Bitcoin price today: gains to $120k, near record high on U.S. regulatory cheer

Introduction & Market Context

Farmers & Merchants Bancorp, Inc. (NASDAQ:FMAO) released its first quarter 2025 investor presentation highlighting continued growth across key metrics. The Ohio-based community bank, which serves markets across the Midwest, reported record net interest income and deposit levels while maintaining its 30-year streak of dividend increases.

Trading at $24.72 in after-hours trading on May 6, 2025, FMAO shares have declined 1.1% from their previous close of $25.10, though they remain well above their 52-week low of $19.95.

The presentation emphasized F&M’s strong market position across Northwest Ohio, Northeast Indiana, and Southern Michigan, where it has established itself as a leading community bank with particular expertise in agricultural lending.

Quarterly Performance Highlights

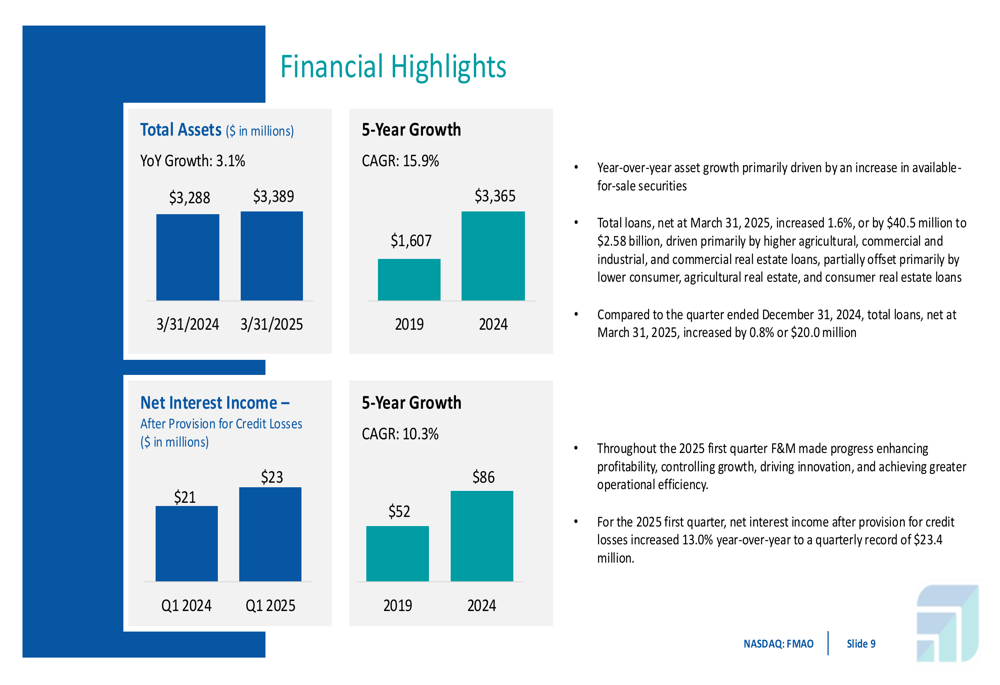

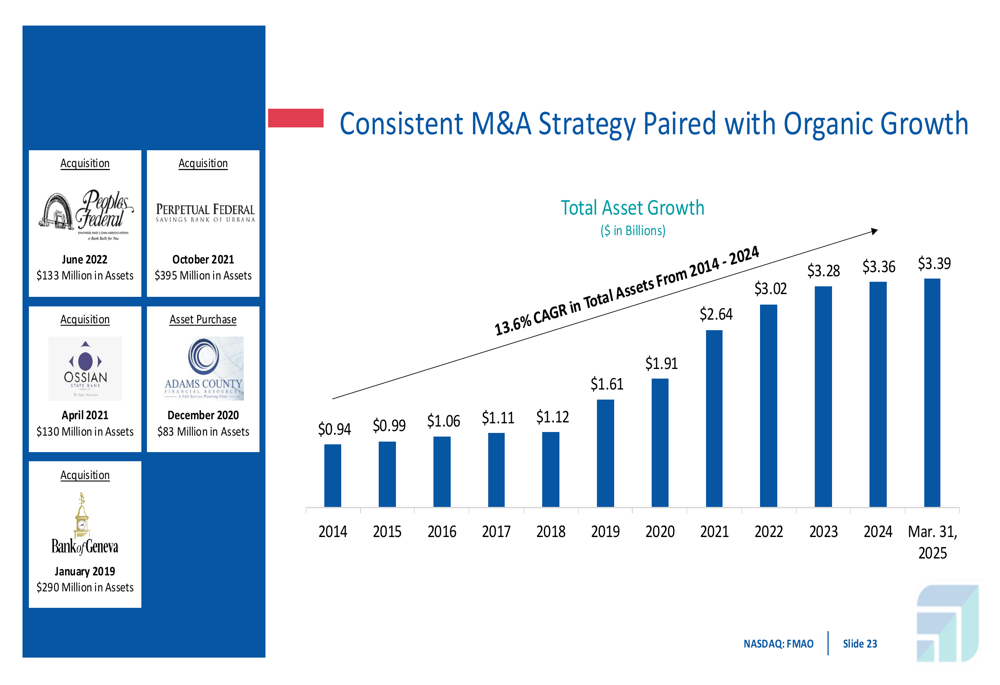

F&M reported total assets of $3.389 billion as of March 31, 2025, representing a 3.1% year-over-year increase. This continues a pattern of consistent growth, with the company achieving a five-year compound annual growth rate (CAGR) of 15.9% in total assets from 2019 to 2024.

Net interest income reached a quarterly record of $23.4 million, up 13.0% compared to the same period last year. The bank has maintained a 10.3% five-year CAGR in this key metric, demonstrating consistent earnings power.

As shown in the following financial highlights chart:

Total (EPA:TTEF) deposits increased 3.0% year-over-year to a record $2.70 billion, while total loans grew 1.6% or $40.5 million to $2.58 billion. The company noted that new offices opened in 2023 contributed $53.9 million in new deposits and $80.5 million in new loans during 2024, validating its expansion strategy.

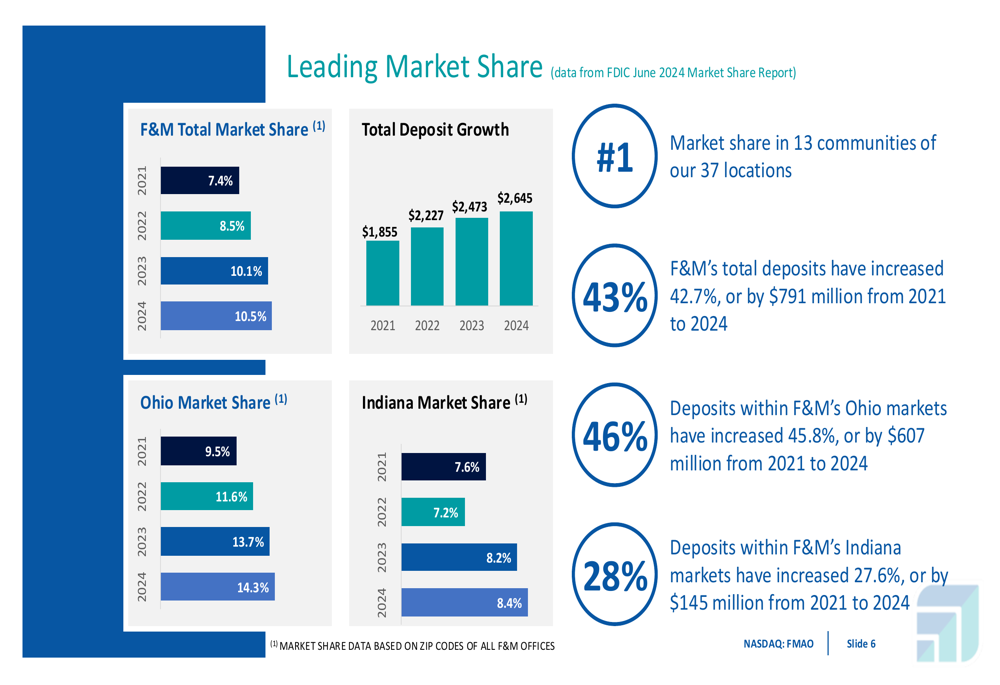

F&M’s market share continues to strengthen, with the bank holding the #1 position in 13 of its 37 locations. Total deposits have increased by 42.7% ($791 million) from 2021 to 2024, reflecting both organic growth and strategic acquisitions.

The following chart illustrates F&M’s leading market share growth:

On March 25, 2025, the Board of Directors declared a cash dividend of $0.22125 per share, representing a 0.6% increase from the prior year. This marks the 30th consecutive year of dividend increases, underscoring the company’s commitment to shareholder returns.

The presentation highlighted that F&M’s total shareholder return from December 31, 2011, to December 31, 2024, significantly outperformed the KBW Regional Banking Index ($492 versus $343 for an initial investment).

Strategic Initiatives

F&M outlined its strategic priorities for 2025, focusing on enhancing profitability, controlling growth, driving innovation, and achieving greater operational efficiency. The bank has implemented a new three-year strategic plan aimed at creating long-term shareholder value.

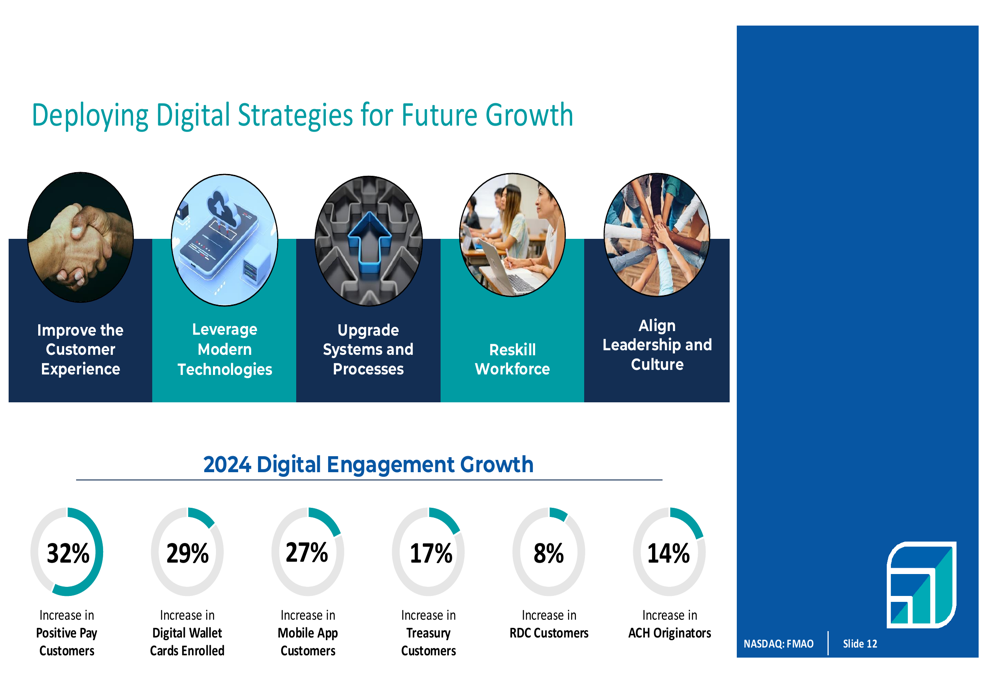

The company’s growth strategy encompasses five key pillars as illustrated below:

Digital transformation remains a priority, with the presentation highlighting significant year-over-year increases in digital engagement metrics. In 2024, the bank saw a 32% increase in positive pay customers, 29% growth in digital wallet cards enrolled, and 27% growth in mobile app customers.

The following chart details F&M’s digital strategy progress:

Agricultural lending continues to be a core strength for F&M, which has been recognized as a Top 100 Farm Lending Bank. The bank’s agricultural loan portfolio reached $370 million as of March 31, 2025, representing steady growth from $283 million in 2020. F&M emphasized that its agricultural business benefits from diversification and historically inverse cycles with commercial loan performance.

Financial Position and Asset Quality

F&M maintains a strong capital and liquidity position, with $611.6 million in total cash, cash equivalents, and securities available for sale as of March 31, 2025. The bank reported a total risk-based capital ratio of 12.83% and a Tier 1 leverage ratio of 8.44%, both well above regulatory requirements.

The presentation highlighted that only approximately 12.1% of total deposits are uninsured, reflecting a stable funding base. The bank has proactively balanced its loan portfolio between fixed and variable rate loans, with approximately 33% of the portfolio subject to repricing within the next 12 months.

Asset quality remains robust, with allowance for credit losses to total loans at 1.08%, non-performing assets to total assets at just 0.13%, and net charge-offs to loans at a minimal 0.01%. The bank’s commercial real estate (CRE) portfolio, which comprises 51.3% of total loans, is well-diversified with only 5.4% exposure to office properties.

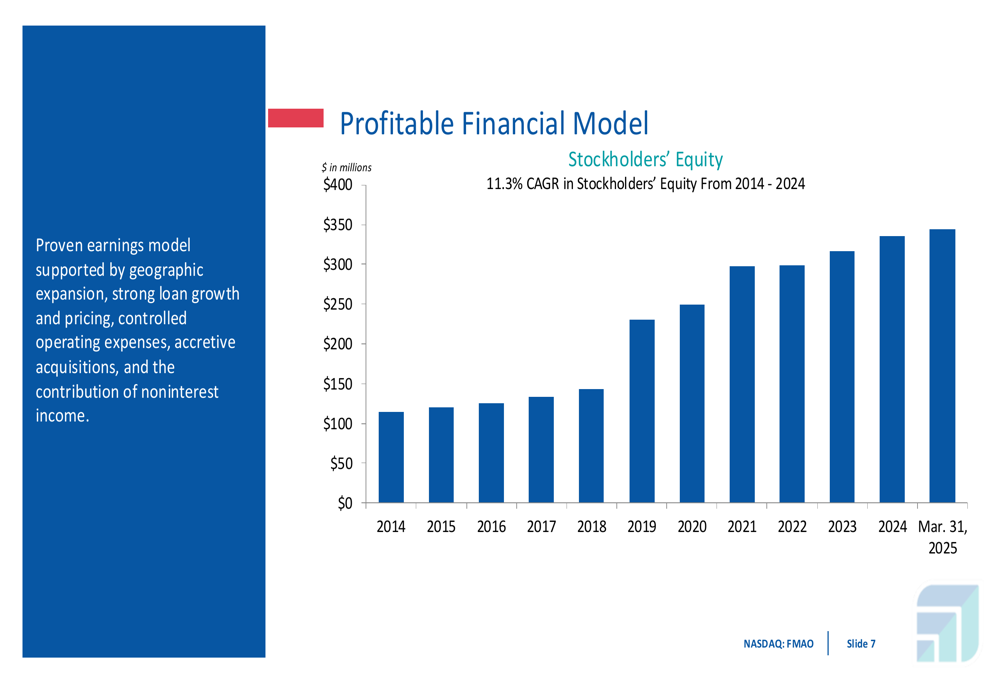

The company’s stockholders’ equity has grown at a compound annual rate of 11.3% from 2014 to 2024, as illustrated in the following chart:

Forward-Looking Statements

Looking ahead, F&M expects to benefit from its strategic initiatives and balanced approach to growth. The bank plans to continue pursuing accretive acquisitions while also focusing on organic growth opportunities.

The presentation emphasized that F&M’s variable rate loan mix positions it well for the current interest rate environment, with approximately 33% of loans subject to repricing in the next 12 months. This is expected to benefit the yield on earning assets, profitability, and liquidity in coming quarters.

F&M’s total asset growth has been impressive, with a 13.6% CAGR from 2014 to 2024, driven by both organic expansion and strategic acquisitions:

The bank’s vision of being "Community vested to help people realize their best lives" and mission to "nurture lasting relationships" underscores its community banking focus:

As F&M continues to execute on its strategic plan, management expressed confidence in the bank’s ability to enhance profitability while maintaining its strong market position and commitment to the communities it serves.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.