Missed the webinar? Here are Investing.com’s top 10 stock picks for 2026

Introduction & Market Context

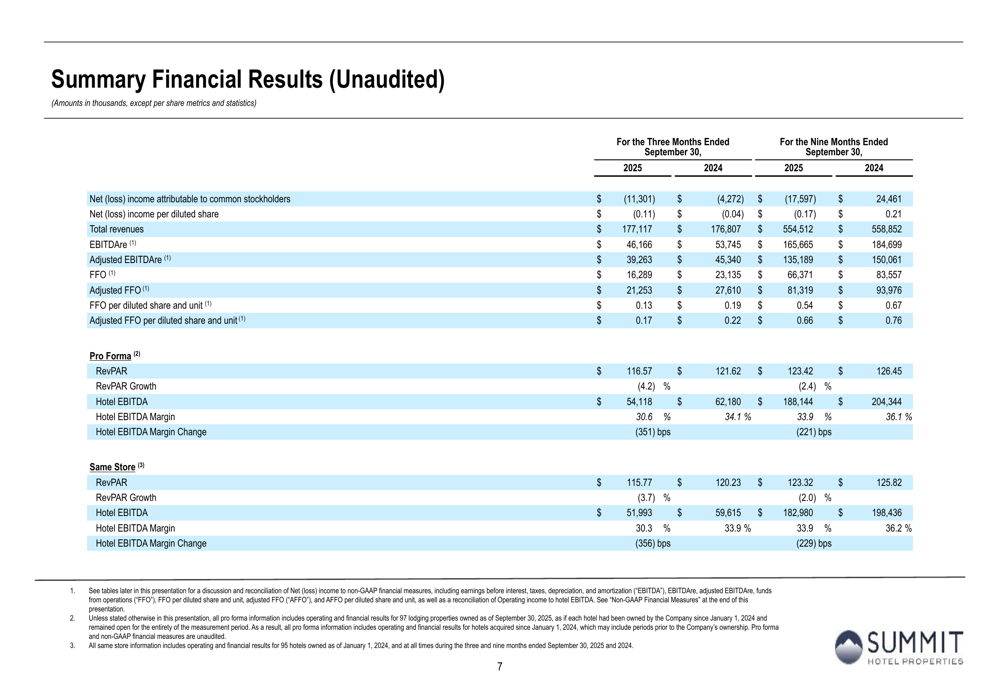

Summit Hotel Properties (NYSE:INN) released its third-quarter 2025 earnings presentation on November 5, revealing a challenging period for the hotel REIT. The company reported a widening net loss and declining key performance metrics compared to the same period last year, while revenue remained relatively stable. The stock closed at $5.14, up 1.17% on the day, but remains well below its 52-week high of $6.99.

The company's presentation highlighted deteriorating performance across several key metrics, most notably a 4.2% year-over-year decline in Revenue Per Available Room (RevPAR). This decline aligns with the company's earnings call, where management reported an EPS of -$0.11, missing analyst expectations of -$0.05 by a significant margin.

Quarterly Performance Highlights

Summit Hotel Properties reported total revenues of $177.12 million for Q3 2025, essentially flat compared to $176.81 million in Q3 2024. However, the company's bottom line deteriorated, with a net loss attributable to common stockholders of $11.3 million, compared to a loss of $4.27 million in the same quarter last year.

As shown in the following summary of financial results, key performance metrics declined across the board:

The company's RevPAR declined to $116.57 in Q3 2025, down 4.2% from $121.62 in Q3 2024. This decline was driven by weakness in both occupancy and average daily rate (ADR). Hotel EBITDA fell to $54.12 million from $62.18 million in the prior year, with margins contracting to 30.6%.

During the earnings call, management noted that government and international travel declined 20% year-over-year, contributing significantly to the overall performance challenges.

Detailed Financial Analysis

A closer examination of Summit's quarterly progression reveals that Q3 represented a significant step down from the stronger performance seen earlier in the year. The following chart illustrates this trend:

The company's Adjusted EBITDAre for Q3 2025 was $39.26 million, down from $45.34 million in Q3 2024. Similarly, Adjusted FFO applicable to common shares and Common Units fell to $21.25 million ($0.17 per share) from $27.61 million ($0.22 per share) in the prior year.

The reconciliation from net loss to Adjusted EBITDAre provides insight into the various adjustments made to arrive at this key performance metric:

Similarly, the reconciliation to Adjusted FFO shows the progression from net loss to this important cash flow metric:

Despite the challenging quarter, Summit Hotel Properties reported some positive developments during the earnings call, including a 5.6% increase in non-rooms revenue and a RevPAR index increase of 140 basis points to 116%, indicating market share gains relative to competitors.

Debt and Capitalization

Summit Hotel Properties' presentation provided a detailed look at its capital structure and debt profile. As of September 30, 2025, the company had a total enterprise value of approximately $2.37 billion and a pro rata enterprise value of $2.05 billion.

The following slide details the company's capitalization structure:

The company's share price has declined over the past year, from $6.86 on September 30, 2024, to $5.49 on September 30, 2025, reducing the market value of common equity. This decline is consistent with the challenging operating environment and deteriorating financial performance.

Summit's debt schedule reveals a well-structured maturity profile with no immediate refinancing needs:

The company has a $275 million delayed draw term loan in place to refinance convertible senior notes maturing in February 2026, providing near-term financial flexibility. The debt maturity ladder shows limited maturities until 2028:

During the earnings call, management highlighted this debt structure as a source of stability, noting that no significant debt maturities are expected until 2028 after addressing the 2026 convertible notes.

Forward-Looking Statements

Summit Hotel Properties' management provided a cautious outlook for the remainder of 2025. According to the earnings call, the company expects RevPAR to decline by 2-2.5% in Q4 2025, resulting in a full-year RevPAR decline of 2.25-2.5%.

Despite these near-term challenges, CEO John Stanner expressed optimism about the company's future, stating, "We remain optimistic on the outlook for our industry generally and Summit more specifically." Management highlighted anticipated demand increases in urban markets and potential benefits from the 2026 World Cup as factors that could drive improved performance next year.

The company continues to pay a quarterly dividend of $0.08 per share, representing a yield of approximately 6% based on the current share price.

Summit's portfolio remains diversified across various hotel brands and locations, potentially positioning the company to benefit from a recovery in travel demand when market conditions improve. However, the continued decline in government and international travel, along with potential macroeconomic pressures affecting leisure demand, remain significant challenges for the near term.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.