Treasury Secretary Bessent announces tariff relief on coffee, fruits

Introduction & Market Context

Dropbox Inc. (NASDAQ:DBX) released its Q3 2025 financial results presentation on November 6, showcasing strong profitability metrics despite facing headwinds in user growth. The cloud storage and productivity company reported earnings per share of $0.74, beating analyst expectations by 15.63%, while revenue reached $634 million, exceeding forecasts by 2.3%.

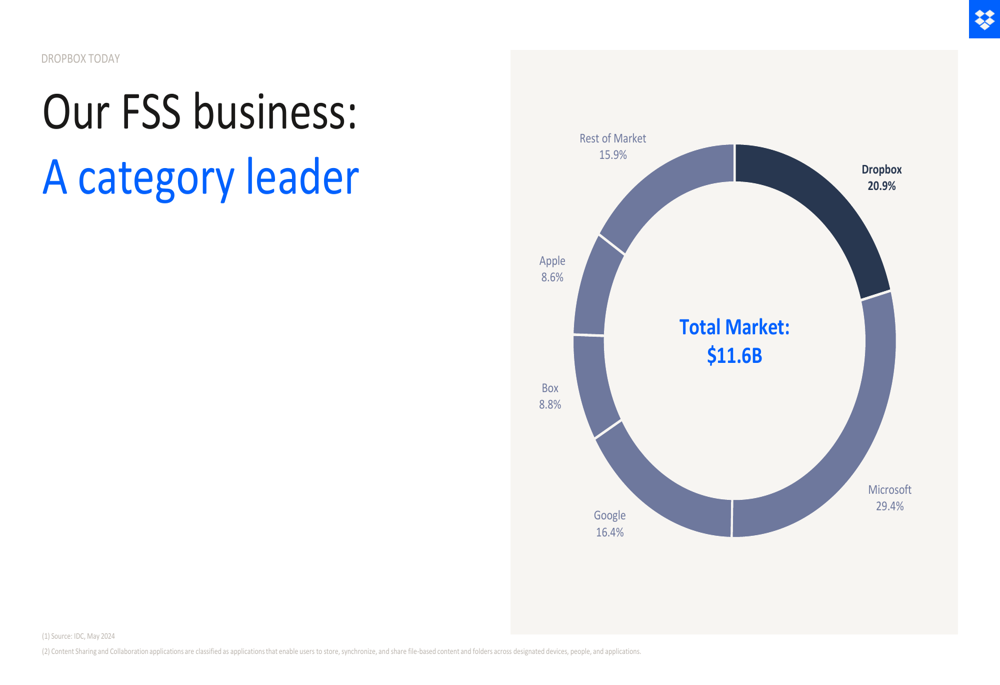

The company operates in the competitive File Sync and Share (FSS) market, where it maintains a 20.9% market share, second only to Microsoft at 29.4%. With over 700 million registered users and 18.07 million paying customers, Dropbox continues to leverage its established position while pivoting toward AI-enhanced productivity tools to drive future growth.

As shown in the following chart of Dropbox’s market position within the FSS category:

Quarterly Performance Highlights

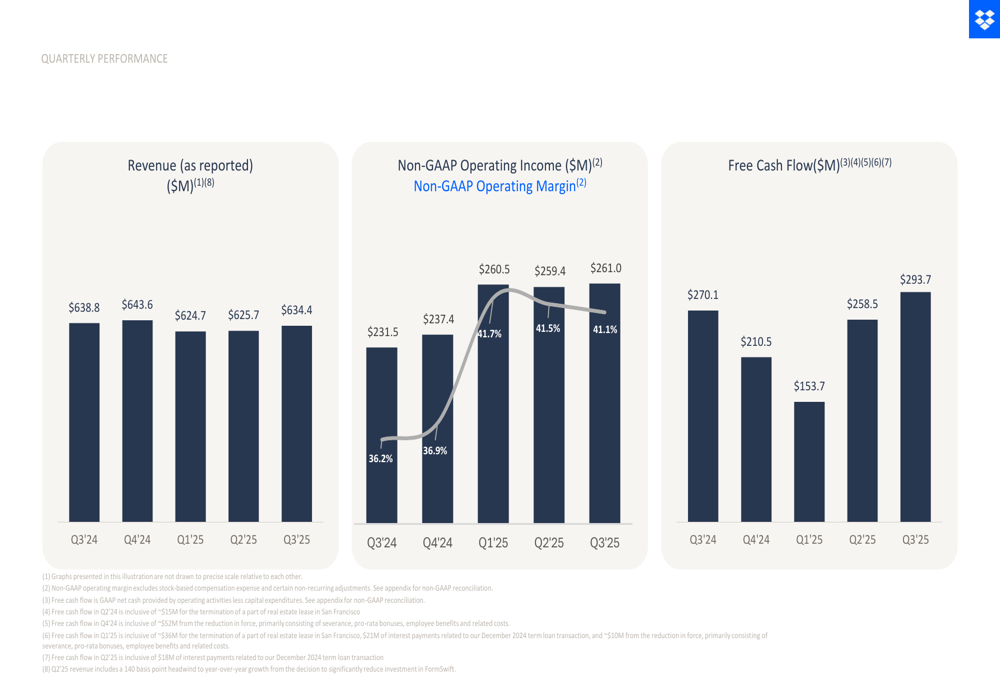

Dropbox reported Q3 2025 revenue of $634.4 million, representing a 70 basis point decline year-over-year but showing sequential improvement from Q2. Despite this modest revenue challenge, the company demonstrated impressive profitability with non-GAAP operating income of $261 million and an operating margin of 41.1%, significantly improved from 36.2% in the same quarter last year.

The company’s financial performance is illustrated in this quarterly breakdown:

Free cash flow performance was particularly strong at $293.7 million, representing a 39% increase year-over-year. This cash generation capability has enabled Dropbox to continue its aggressive share repurchase program, which has reduced diluted weighted average shares outstanding to 279 million in 2025 YTD, down from 323 million in 2024.

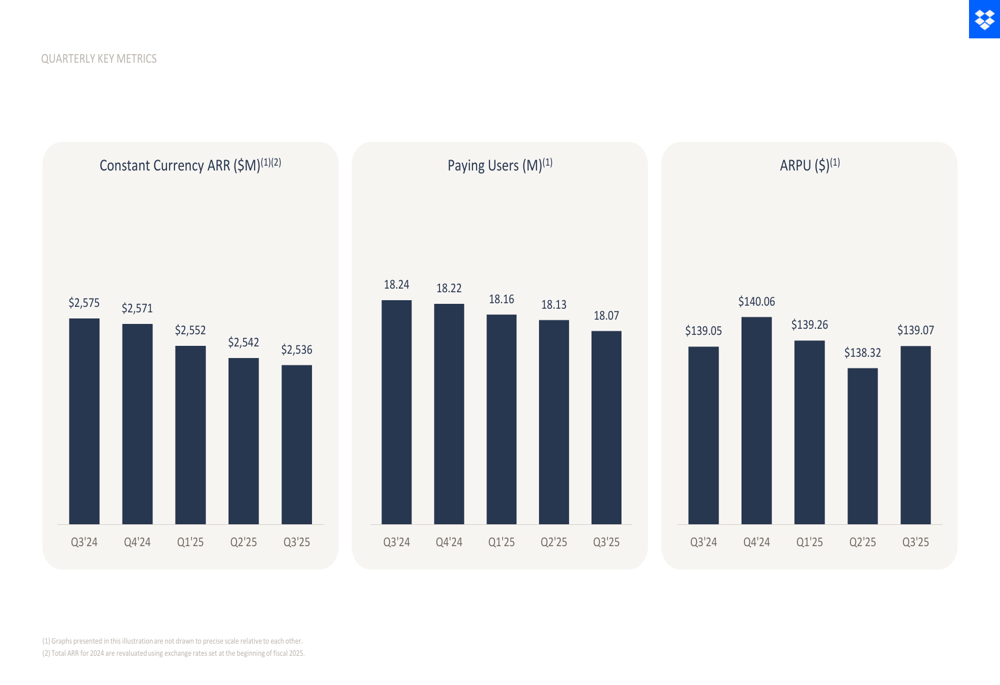

The company’s key operational metrics showed some pressure, with paying users declining slightly to 18.07 million from 18.24 million a year earlier. Average Revenue Per User (ARPU) remained relatively stable at $139.07, compared to $139.05 in Q3 2024.

As shown in the following quarterly metrics chart:

Strategic Initiatives

Dropbox is actively addressing growth challenges in its core business by expanding into AI-powered productivity tools, most notably with its new product "Dash." The company positions Dash as an "AI teammate" that helps users search across files and applications, draft content, summarize information, and organize work from a single interface.

CEO Drew Houston emphasized the strategic importance of this initiative during the earnings call, stating, "We believe and we see there’s a lot of important technical and design work that we’re doing with Dash to take AI the last mile at work."

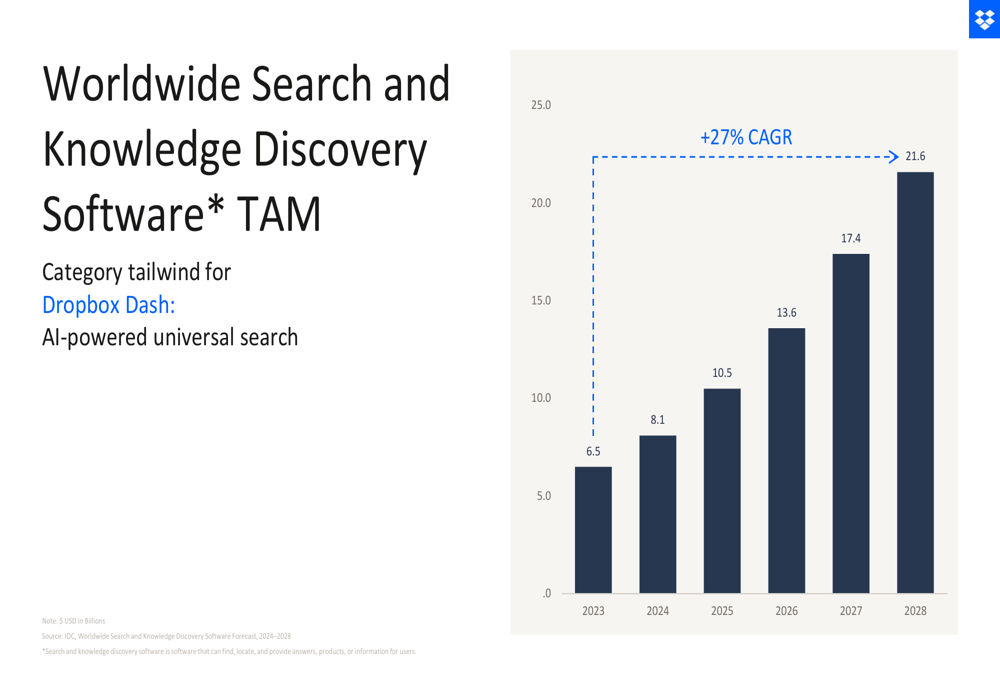

The company is targeting the Search and Knowledge Discovery Software market with Dash, a sector projected to grow at a 27% CAGR from 2023 to 2028, reaching $21.6 billion by 2028. Dropbox has implemented a multi-pronged go-to-market strategy for Dash, including managed sales for larger SMBs, self-serve options for small teams, and integration with its existing FSS product for its installed base.

As illustrated in this chart showing the projected growth of the Search and Knowledge Discovery Software market:

Additionally, Dropbox announced the strategic acquisition of Mobius Labs to enhance its AI capabilities, though specific details about this acquisition were not included in the presentation.

Competitive Industry Position

Dropbox continues to be recognized as a leader in its category, as evidenced by its positioning in G2’s evaluation of Cloud Content Collaboration Software. The company scores highly on both customer satisfaction and market presence, reinforcing its strong competitive position despite facing competition from larger tech companies.

The following chart illustrates Dropbox’s leadership position according to G2:

The company’s core value proposition centers around three key pillars: securing content with robust compliance and authentication features, organizing files with smart search and collaboration tools, and sharing content with advanced controls and permission management.

Dropbox has built a substantial infrastructure to support its services, including core data centers, network points of presence, and public data centers distributed globally. This infrastructure manages over 4,700 petabytes of customer storage as of 2024.

Forward-Looking Statements

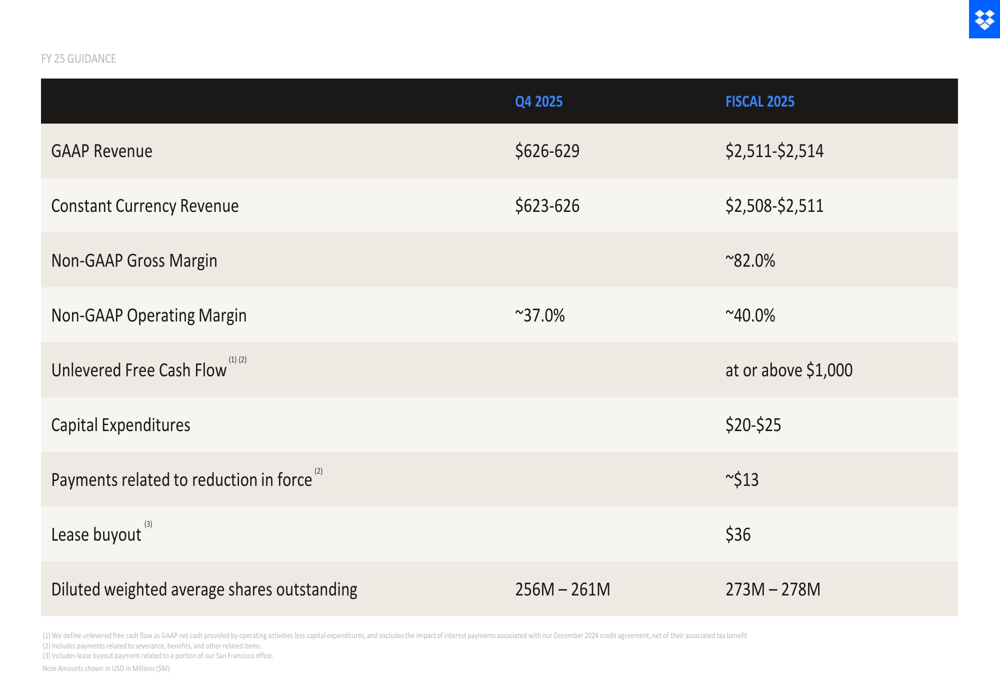

Dropbox raised its full-year 2025 revenue guidance to between $2.511 billion and $2.514 billion, reflecting confidence in its near-term outlook despite the competitive landscape. For Q4 2025, the company expects revenue between $626-629 million.

The financial guidance also projects non-GAAP gross margin of approximately 82.0% and non-GAAP operating margin of approximately 40.0% for the full year. Unlevered free cash flow is expected to reach or exceed $1 billion.

As detailed in the following guidance slide:

The company maintains a strong liquidity position with $925 million in cash and investments as of Q3 2025, plus $1.55 billion in remaining availability on its delayed draw term loan, for total liquidity of $2.475 billion. This provides Dropbox with significant financial flexibility as it continues to invest in AI capabilities while returning capital to shareholders.

Looking ahead, key focus areas include scaling the Dash product and strengthening the self-serve Teams business. Management indicated during the earnings call that the initial focus for Dash is on driving adoption rather than immediate revenue generation, suggesting a longer-term strategy for this new product line.

While Dropbox faces ongoing challenges with slight declines in its user base and constant currency ARR, the company’s strong profitability metrics and strategic pivot toward AI-enhanced productivity tools position it to navigate the evolving competitive landscape in cloud storage and collaboration software.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.