U.S. stock futures slip lower on waning rate cut bets; Applied Materials falls

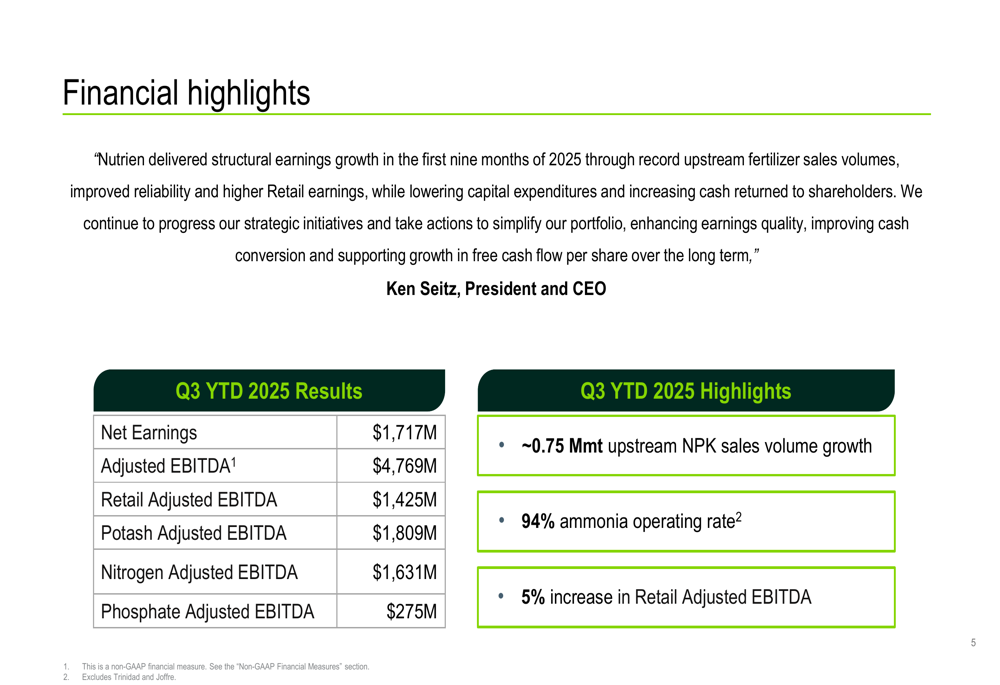

Nutrien Ltd (NYSE:NTR) shares rose 3.87% following the release of its Q3 2025 results presentation, which highlighted strong performance across all business segments and strategic portfolio optimization initiatives. The company reported net earnings of $1,717 million and adjusted EBITDA of $4,769 million for the first nine months of 2025, driven by higher fertilizer sales volumes and improved pricing.

Quarterly Performance Highlights

Nutrien delivered solid Q3 2025 results, with adjusted EBITDA reaching $1.4 billion, representing a 42% year-over-year increase. The company’s performance was supported by higher fertilizer sales volumes, which grew by 4% from 20.73 million metric tonnes in Q3 YTD 2024 to 21.47 million metric tonnes in Q3 YTD 2025.

As shown in the following financial highlights chart, the company achieved significant adjusted EBITDA contributions across all segments, with Potash leading at $1,809 million, followed by Nitrogen at $1,631 million, Retail at $1,425 million, and Phosphate at $275 million for Q3 YTD 2025:

The Retail segment demonstrated impressive growth, with Q3 adjusted EBITDA increasing 52% year-over-year from $151 million to $230 million. This growth was primarily driven by a 35% increase in proprietary products gross margin, which rose from $198 million to $268 million, and a 7% improvement in crop nutrients gross margin per tonne.

The Potash segment also showed strong performance, with Q3 adjusted EBITDA increasing from $555 million in Q3 2024 to $733 million in Q3 2025. This growth was largely attributable to a 30% increase in average net selling price, which rose from $213/mt to $277/mt, offsetting a slight 2% decrease in sales volumes.

Similarly, the Nitrogen segment reported significant growth, with Q3 adjusted EBITDA increasing from $355 million to $556 million year-over-year. This improvement was driven by a 20% increase in average net selling price and a 15% increase in sales volumes, reflecting strong demand and increased production of ammonia and upgraded nitrogen products.

Strategic Initiatives

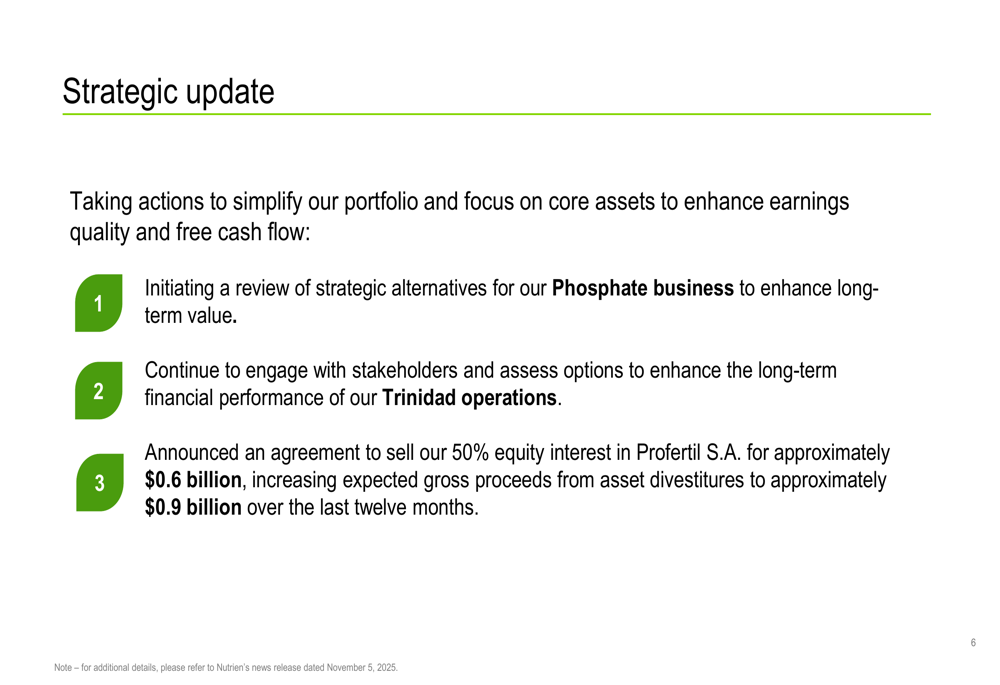

Nutrien outlined several strategic initiatives aimed at simplifying its portfolio and focusing on core assets. The company is initiating a review of strategic alternatives for its Phosphate business, which contributes approximately 6% of total EBITDA, according to the earnings call.

As illustrated in the following strategic update slide, Nutrien is also continuing to engage with stakeholders and assess options for its Trinidad operations, which contribute less than 1% of free cash flow:

Notably, Nutrien announced an agreement to sell its 50% equity interest in Profertil S.A. for approximately $0.6 billion, increasing expected gross proceeds from asset divestitures to approximately $0.9 billion over the last twelve months. These strategic moves are expected to enhance earnings quality and free cash flow.

The company has also maintained a disciplined approach to capital expenditures, with forecasted 2025 capital expenditure in the range of $2.0-$2.1 billion, down from $2.2 billion in 2024 and $2.6 billion in 2023. This reflects Nutrien’s focus on high-value investments in retail proprietary products, mine automation, and projects that improve reliability and energy efficiency.

Forward-Looking Statements

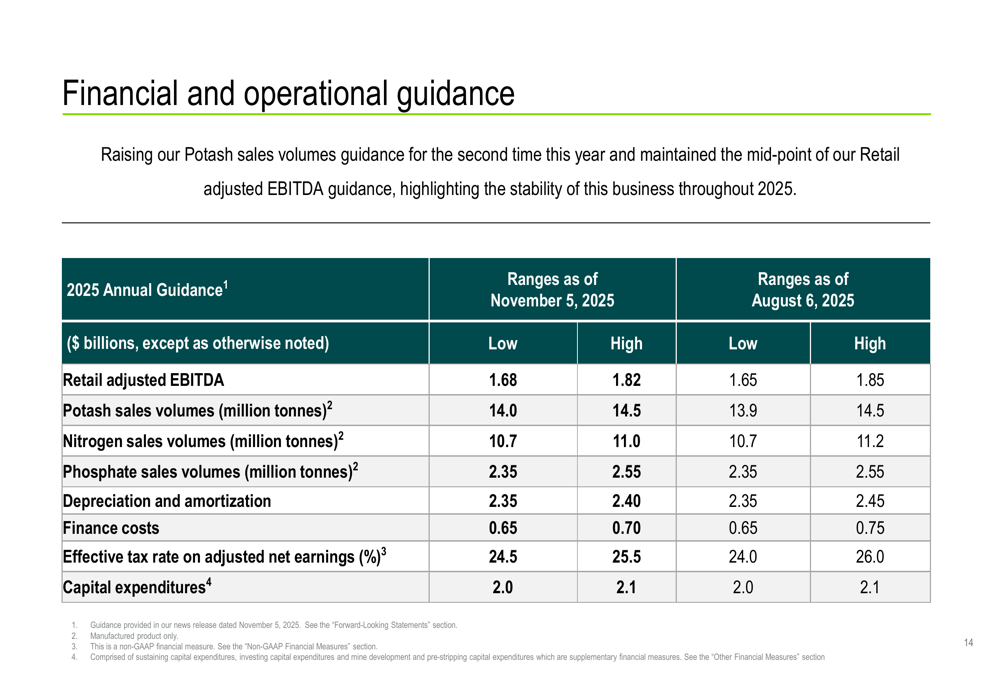

Nutrien’s 2025 financial and operational guidance remained largely stable compared to previous forecasts, reflecting confidence in the company’s business outlook despite agricultural market challenges. The company slightly narrowed its guidance ranges for several metrics, as shown in the following guidance comparison:

The company maintained its Retail adjusted EBITDA guidance at $1.68-1.82 billion, slightly adjusting the lower end upward from the previous $1.65-1.85 billion range. Potash sales volumes guidance was refined to 14.0-14.5 million tonnes, up from 13.9-14.5 million tonnes, while Nitrogen sales volumes guidance was slightly narrowed to 10.7-11.0 million tonnes.

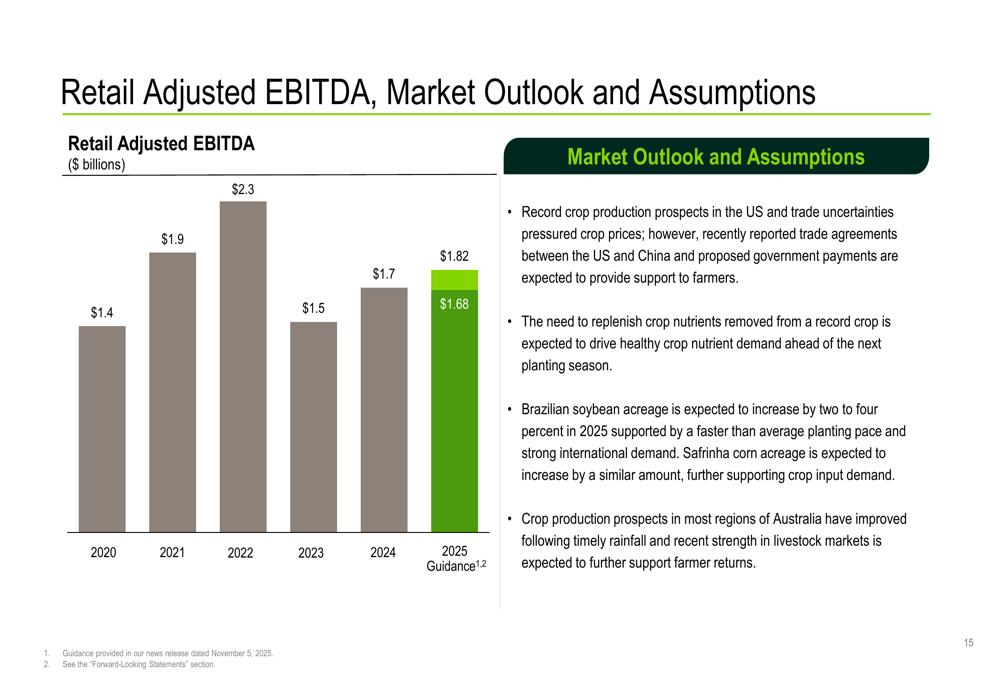

Nutrien’s market outlook for Retail highlights record crop production prospects in the US, alongside trade uncertainties that have pressured crop prices. However, the company expects healthy crop nutrient demand driven by the need to replenish soil nutrients, as illustrated in the following Retail outlook:

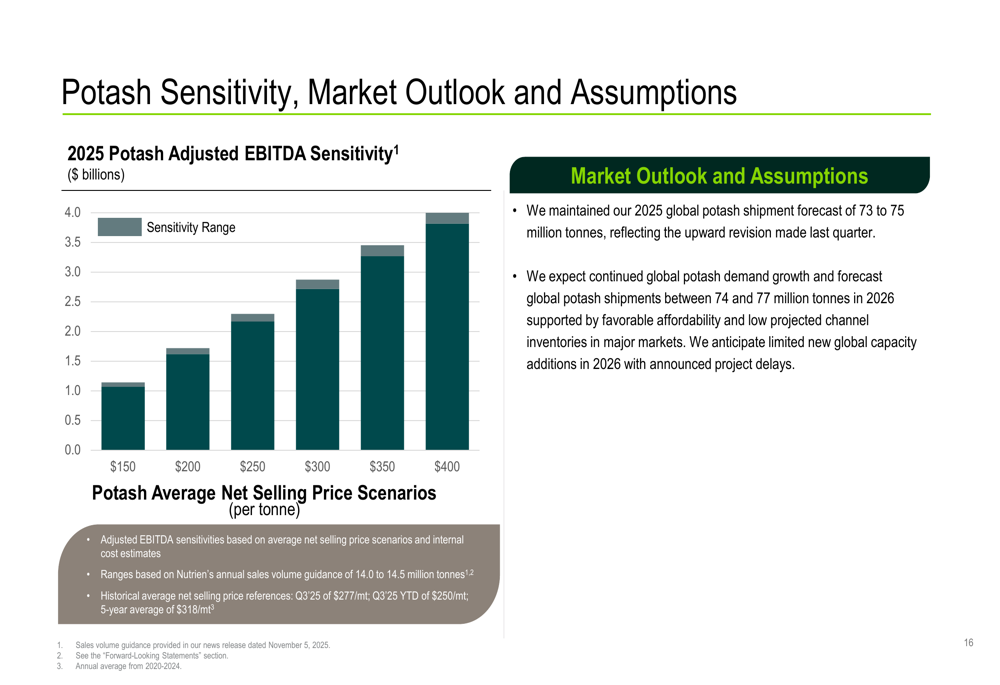

For the Potash segment, Nutrien maintained its 2025 global potash shipment forecast at 73 to 75 million tonnes and expects continued global demand growth with limited new capacity additions in 2026:

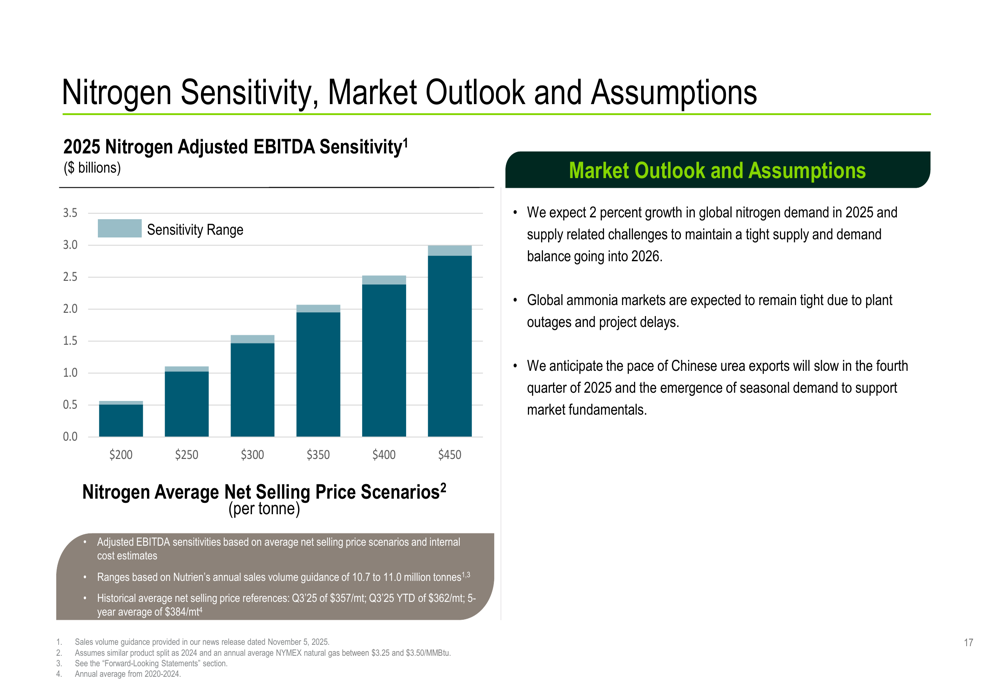

The Nitrogen market outlook anticipates 2% growth in global nitrogen demand in 2025, with global ammonia markets expected to remain tight and a slowing pace of Chinese urea exports:

Competitive Industry Position

Nutrien’s strong performance comes amid challenging global agricultural markets characterized by tight supply chains and fluctuating crop prices. The company’s strategic focus on portfolio optimization and cost reduction has strengthened its competitive position, as evidenced by the 5% reduction in selling and general administrative expenses from $3,090 million to $2,947 million.

CEO Ken Seitz highlighted the company’s progress, stating, "We are demonstrating significant progress across all our strategic priorities," emphasizing "structural earnings growth through record upstream fertilizer sales volumes, improved reliability, higher Retail earnings, lower capital expenditures and increasing cash returned to shareholders."

The market responded positively to Nutrien’s results and strategic direction, with the stock closing at $54.80, up 3.87% following the earnings release. This performance positions the stock well within its 52-week range of $43.70 to $65.08, reflecting investor confidence in the company’s operational efficiency and market strength.

Nutrien’s commitment to shareholder returns was evident in the 42% increase in share repurchases, which rose from $50 million in Q3 YTD 2024 to $401 million in Q3 YTD 2025, while maintaining stable dividend payments at approximately $798 million.

As Nutrien continues to execute its strategic initiatives and capitalize on favorable market conditions in key segments, the company appears well-positioned to deliver sustained value to shareholders while navigating the evolving global agricultural landscape.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.