60%+ returns in 2025: Here’s how AI-powered stock investing has changed the game

Introduction & Market Context

Spin Master Corp (TSE:TOY) presented its third-quarter 2025 results on October 30, revealing a company navigating challenging market conditions with mixed performance across its three creative centers. The global children's entertainment company, known for brands like PAW Patrol and Rubik's Cube, saw its stock surge 15.42% following the earnings announcement, closing at $22.30, as investors responded positively to better-than-expected results despite revenue declines.

The company's diversified portfolio across Toys, Entertainment, and Digital Games demonstrated varying levels of resilience in a difficult market environment, with Digital Games emerging as a bright spot amid broader challenges in the traditional toy segment.

Quarterly Performance Highlights

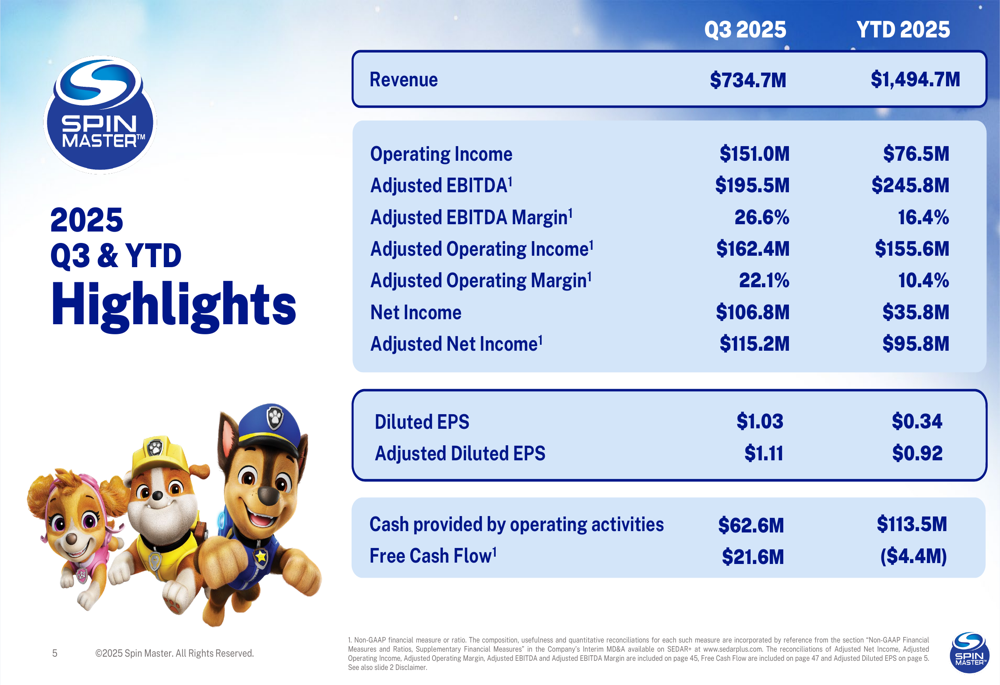

Spin Master reported Q3 2025 revenue of $734.7 million, representing a 17.0% decrease compared to the same period last year. Despite this decline, the company delivered adjusted diluted earnings per share of $1.11, exceeding analyst expectations of $1.05. Operating income reached $151.0 million, while adjusted EBITDA came in at $195.5 million with a robust margin of 26.6%.

As shown in the following financial highlights chart:

Net income for the quarter stood at $106.8 million, translating to diluted EPS of $1.03. The company generated $62.6 million in cash from operating activities and free cash flow of $21.6 million during the quarter, demonstrating continued ability to generate cash despite revenue headwinds.

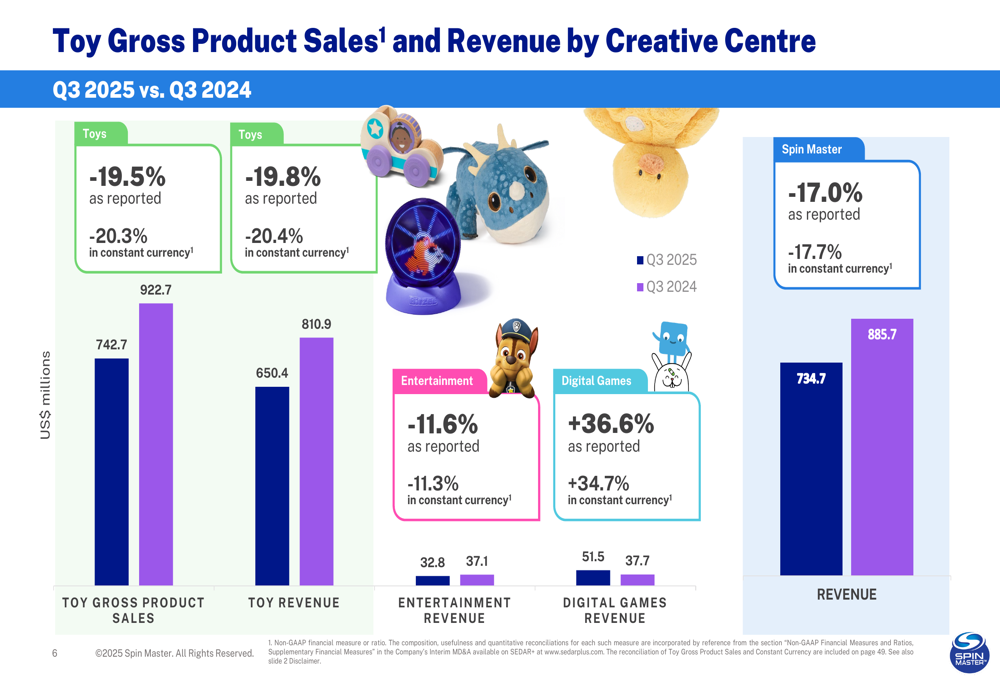

The revenue breakdown by creative center reveals divergent performance across segments:

While overall Toy Gross Product Sales declined by 19.5% to $742.7 million, Digital Games revenue showed impressive growth of 36.6% year-over-year, reaching $51.5 million. Entertainment revenue decreased by 11.6% to $32.8 million compared to Q3 2024.

Segment Analysis

The Toys segment, which remains Spin Master's largest business, faced significant challenges in Q3 2025. Toy revenue declined 19.8% to $650.4 million, though the segment still delivered solid profitability with an operating margin of 19.8% and adjusted EBITDA of $156.4 million.

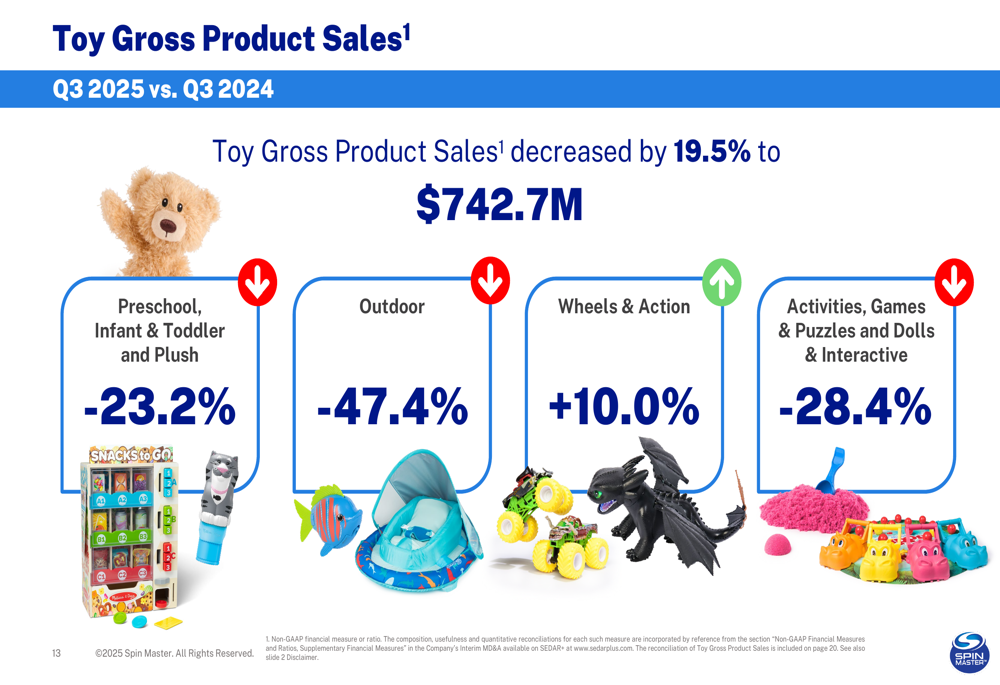

Performance varied significantly across toy categories as illustrated in this breakdown:

The Wheels & Action category was the standout performer with 10.0% growth, while other categories experienced declines, with Outdoor toys seeing the steepest drop at 47.4%. Despite these challenges, Spin Master's point-of-sale metrics outperformed the broader industry, declining 1.2% compared to the industry's 2.6% decrease.

The Entertainment segment generated $32.8 million in revenue with an impressive operating margin of 36.3%. This division continues to leverage key franchises including:

The Digital Games segment emerged as the growth engine for Spin Master in Q3 2025, with revenue increasing 36.6% to $51.5 million. This segment delivered strong profitability with an operating margin of 30.9% and adjusted operating margin of 33.6%.

Despite the revenue growth, Digital Games experienced a decline in monthly active users (MAU), which decreased 12% year-over-year to approximately 51 million in Q3 2025. However, total subscriptions increased by 4% to approximately 453,000 compared to Q3 2024.

Balance Sheet & Cash Flow

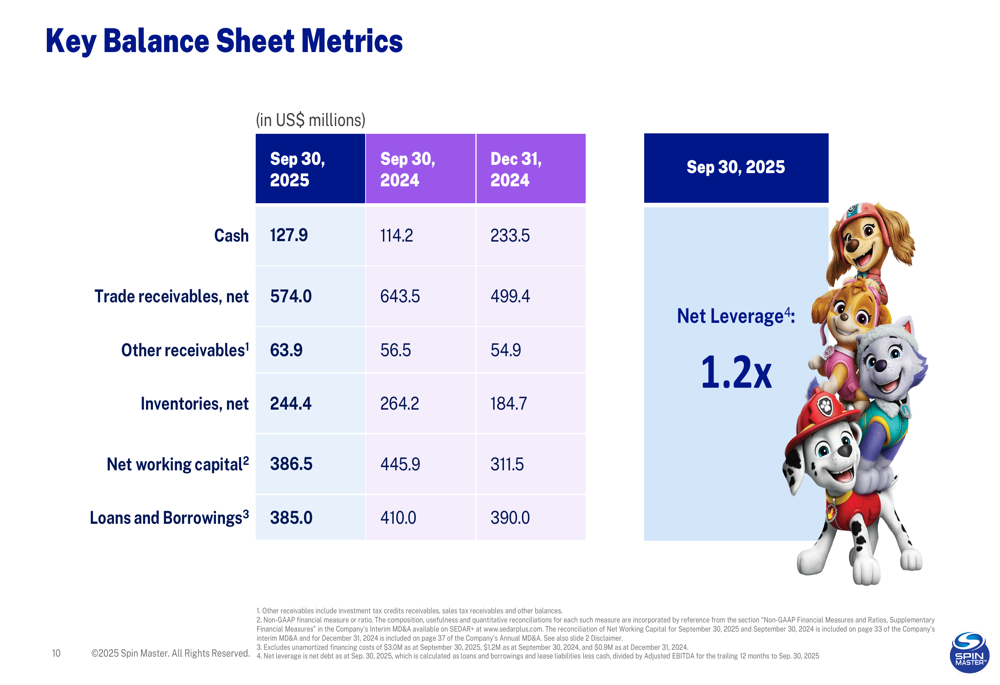

Spin Master maintained a solid balance sheet position with $127.9 million in cash as of September 30, 2025. The company's net working capital stood at $386.5 million, down from $445.9 million a year earlier, reflecting improved inventory management.

The key balance sheet metrics show the company's financial position:

Inventory levels decreased to $244.4 million from $264.2 million in the prior year, demonstrating the company's efforts to optimize working capital. Net leverage remained manageable at 1.2x, providing financial flexibility for future investments and strategic initiatives.

Strategic Initiatives & Outlook

Facing potential tariff impacts, Spin Master outlined a comprehensive mitigation strategy focused on four key areas: procurement, pricing strategy, supply chain optimization, and financial management. The company is actively moving production for the U.S. market out of China while implementing different shipping methodologies to minimize tariff impacts.

CEO Christina Miller expressed optimism during the earnings call, stating, "We fundamentally believe we can return this business to profitable growth." She emphasized the importance of creativity and innovation as core elements of the business strategy moving forward.

The company is also maintaining its commitment to corporate social responsibility under the vision "Reimagining Everyday Play for Future Generations," focusing on environmental sustainability, product quality, people development, and community engagement.

Market Reaction & Analyst Perspectives

The market responded positively to Spin Master's Q3 results, with the stock surging 15.42% following the announcement. This reaction suggests investors are focusing on the company's ability to maintain strong margins and deliver better-than-expected earnings despite revenue challenges.

According to the earnings call, analysts showed particular interest in the performance of the Melissa & Doug brand, digital games monetization strategies, and the company's tariff mitigation efforts. The management team outlined strategies for the upcoming holiday season, emphasizing innovation and consumer engagement as key priorities.

CFO Jonathan Reuter highlighted opportunities for continued operating leverage, noting, "We see an opportunity to continue. We know there's an opportunity to keep driving operating leverage in the business."

With a current stock price of $22.30, significantly above its 52-week low of $18.51 but still below its high of $35.44, Spin Master appears positioned to navigate ongoing industry challenges while leveraging growth opportunities in its Digital Games segment and implementing strategic initiatives to return to overall growth.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.