Bitcoin set for a rebound that could stretch toward $100000, BTIG says

Introduction & Market Context

MasterBrand Inc (NYSE:MBC), North America's leading residential cabinet manufacturer, released its third quarter 2025 results on November 4, showing declining performance across key metrics amid challenging market conditions. The company's stock fell 1.12% in aftermarket trading to $12.31 following an earnings per share miss, as the cabinet maker continues to navigate a subdued housing and remodeling market.

The quarterly presentation revealed a company in transition, balancing near-term headwinds with strategic initiatives including operational improvements and the pending merger with American Woodmark, expected to close in early 2026.

Quarterly Performance Highlights

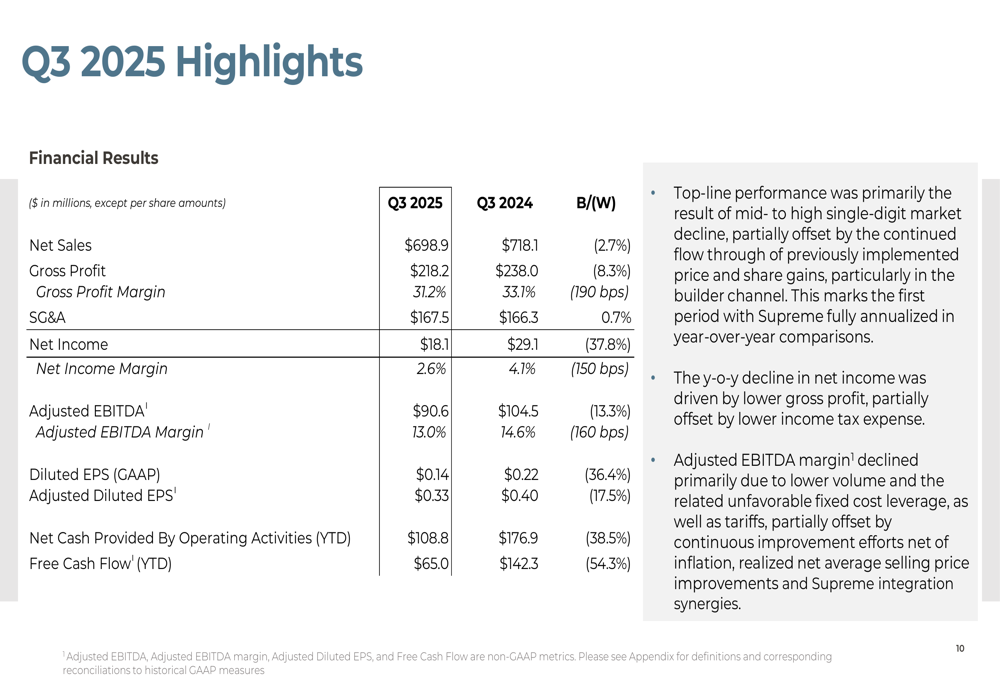

MasterBrand's Q3 2025 financial results showed declines across all key metrics compared to the same period last year. Net sales decreased 2.7% to $698.9 million, while net income fell 37.8% to $18.1 million. The company's adjusted EBITDA declined 13.3% to $90.6 million, with margins contracting 160 basis points to 13.0%.

As shown in the following detailed financial comparison:

The company reported diluted EPS of $0.14, down 36.4% from $0.22 in Q3 2024 and significantly below analyst expectations of $0.52, representing a 36.54% negative surprise. This earnings miss was a key factor in the stock's aftermarket decline.

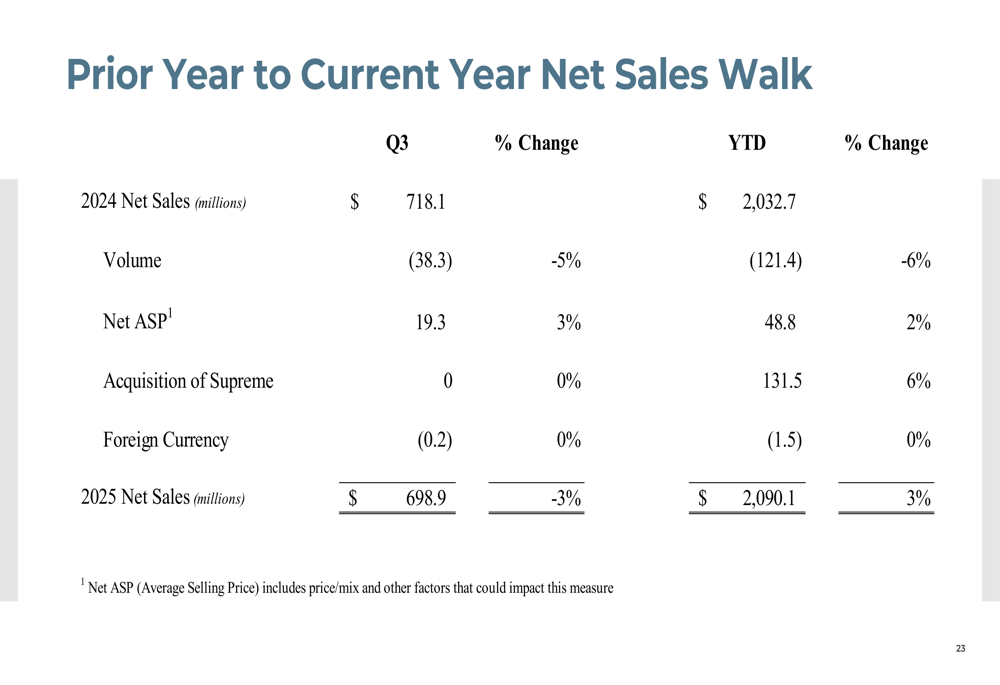

A deeper analysis of the sales performance reveals that while pricing remained positive, volume declines were the primary driver of the revenue decrease:

Strategic Initiatives

Despite current challenges, MasterBrand continues to emphasize its strategic transformation initiatives, which have generated over $180 million in cumulative annual savings since 2019. The company anticipates an additional $50 million in incremental savings for 2025 through its operational excellence program.

A central element of MasterBrand's forward strategy is its pending merger with American Woodmark, which the company expects will create significant value through complementary strengths and cost synergies.

CEO Dave Banyard emphasized the company's long-term strategy during the earnings call, stating, "While near-term challenges persist, our long-term strategy is intact, and our confidence in the business remains strong." CFO Andi Simon added, "We remain very excited about the pending merger between MasterBrand and American Woodmark, which we believe will create a stronger, more resilient company."

Market Positioning

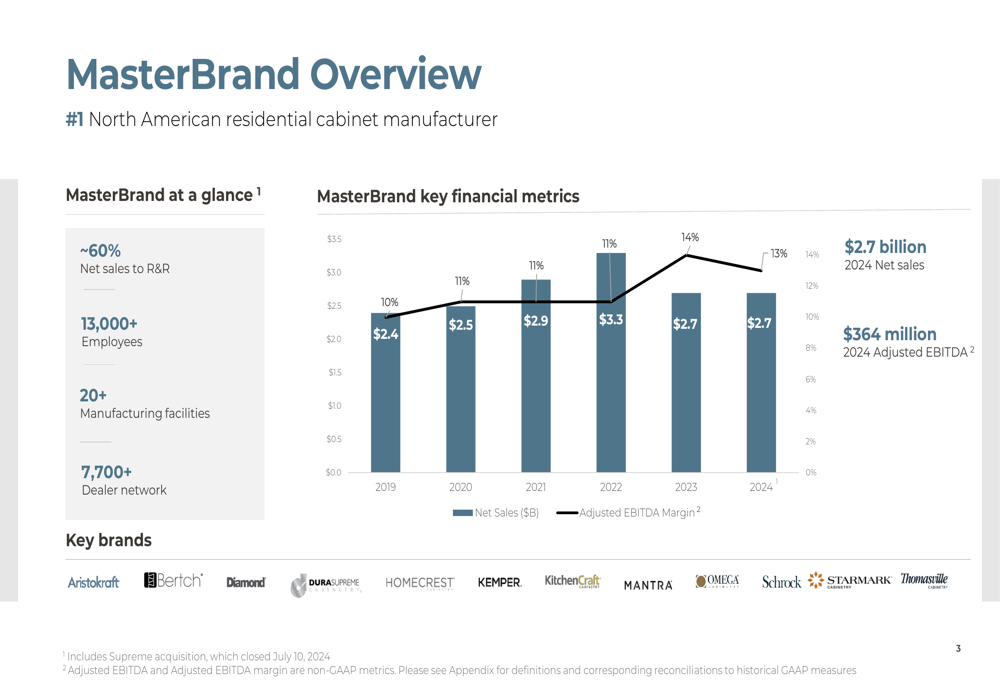

MasterBrand maintains its position as the leading North American cabinet manufacturer with a diversified channel mix and multi-branded strategy across various price points. The company's presentation highlighted its comprehensive market coverage:

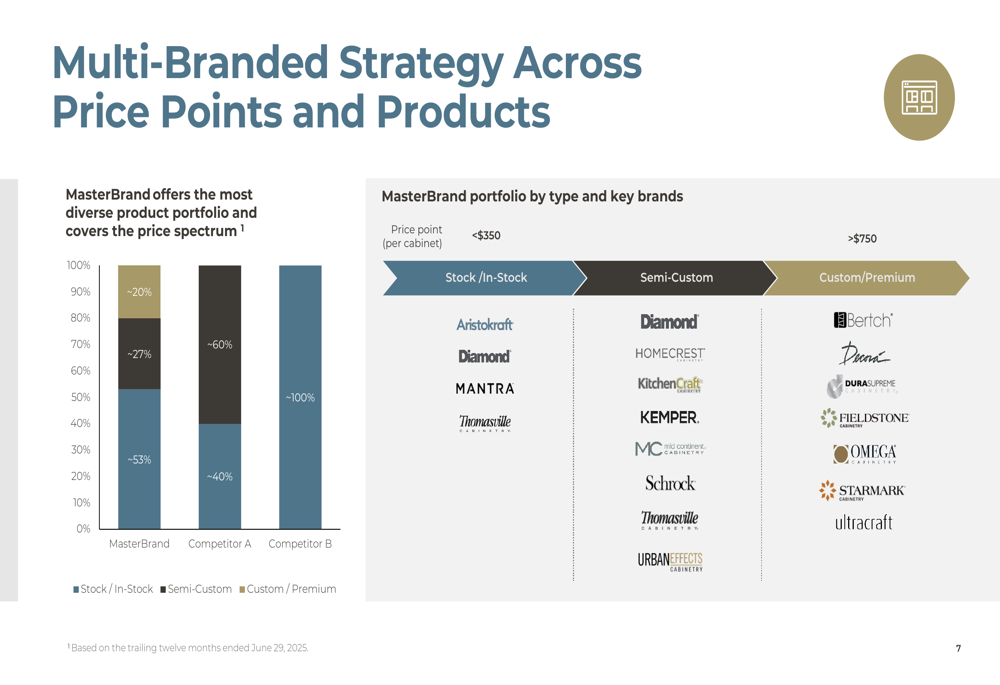

The company's multi-branded approach allows it to serve different market segments with targeted offerings, providing resilience during market fluctuations:

MasterBrand's channel distribution remains diversified with 55% of sales through dealer channels, 32% through retail, and 13% through builder channels. This diversification helps buffer against sector-specific downturns, though the current market challenges are affecting all segments.

Forward-Looking Statements

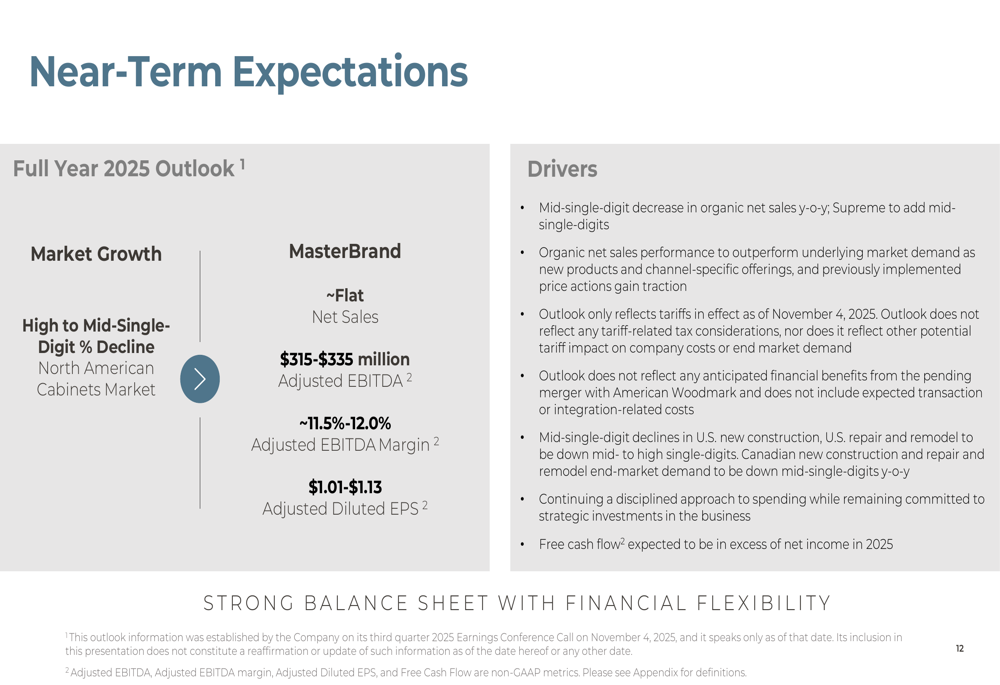

Looking ahead, MasterBrand provided a cautious outlook for the remainder of 2025, projecting approximately flat net sales for the full year despite an expected high to mid-single-digit percentage decline in the North American cabinets market.

The company expects adjusted EBITDA of $315-$335 million with margins of 11.5%-12.0%, and adjusted diluted EPS of $1.01-$1.13. Management anticipates free cash flow will exceed net income in 2025, providing financial flexibility during challenging market conditions.

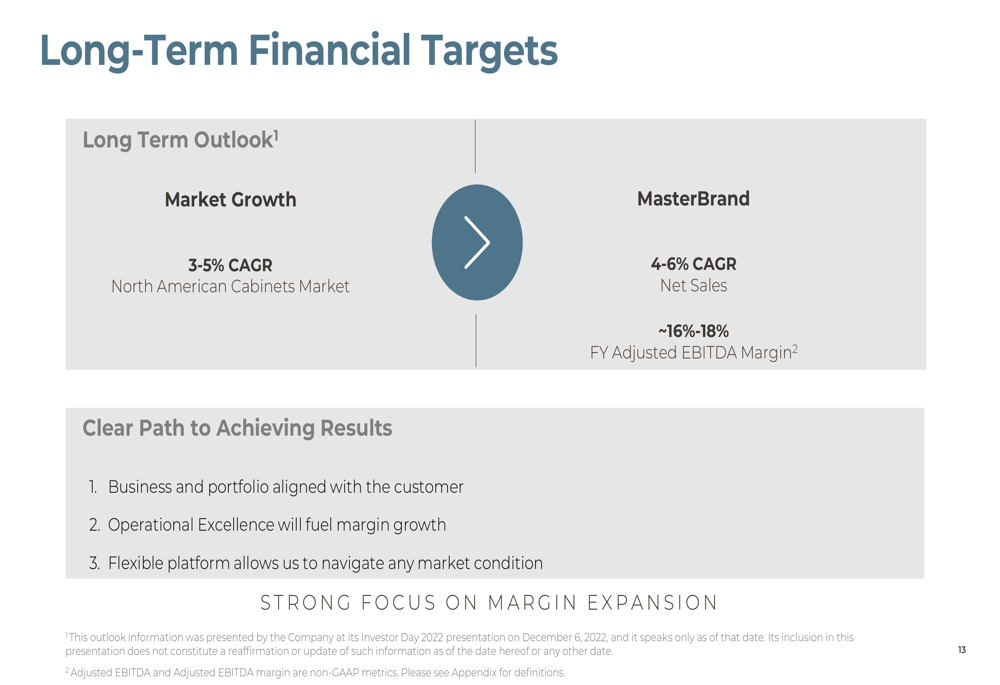

For the longer term, MasterBrand maintains optimistic targets of 4-6% compound annual growth rate in net sales and adjusted EBITDA margins of 16-18%, predicated on a gradual market recovery beginning in late 2026 or early 2027.

Risks and Challenges

Several risks could impact MasterBrand's performance and strategic initiatives. Continued subdued market demand through 2026 poses a significant challenge to revenue growth. New tariffs could affect product pricing and profitability, a concern raised by analysts during the earnings call.

Integration risks associated with both the Supreme acquisition and the pending American Woodmark merger could affect operational efficiency. Additionally, broader economic pressures may continue to impact consumer spending in the housing and remodeling sectors.

Despite these challenges, MasterBrand's diversified product portfolio, operational improvements, and strategic merger plans position the company to weather current market conditions while preparing for an eventual recovery. Investors will be watching closely to see if the company can deliver on its promises of outperforming the market and achieving its long-term financial targets.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.