LATAM Airlines pilots in Chile to begin strike at midnight Wednesday

Introduction & Market Context

Scatec Solar OL (SCATC) presented its third-quarter 2025 results on October 30, showing significant revenue growth despite a challenging environment for renewable energy developers. The company’s stock responded positively, rising 2.52% to close at 107.1 NOK following the presentation.

The Norwegian renewable energy developer highlighted its accelerating growth strategy while maintaining focus on debt reduction, as global demand for solar and battery storage solutions continues to expand in emerging markets where Scatec operates.

Quarterly Performance Highlights

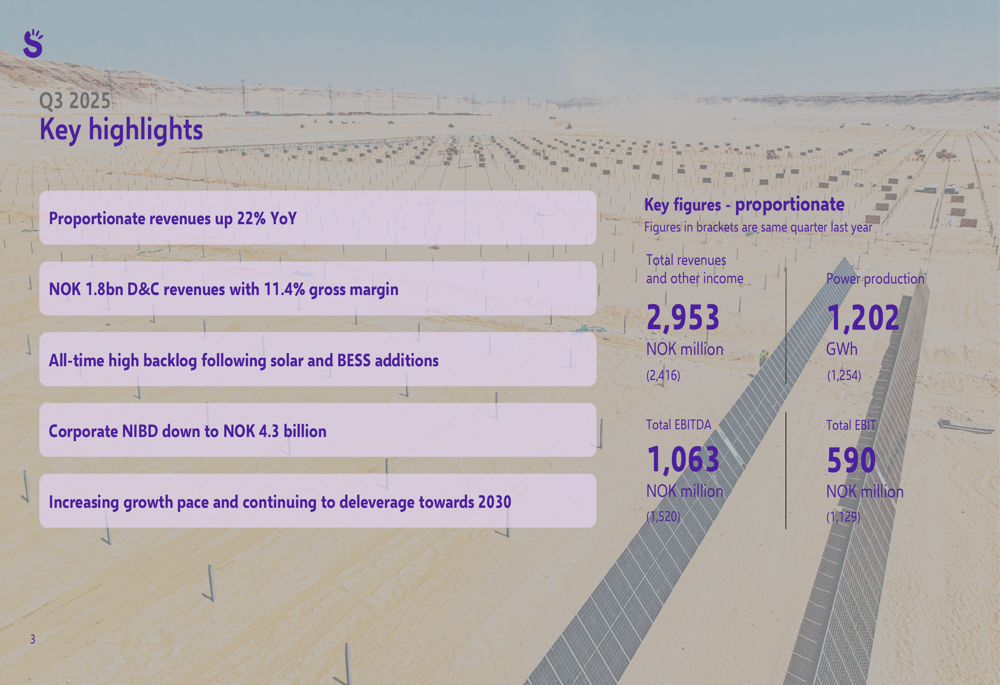

Scatec reported proportionate revenues of NOK 2,953 million in Q3 2025, representing a 22% increase year-over-year. This growth was primarily driven by record-high construction activity, with NOK 1.8 billion in Design & Construction (D&C) revenues at an 11.4% gross margin.

Power production reached 1,202 GWh during the quarter, slightly down from 1,254 GWh in the same period last year, reflecting the impact of asset divestments partially offset by new projects coming online. Power production revenues remained stable at NOK 1.2 billion.

As shown in the following chart of key quarterly highlights:

Despite the revenue growth, total EBITDA declined to NOK 1,063 million from NOK 1,520 million in Q3 2024, while EBIT fell to NOK 590 million from NOK 1,129 million. This reduction was largely due to one-off gains from asset sales in the previous year, as the company noted divested assets and adjusted one-offs of NOK 620 million affecting the year-over-year comparison.

The Philippines operations continued to be a significant contributor to financial results, with the company noting:

"We see strong contribution from our Philippines operations, with ancillary services providing substantial revenue alongside our contracted and spot market sales," said Terje Pilskog, CEO of Scatec.

Strategic Initiatives

Scatec emphasized its strategic positioning in markets where renewables represent the most cost-efficient energy source. The company highlighted its diversified market portfolio spanning established markets like Egypt, South Africa, Philippines, and Brazil, alongside newer growth markets including Romania, Tunisia, Botswana, and Colombia.

The company’s market selection strategy is based on specific criteria including required project returns, cost efficiency of renewables, growing power demand, and stable regulatory environments.

The following image illustrates Scatec’s diversified market portfolio:

A key strategic focus remains the integration of solar PV with Battery Energy Storage Systems (BESS), with CEO Terje Pilskog noting during the earnings call that "battery technology is a game changer for the industry." Scatec has positioned itself at the forefront of this integration with projects in South Africa, the Philippines, and Egypt.

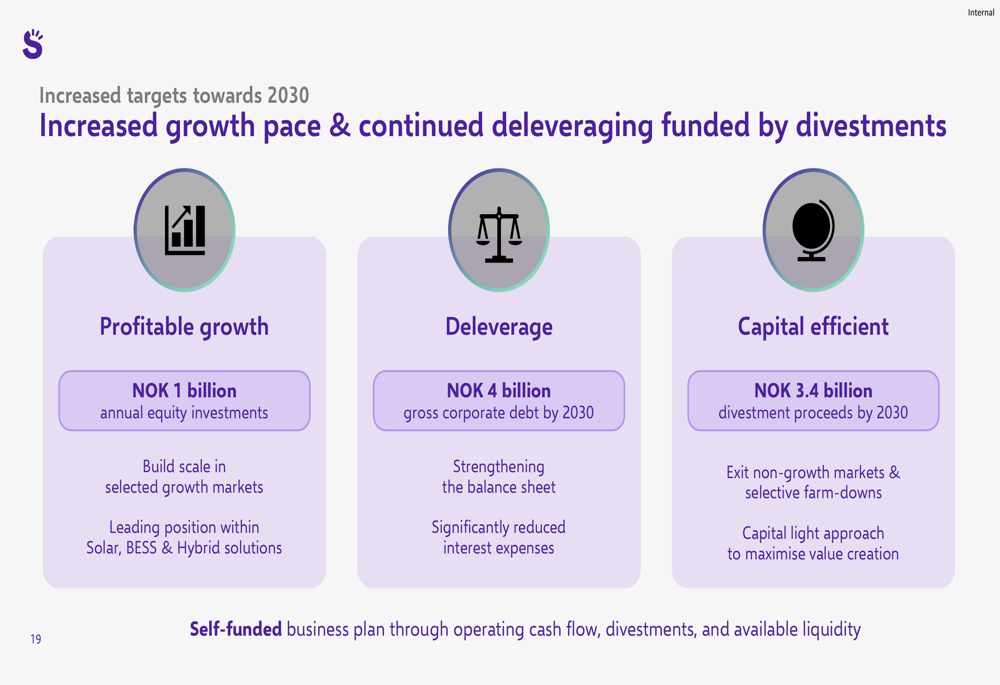

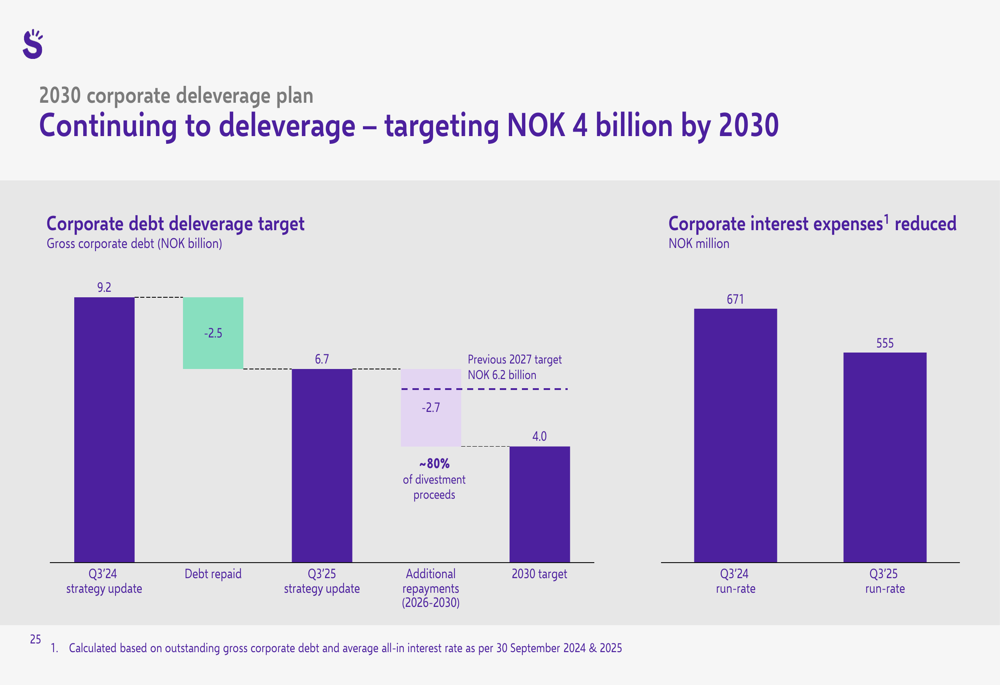

The company’s growth strategy toward 2030 centers around three pillars: profitable growth through NOK 1 billion annual equity investments, deleveraging to NOK 4 billion gross corporate debt by 2030, and capital efficiency through NOK 3.4 billion in divestment proceeds by 2030.

As illustrated in the following strategic targets slide:

Detailed Financial Analysis

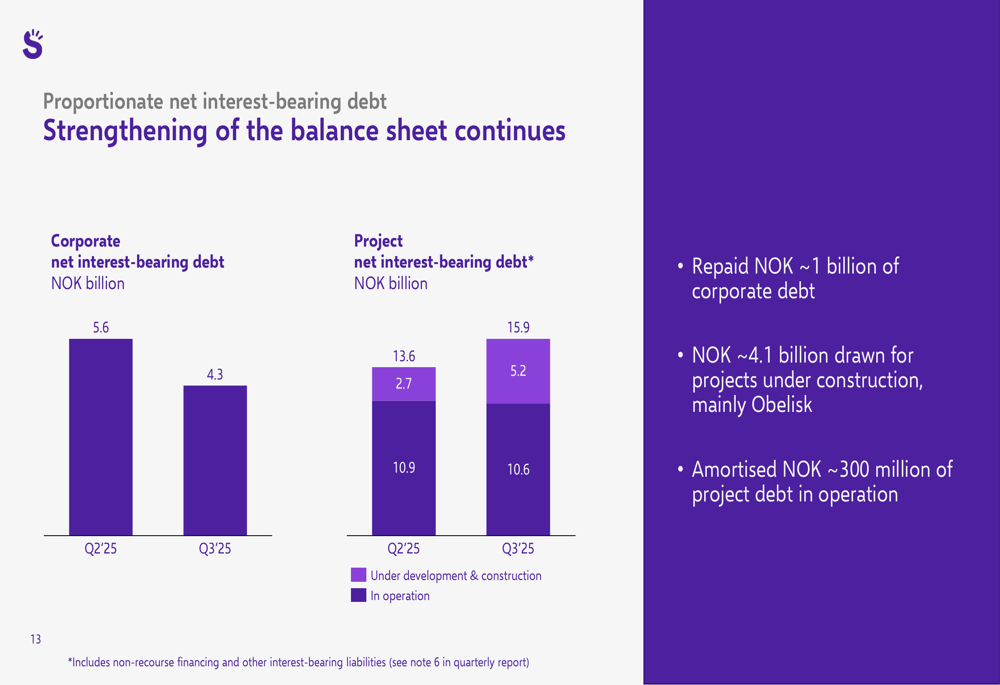

Scatec’s balance sheet continued to strengthen during Q3, with corporate net interest-bearing debt (NIBD) reduced to NOK 4.3 billion. The company maintained a strong liquidity position of approximately NOK 4.7 billion, providing financial flexibility for ongoing and future projects.

The following chart shows the company’s progress in reducing corporate debt:

The company’s construction activity reached an all-time high, with 1,749 MW of solar capacity and 687 MWh of BESS currently under construction across multiple markets. Major projects include 273 MW solar in South Africa, 120 MW solar in Tunisia, and the substantial 1,125 MW solar plus 100MW/200MWh BESS Obelisk project in Egypt.

Scatec’s backlog has grown significantly, with NOK 21 billion in remaining EPC (Engineering, Procurement, and Construction) revenues across construction and backlog projects. The company maintains an estimated average gross margin of 10-12% on these projects.

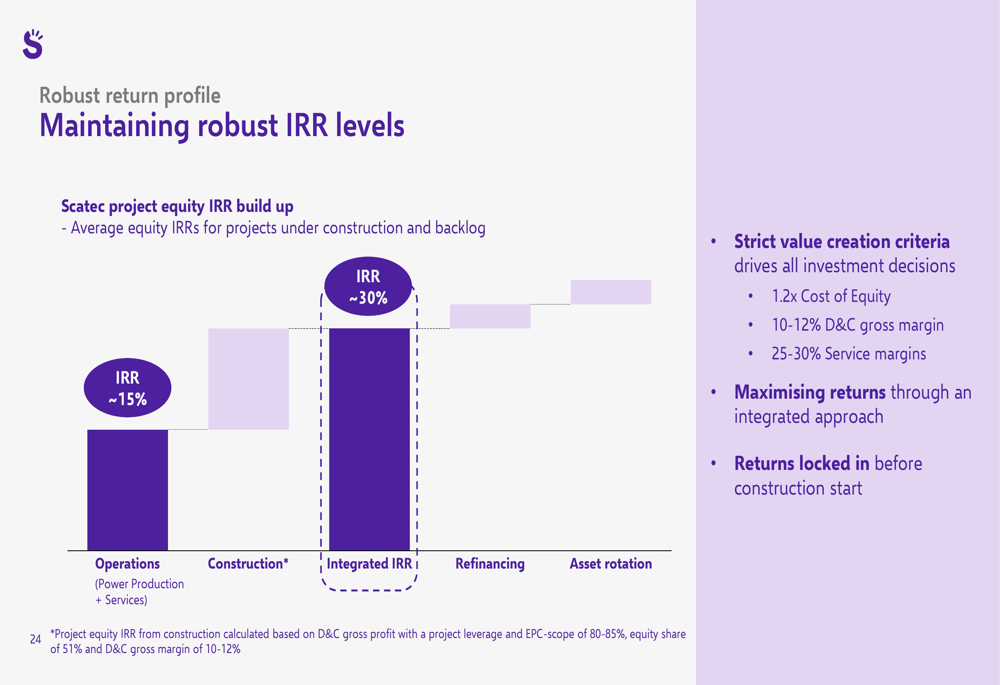

The company’s robust return profile is maintained through multiple value creation levers, as shown in this IRR breakdown:

Forward-Looking Statements

For the full year 2025, Scatec provided guidance of 4,100-4,200 GWh in power production and NOK 4,250-4,450 million in EBITDA. For Q4 2025 specifically, the company expects power production of 1,000-1,100 GWh and Philippines EBITDA of NOK 280-380 million.

The company reaffirmed its 2030 strategic roadmap, targeting continued growth and deleveraging. Scatec plans to invest NOK 1 billion in equity annually, aiming to more than double its operating capacity to 9 GW by 2030.

Divestments remain a key component of Scatec’s capital allocation strategy, with a target of NOK 3.4 billion in divestment proceeds by 2030 to fund growth and debt repayments. The company has demonstrated its ability to execute value-accretive deals with several successful divestments since 2023.

The corporate deleveraging plan shows a clear path toward the 2030 target:

"We are ahead of plan on our strategic targets for 2027," said Hans Jakob Hegge, CFO of Scatec. "Our deleveraging progress has been substantial, and we continue to secure equity investments at a pace that exceeds our original projections."

With renewable energy costs continuing to decline and global demand for clean energy growing, particularly in Scatec’s target markets, the company appears well-positioned to capitalize on the estimated USD 560 trillion in investments expected across its regions and technologies through 2050.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.