, marking its fourth consecutive annual increase.

As shown in the shareholder returns overview:

The company returned $32 million in dividends in Q3 2025 and has executed its share repurchase program at an average price of approximately $45 per share, buying back $352 million worth of shares year-to-date.

California Resources' stock closed at $46.65 following the earnings release on November 5, representing a 2.51% increase, reflecting investor confidence in the company's strategy and performance despite the slight revenue miss.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.