Eos Energy stock falls after Fuzzy Panda issues short report

Introduction & Market Context

Peoples Bancorp Inc. (NASDAQ:PEBO) presented its third quarter 2025 earnings on October 21, showing resilience in a challenging banking environment. The regional bank reported earnings per share of $0.83, meeting analyst expectations despite a slight revenue miss. The stock responded positively, rising 1.85% to $29.23 in regular trading after gaining 1.11% in pre-market activity.

The bank’s presentation highlighted its strategic focus on organic growth while managing exposure to higher-risk segments. This balanced approach appears to be resonating with investors, as the stock trades well above its 52-week low of $26.21, though still below its high of $37.07.

Quarterly Performance Highlights

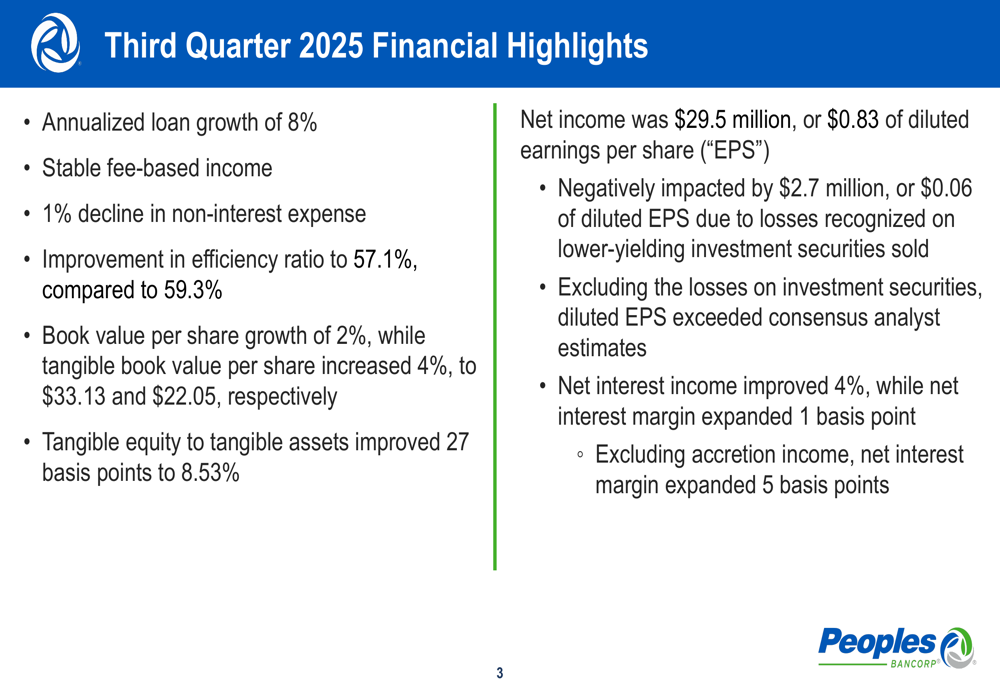

Peoples Bancorp reported net income of $29.5 million, or $0.83 per diluted share for Q3 2025. This performance was achieved despite a $2.7 million ($0.06 per share) negative impact from losses on investment securities sold. Excluding these losses, the bank would have exceeded consensus analyst estimates.

The quarter showed notable improvements in several key metrics, including an 8% annualized loan growth, 4% increase in net interest income, and enhancement in the efficiency ratio to 57.1% from 59.3% in the previous quarter.

As shown in the following summary of financial highlights:

Book value per share grew 2% while tangible book value per share increased 4% to $33.13 and $22.05 respectively. The bank’s tangible equity to tangible assets ratio improved by 27 basis points to 8.53%, demonstrating strengthened capital positioning.

Loan Portfolio Growth and Composition

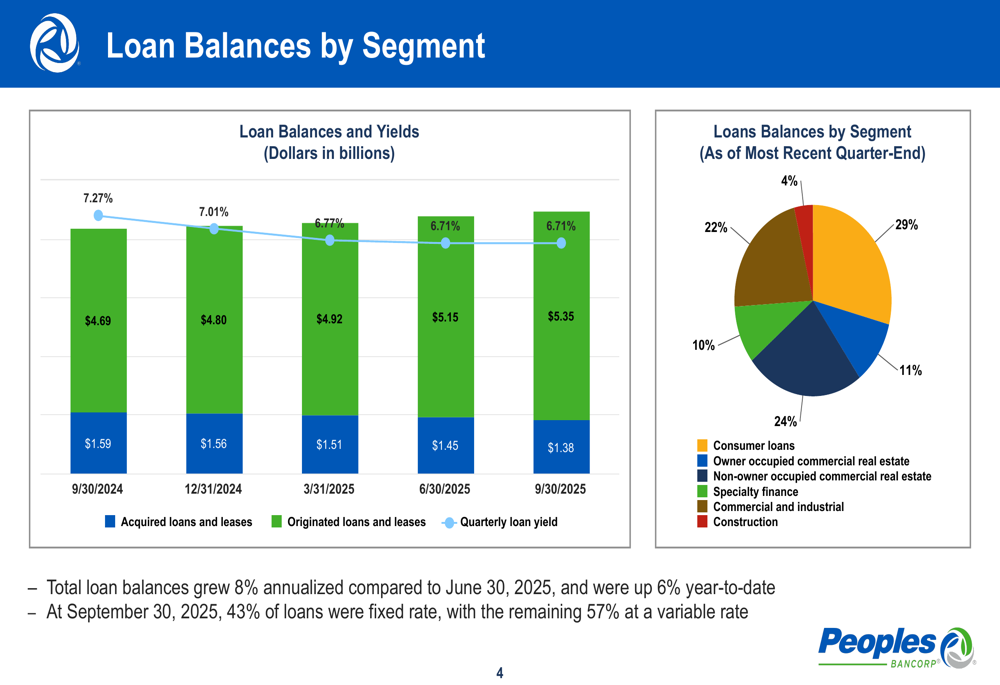

Peoples Bancorp’s loan portfolio showed strong growth momentum, with total balances increasing at an 8% annualized rate compared to June 30, 2025. The composition reflects a well-diversified approach across various sectors, with owner-occupied commercial real estate representing the largest segment at 29%.

The bank continues its transition from acquired to originated loans, with originated loans now comprising the vast majority of the portfolio. The loan mix is balanced between fixed (43%) and variable (57%) rate loans, positioning the bank to manage interest rate fluctuations effectively.

The following chart illustrates the loan growth trajectory and portfolio composition:

Credit Quality and Risk Management

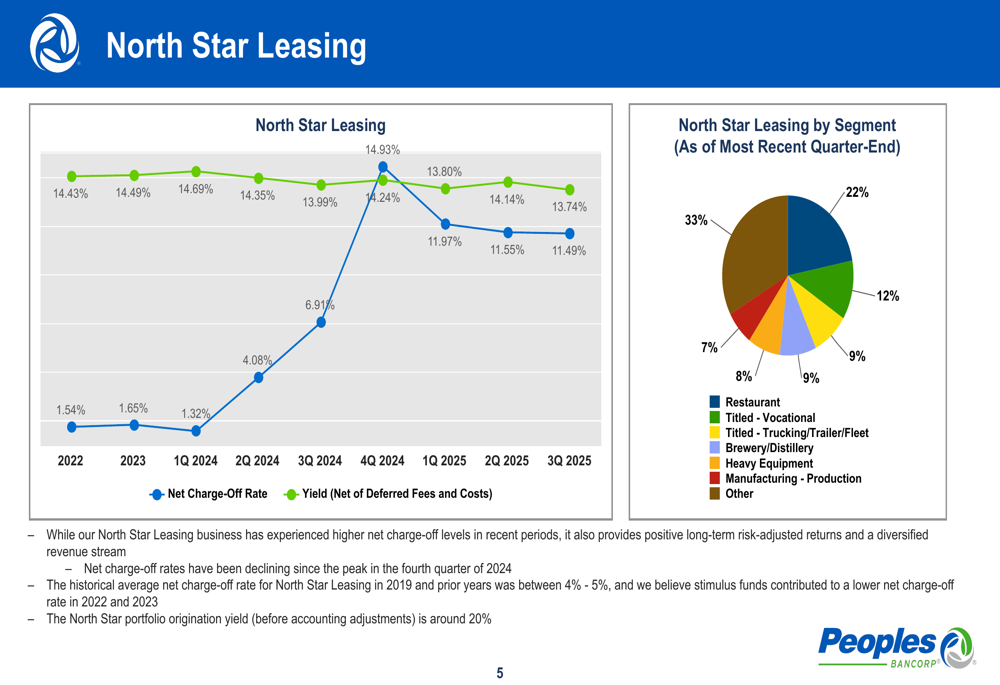

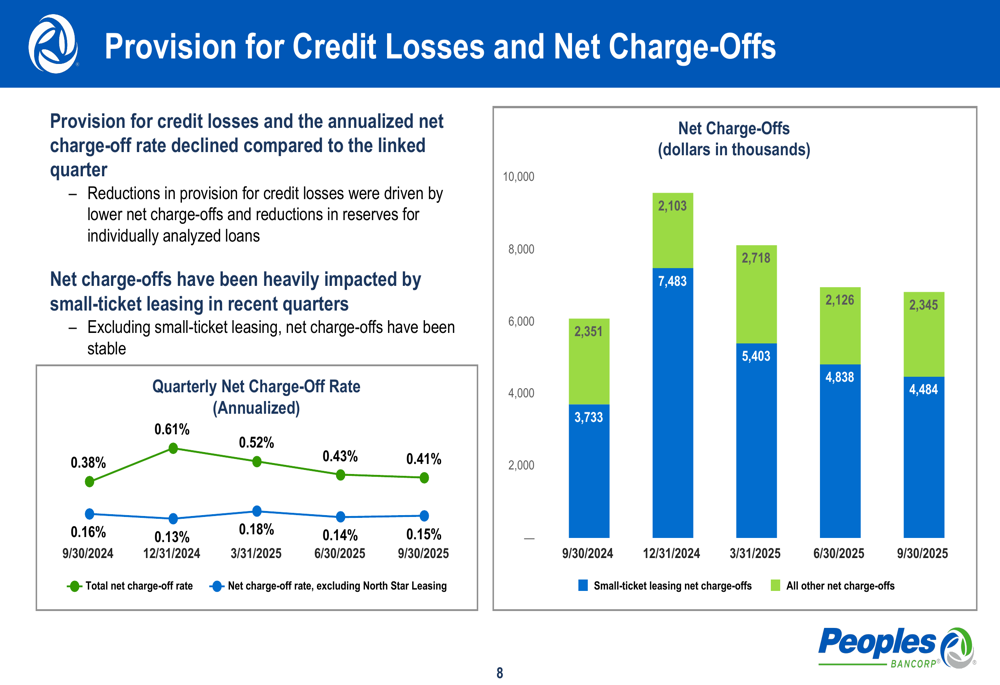

A significant focus of the presentation was the bank’s strategic management of its North Star Leasing (NSL) segment. While providing diversification and higher yields, this segment has experienced elevated charge-off levels in recent periods. The bank has been actively reducing its exposure to high-balance small-ticket leasing accounts, which have been a source of credit challenges.

As shown in the following chart of North Star Leasing performance:

Net charge-off rates have been declining from their peak of 14.56% in Q4 2024 to 11.49% in Q3 2025, suggesting the bank’s risk management strategies are taking effect. The NSL portfolio maintains attractive yields of approximately 13.74%, providing strong risk-adjusted returns despite the higher charge-offs.

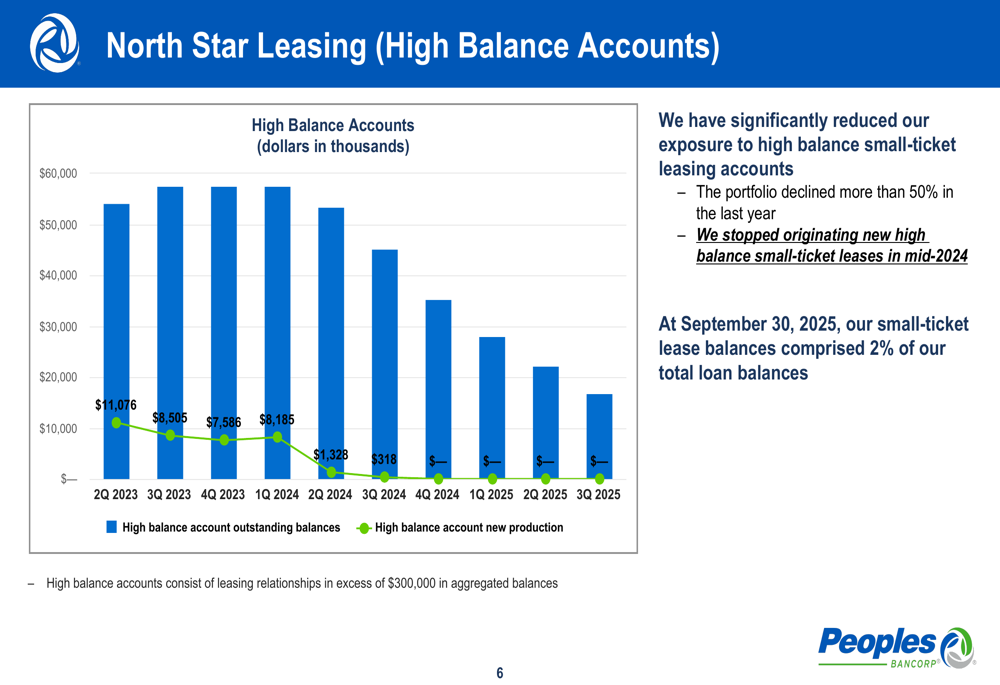

Peoples has significantly reduced its exposure to high-balance small-ticket leasing accounts, as illustrated in this trend chart:

This strategic reduction has decreased the bank’s risk profile, with small-ticket lease balances now comprising only 2% of total loan balances as of September 30, 2025.

Overall asset quality metrics showed mixed trends, with nonperforming loans declining nearly $2 million compared to June 30, while criticized loans increased by $24 million. The bank noted that it expects some of these criticized credits to be paid off in coming quarters.

Net Interest Income and Margin Trends

Net interest income, the bank’s primary revenue driver, grew nearly $4 million compared to the linked quarter, reaching $91.35 million. The net interest margin expanded by one basis point to 4.16%, despite declining accretion income from acquired loans.

Excluding accretion income, which contributed only 8 basis points to the margin (down from 12 basis points in Q2), the core net interest margin expanded by 5 basis points. This suggests underlying strength in the bank’s core lending activities.

The following chart details the net interest income and margin trends:

This performance aligns with the bank’s guidance for full-year net interest margin between 4.00% and 4.20%, positioning it favorably compared to many regional banking peers.

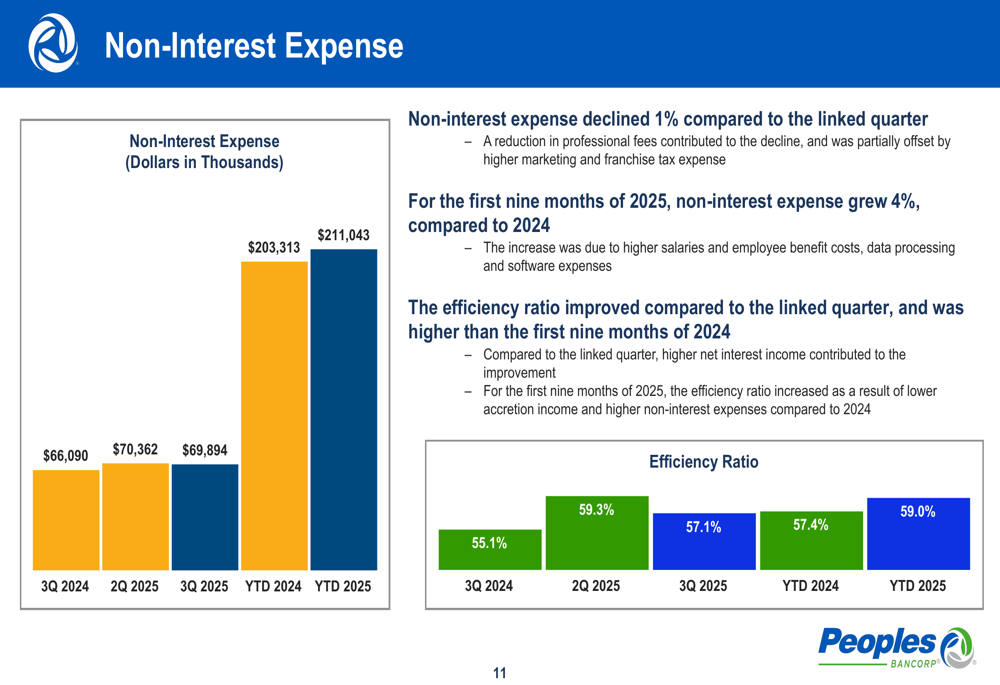

Expense Management and Efficiency

Peoples Bancorp demonstrated effective cost control, with non-interest expense declining 1% compared to the linked quarter to $69.89 million. This decline was primarily driven by lower professional fees. The efficiency ratio improved to 57.1% from 59.3% in the previous quarter, indicating better operating leverage.

The following chart illustrates the expense trends and efficiency ratio:

For the first nine months of 2025, non-interest expense grew 4% year-over-year due to higher salaries, employee benefits, data processing, and software expenses. However, the recent quarterly improvement suggests the bank is focusing on expense discipline while investing in necessary technology and talent.

Deposit Base and Funding

The bank’s deposit base remained relatively stable compared to the previous quarter, excluding brokered certificates of deposit. Increases in money market, interest-bearing demand, and non-interest bearing deposit balances were offset by declines in certificates of deposit.

The cost of deposits held steady at 1.76% for the second consecutive quarter, following several quarters of declining costs. This stabilization in funding costs supports the bank’s net interest margin outlook.

The deposit mix shows a reliance on brokered deposits at 26%, which may present both opportunities and challenges in a shifting rate environment.

Forward-Looking Statements

Looking ahead, Peoples Bancorp provided an optimistic outlook for the remainder of 2025. The bank expects to maintain positive operating leverage, with loan growth between 4% and 6% for the full year. The net interest margin is projected to remain between 4.00% and 4.20%.

CEO Tyler Wilcox emphasized the company’s strategic focus during the earnings call, stating, "We continue to develop our business organically as we await the right opportunity to grow through acquisitions." This suggests a disciplined approach to growth that balances organic expansion with potential M&A activity.

For 2026, management projects loan growth of 3-5%, slightly more conservative than the current year’s pace, and anticipates a net interest margin of 4.2%. The bank expects quarterly fee-based income between $27-29 million and non-interest expenses of $71-73 million.

Potential headwinds identified include Federal Reserve rate cuts that could impact margins, softening consumer markets affecting loan demand, and global economic uncertainties. However, the bank’s diversified business model and improving efficiency position it to navigate these challenges effectively.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.