Moody’s downgrades Senegal to Caa1 amid rising debt concerns

Introduction & Market Context

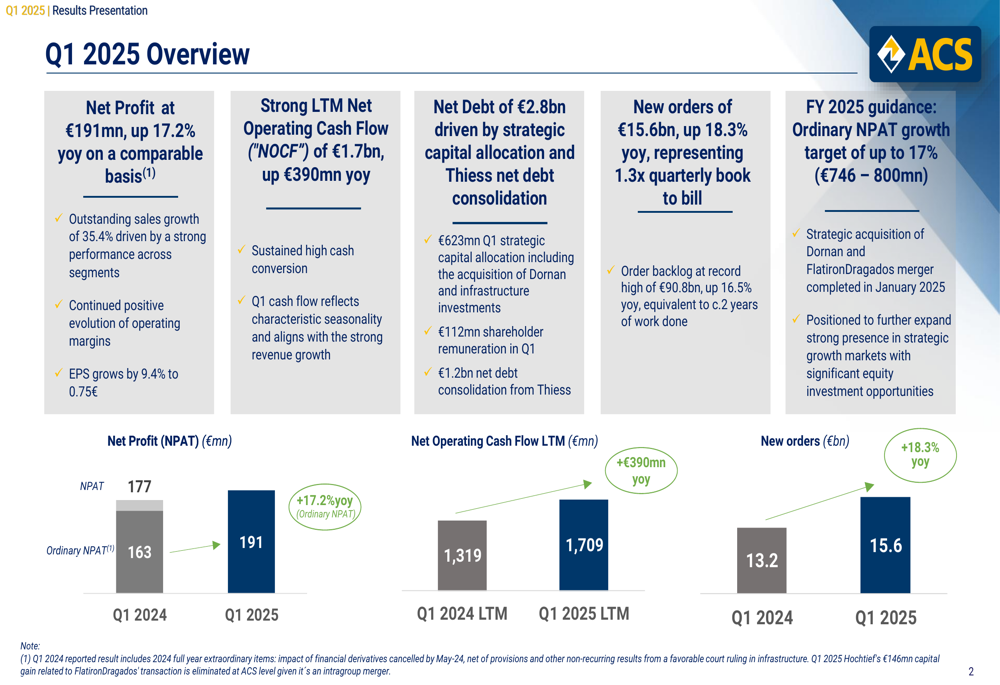

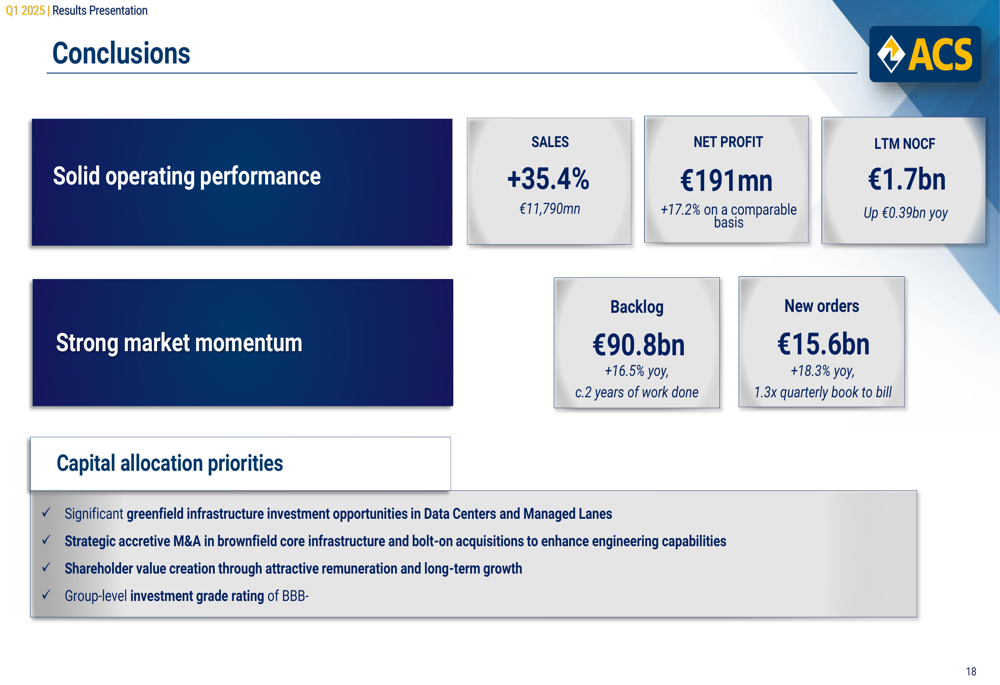

ACS Group presented its Q1 2025 financial results on May 13, 2025, reporting strong growth across key metrics despite increased net debt from strategic acquisitions. The construction and infrastructure giant delivered a 17.2% increase in net profit on a comparable basis, reaching €191 million, while sales surged 35.4% to €11.79 billion.

The company’s performance was bolstered by exceptional growth in its Turner segment and the successful integration of strategic acquisitions, including Dornan and the consolidation of Thiess. ACS continues to benefit from its strong positioning in high-growth sectors like data centers and sustainable infrastructure, particularly in the North American market.

As shown in the following overview of key financial metrics, ACS demonstrated robust growth across most performance indicators:

Quarterly Performance Highlights

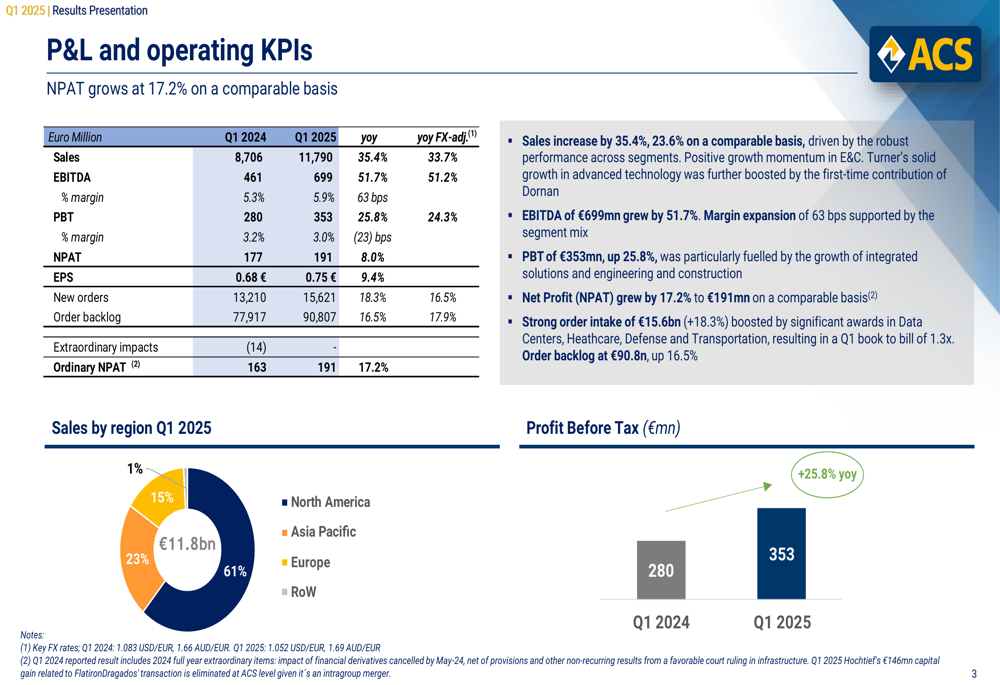

ACS Group reported significant improvements in profitability metrics for Q1 2025, with EBITDA increasing 51.7% year-over-year to €699 million, representing a margin expansion from 5.3% to 5.9%. Profit before tax grew 25.8% to €353 million, while earnings per share rose 9.4% to €0.75.

The company’s sales distribution remains heavily weighted toward North America, which accounts for 61% of total revenue, followed by Europe (23%) and Asia Pacific (15%). This geographic diversification, combined with a strategic focus on high-growth sectors, has contributed to ACS’s strong performance in the quarter.

The detailed breakdown of profit and loss statement and key performance indicators is illustrated in the following slide:

The company’s attributable ordinary net profit showed solid growth across most segments, with Integrated Solutions (particularly Turner) and Engineering & Construction delivering exceptional performance. However, the Infrastructure segment, primarily Abertis, experienced a decline in profitability compared to the previous year.

Detailed Financial Analysis

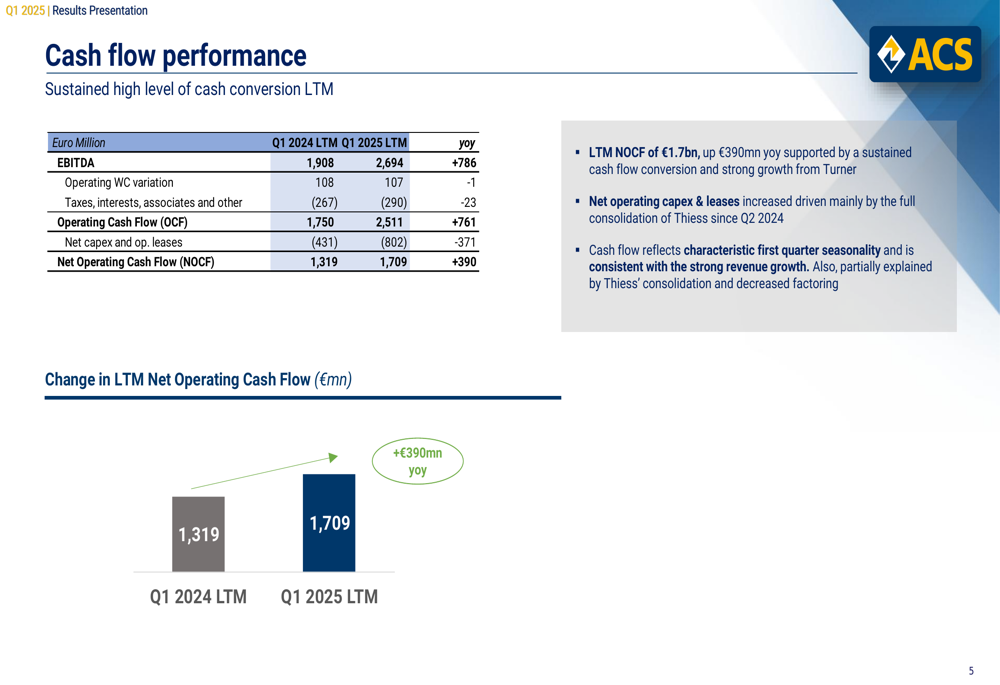

ACS Group maintained strong cash flow generation, with last twelve months (LTM) net operating cash flow reaching €1.7 billion, an increase of €390 million year-over-year. This robust cash performance supported the company’s strategic capital allocation, including acquisitions and shareholder remuneration.

The following slide illustrates the company’s sustained high level of cash conversion and strong cash flow performance:

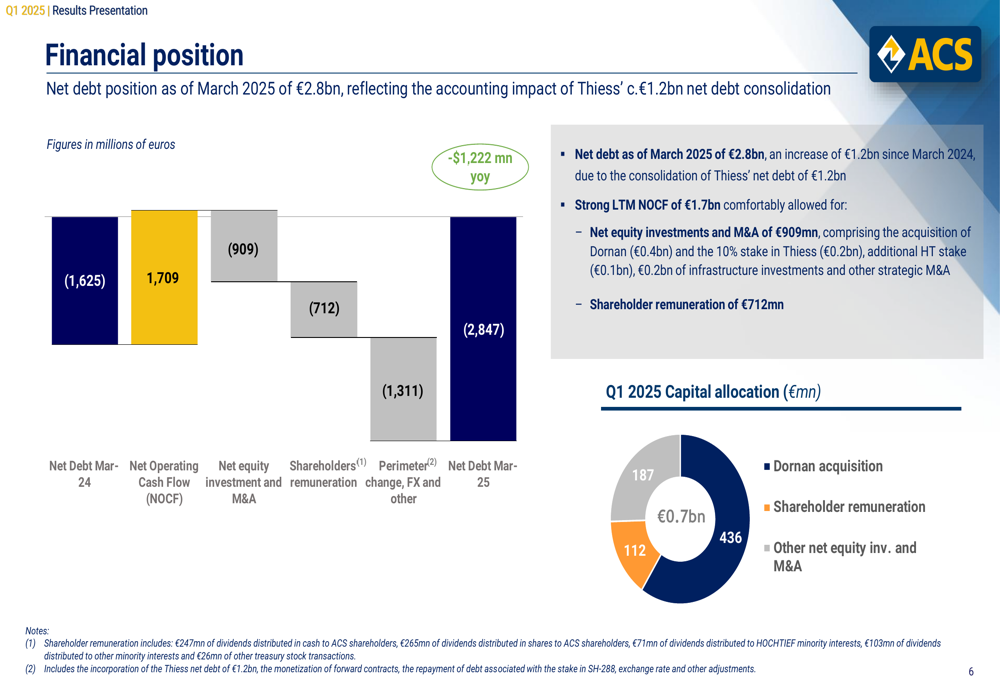

Despite strong cash generation, ACS’s net debt position increased to €2.8 billion as of March 2025, up from €1.6 billion a year earlier. This increase was primarily driven by strategic acquisitions, including Dornan (€187 million) and a 10% stake in Thiess, as well as the consolidation of Thiess’s net debt of approximately €1.2 billion.

The company’s capital allocation strategy is detailed in the following financial position slide:

Segment Performance

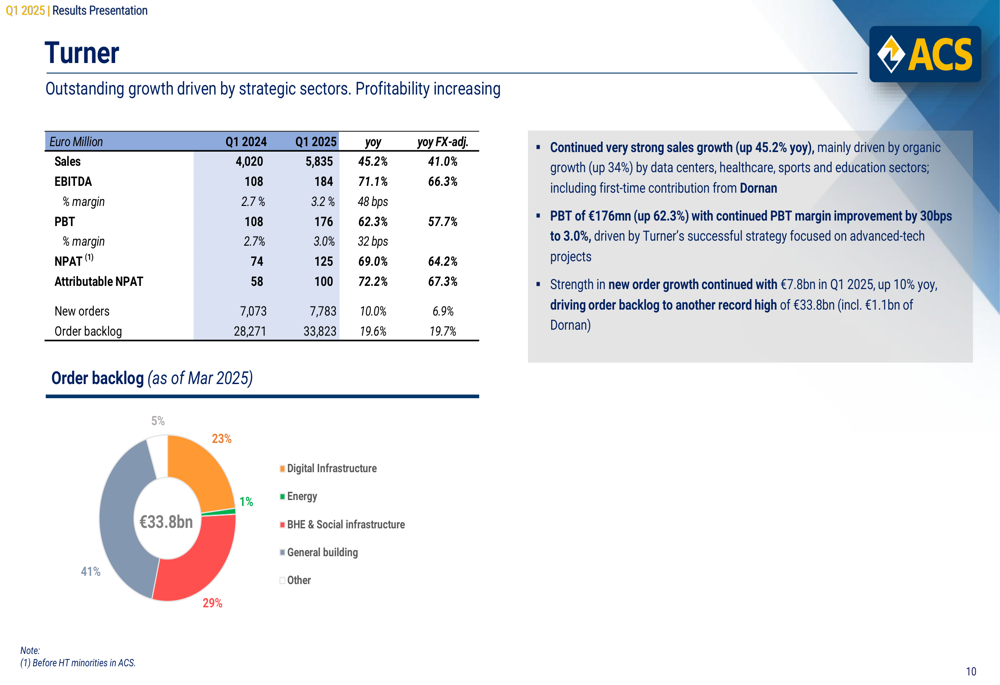

Turner, ACS’s largest segment, delivered outstanding growth with sales increasing 45.2% year-over-year to €5.8 billion. This growth was driven by both organic expansion (34%) in data centers, healthcare, sports, and education sectors, as well as the first-time contribution from Dornan. Turner’s profit before tax surged 62.3% to €176 million, with margin improvement of 30 basis points to 3.0%.

The following slide highlights Turner’s exceptional performance and strategic focus on advanced-tech projects:

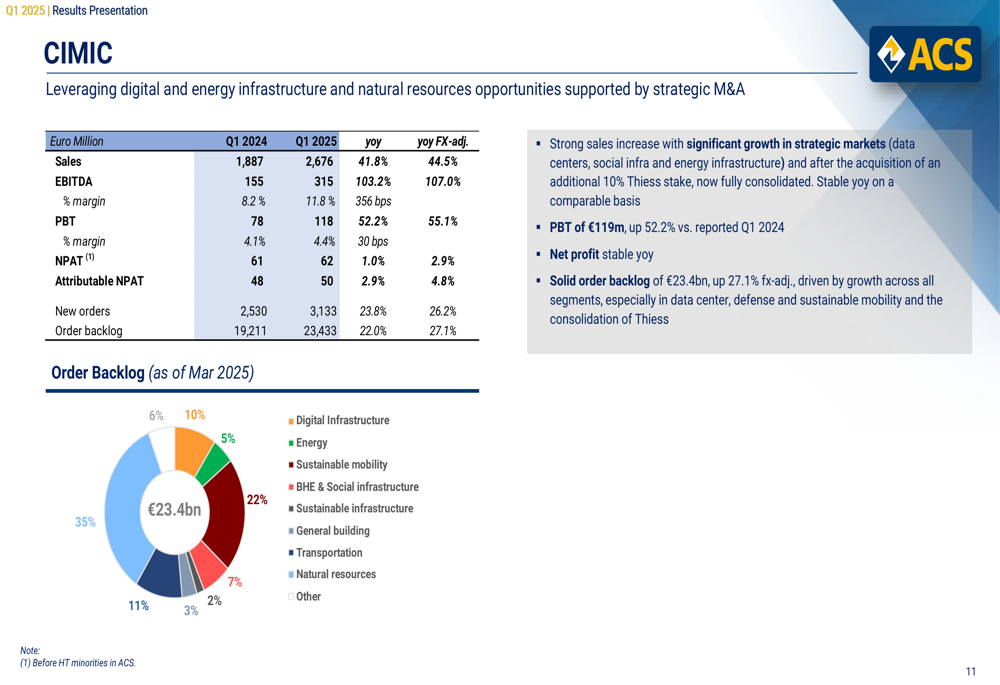

CIMIC also demonstrated strong sales growth, with revenue increasing 41.8% to €2.7 billion, driven by significant growth in strategic markets. While profit before tax grew 52.2% to €118 million, net profit remained relatively stable year-over-year at €62 million. CIMIC’s order backlog reached €23.4 billion, up 22.0% from the previous year.

The detailed performance of CIMIC is illustrated in the following slide:

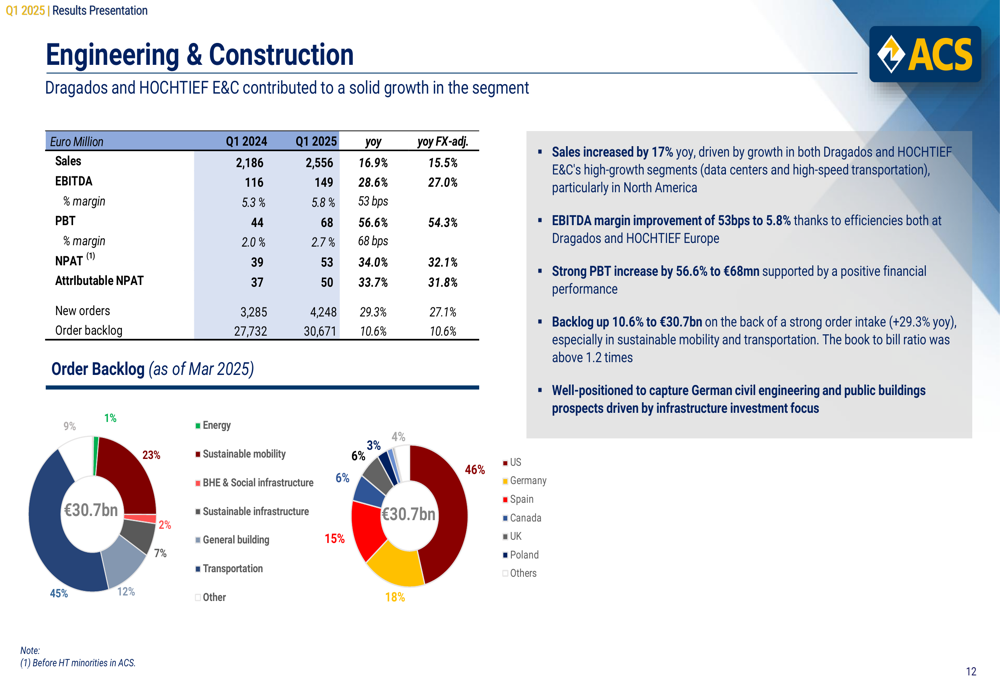

The Engineering & Construction segment, comprising Dragados and HOCHTIEF E&C, contributed to solid growth with sales increasing 16.9% to €2.6 billion and net profit rising 34.0% to €53 million. The segment’s order backlog stood at €30.7 billion, up 10.6% year-over-year.

The following slide provides a comprehensive overview of the Engineering & Construction segment’s performance:

Strategic Initiatives

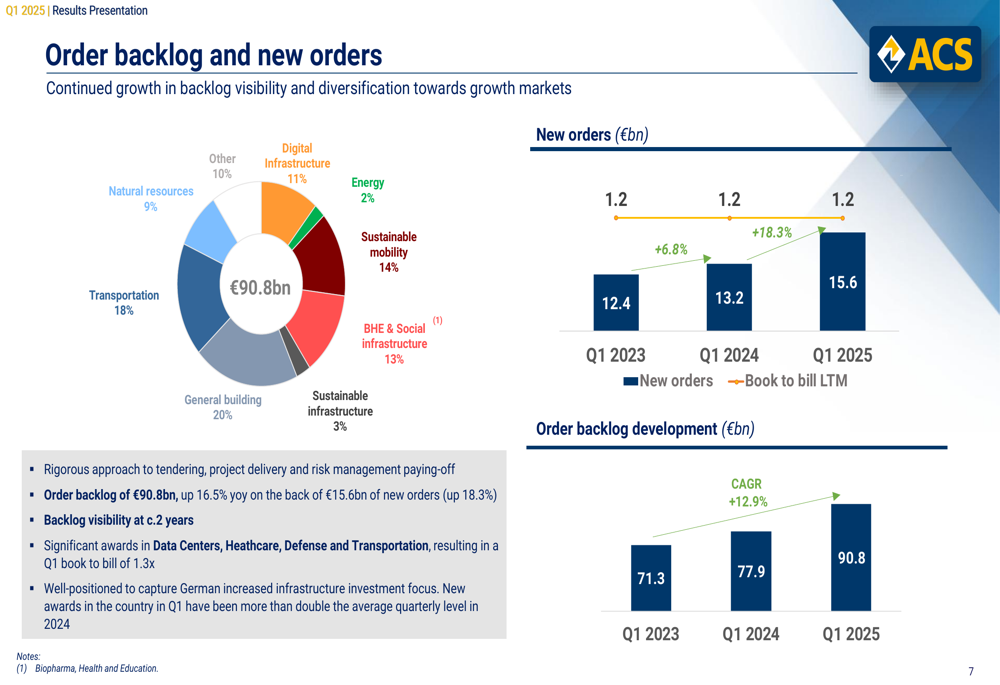

ACS Group continues to build a robust order book, with new orders in Q1 2025 reaching €15.6 billion, up 18.3% year-over-year. This strong order intake has driven the company’s order backlog to a record €90.8 billion, representing approximately two years of work and providing significant visibility for future growth.

The order backlog is well-diversified across sectors, with general building (20%), transportation (18%), sustainable mobility (14%), and social infrastructure (13%) representing the largest segments. This diversification helps mitigate sector-specific risks and positions ACS to capitalize on various growth opportunities.

As shown in the following slide, the company’s order backlog has consistently grown over the past two years:

Forward-Looking Statements

Looking ahead, ACS Group has maintained its full-year 2025 guidance, targeting ordinary net profit growth of up to 17% to reach €746-800 million. This guidance incorporates the strategic acquisition of Dornan and the FlatironDragados merger completed in January 2025.

The company’s capital allocation priorities include significant greenfield infrastructure investment opportunities in data centers and managed lanes, strategic accretive M&A in brownfield core infrastructure, and bolt-on acquisitions to enhance engineering capabilities. ACS also remains committed to shareholder value creation through attractive remuneration and long-term growth while maintaining its investment grade rating of BBB-.

The following slide summarizes ACS’s conclusions and strategic priorities:

In summary, ACS Group delivered a strong start to 2025, with robust growth across most segments and metrics. The company’s strategic focus on high-growth sectors, particularly data centers and infrastructure, combined with its geographic diversification and record order backlog, positions it well for continued growth despite the increased debt from recent acquisitions. Management’s confidence in achieving its full-year targets reflects the solid foundation established in the first quarter and the strong visibility provided by the company’s substantial order backlog.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.