Flutter Entertainment beats Q3 earnings estimate despite sports results impact

Introduction & Market Context

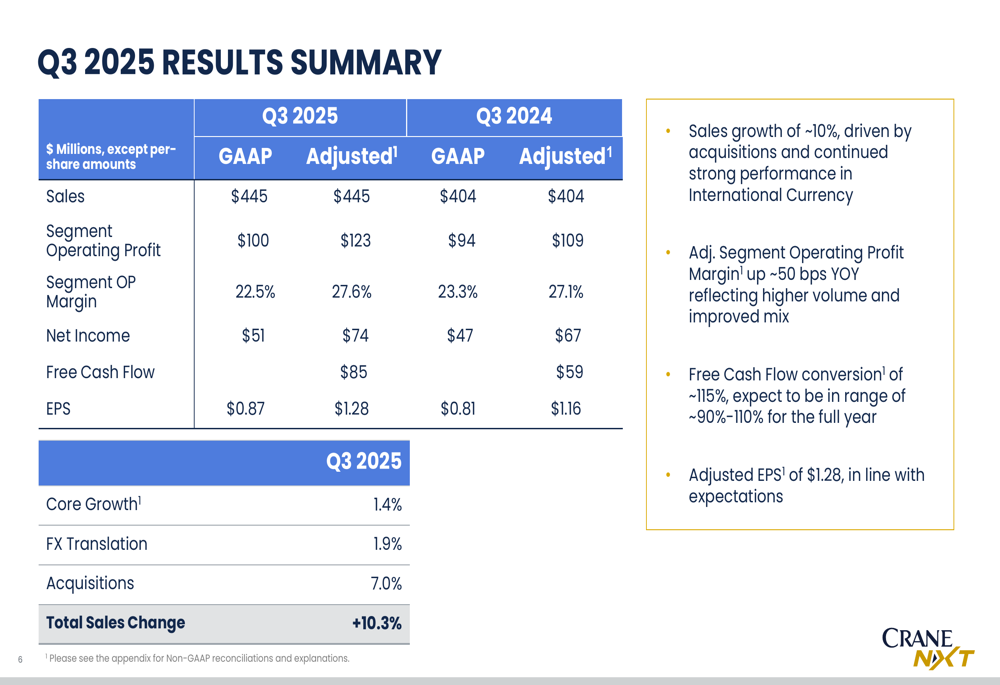

Crane NXT Co (NYSE:CXT) presented its third quarter 2025 financial results on November 6, showcasing 10% sales growth while narrowing its full-year earnings guidance. Despite reporting adjusted earnings per share of $1.28, which exceeded analyst expectations of $1.26, the company’s stock fell 5.36% to $61.78 in after-hours trading.

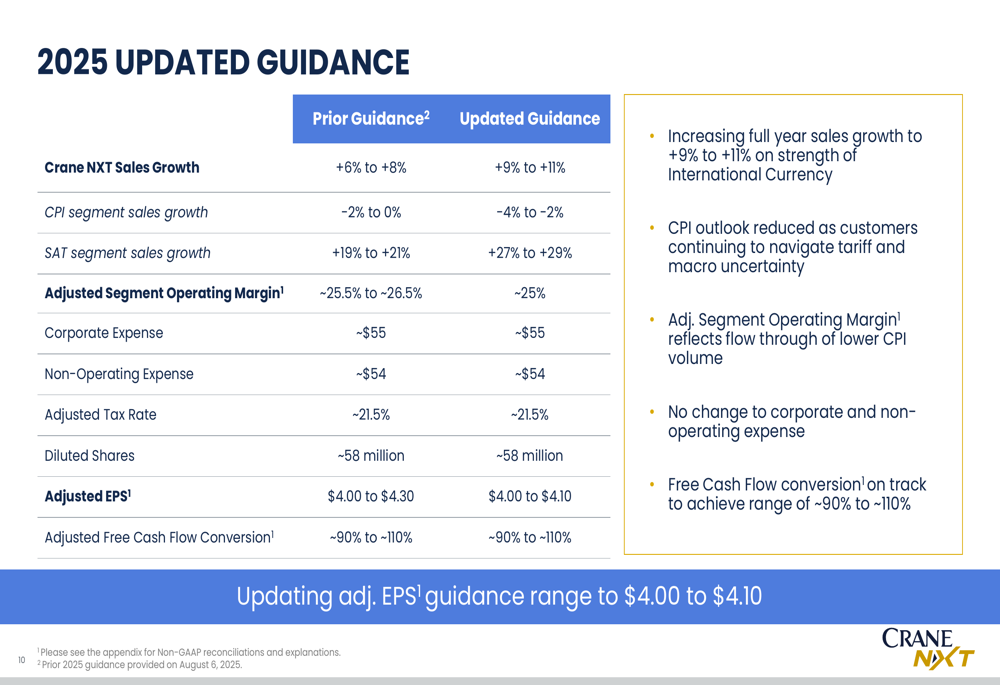

The mixed market reaction came as Crane NXT narrowed its full-year adjusted EPS guidance to $4.00-$4.10 from the previous range of $4.00-$4.30, potentially disappointing investors who were expecting results toward the higher end of the range.

Quarterly Performance Highlights

Crane NXT reported Q3 2025 sales of $445 million, representing 10.3% growth when accounting for core growth, foreign exchange impacts, and acquisitions. The company achieved an adjusted segment operating profit margin of 27.6%, up approximately 50 basis points year-over-year, reflecting higher volume and improved mix.

As shown in the comprehensive results summary below:

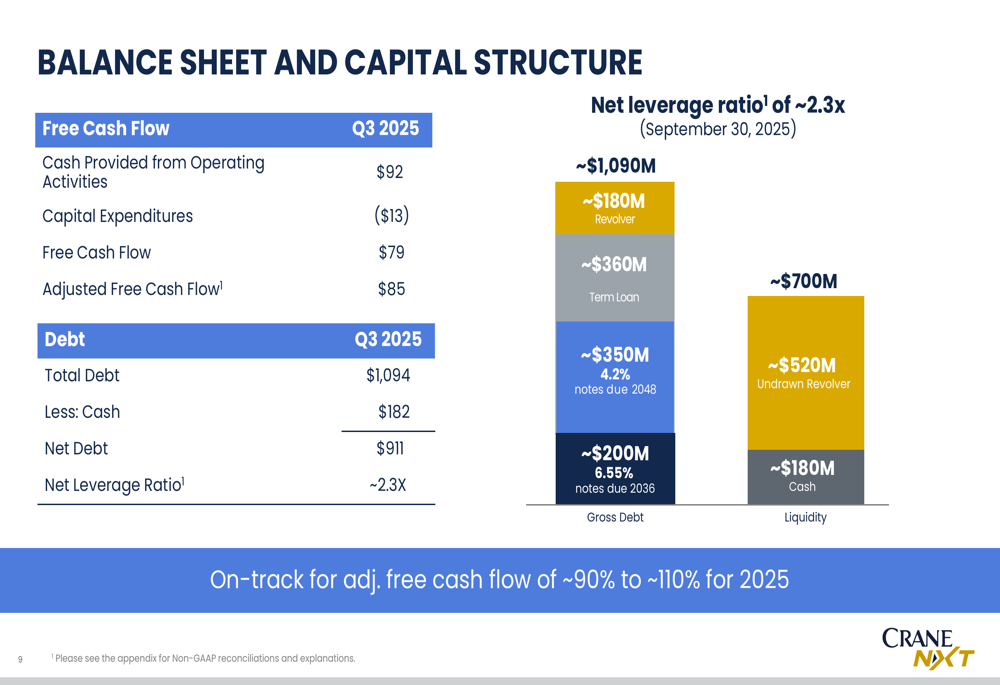

Free cash flow conversion reached approximately 115% in the quarter, with the company expecting to maintain a range of 90-110% for the full year. This strong cash generation supports Crane NXT’s strategic initiatives and potential future acquisitions.

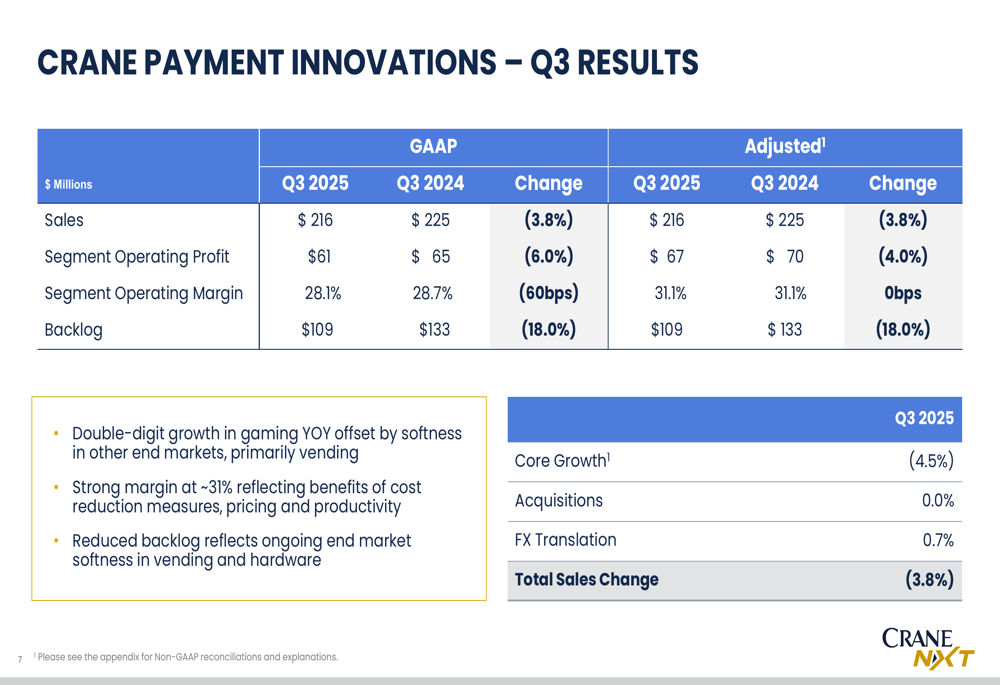

The company’s performance varied significantly across its two main segments. The Security and Authentication Technologies (SAT) segment delivered exceptional growth with sales increasing 28.1% to $229 million, driven by strong demand in international currency markets. Meanwhile, the Crane Payment Innovations (CPI) segment faced headwinds, with sales declining 3.8% to $216 million, primarily due to softness in vending markets.

Strategic Initiatives

A key highlight from the presentation was Crane NXT’s announcement of its agreement to acquire Antares Vision, a global leader in detection, inspection, and track & trace technologies. This strategic acquisition, expected to close in the first half of 2026, will expand Crane NXT’s technology solutions into the life sciences and food & beverage markets.

The following slide provides an overview of Antares Vision’s capabilities and financial profile:

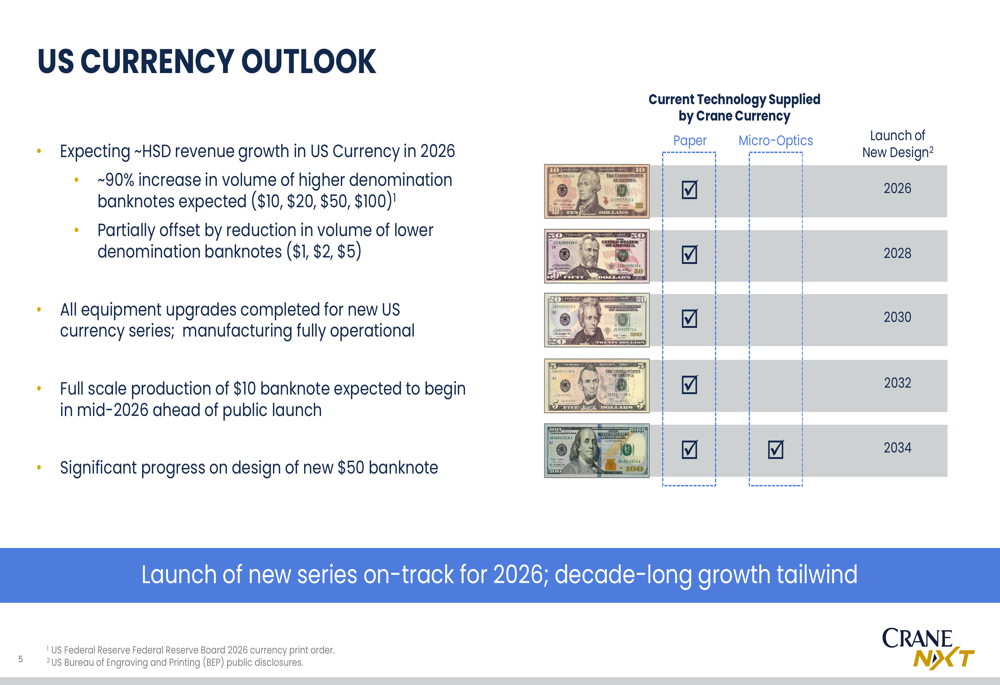

Another significant growth driver highlighted in the presentation is the upcoming launch of a new US currency series. Crane NXT expects high-single-digit revenue growth in its US Currency business in 2026, driven by a 90% increase in volume for higher denomination banknotes ($10, $20, $50, $100). The company has completed all equipment upgrades for the new series and expects full-scale production of the $10 banknote to begin in mid-2026.

Forward-Looking Statements

Crane NXT updated its full-year 2025 guidance, increasing its sales growth projection to 9-11% from the previous 6-8%, primarily driven by strength in International Currency. However, the company reduced its CPI segment sales growth outlook to -4% to -2% (from -2% to 0%) as customers continue to navigate tariff and macroeconomic uncertainties.

The updated guidance also reflects a slight adjustment in adjusted segment operating margin to approximately 25%, down from the previous range of 25.5-26.5%, due to lower CPI volume. As mentioned earlier, the company narrowed its adjusted EPS guidance to $4.00-$4.10.

Looking beyond 2025, Crane NXT is positioning itself for accelerated growth in 2026, with momentum building in key strategic areas. The company announced it will hold an Investor Day on February 25, 2026, in New York City, where it will likely provide more details on its long-term strategy and financial targets.

Detailed Financial Analysis

Crane NXT maintained a solid balance sheet with $182 million in cash and $1,094 million in total debt as of September 30, 2025, resulting in a net debt of $911 million and a net leverage ratio of approximately 2.3x. This financial position provides flexibility for future strategic investments and shareholder returns.

The company’s liquidity and debt structure are illustrated in the following slide:

The SAT segment’s strong performance was driven by core sales growth of 8.8%, acquisitions contributing 15.8%, and favorable foreign exchange impact of 3.4%. The segment’s backlog increased by 27.4% to $448 million, with a book-to-bill ratio of approximately 1, indicating continued strong demand.

In contrast, the CPI segment faced challenges with core sales declining by 4.5%, partially offset by a positive foreign exchange impact of 0.7%. The segment’s backlog decreased by 18% to $109 million, reflecting ongoing end market softness in vending and hardware. Despite these challenges, the segment maintained a strong operating margin of 28.1%, demonstrating effective cost management through pricing, productivity, and cost reduction measures.

Competitive Industry Position

Crane NXT continues to strengthen its market-leading positions across its business segments. In the currency and authentication markets, the company is migrating customers to advanced micro-optics technology while building a strong backlog in international currency, with orders booked into 2027.

In the payment solutions space, despite short-term challenges in vending markets, the CPI Service business is adding new customers and growing annual recurring revenue at a mid-single-digit rate. The gaming segment within CPI delivered double-digit growth year-over-year, partially offsetting weakness in other end markets.

The acquisition of Antares Vision represents a strategic expansion into adjacent markets with growth tailwinds, particularly in life sciences and food & beverage, where track and trace technologies are increasingly critical for regulatory compliance and supply chain security.

As Crane NXT navigates the current macroeconomic environment, its diversified business model, strong margin profile, and strategic growth initiatives position the company well for long-term success, despite near-term challenges in certain segments.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.