Bitcoin set for a rebound that could stretch toward $100000, BTIG says

Introduction & Market Context

Synsam AB (STO:SYNSAM) released its Q3 2025 results presentation on November 18, 2025, showcasing strong performance across its Nordic operations despite a restrained consumer environment. The optical retailer's stock responded positively, rising 4.24% to 61.50 SEK following the announcement.

The company continues to gain market share across the Nordic region while maintaining its strategic focus on subscription-based services and technological innovation. This quarter's results demonstrate Synsam's resilience in navigating challenging market conditions while executing its long-term growth strategy.

Quarterly Performance Highlights

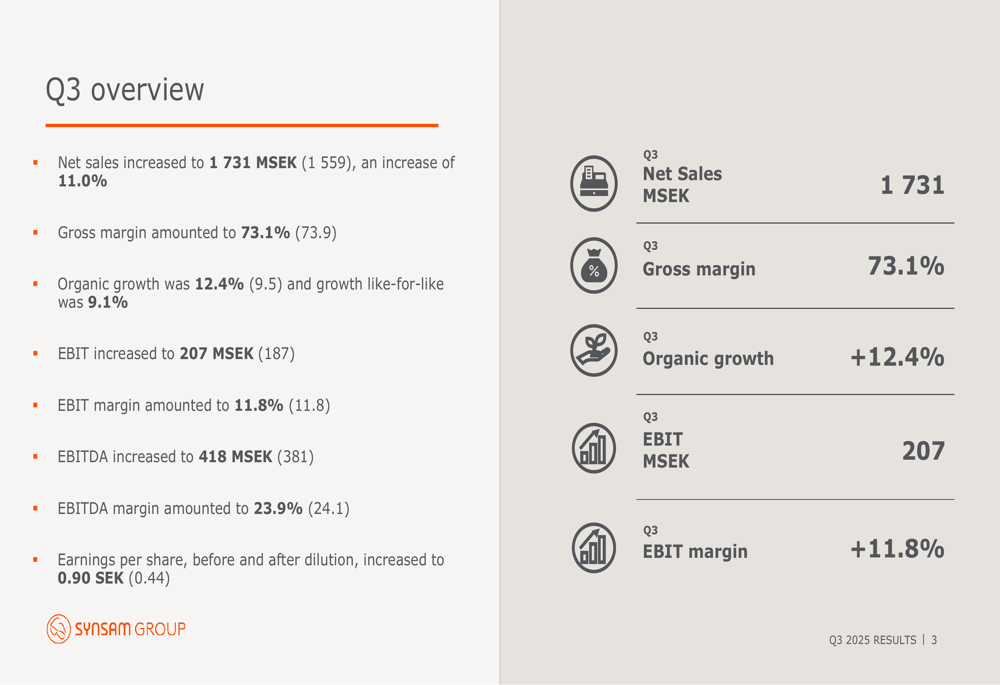

Synsam reported robust financial results for Q3 2025, with net sales increasing to 1,731 MSEK, representing an 11.0% growth compared to 1,559 MSEK in the same period last year. The company achieved significant organic growth of 12.4% (vs 9.5% in Q3 2024) and like-for-like growth of 9.1% (vs 6.3%).

EBIT rose to 207 MSEK from 187 MSEK in Q3 2024, while maintaining a stable EBIT margin of 11.8%. Notably, earnings per share more than doubled to 0.90 SEK from 0.44 SEK in the comparable period.

As shown in the following overview of Q3 performance metrics:

The company's gross margin experienced a slight contraction to 73.1% from 73.9% in the prior year, which management attributed to mix effects and planned campaigns during the earnings call. Despite this minor decline, Synsam maintained strong profitability with an EBITDA margin of 23.9% (vs 24.1% in Q3 2024).

Regional Performance Analysis

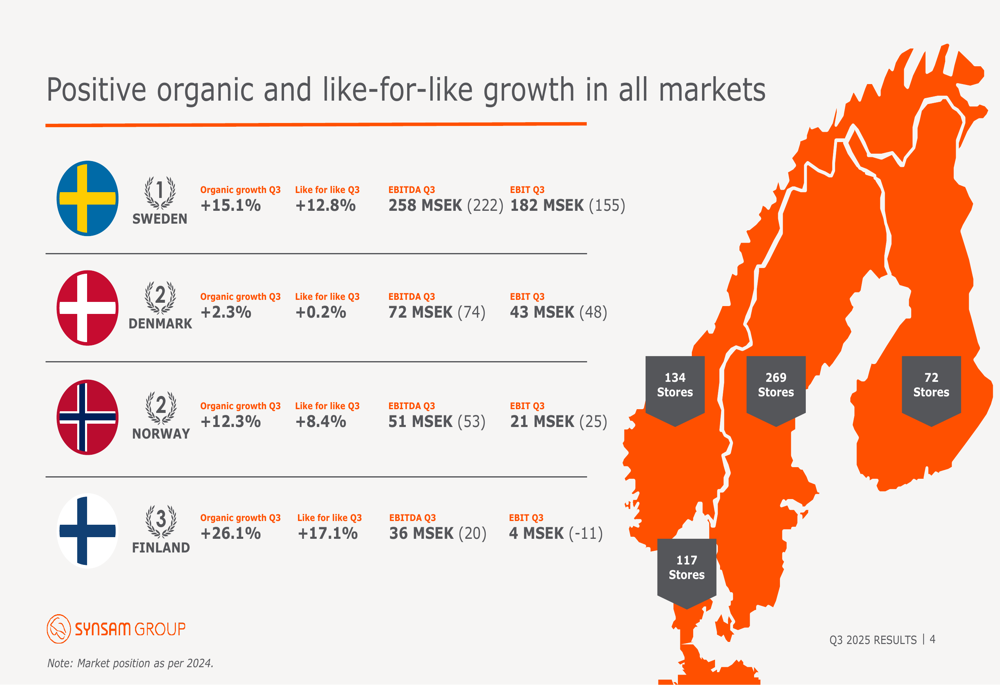

Synsam demonstrated positive organic growth across all its Nordic markets, with particularly strong performance in Finland and Sweden. The company operates a total of 592 stores across the region, with its largest presence in Sweden (269 stores).

The regional breakdown reveals varying growth rates and profitability metrics:

Sweden led with impressive 15.1% organic growth and 12.8% like-for-like growth, generating an EBIT of 182 MSEK. Finland showed the most dramatic improvement with 26.1% organic growth and 17.1% like-for-like growth, turning around from a negative EBIT position last year to 4 MSEK this quarter.

Denmark delivered more modest growth at 2.3% organic and 0.2% like-for-like, but achieved a notable 14.8% EBIT margin according to the earnings call transcript, exceeding the company's targets. Norway maintained solid performance with 12.3% organic growth and 8.4% like-for-like growth.

Business Segment Performance

Synsam's business is divided into two main segments: the subscription-based Synsam Lifestyle and traditional cash sales. Both segments demonstrated strong growth in Q3 2025.

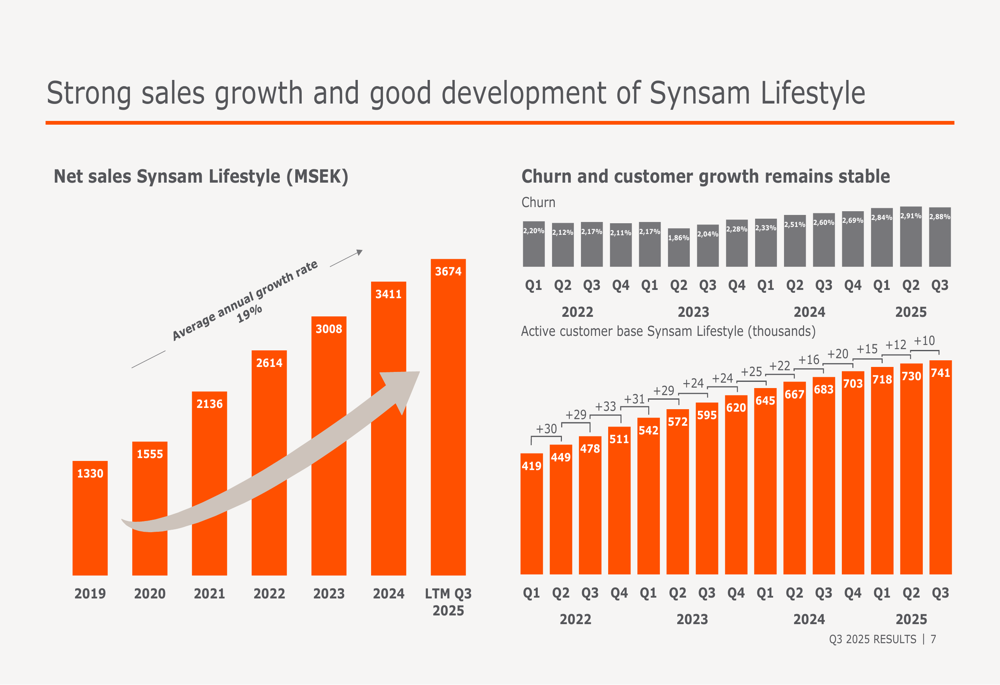

The Synsam Lifestyle subscription business generated sales of 897 MSEK, increasing 10.8% from 809 MSEK in Q3 2024. This segment continues to be a key growth driver for the company, with a remarkable 19% average annual growth rate since 2019.

The following chart illustrates the consistent growth trajectory of the Lifestyle segment:

Meanwhile, the traditional cash business also performed well, with net sales of 835 MSEK, up 11.2% from 750 MSEK in the same period last year. This segment has maintained a steady 5% average annual growth rate since 2019.

As shown in the following visualization of cash sales development:

The company's dual business model provides balanced growth opportunities while the subscription model continues to build a stable recurring revenue base. The active customer base for Synsam Lifestyle has remained stable, with consistent churn rates, indicating strong customer satisfaction and retention.

Technology Implementation & Innovation

Synsam continues to invest in technological innovation, with its Synsam EyeView digital eye examination system showing promising adoption rates. During Q3 2025, 17% of all eye examinations in Sweden and 20% in Norway were conducted using this technology.

The earnings call also highlighted the introduction of innovative products such as smart glasses and hearing spectacles, though these were not prominently featured in the presentation slides. These innovations align with the company's strategic focus on being "best in town," as emphasized by CCO Jimmy Engström during the earnings call.

Long-term Financial Trends

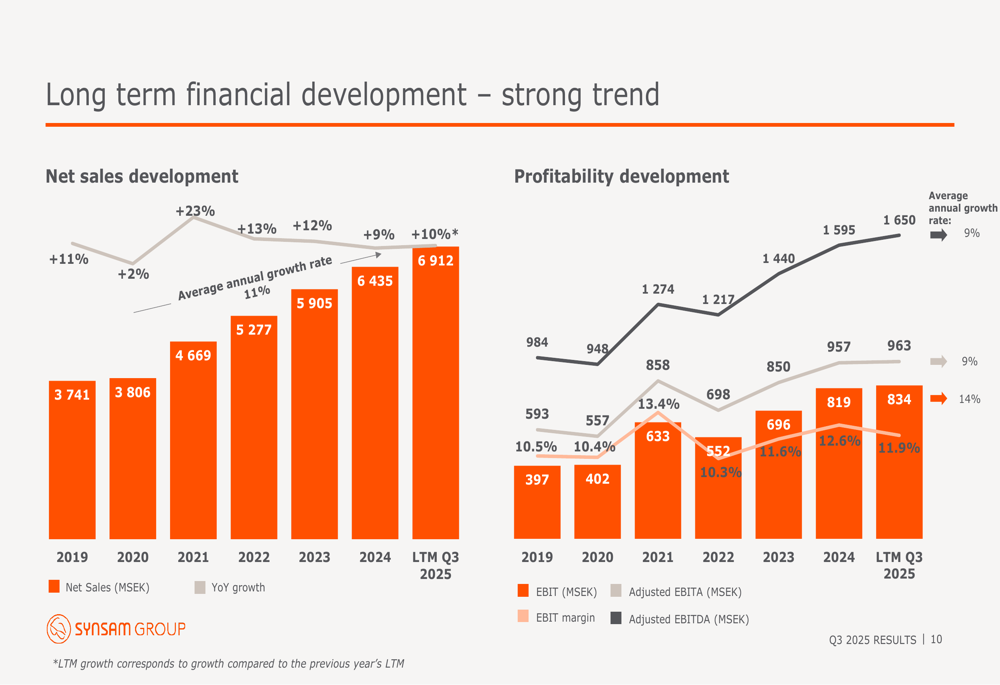

Synsam's presentation emphasized its consistent long-term financial development, showcasing steady growth in both net sales and profitability metrics since 2019.

The following chart illustrates these long-term trends:

Net sales have grown at an 11% average annual rate from 3,741 MSEK in 2019 to 6,912 MSEK in the last twelve months ending Q3 2025. Similarly, EBIT has shown a 9% average annual growth rate over the same period.

Cash flow remains strong, with cash flow from operating activities before changes in working capital increasing to 329 MSEK from 298 MSEK in Q3 2024. The company's net debt to adjusted EBITDA ratio stands at 1.87, slightly higher than 1.76 in the previous year but improved from 1.88 in Q4 2024.

Forward-Looking Statements

Looking ahead, Synsam expressed optimism about its growth prospects despite operating in what it describes as a "restrained" consumer market. The company expects continued positive development across all markets, with particular emphasis on Denmark for 2026.

CFO Per Hedblom indicated during the earnings call that Synsam aims to move higher within its 12-15% EBIT margin target range over the coming years. The company does not anticipate significant legislative changes impacting its operations in 2026, though it noted that credit legislation changes in Denmark could potentially affect lifestyle sales.

Synsam's strategy continues to focus on organic growth, operational efficiency, and technological innovation to maintain its market leadership position across the Nordic region. With double-digit growth in both business segments and improving performance in previously challenging markets like Finland, the company appears well-positioned to continue its growth trajectory despite macroeconomic pressures.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.