Bill Holdings jumps amid reports payments firm is exploring potential sale

Introduction & Market Context

DexCom Inc. (NASDAQ:DXCM) presented its third-quarter 2025 earnings results on October 30, showcasing accelerating growth and record-breaking financial performance. The continuous glucose monitoring (CGM) technology leader reported significant progress across its product portfolio, with particular strength in both domestic and international markets.

Despite the strong quarterly results, DexCom’s stock remained relatively stable in after-hours trading, closing at $68.18, down just 0.01%. The stock has traded between $57.52 and $93.25 over the past 52 weeks, suggesting investors had already priced in the positive performance.

Quarterly Performance Highlights

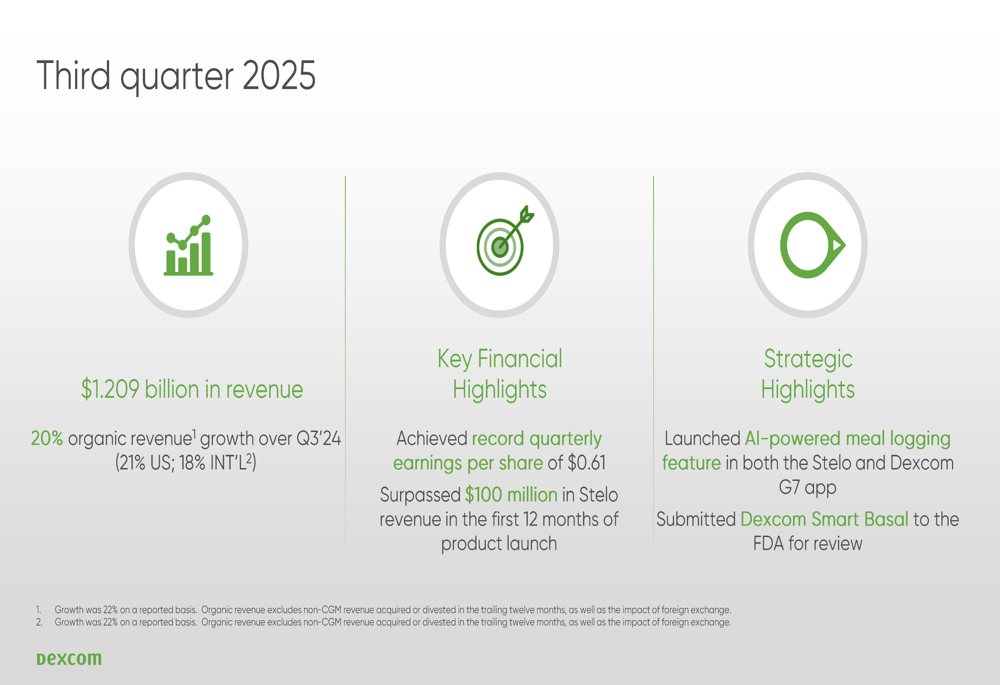

DexCom reported Q3 2025 revenue of $1.209 billion, representing 20% organic growth year-over-year. The company saw balanced growth across regions, with U.S. revenue increasing by 21% and international revenue growing by 18% on an organic basis.

As shown in the following quarterly highlights slide, DexCom achieved record quarterly earnings per share of $0.61 and surpassed $100 million in Stelo revenue within the first 12 months of that product’s launch:

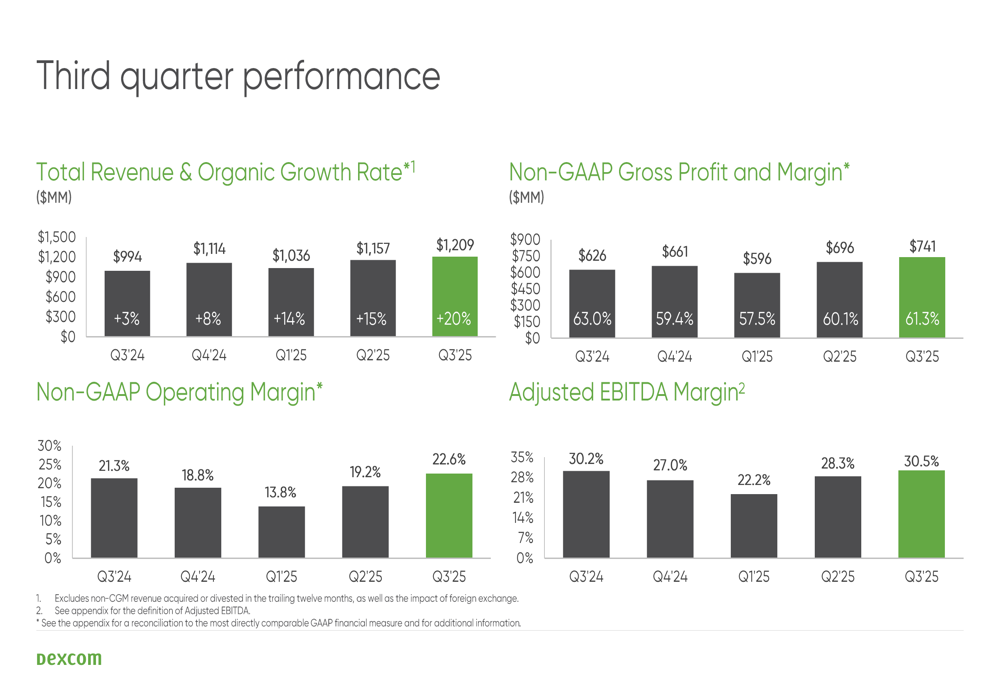

The company’s financial performance demonstrated consistent improvement throughout 2025, with accelerating growth rates and strengthening margins. The quarterly performance charts illustrate this positive trajectory across key financial metrics:

Detailed Financial Analysis

DexCom’s gross profit for Q3 2025 reached $741 million, representing a non-GAAP gross margin of 61.3%, an improvement from 60.1% in the previous quarter but slightly below the 63.0% reported in Q3 2024. The company’s operating efficiency continued to improve, with non-GAAP operating margin expanding to 22.6%, up from 19.2% in Q2 2025 and 21.3% in the year-ago quarter.

Adjusted EBITDA margin reached 30.5% in Q3 2025, showing steady improvement from 28.3% in Q2 2025 and slightly higher than the 30.2% reported in Q3 2024. This performance reflects DexCom’s ability to scale operations efficiently while continuing to invest in growth initiatives.

The company’s revenue growth was balanced across product categories and geographies. U.S. revenue totaled $852 million, while international revenue reached $357.4 million. DexCom maintained a strong cash position, with over $3.3 billion in cash and cash equivalents, providing substantial flexibility for future investments and strategic initiatives.

Strategic Initiatives & Product Innovation

DexCom continues to drive growth through product innovation and market expansion. In Q3, the company launched an AI-powered meal logging feature in both the Stelo and Dexcom G7 apps, enhancing the user experience and functionality of its CGM systems. Additionally, DexCom submitted its Smart Basal technology to the FDA for review, potentially expanding its product portfolio in the insulin management space.

The Stelo product line, targeted at Type 2 diabetes patients, has shown remarkable traction, surpassing $100 million in revenue within its first year on the market. This success underscores DexCom’s effective strategy in addressing the broader diabetes market beyond its traditional Type 1 diabetes focus.

Jake Leach, President and Interim CEO, emphasized the company’s customer-centric approach during the earnings call, stating, "The customer is and will always be the North Star for this company." This philosophy appears to be driving both product development and market expansion strategies.

Forward-Looking Statements & Guidance

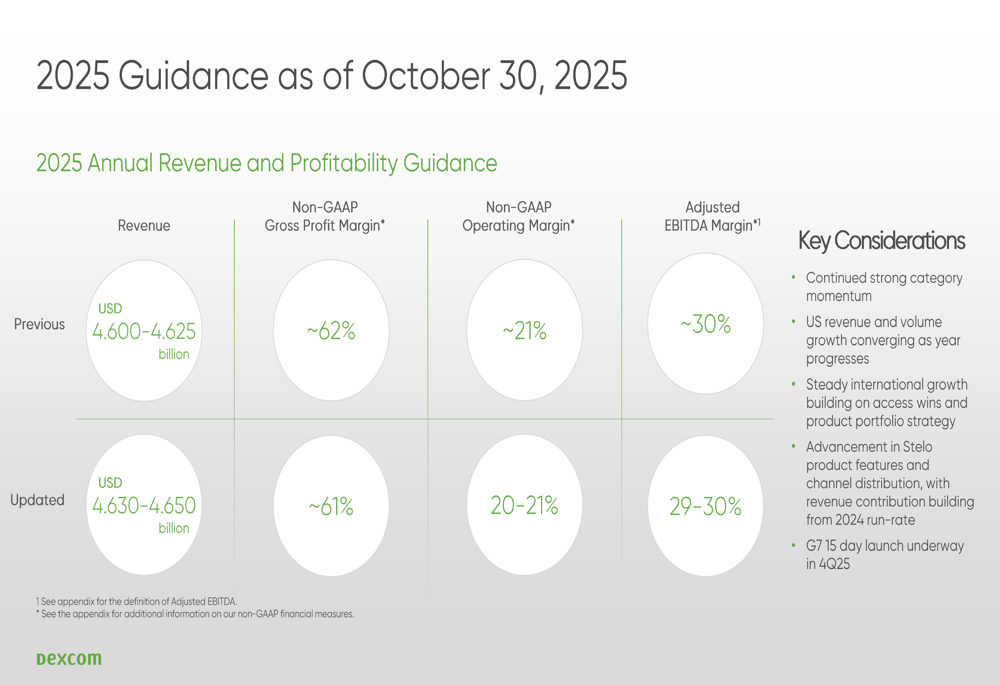

Based on its strong performance, DexCom raised its full-year 2025 guidance, as illustrated in the following slide:

The updated guidance projects annual revenue between $4.630-4.650 billion, up from the previous range of $4.600-4.625 billion. The company maintained its profitability outlook with slight adjustments, forecasting a non-GAAP gross profit margin of approximately 61% and a non-GAAP operating margin of 20-21%.

Key considerations supporting this guidance include continued strong category momentum, revenue and volume growth convergence in the U.S. market, sustained international growth, and the advancement of Stelo product features and distribution channels. DexCom also highlighted the upcoming G7 15-day sensor launch planned for Q4 2025, which could further strengthen its competitive position.

CFO Jereme Sylvain expressed confidence in the company’s operational improvements during the earnings call, stating, "Our goal is to continue to deliver operating margin improvement over time." This focus on profitability alongside growth suggests a balanced approach to scaling the business.

While DexCom’s outlook remains positive, the company faces potential challenges including sensor quality concerns, market saturation in the CGM space, macroeconomic pressures affecting healthcare budgets, and potential supply chain disruptions. However, the company’s strong cash position and continued innovation provide significant buffers against these risks.

As DexCom continues to execute on its growth strategy, investors will be watching closely for the successful launch of new products and continued expansion in both the Type 1 and Type 2 diabetes markets. With its record-breaking Q3 performance and raised guidance, DexCom appears well-positioned to maintain its leadership in the CGM technology space through the remainder of 2025 and beyond.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.