Janux stock plunges after hours following mCRPC trial data

Introduction & Market Context

Middleby Corp (NASDAQ:MIDD) released its third-quarter 2025 earnings presentation on November 6, revealing mixed financial results with revenue growth offset by margin pressures. The company's shares jumped 6.9% in premarket trading following the earnings release, which exceeded analyst expectations with EPS of $2.37 compared to forecasts of $2.11.

The commercial foodservice equipment manufacturer reported quarterly revenue of $982.1 million, up 4.2% year-over-year, while navigating significant tariff headwinds and implementing strategic restructuring initiatives including the planned separation of its Food Processing business.

Quarterly Performance Highlights

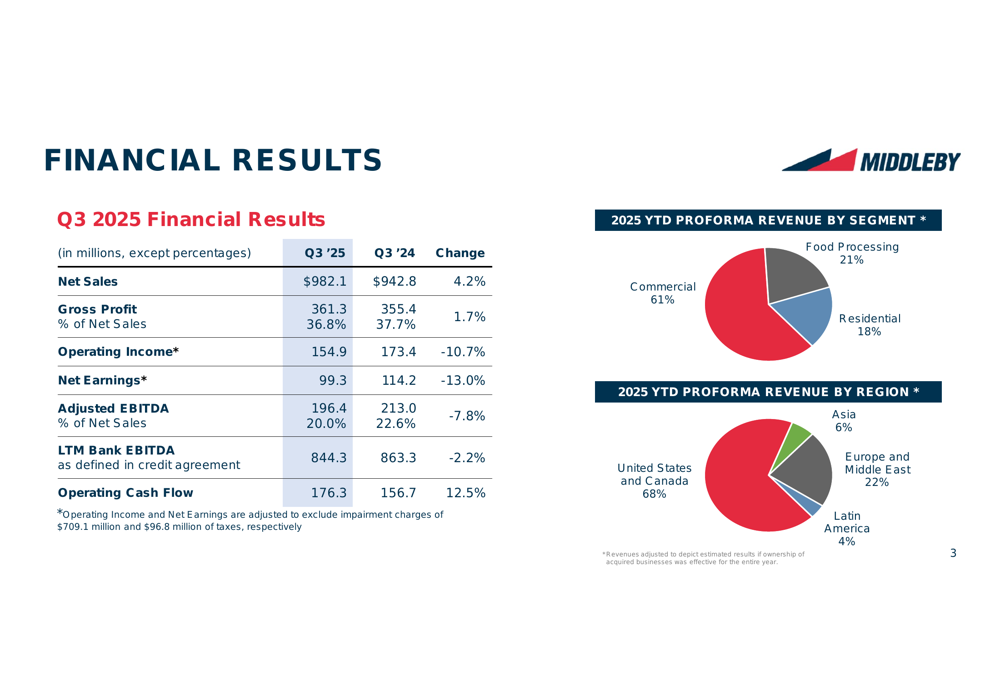

Middleby's Q3 2025 results showed modest top-line growth but declining profitability metrics. The company reported net sales of $982.1 million, a 4.2% increase from $942.8 million in Q3 2024. Gross profit rose 1.7% to $361.3 million, representing 36.8% of net sales.

However, adjusted EBITDA declined 7.8% to $196.4 million, with EBITDA margin contracting to 20.0% of net sales. Adjusted operating income fell 10.7% to $154.9 million, while adjusted net earnings dropped 13.0% to $99.3 million.

As shown in the following revenue breakdown by segment and region:

Operating cash flow was a bright spot, increasing 12.5% to $176.3 million compared to the prior year period. The company's revenue mix remains heavily weighted toward the Commercial Foodservice segment (61%) and the North American market (68%).

Segment Performance Analysis

The Commercial Foodservice segment, Middleby's largest business unit, posted net sales of $606.0 million, up 2.4% year-over-year with organic growth of 1.6%. Segment adjusted EBITDA decreased slightly by 1.0% to $161.6 million. Management noted that growth was driven by general market, institutional and emerging chain business, partially offset by weakness in large quick-service restaurant customers facing lower traffic and cost pressures.

The Residential Kitchen segment reported modest sales growth of 0.9% to $174.8 million, but experienced a significant 17.4% decline in adjusted EBITDA to $17.1 million. The company recorded a substantial $709.1 million non-cash impairment charge related to this segment, reflecting ongoing challenges.

The Food Processing segment delivered the strongest revenue growth at 13.2%, reaching $201.3 million, though organic sales declined 5.5%. Adjusted EBITDA for this segment fell 12.4% to $37.6 million, with margin pressure attributed to volume declines, tariff impacts, and unfavorable geographic mix.

Strategic Initiatives

Middleby highlighted several strategic initiatives aimed at enhancing shareholder value, with the most significant being the planned separation of its Food Processing business. The company confirmed this spin-off remains on track for completion in the first half of 2026, following a comprehensive assessment announced in February 2025.

The company is also conducting a strategic review of its Residential Kitchen business, considering various options including potential separation. These strategic moves are designed to allow greater focus on core strategies and potentially unlock value for shareholders.

As illustrated in the company's strategic initiatives slide:

Additionally, Middleby has invested in operational improvements, including a new state-of-the-art facility in Greenville, Michigan, serving as a "Center of Excellence" for refrigeration products, and a 65,000 square foot innovation center in Venice, Italy, focused on food processing technologies.

Tariff Impact & Outlook

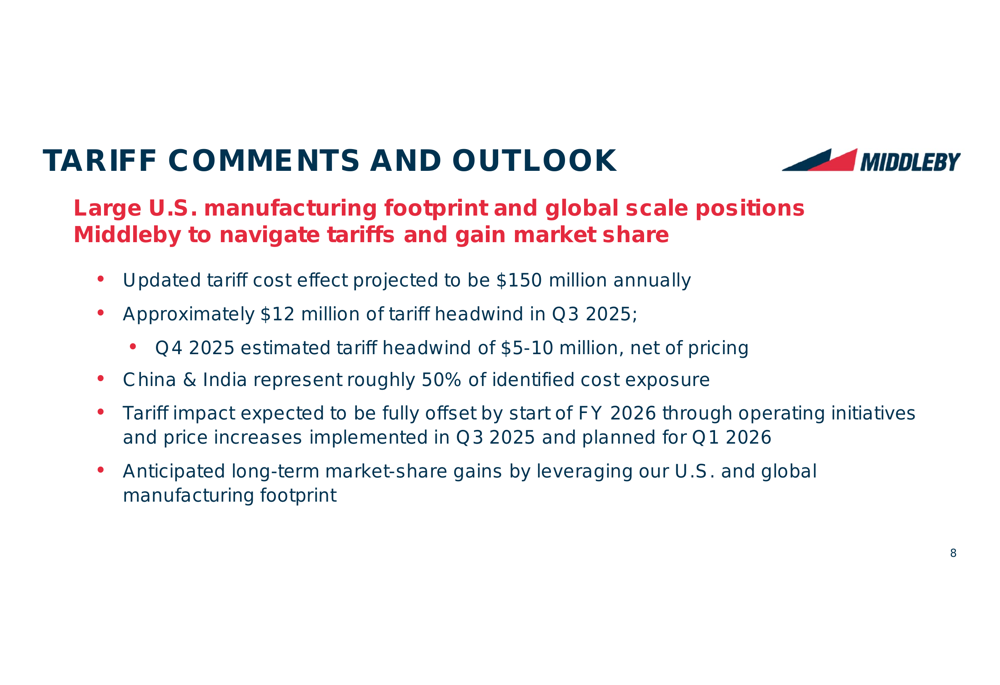

A significant challenge highlighted in the presentation is the impact of tariffs on Middleby's operations. The company projects annual tariff costs of approximately $150 million, with $12 million affecting Q3 2025 results and an estimated $5-10 million impact expected in Q4 2025 (net of pricing actions).

Management emphasized that Middleby's large U.S. manufacturing footprint and global scale position the company to navigate tariff challenges better than competitors. The company expects to fully offset tariff impacts by the start of FY 2026 through a combination of operating initiatives and price increases implemented in Q3 2025 and planned for Q1 2026.

The tariff mitigation strategy is outlined in the following slide:

Capital Allocation & Share Repurchases

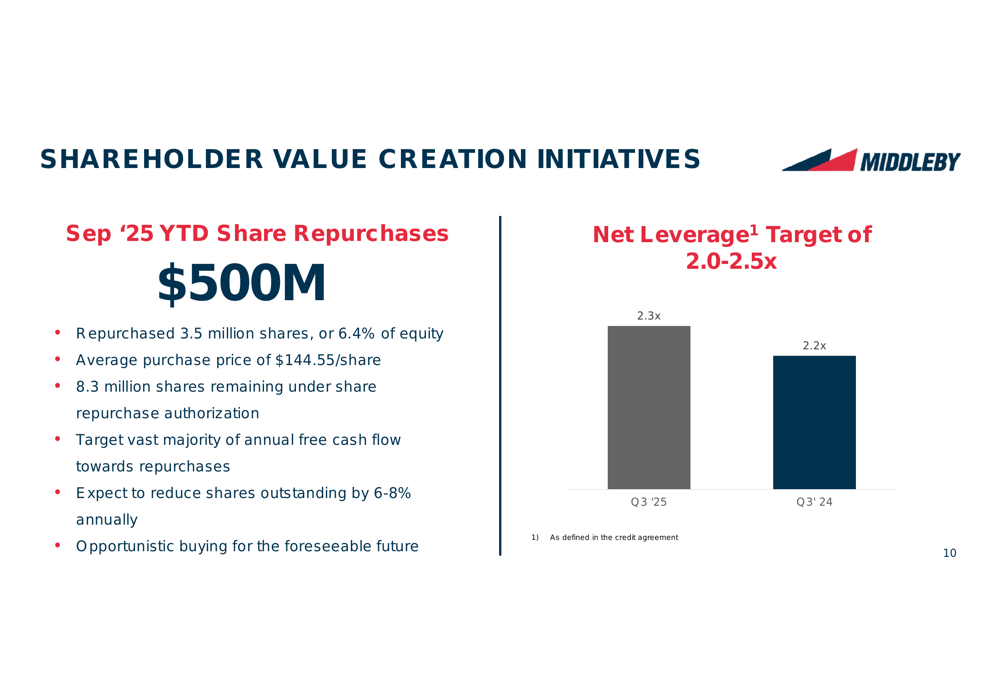

Middleby has been actively returning capital to shareholders through an aggressive share repurchase program. Year-to-date through September 2025, the company has repurchased $500 million worth of shares, representing approximately 3.5 million shares or 6.4% of outstanding equity at an average price of $144.55 per share.

Management indicated plans to target the "vast majority" of annual free cash flow toward repurchases, with an expectation to reduce shares outstanding by 6-8% annually for the foreseeable future. The company is maintaining its net leverage target of 2.0-2.5x, with current leverage at 2.3x as of Q3 2025.

The share repurchase strategy and leverage targets are shown in the following slide:

Forward-Looking Statements

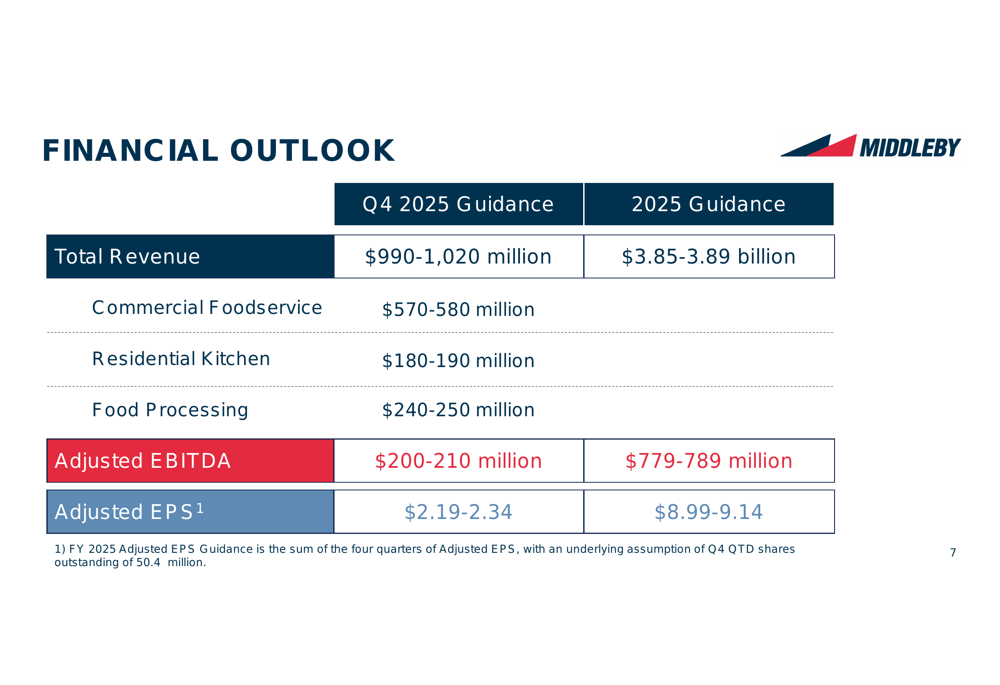

Middleby provided guidance for both Q4 2025 and the full year. For the fourth quarter, the company expects revenue between $990-1,020 million, with adjusted EBITDA of $200-210 million and adjusted EPS of $2.19-2.34.

Full-year 2025 guidance projects revenue of $3.85-3.89 billion, adjusted EBITDA of $779-789 million, and adjusted EPS of $8.99-9.14. The guidance reflects management's expectation of continued revenue growth despite ongoing tariff pressures.

The detailed financial outlook is presented in the following guidance table:

CEO Tim Fitzgerald expressed confidence in the company's strategic direction despite market challenges, stating in the earnings call, "While we are navigating some market volatility, Middleby is stronger today than any point in our history." The company continues to focus on next-generation automation and IoT capabilities to maintain its competitive edge in the foodservice equipment industry.

With the planned separation of its Food Processing business progressing and strategic review of the Residential Kitchen segment underway, Middleby appears positioned for potential structural changes in 2026 that could reshape the company's focus and market positioning.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.