Bitcoin set for a rebound that could stretch toward $100000, BTIG says

Introduction & Market Context

Intel Corporation (NASDAQ:INTC) presented its third quarter 2025 earnings on October 23, showcasing results that exceeded expectations across key metrics. The company reported its fourth consecutive quarter of solid performance, with AI-driven demand emerging as a significant growth catalyst across business segments.

Following the earnings announcement, Intel's stock rose by 3.37% to $36.92 in after-hours trading, reflecting positive investor sentiment about the company's performance and strategic direction. The stock has delivered impressive returns year-to-date, approaching its 52-week high of $39.65.

Executive Summary

Intel's presentation highlighted four key areas of progress: consistent financial performance, balance sheet improvements, AI-driven demand, and cultural and execution enhancements. The company emphasized meaningful progress in strengthening its financial position through partnerships with the U.S. Government, NVIDIA, and SoftBank Group, as well as through monetization of assets including Altera and Mobileye.

As shown in the executive summary slide, Intel is focusing on streamlining operations, engineering focus, and increased collaboration through return-to-office initiatives:

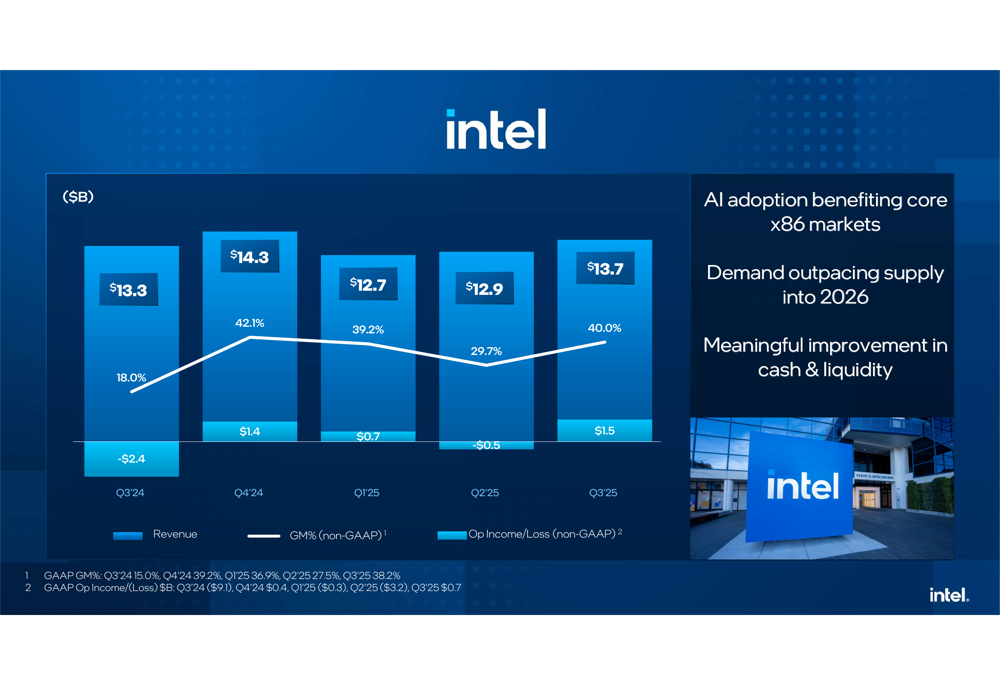

Quarterly Performance Highlights

Intel reported Q3 2025 revenue of $13.7 billion, up 2.8% year-over-year and $0.6 billion above the July outlook. The company's gross margin reached 40.0% (non-GAAP), a substantial improvement of 22.0 percentage points year-over-year and 4.0 percentage points above guidance. Earnings per share came in at $0.23, up $0.69 year-over-year and significantly above the July outlook.

The following slide illustrates these key financial metrics, highlighting the company's performance relative to expectations:

Intel's financial performance over the past five quarters shows a pattern of improving profitability despite revenue fluctuations. The company returned to operational profitability in Q3 with $1.5 billion in non-GAAP operating income, compared to a loss of $2.4 billion in the same quarter last year.

As shown in the quarterly trend chart below, gross margins have stabilized around 40% after significant volatility in previous quarters:

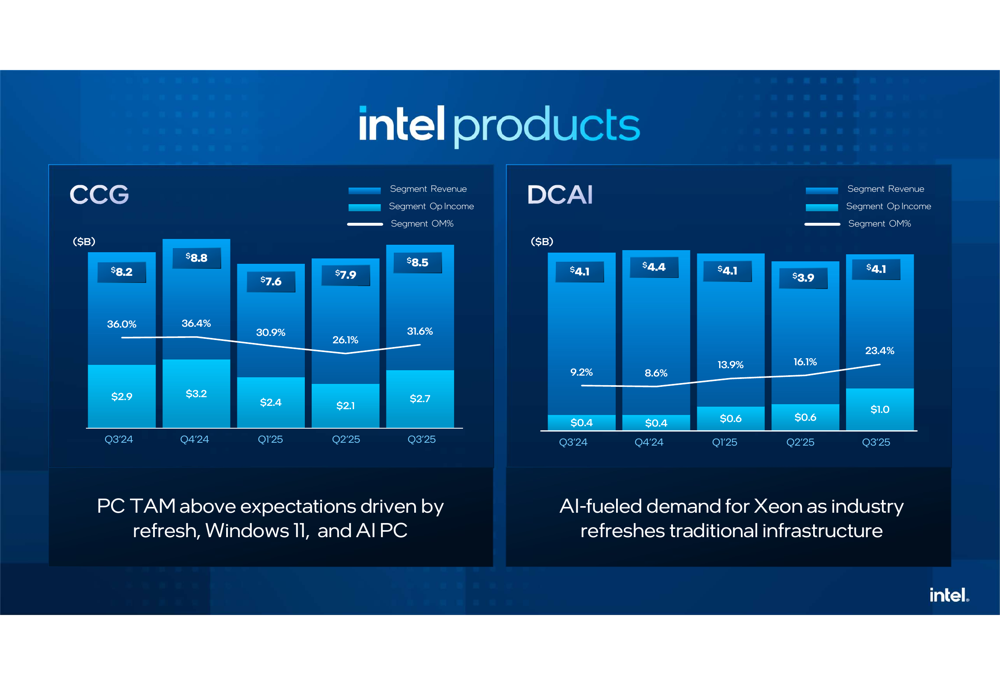

Segment Analysis

Intel's Client Computing Group (CCG) delivered Q3 revenue of $8.5 billion, with segment operating income of $2.7 billion, representing a 31.6% operating margin. The company noted that PC total addressable market (TAM) exceeded expectations, driven by refresh cycles, Windows 11 adoption, and increasing demand for AI PCs.

The Data Center and AI (DCAI) segment generated $4.1 billion in revenue with a segment operating margin of 23.4%, showing significant improvement from 9.2% in Q3 2024. Management attributed this growth to AI-fueled demand for Xeon processors driving infrastructure refreshes.

The following chart illustrates the performance of these key segments:

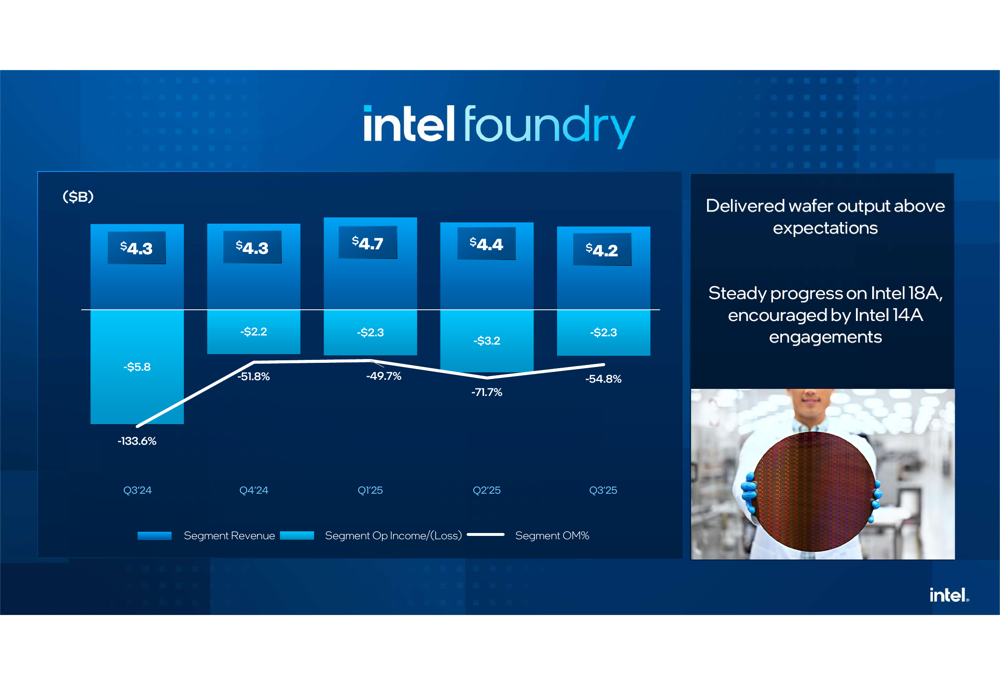

Intel Foundry continues to face challenges, reporting Q3 revenue of $4.2 billion with an operating loss of $2.3 billion, resulting in a -54.8% operating margin. While still operating at a significant loss, this represents an improvement from the -71.7% margin in the previous quarter. The company highlighted that wafer output exceeded expectations and noted steady progress on Intel 18A technology, with encouraging Intel 14A engagements.

The foundry segment's performance is illustrated in the following slide:

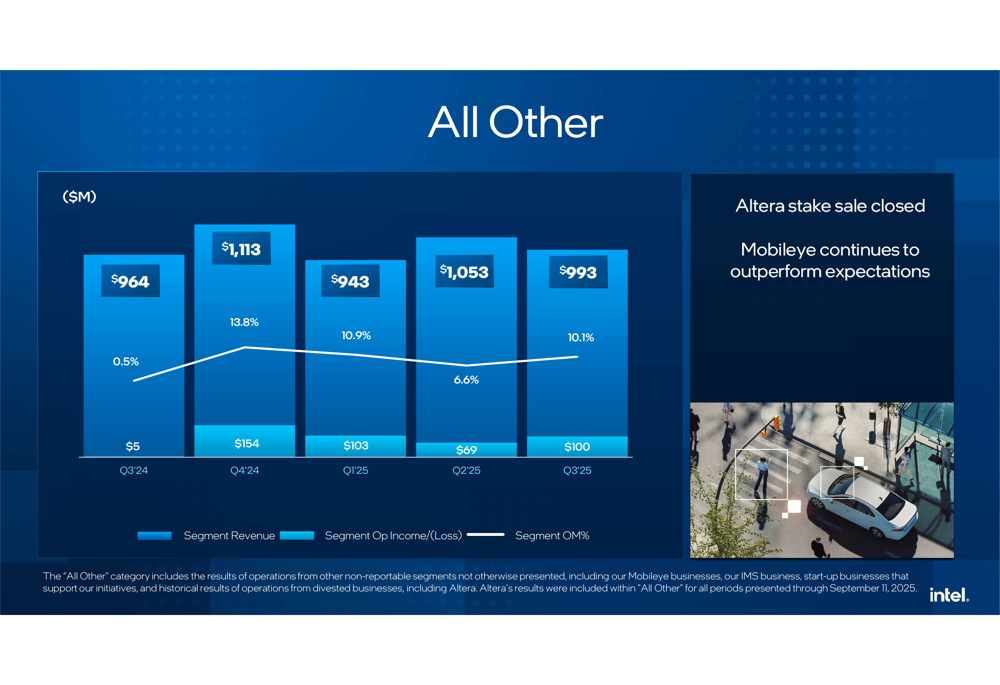

Intel's "All Other" business segments, which include Mobileye and divested businesses such as Altera (through September 11, 2025), generated $993 million in revenue with a 10.1% operating margin. The company noted that the Altera stake sale has closed and that Mobileye continues to outperform expectations.

Strategic Initiatives and Partnerships

The presentation emphasized Intel's strategic focus on AI as a key growth driver. CEO Lip-Bu Tan highlighted that AI is driving demand for compute within core x86 markets and strengthening Intel's U.S.-based Foundry position. The company noted that AI-fueled demand for its products is outpacing supply, with this trend expected to continue into 2026.

Intel's partnerships with NVIDIA and support from the U.S. Government through the CHIPS Act were presented as strategic advantages. The company also highlighted its progress in monetizing assets, including the completed Altera stake sale, to strengthen its balance sheet and focus on core operations.

Forward Guidance

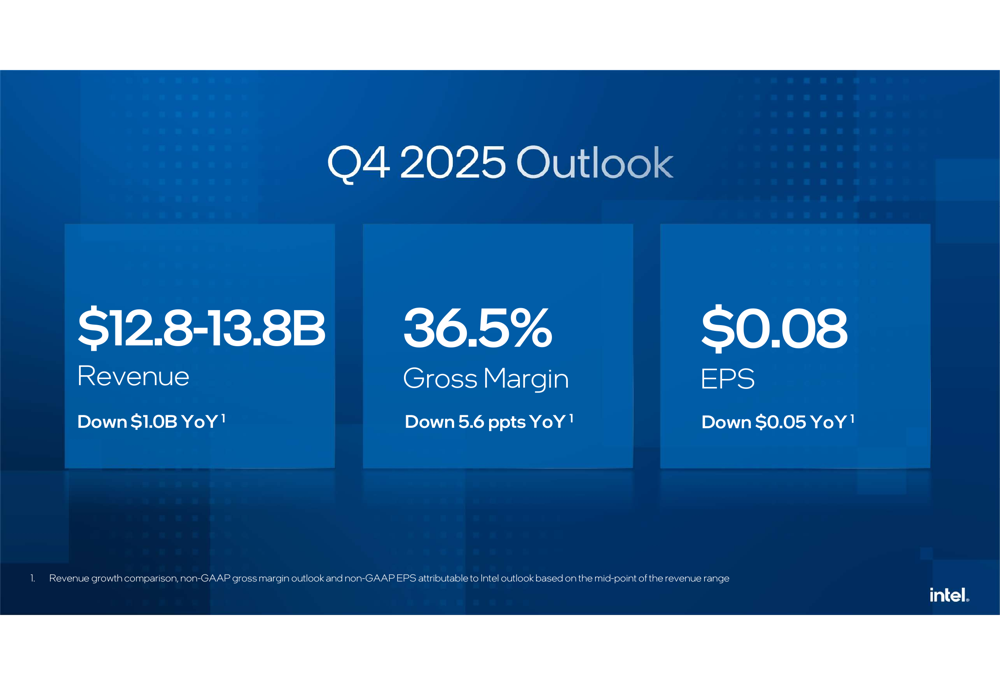

Looking ahead to Q4 2025, Intel provided guidance that suggests some moderation in performance. The company projects revenue between $12.8-13.8 billion, representing a $1.0 billion decrease year-over-year. Gross margin is expected to be 36.5%, down 5.6 percentage points year-over-year, with earnings per share forecast at $0.08, down $0.05 year-over-year.

The following slide details Intel's Q4 2025 outlook:

Conclusion

Intel's Q3 2025 presentation portrays a company making steady progress in its transformation journey, with AI emerging as a significant growth catalyst across business segments. While the core CCG and DCAI segments show improving profitability, the Foundry business continues to operate at a substantial loss despite some sequential improvement.

The company's ability to exceed expectations for the fourth consecutive quarter demonstrates execution improvements, but the more modest Q4 outlook suggests potential challenges ahead. Intel's strategic partnerships, particularly with NVIDIA, and its focus on AI-driven computing position the company to capitalize on industry trends, though competition in the AI space remains intense.

As Intel continues its transformation, investors will be closely monitoring the company's ability to maintain momentum in its core businesses while improving the profitability of its Foundry operations, which remains a significant drag on overall financial performance.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.