60%+ returns in 2025: Here’s how AI-powered stock investing has changed the game

Introduction & Market Context

Tourmaline Oil Corp. (TSX:TOU) recently presented its corporate strategy following a challenging third quarter where the company missed earnings expectations. The November 2025 presentation outlines Tourmaline's position as Canada's largest natural gas producer and details ambitious growth plans through 2031, despite recent financial underperformance.

The company's stock has been under pressure, trading at CAD 59.71 after falling 2.58% on November 6, well below its 52-week high of CAD 70.73. This follows a disappointing Q3 2025 earnings report where Tourmaline posted EPS of CAD 0.49, missing analyst expectations of CAD 0.82 by 40.26%, while revenue of CAD 1.48 billion fell short of forecasts by 3.27%.

Growth Strategy & Production Outlook

Despite recent challenges, Tourmaline's presentation emphasizes its scale and growth trajectory. The company currently produces between 655,000-665,000 barrels of oil equivalent per day (boepd) and projects 2026 production to reach 690,000-710,000 boepd. More notably, the company outlines an EP Growth Plan that aims to increase production to 850,000 boepd by 2031.

As shown in the following overview slide, Tourmaline boasts substantial reserves of 5.5 billion boe (24.8 Tcf gas and 1,356 MMbbls liquids) and maintains the lowest capital cost structure in the basin:

This ambitious growth plan comes despite Q3 2025 production averaging 634,750 boepd, which CEO Mike Rose noted was "at the high end of guidance" during the earnings call. The company's production outlook shows systematic development across multiple areas, with significant contributions expected from North Montney and Groundbirch expansions.

Competitive Positioning

Tourmaline's presentation highlights its dominant position in the North American natural gas market. The company ranks as Canada's largest natural gas producer and the fifth largest gas-focused producer across North America, emphasizing that "scale is a key component in driving down costs, leveraging transport & marketing opportunities, and remaining relevant."

The following chart illustrates Tourmaline's natural gas production relative to other major North American producers:

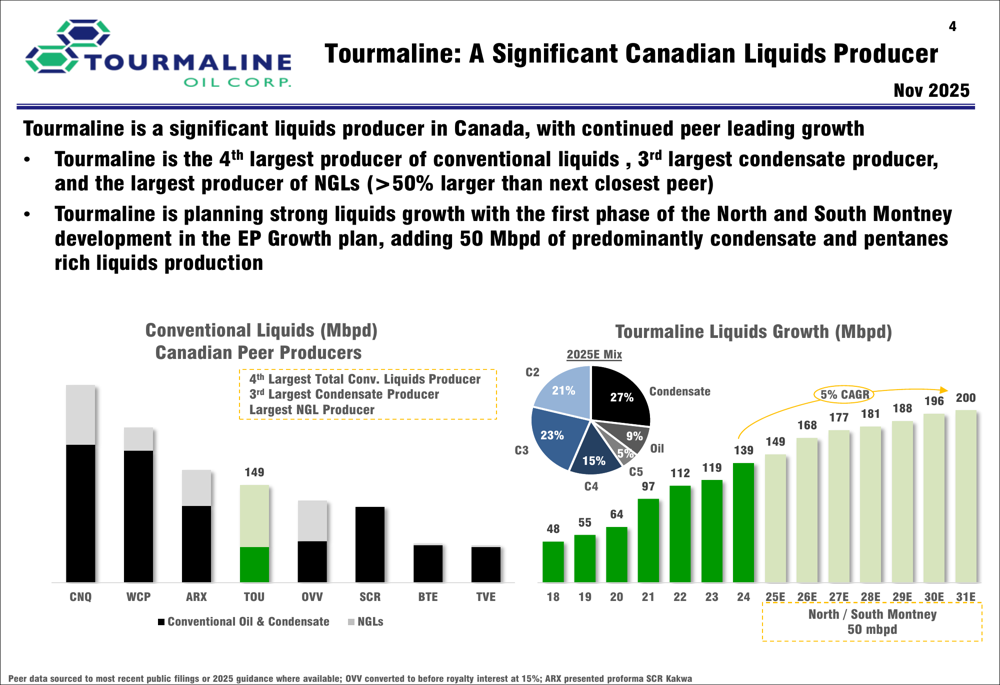

Beyond natural gas, Tourmaline has established itself as a significant liquids producer in Canada, ranking as the 4th largest producer of conventional liquids, 3rd largest condensate producer, and the largest producer of NGLs—more than 50% larger than its closest peer. The company expects to add 50,000 barrels per day of predominantly condensate and pentanes-rich liquids production through its North and South Montney development.

As shown in the following slide, Tourmaline's liquids business has grown substantially and is projected to continue expanding:

Financial Projections & Performance

Tourmaline's presentation outlines ambitious financial targets that stand in contrast to its recent performance. For 2026, the company projects cash flow of CAD 4.0 billion and free cash flow of CAD 0.9 billion. By 2031, these figures are expected to reach CAD 5.79 billion and CAD 2.995 billion, respectively, assuming flat commodity prices.

However, these projections come after a challenging Q3 2025 where cash flow totaled CAD 720 million and earnings were just CAD 190 million. During the earnings call, management cited "weak AECO and Station 2 gas prices, the lowest in 30 years" as a significant headwind.

The company has demonstrated consistent improvement in capital efficiency over time, which it expects to continue supporting its financial goals:

Infrastructure & LNG Strategy

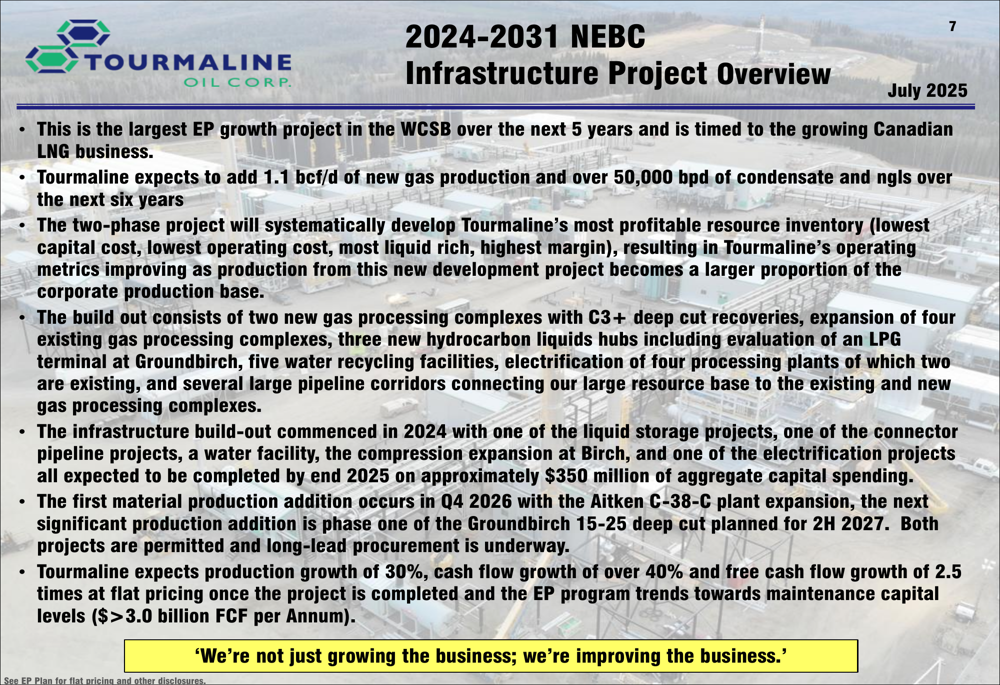

A cornerstone of Tourmaline's growth strategy is its NEBC infrastructure project, described as "the largest EP growth project in the WCSB over the next 5 years." The company plans to add 1.1 bcf/d of new gas production and over 50,000 bpd of condensate and NGLs over the next six years.

As detailed in the following slide, the infrastructure buildout includes new gas processing complexes, liquids hubs, water recycling facilities, and plant electrification:

Tourmaline is also expanding its exposure to international pricing through LNG partnerships and agreements, positioning itself to benefit from global natural gas markets beyond local AECO pricing. The company's transportation and marketing strategy includes diversification across multiple pricing hubs:

The company's LNG strategy includes partnerships with Rockies LNG and support for the NeeStaNan Utility Corridor (Hudson Bay LNG), with growing LNG exposure projected over the coming decade:

Operational Efficiency & Environmental Performance

Tourmaline emphasizes its operational efficiency and continuous improvement in drilling and completion (D&C) performance. The company has achieved significant cost reductions while increasing well productivity:

During the earnings call, CEO Mike Rose highlighted the company's focus on cost reduction, stating, "We're targeting a 5% OPEX reduction in the Deep Basin next year." This aligns with the presentation's emphasis on margin improvement and cost efficiency.

On the environmental front, Tourmaline claims the lowest net emissions intensity among Canadian senior producers, having achieved a 41% emission intensity reduction since 2013. The company has received an "A" rating from MSCI for its environmental performance.

Outlook & Challenges

While Tourmaline's presentation paints an optimistic picture of growth and financial strength, the company faces significant challenges. The recent earnings miss highlights vulnerability to weak natural gas prices, which management acknowledged as a continuing concern.

The company is banking on LNG Canada to improve market dynamics, with Rose noting during the earnings call that "LNG Canada will go from not doing anything in the first half of this year to doing close to and up to 2 billion cubic feet a day." This increased demand could potentially support natural gas prices and Tourmaline's financial performance.

Tourmaline's dividend strategy remains a focus, with the company highlighting a base dividend yield of 3% and total yield (including special dividends) of 5%. The company's substantial insider ownership—the largest among senior E&P peers—aligns management interests with shareholders as it pursues its ambitious growth strategy.

Despite recent underperformance, Tourmaline's presentation makes a compelling case for its long-term potential, summarized by the quote: "We're not just growing the business; we're improving the business." Investors will be watching closely to see if the company can overcome current market challenges to deliver on its ambitious growth and financial targets.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.