60%+ returns in 2025: Here’s how AI-powered stock investing has changed the game

Introduction & Market Context

Origin Bancorp, Inc. (NASDAQ:OBK) recently presented its third quarter 2025 results, revealing a significant earnings decline despite improvements in net interest margin and deposit growth. The company's stock reacted negatively to the earnings miss, dropping 9.78% in premarket trading to $31, reflecting investor concerns about the substantial impact of a fraud incident on quarterly performance.

The banking institution, which operates primarily across Texas, Louisiana, and Mississippi, reported earnings per share of $0.27, falling well short of the $0.80 analyst forecast – a 66.25% negative surprise. This disappointing performance occurred despite revenue exceeding expectations at $109.83 million.

Quarterly Performance Highlights

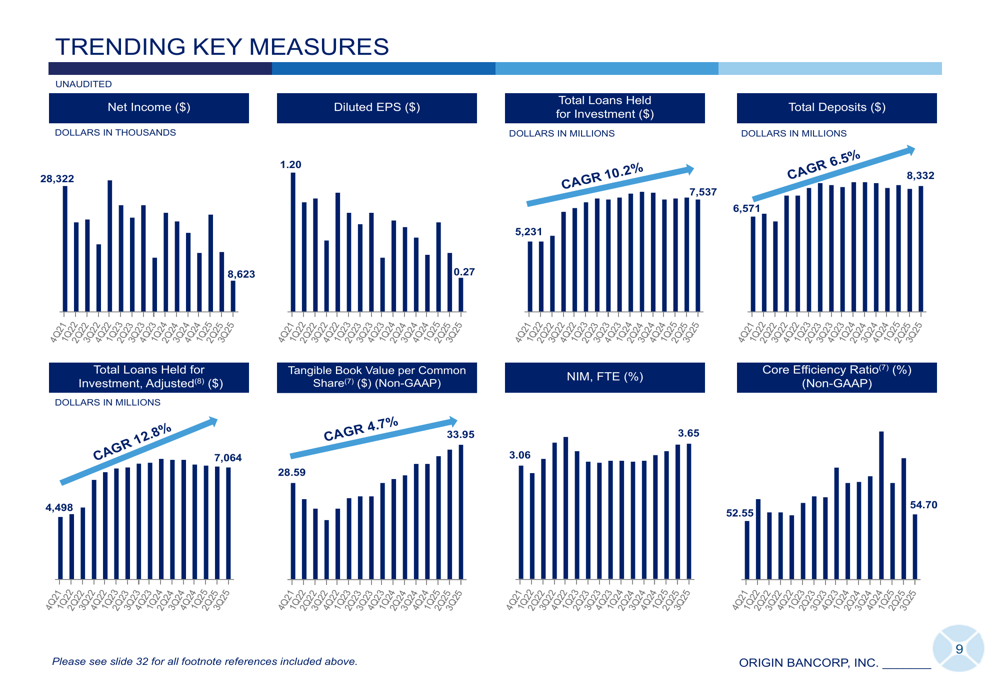

Origin Bancorp's third quarter 2025 results showed mixed performance across key metrics. Net income fell to $8.62 million from $14.65 million in the previous quarter, with diluted EPS declining to $0.27 from $0.47 quarter-over-quarter. Total assets increased to $9.79 billion from $9.68 billion, while deposits grew to $8.33 billion from $8.12 billion in the second quarter.

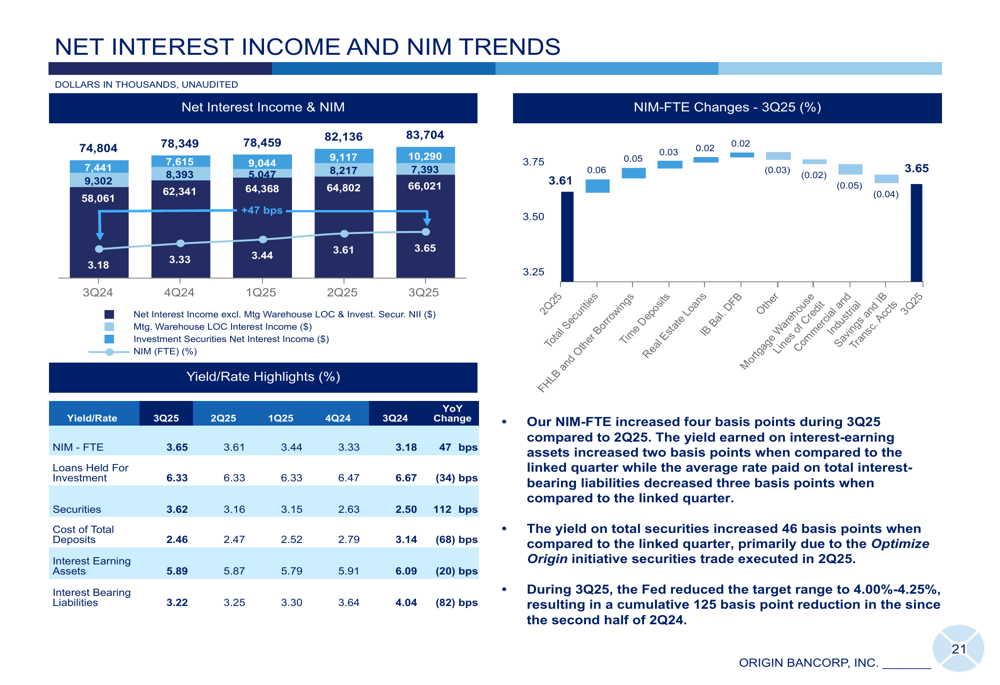

A bright spot in the quarterly performance was the improvement in net interest margin (NIM), which expanded by 4 basis points to 3.65%. This improvement reflects the company's ongoing efforts to optimize its balance sheet and manage funding costs effectively.

The company continues to build tangible book value, which reached $33.95 per share, marking the 12th consecutive quarter of growth in this important metric. This consistent growth demonstrates Origin's ability to generate and retain capital despite quarterly earnings volatility.

Credit Quality and Risk Management

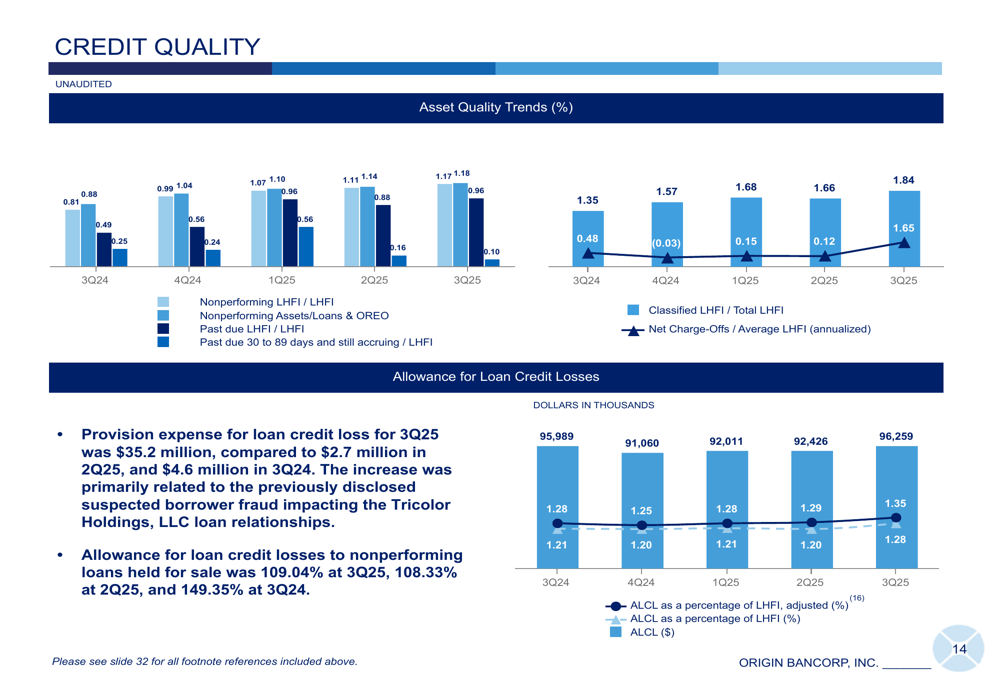

The most significant factor impacting Origin's third quarter results was a substantial increase in loan loss provisions. The company reported provision expense for loan credit losses of $35.2 million in Q3 2025, compared to just $2.7 million in the previous quarter and $4.6 million in the same quarter last year.

This dramatic increase was primarily attributed to a previously disclosed suspected borrower fraud involving Tricolor Holdings, LLC loan relationships. During the earnings call, executives emphasized that this was an isolated incident that has been fully charged off, with no significant broader credit deterioration observed in the portfolio.

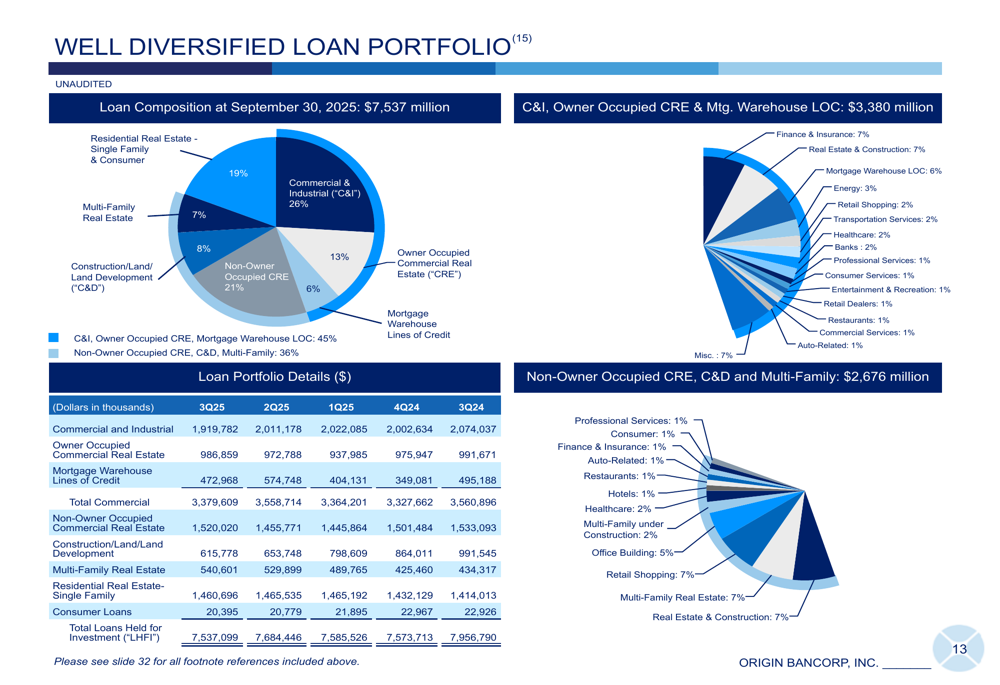

Despite this specific incident, Origin's overall asset quality metrics remain relatively stable. The company maintains a diversified loan portfolio with careful attention to potentially vulnerable sectors such as commercial real estate office space, multi-family real estate, hotels, and retail shopping centers.

Strategic Initiatives

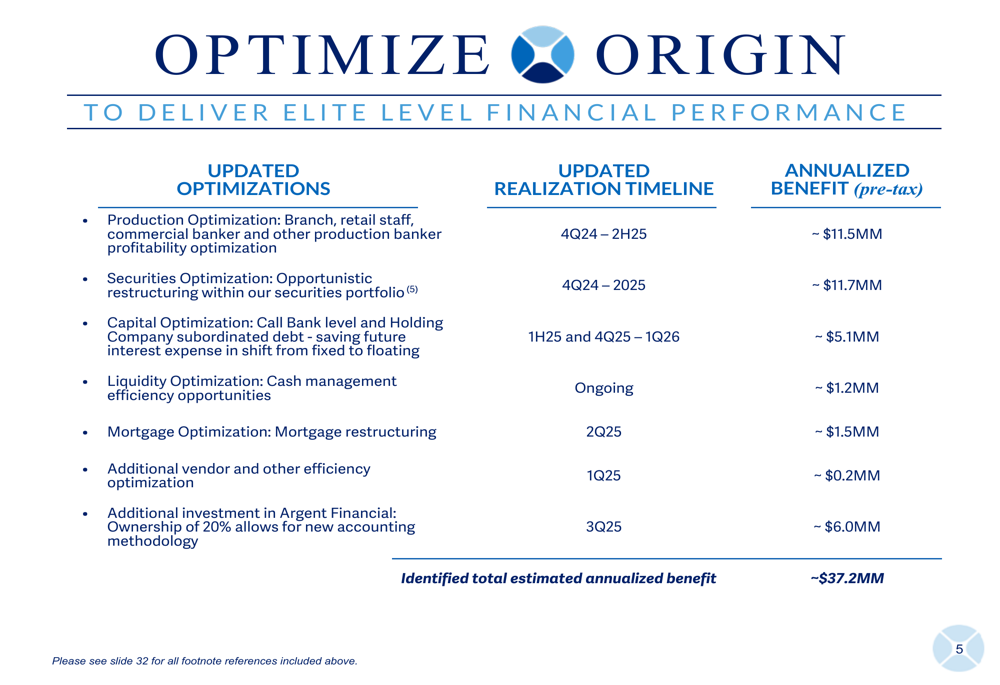

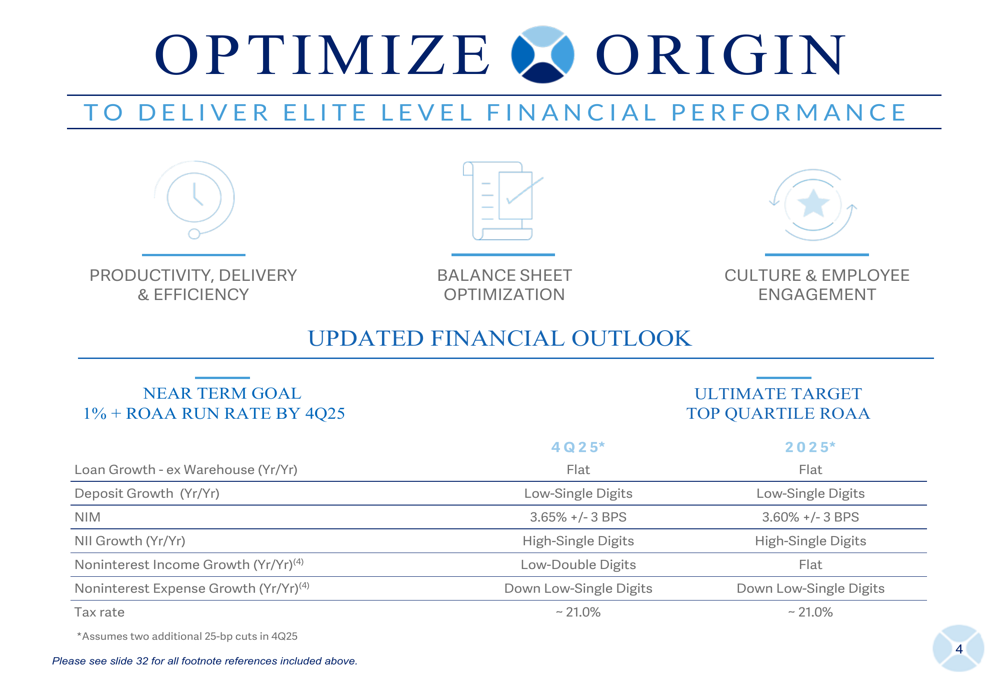

A central focus of Origin's investor presentation was its "Optimize Origin" initiative, which aims to deliver approximately $37.2 million in annualized pre-tax benefits through various optimization strategies. These include production optimization ($11.5 million), securities optimization ($11.7 million), capital optimization ($5.1 million), and additional investment in Argent Financial ($6.0 million).

President Lance Hall emphasized the company's progress on this front during the earnings call, stating, "We are ahead of pace on our stated plan and are creating real traction on our goal of being a top quartile ROA performer." CEO Drake Mills addressed the EPS miss by noting, "This isolated event does not define Origin."

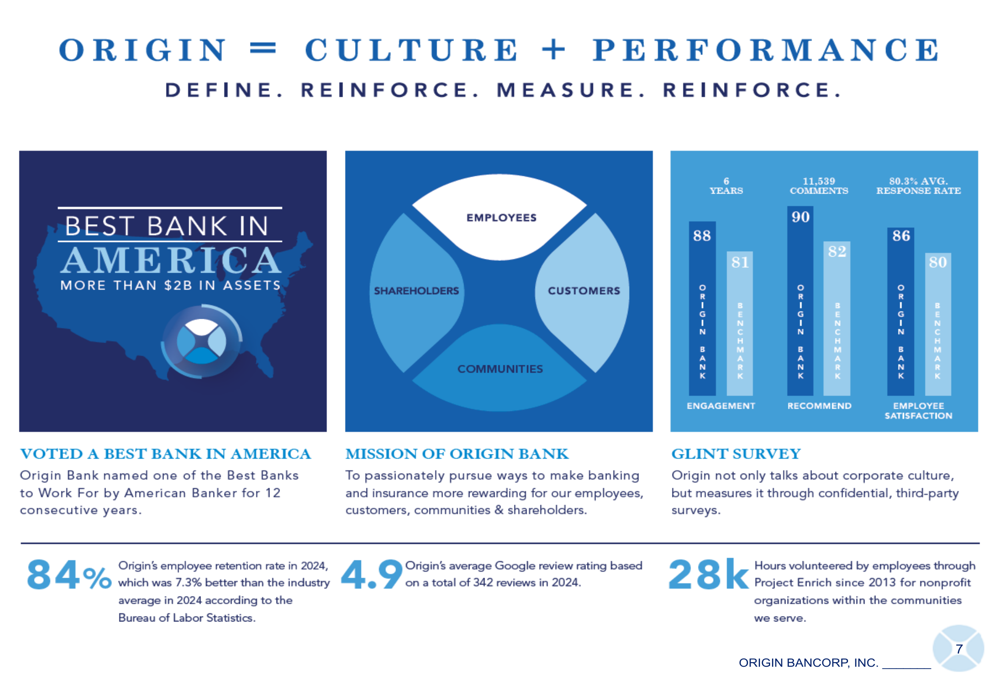

The company highlighted its strong corporate culture as a competitive advantage, with an 84% employee retention rate (7.3% above the industry average), a 4.9 average Google review rating, and recognition as one of the "Best Banks to Work For" by American Banker for 12 consecutive years.

Geographic Footprint and Growth Markets

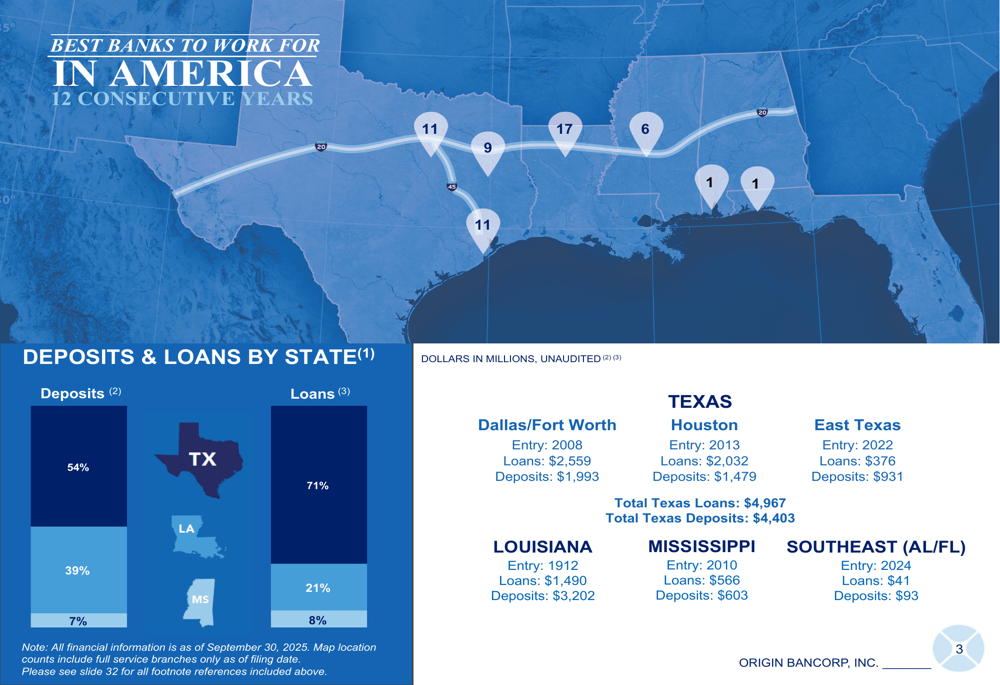

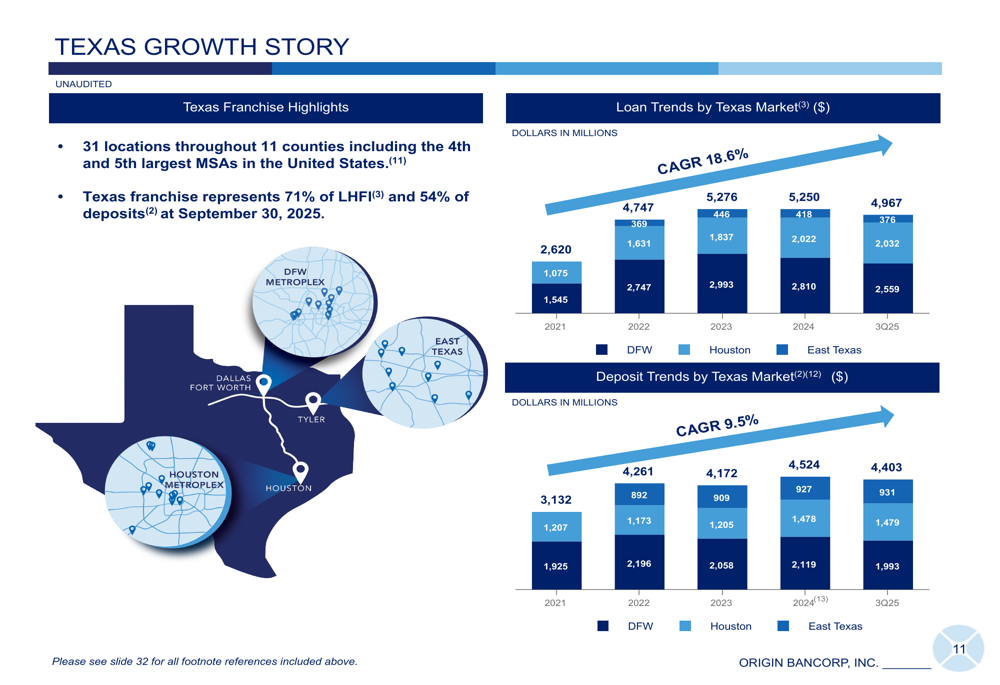

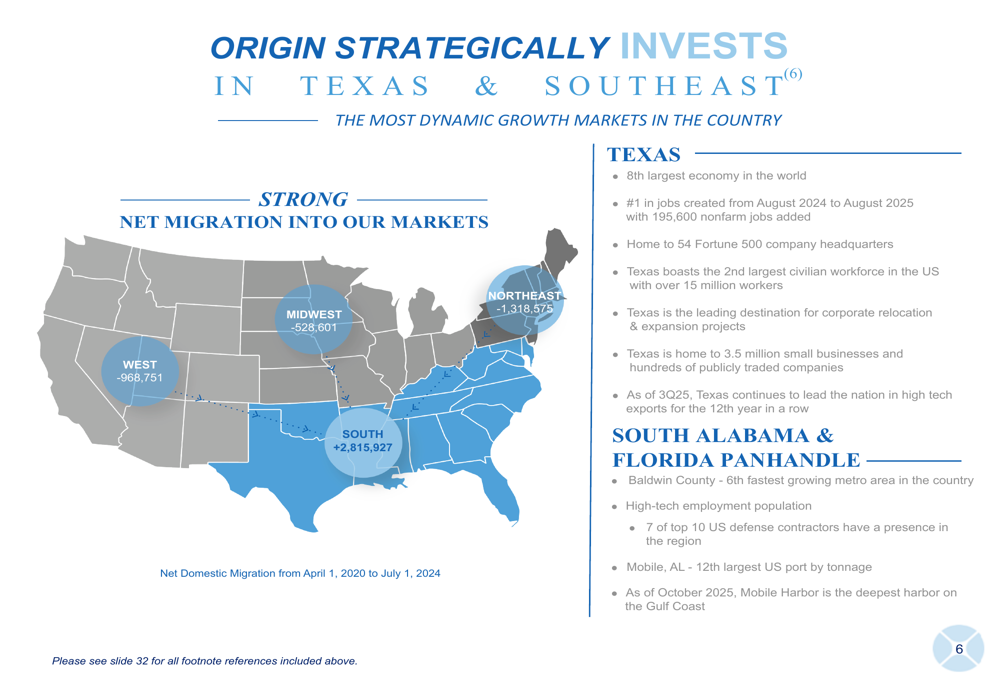

Origin Bancorp maintains a strategic focus on high-growth markets in the Southern United States, with particular emphasis on Texas, which represents 71% of loans and 54% of deposits. The company operates 31 locations across 11 Texas counties, highlighting the state's economic strength as the 8th largest economy globally and #1 in job creation nationally.

The Texas market continues to be central to Origin's growth strategy, with significant presence in Dallas-Fort Worth, Houston, and East Texas. The company views the state's robust economic fundamentals, including its position as home to 54 Fortune 500 headquarters and status as a leading destination for corporate relocation, as key drivers for future growth.

In addition to its Texas operations, Origin is strategically positioned in the Southeast, particularly in South Alabama and the Florida Panhandle. These markets feature high-tech employment populations, presence of top US defense contractors, and include the deepest harbor on the Gulf Coast, offering diversification and growth potential beyond the company's core Texas market.

Forward-Looking Statements

Origin Bancorp has updated its financial outlook, revising loan growth guidance for 2025 to flat, a significant shift from earlier growth expectations. The company anticipates modest 2% loan growth in Q4, with mid to high single-digit growth projected for 2026.

Despite the loan growth revision, Origin maintains its net interest margin guidance between 3.60% and 3.65% for 2025. The company expects low-single-digit deposit growth, high-single-digit net interest income growth, and a reduction in noninterest expenses for the remainder of the year.

The company continues to actively manage capital, having repurchased 265,248 shares in Q3 2025 at an average price of $35.85 per share. Origin has $40.5 million remaining in its authorized share repurchase program, providing flexibility for continued capital management.

Conclusion

Origin Bancorp's third quarter 2025 results present a complex picture of a company navigating significant challenges while implementing strategic optimizations. The substantial EPS miss due to the fraud-related loan loss provision overshadowed improvements in net interest margin and deposit growth.

Looking ahead, investors will likely focus on the company's ability to execute its "Optimize Origin" initiative, manage credit quality effectively, and capitalize on its strong position in growth markets, particularly in Texas. While the isolated fraud incident created a significant short-term earnings impact, the company's underlying fundamentals and strategic direction remain intact, with potential for improved performance as optimization efforts take hold.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.