Bitcoin set for a rebound that could stretch toward $100000, BTIG says

Introduction & Market Context

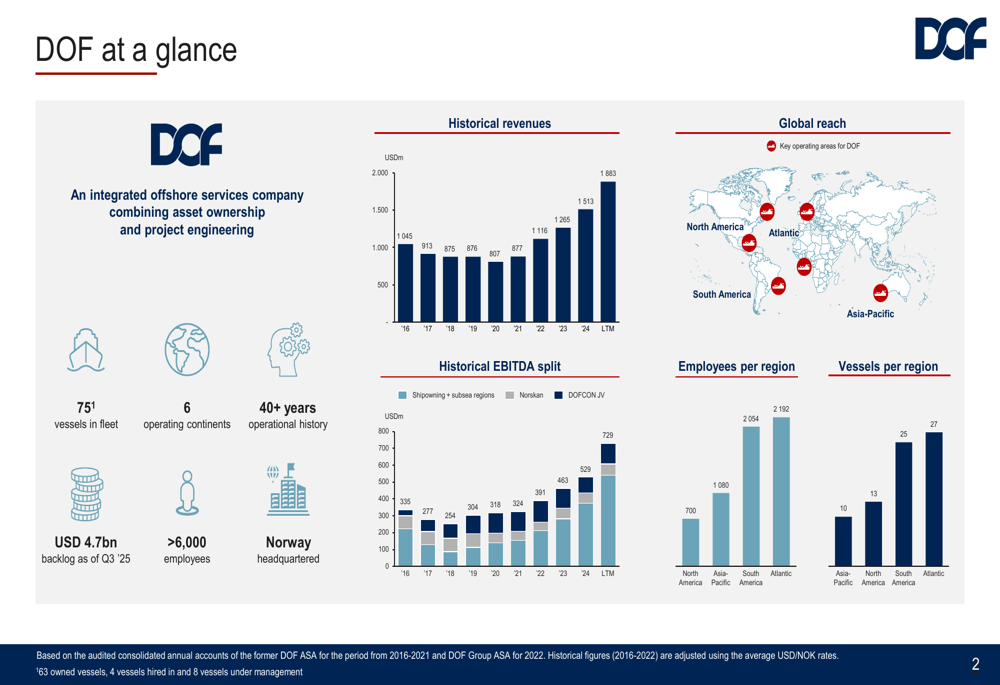

DOF Group ASA (OB:DOFG) presented its third quarter 2025 results on November 5, showing continued strong performance across its offshore services segments. The integrated offshore services company, which operates a fleet of 75 vessels across six continents, reported solid financial metrics and significant contract awards that strengthened its already substantial backlog.

Following the presentation, DOF Group's stock rose by 1.79% to 93.60, approaching its 52-week high of 103.00, reflecting positive investor sentiment about the company's strategic direction and financial performance.

As shown in the following snapshot of DOF's global presence and key metrics:

Quarterly Performance Highlights

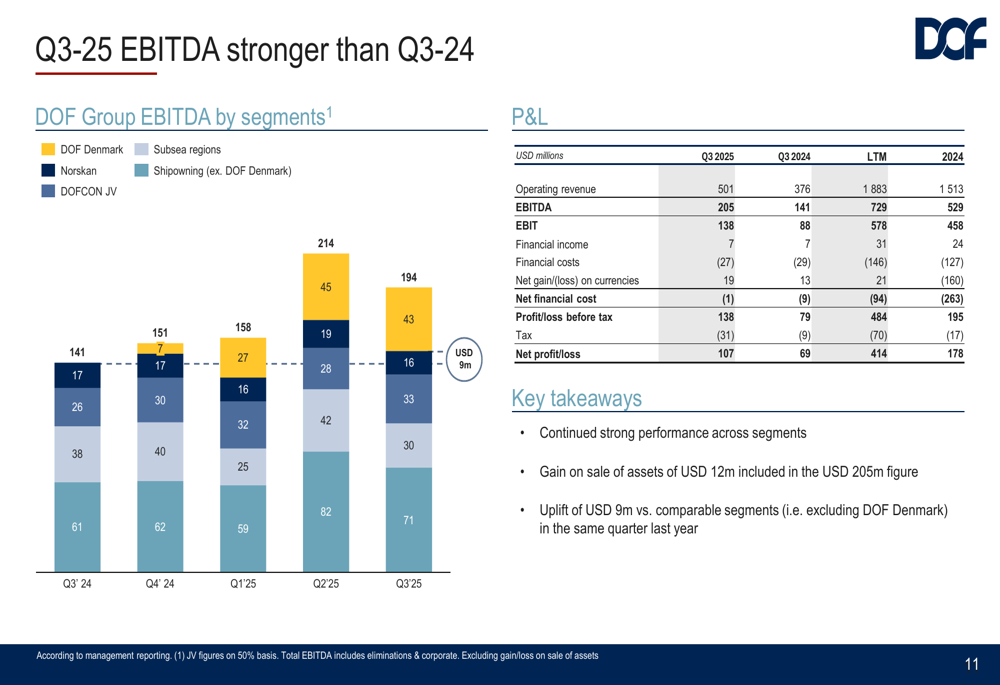

DOF Group reported an EBITDA of $205 million for Q3 2025, which included a $12 million gain from vessel sales. The company's DOF Denmark segment contributed $54 million to the EBITDA figure, which also included gains from asset sales. The quarter saw an average fleet utilization of 87%, down from 92% in the comparative period.

The company's financial performance remained strong across all segments, with a $9 million uplift compared to the same segments in Q3 2024 (excluding DOF Denmark). The cash position increased by more than $120 million during the quarter, strengthening the company's financial flexibility.

The following chart breaks down DOF's Q3 2025 EBITDA performance by segment:

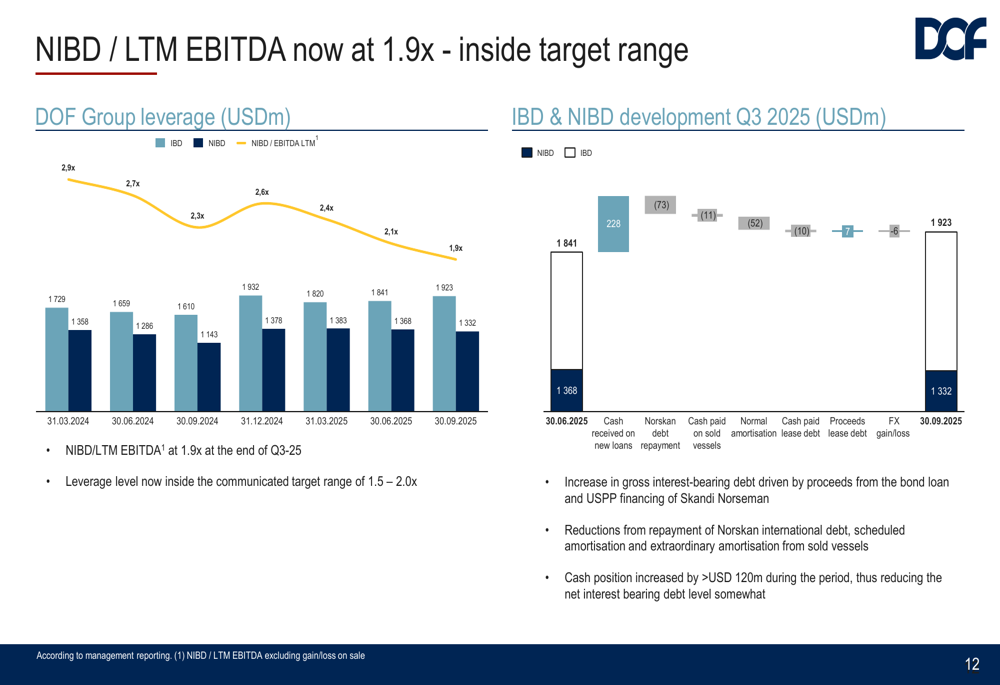

The company's leverage position also improved, with the NIBD/LTM EBITDA ratio reaching 1.9x at the end of Q3, now within the company's target range of 1.5-2.0x. This represents a significant improvement in the company's debt position.

As illustrated in this chart showing DOF Group's leverage development:

Strategic Initiatives

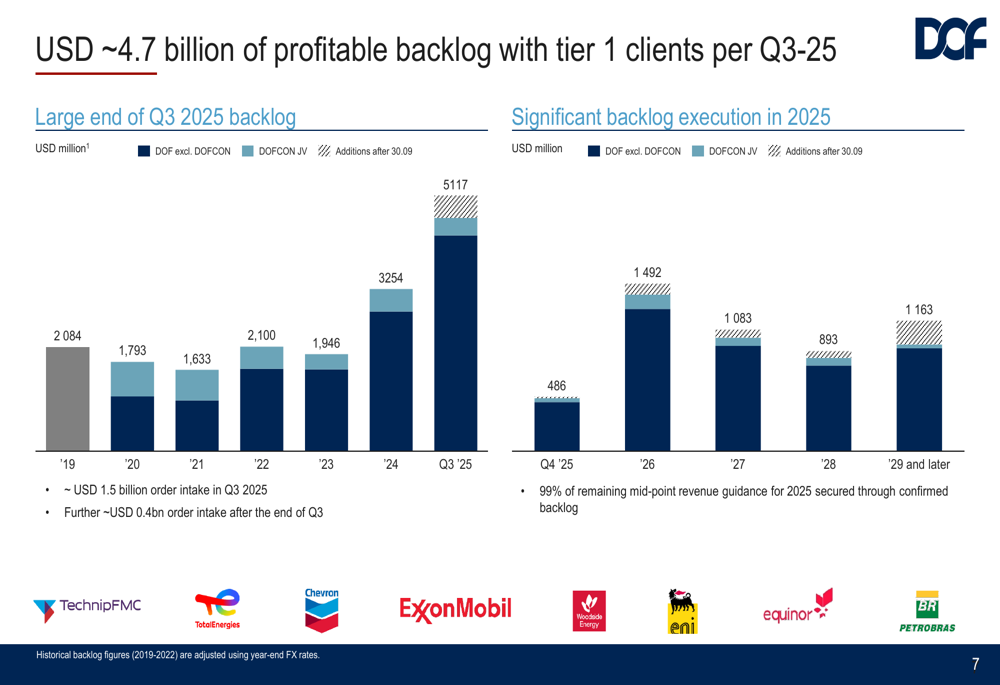

DOF Group secured $1.5 billion in new orders during Q3 2025, with an additional $0.4 billion in orders after the quarter's end. This activity has built the company's backlog to $4.7 billion, providing strong revenue visibility for the coming years. The company noted that 99% of the remaining mid-point revenue guidance for 2025 is already secured through confirmed backlog.

The following chart illustrates DOF's growing backlog and its distribution across future periods:

Significant contract awards during and after Q3 include several multi-year contracts with major clients such as Petrobras, Equinor, and TotalEnergies. Notably, DOF secured a three-year PIDF (service contracts) in Brazil worth approximately $390 million, encompassing more than 4,000 planned inspections with commencement in H1 2026.

The company also announced the extension of PLSV (Pipelay Support Vessel) contracts in Brazil, securing backlog through 2030. Three of DOFCON's PLSVs had contracts with Petrobras extended, with the commencement of new contracts shifted to Q1 2027, adding approximately $100 million to DOF's backlog.

As part of its fleet optimization strategy, DOF sold three of its lowest-capacity AHTS vessels during Q3. Two vessels, Skandi Tender and Skandi Trader, were delivered to their new owner during the quarter, while Skandi Handler is scheduled for delivery to its buyer in Q4.

Detailed Financial Analysis

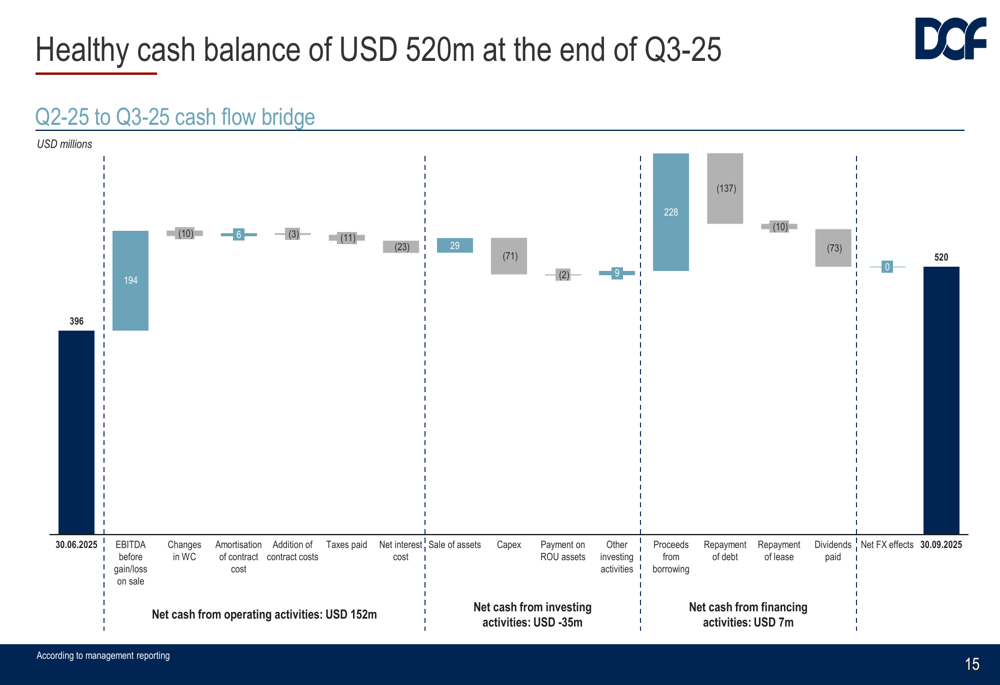

DOF Group's cash flow remained strong during Q3 2025, with net cash from operating activities of $152 million. The company ended the quarter with a healthy cash balance of $520 million, representing an increase of over $120 million from the previous quarter.

The following cash flow bridge illustrates the movement of funds during Q3 2025:

The company has also made significant progress in improving its debt profile. During the quarter, DOF repaid Norskan's international debt of $78 million, eliminating all balloon maturities prior to 2030. Additionally, the company secured funding for its newbuild vessel, Skandi Norseman, through the issuance of $140 million in Senior Secured US Private Placement notes.

DOF Group increased its quarterly dividend to $0.35 per share, to be paid on November 27, 2025. This brings the total dividends paid and declared year-to-date to $234 million, reflecting the company's strong cash generation and commitment to shareholder returns.

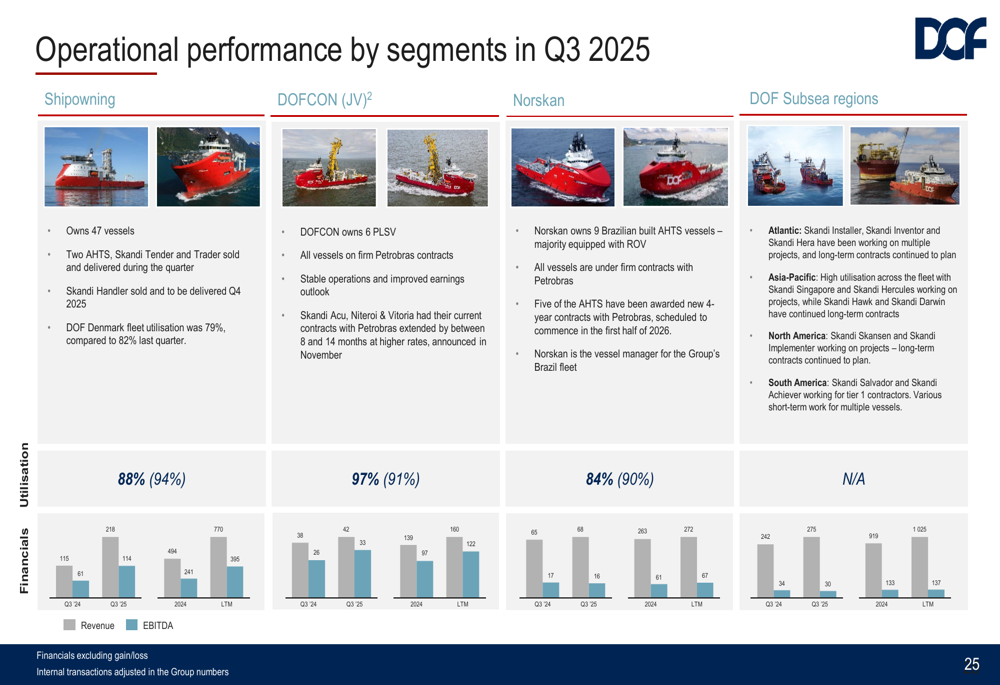

The operational performance across DOF's segments shows the diversity and strength of the company's business model:

Forward-Looking Statements

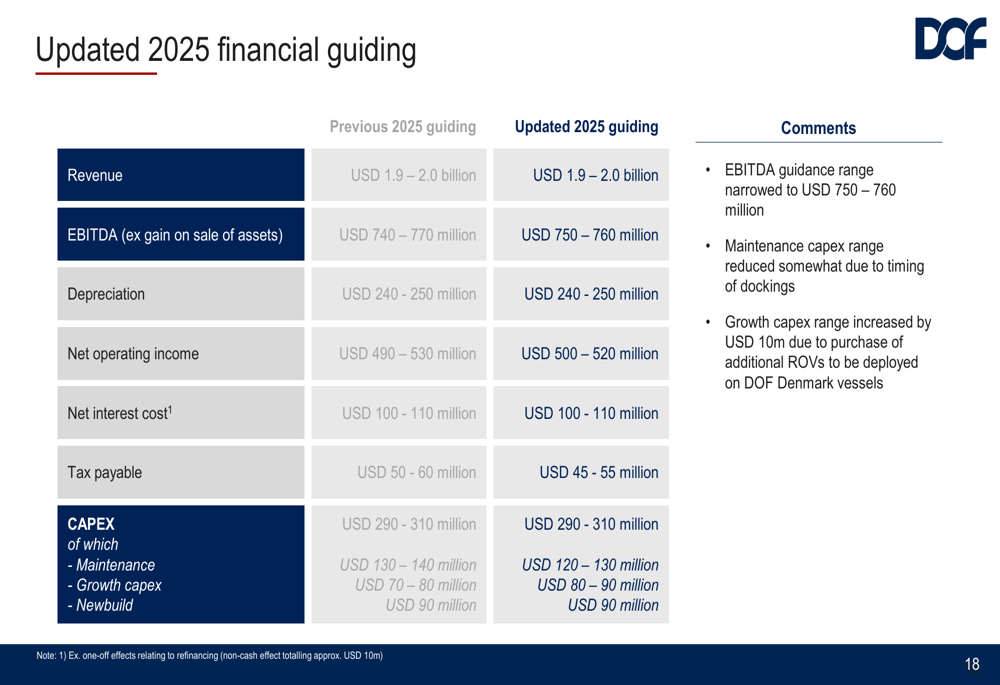

DOF Group narrowed its 2025 EBITDA guidance to $750-760 million, reflecting confidence in its full-year performance. The company maintained its revenue guidance at $1.9-2.0 billion and expects depreciation of $240-250 million and capital expenditures of $290-310 million for the year.

The following table shows DOF's updated financial guidance for 2025:

The company expressed optimism about future prospects, citing an all-time high backlog and continued high tendering activity across regions. With 99% of the remaining 2025 revenue already secured and significant contracts extending into 2030, DOF Group appears well-positioned to maintain its strong performance.

Management highlighted the company's integrated service model and global presence as key competitive advantages in the current market environment. The combination of vessel ownership and specialized subsea services has enabled DOF to secure long-term contracts with tier-one clients, providing stability and visibility for future earnings.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.