Goldman Sachs expects Nvidia ’beat and raise,’ lifts price target to $240

Introduction & Market Context

First Citizens BancShares (NASDAQ:FCNCA) presented its third quarter 2025 earnings results on October 23, 2025, highlighting solid loan and deposit growth amid strategic expansion efforts. The company’s stock responded positively to the results, rising 1.5% to $1,768.67 in regular trading, after gaining 2.15% in pre-market activity.

The bank reported adjusted earnings per share of $44.62, exceeding analyst expectations of $41.94, representing a 6.4% positive surprise. However, net income declined year-over-year as the company navigated a changing interest rate environment and increased provisions for credit losses.

First Citizens’ presentation revealed its continued integration of SVB assets and a new expansion initiative through the acquisition of 138 BMO Bank branches, demonstrating its strategic focus on growth despite macroeconomic challenges.

Quarterly Performance Highlights

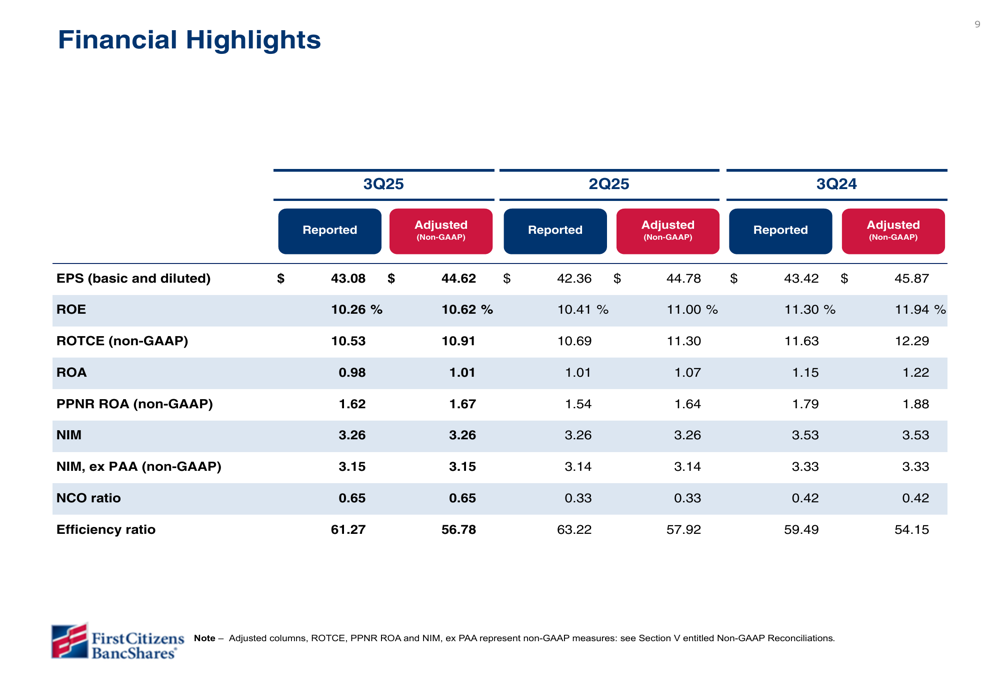

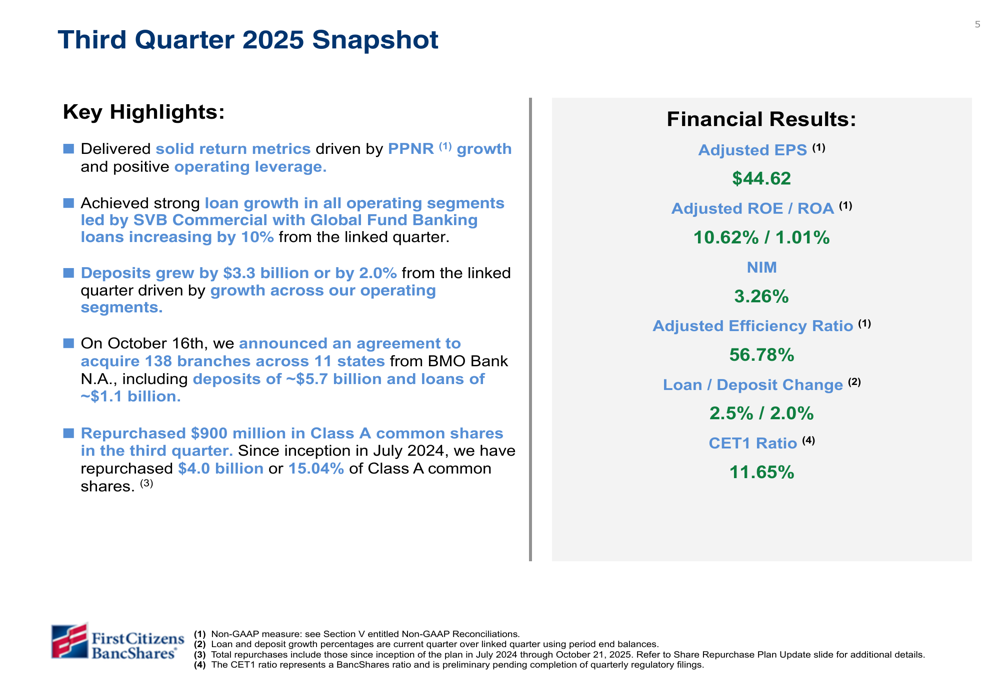

First Citizens delivered solid financial performance in Q3 2025, with adjusted return metrics driven by pre-provision net revenue growth and positive operating leverage. The company achieved an adjusted return on equity of 10.62% and return on assets of 1.01%, though both metrics declined from the year-ago period.

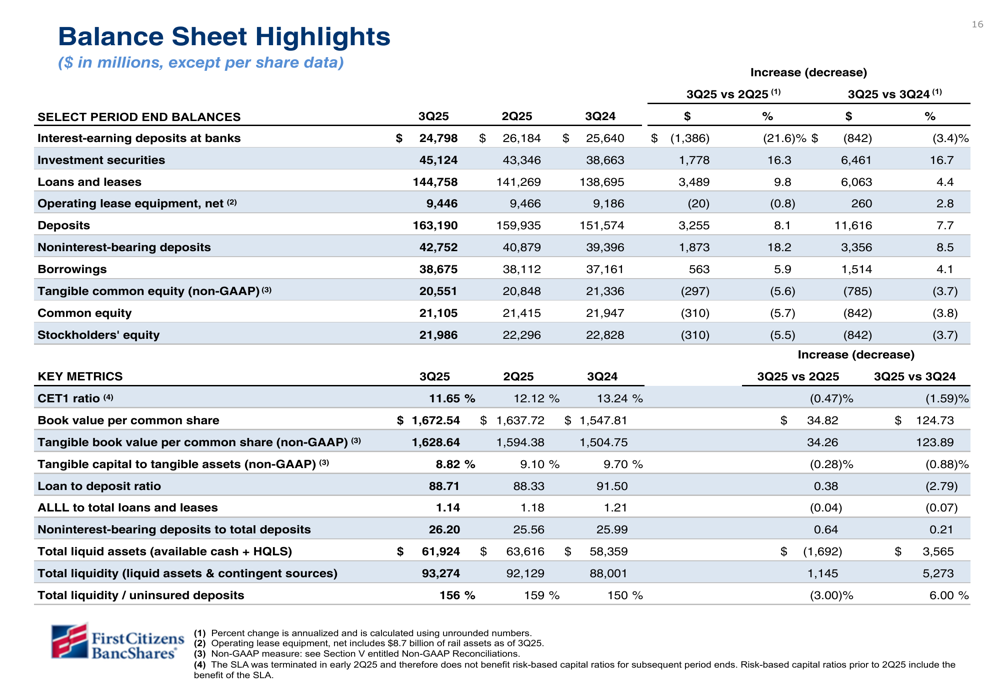

As shown in the following financial highlights table, the company maintained stable performance across key metrics compared to the previous quarter, while showing some decline from the prior year:

Loan growth was particularly strong, increasing by $3.5 billion or 2.5% from the linked quarter, with growth across all operating segments. The SVB Commercial segment led this expansion with Global Fund Banking loans increasing by 10% quarter-over-quarter. Total deposits also grew by $3.3 billion or 2.0% from the previous quarter, marking seven consecutive quarters of deposit growth.

The following snapshot provides a comprehensive overview of the quarter’s key highlights and financial results:

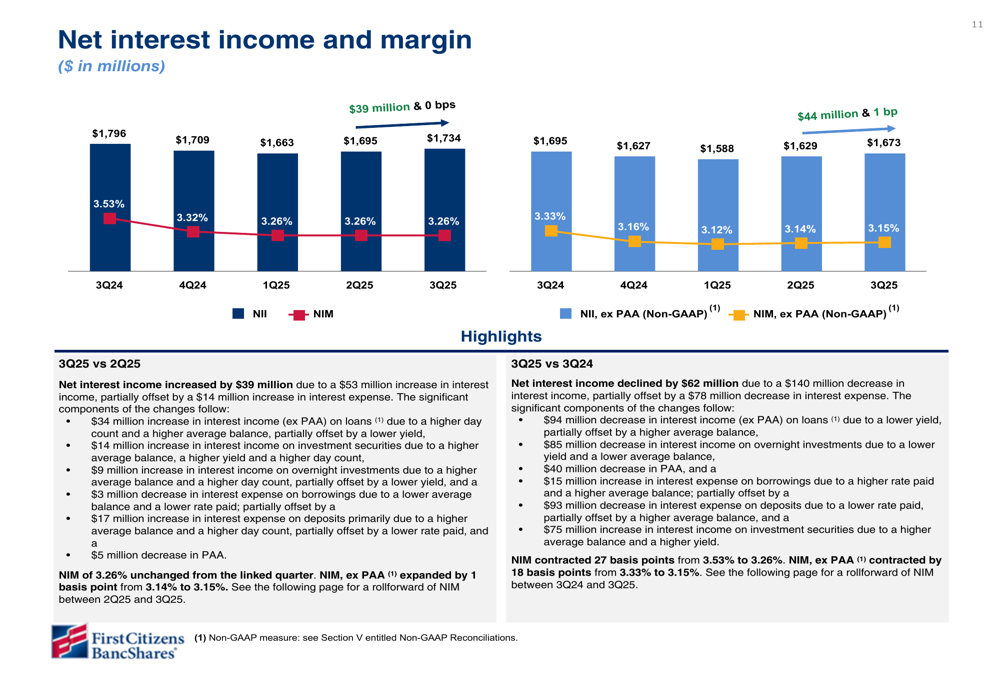

Net interest income increased by $39 million or 2.3% quarter-over-quarter, though it decreased by $62 million or 3.5% year-over-year. The net interest margin remained stable at 3.26% compared to the previous quarter, while the efficiency ratio improved from 57.92% to 56.78%.

Detailed Financial Analysis

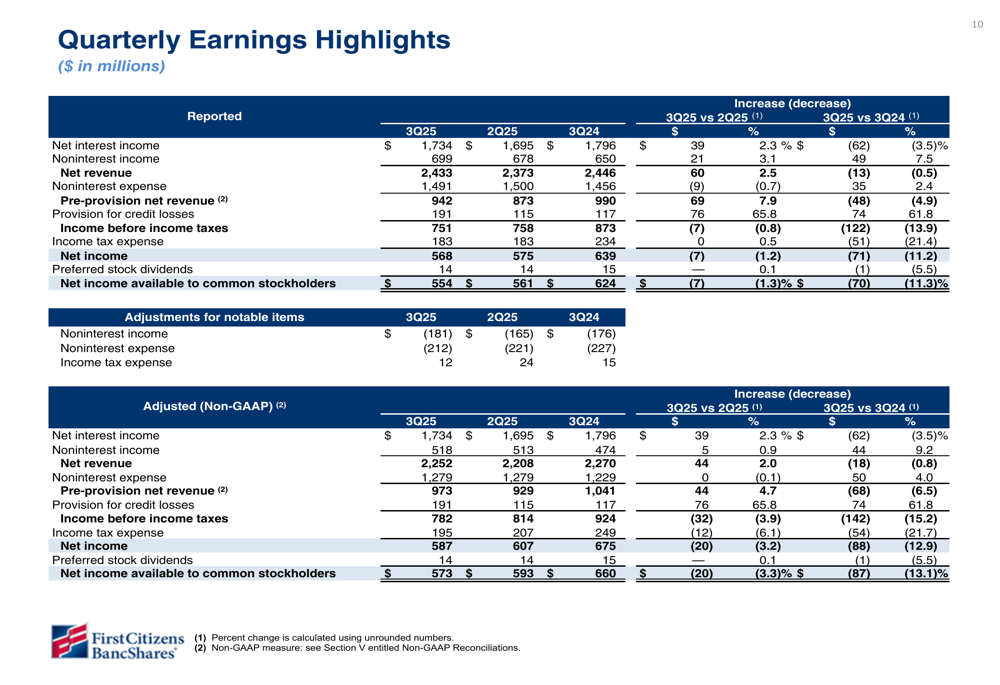

First Citizens’ quarterly earnings breakdown reveals the components driving its financial performance. While net revenue increased by 2.5% from the linked quarter, it decreased slightly by 0.5% year-over-year. The company’s pre-provision net revenue showed strong growth of 7.9% quarter-over-quarter, though it declined by 4.9% compared to the same period last year.

The following chart details the quarterly earnings components:

Net interest income and margin trends show stability in the face of a changing rate environment. The company’s net interest margin (NIM) remained unchanged at 3.26% from the linked quarter, with NIM excluding purchase accounting adjustments (PAA) expanding by 1 basis point to 3.15%.

The following chart illustrates the net interest income and margin trends:

A significant factor in the quarter’s results was the provision for credit losses, which increased by $76 million or 65.8% from the linked quarter to $191 million. This increase was partly attributed to a large, individual client loss in the Commercial Bank segment, though the company described overall credit quality as "stable."

The company’s balance sheet continued to strengthen, with total assets reaching $233.1 billion. The loan-to-deposit ratio increased slightly to 88.71% from 88.33% in the previous quarter, while noninterest-bearing deposits as a percentage of total deposits improved to 26.20% from 25.56%.

The following balance sheet highlights provide a comprehensive overview:

Strategic Initiatives & Expansion

First Citizens announced a significant expansion through the acquisition of 138 branches from BMO Bank N.A., spanning 11 states. This transaction, announced on October 16th, includes approximately $5.7 billion in deposits and $1.1 billion in loans, further enhancing the company’s geographic footprint and deposit base.

The company’s capital return strategy remained aggressive, with $900 million in Class A common shares repurchased during the third quarter. Since the inception of the repurchase program in July 2024, First Citizens has repurchased $4.0 billion or 15.04% of Class A common shares, demonstrating its commitment to returning capital to shareholders while maintaining a strong CET1 ratio of 11.65%.

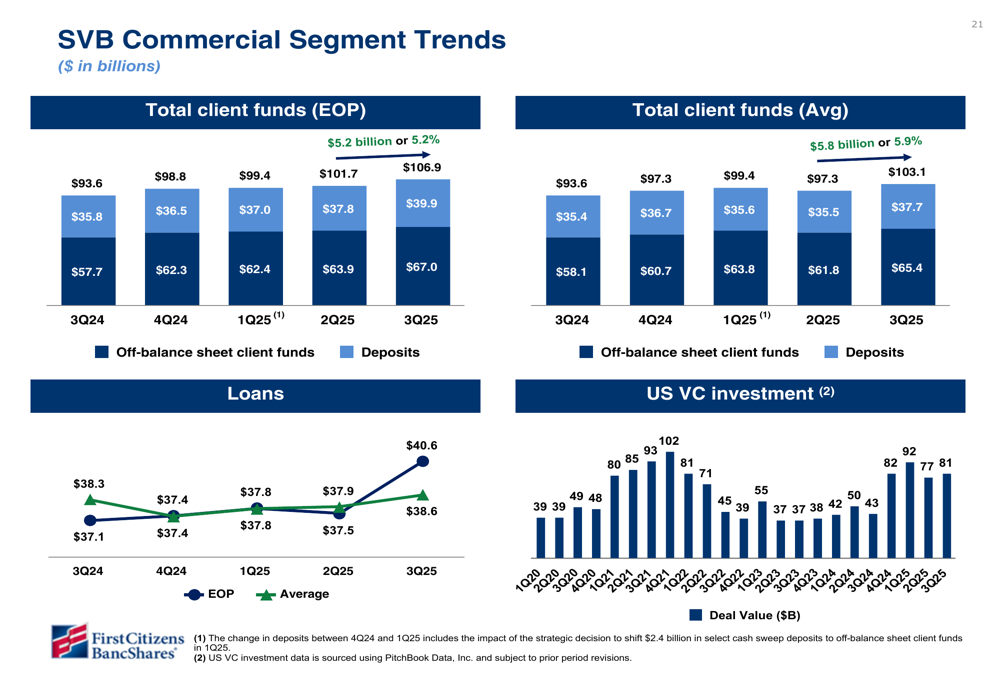

The SVB Commercial segment continued to show strong performance, with total client funds reaching $106.9 billion at the end of the quarter, up from $101.7 billion in the previous quarter. The following chart illustrates the positive trends in this segment:

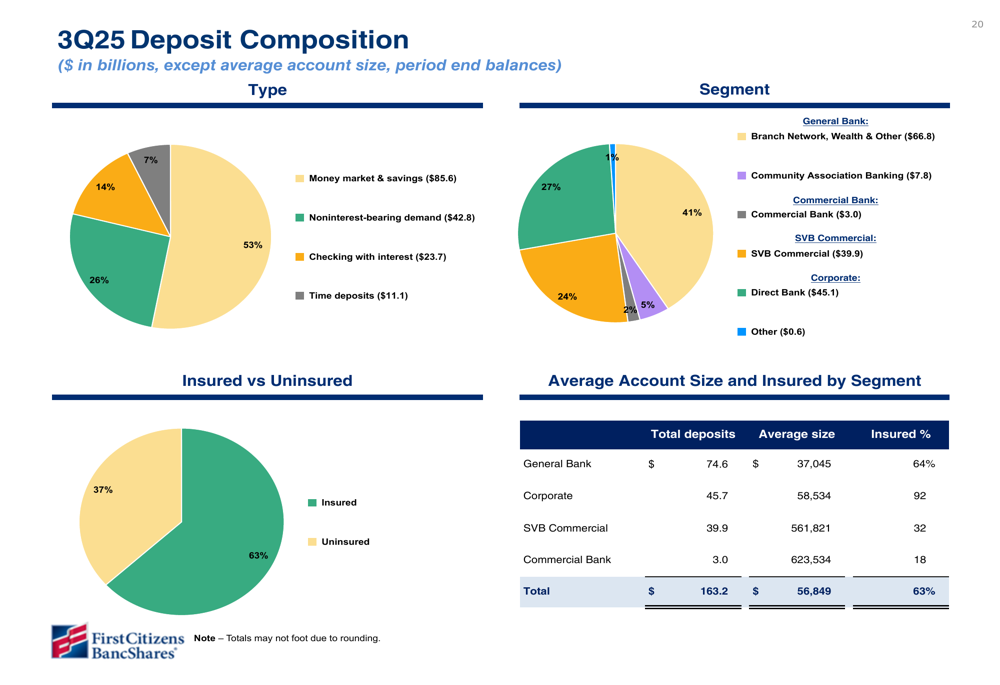

The company’s deposit composition remains diversified, with money market and savings accounts comprising the largest portion at $85.6 billion, followed by noninterest-bearing demand deposits at $42.8 billion. The company’s deposit base is 37% insured and 63% uninsured, with significant variations in insurance coverage across segments.

The following deposit breakdown provides insights into the composition:

Forward-Looking Statements

First Citizens outlined its strategic priorities for 2025, focusing on four key areas: client focus, talent and culture, operational efficiency, and balance sheet optimization. The company emphasized risk management as a foundational element underlying all priorities.

The company’s financial outlook projects Q4 loan growth in the range of $143-$146 billion and deposits between $161-$165 billion. Net interest income is expected to remain stable, with full-year guidance set between $6.74-$6.84 billion. The company anticipates two potential Federal Reserve rate cuts in 2026, which could impact future net interest margins.

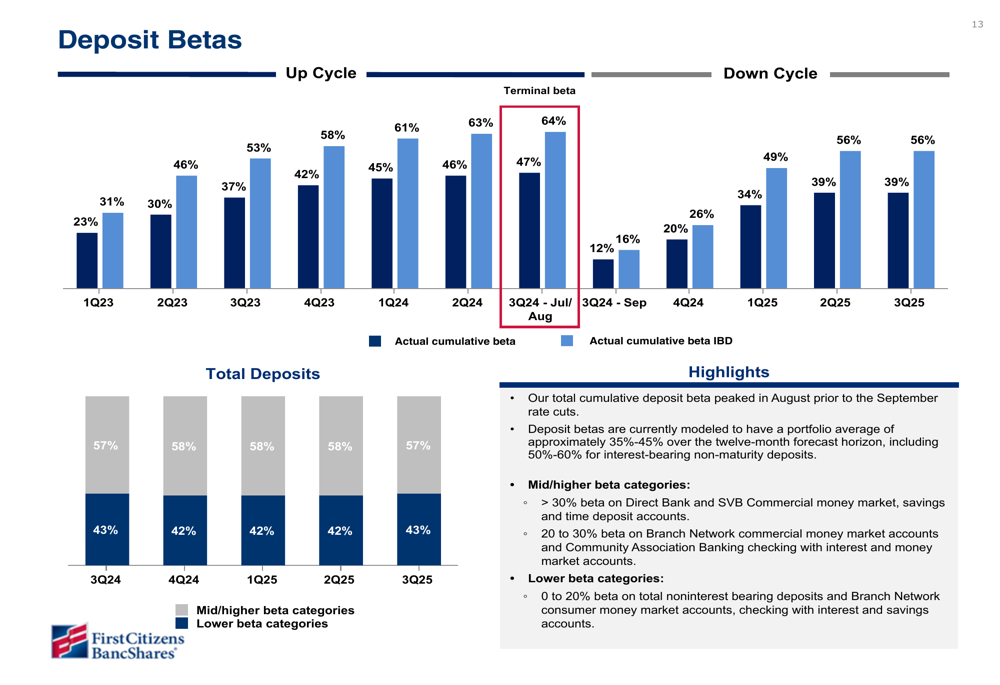

Deposit betas are currently modeled to have a portfolio average of approximately 35%-45% over the twelve-month forecast horizon, including 50%-60% for interest-bearing non-maturity deposits. The following chart illustrates the deposit beta trends:

CEO Frank Holding expressed the company’s commitment to being "a dependable, thoughtful partner to our clients, communities, and shareholders," while CFO Craig Nix highlighted the company’s "consistent performance" in delivering strong financial results.

Despite the positive outlook, First Citizens faces several challenges, including macroeconomic uncertainties, integration risks associated with the BMO Bank branch acquisition, maintaining growth momentum in a competitive banking environment, potential credit quality issues, and regulatory challenges related to advancing Category 3 readiness.

The company’s strategic focus on growth and efficiency, combined with its strong capital position and expanding footprint, positions it well to navigate these challenges while continuing to deliver value to shareholders.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.