TSMC earnings; Oracle analyst meeting; Gold’s new high - what’s moving markets

Introduction & Market Context

Addiko Bank AG (WBAG:ADKO) presented its first half 2025 results on August 13, 2025, revealing a mixed performance characterized by strong consumer lending growth offset by challenges in its SME segment. The Central and South-Eastern Europe (CSEE) focused bank reported a 6% year-over-year decline in net profit amid a changing interest rate environment following eight ECB rate cuts since June 2024, totaling a reduction of 2.0%.

The bank’s stock closed at €22.7 on the presentation day, down 0.88%, reflecting investor caution regarding the adjusted outlook for 2025 and the announcement that guidance for 2026 is under review.

Quarterly Performance Highlights

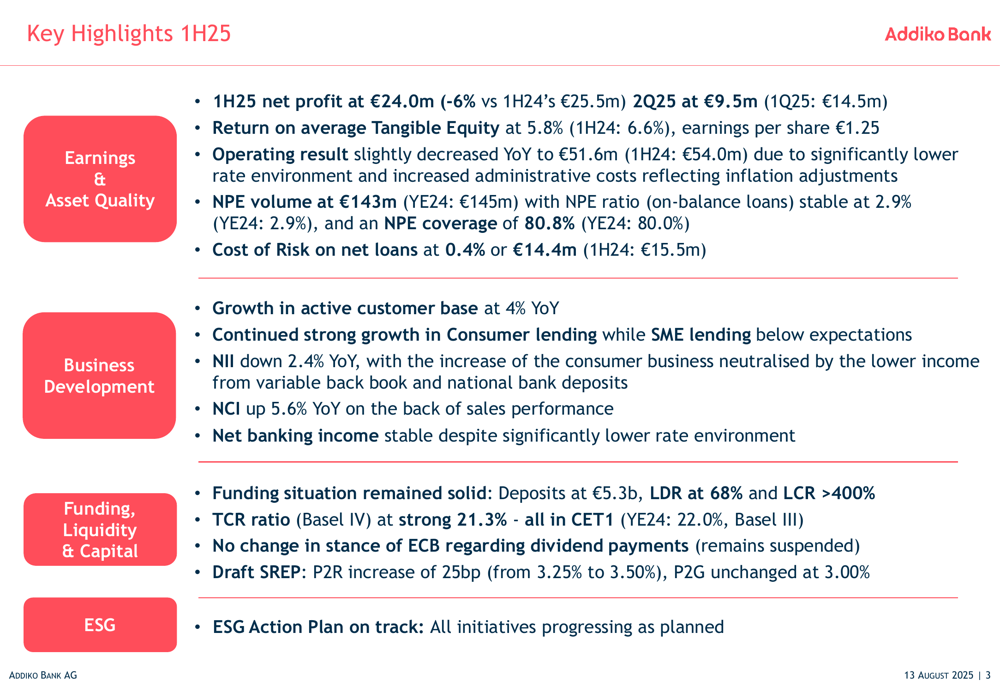

Addiko Bank reported a net profit of €24.0 million for the first half of 2025, down 6% from €25.5 million in the same period last year. The second quarter showed a significant slowdown with profit of €9.5 million, compared to €14.5 million in the first quarter.

As shown in the following key performance indicators, the bank maintained stable asset quality despite profitability challenges:

Return on average Tangible Equity declined to 5.8% from 6.6% in 1H24, while earnings per share reached €1.25. The operating result slightly decreased year-over-year to €51.6 million from €54.0 million, primarily due to the lower interest rate environment and increased administrative costs.

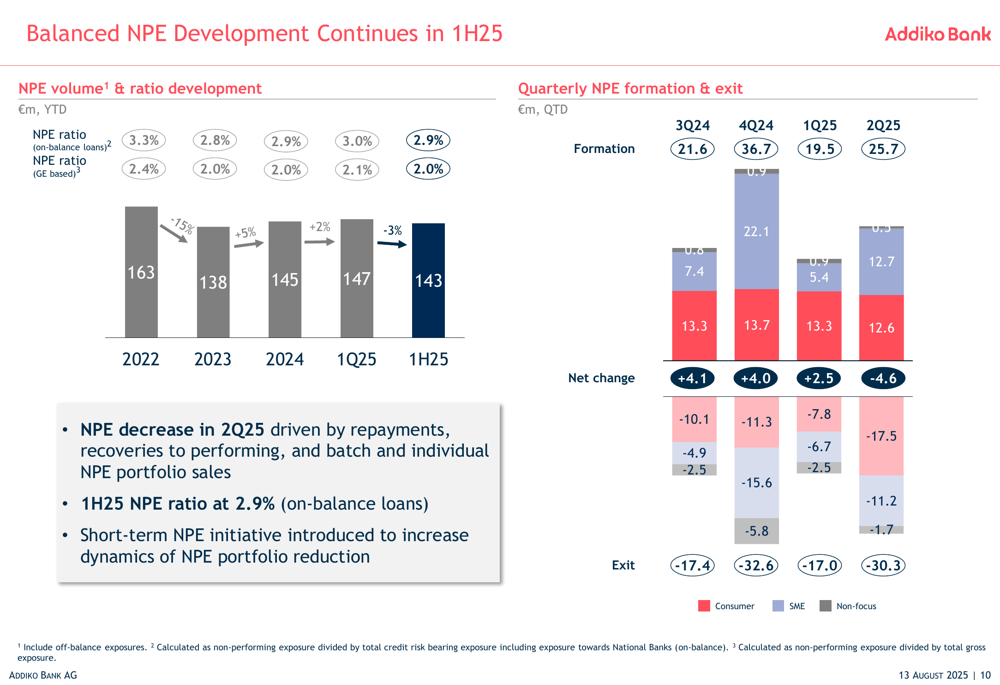

The bank’s asset quality remained stable with the non-performing exposure (NPE) ratio unchanged at 2.9% compared to year-end 2024, while NPE coverage improved slightly to 80.8% from 80.0%.

Detailed Financial Analysis

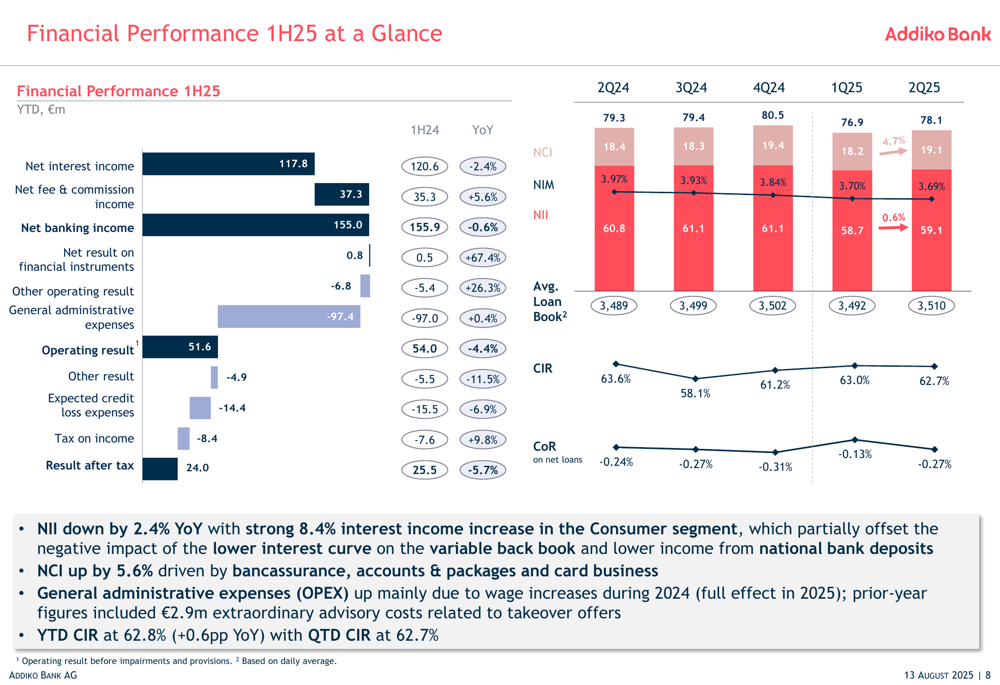

Addiko’s financial performance for the first half of 2025 showed resilience in maintaining stable net banking income despite interest rate headwinds. The bank’s net interest income declined by 2.4% year-over-year, partially offset by a 5.6% increase in net fee and commission income.

The following chart provides a comprehensive view of the bank’s financial performance:

Administrative expenses increased primarily due to wage increases implemented during 2024, putting pressure on the operating result. Cost of risk remained well-managed at 0.4% of net loans, amounting to €14.4 million compared to €15.5 million in 1H24.

Addiko Bank maintained a strong capital position with a Total Capital Ratio (TCR) of 21.3% under Basel IV calculations, as illustrated in this chart:

The bank noted that overall risk-weighted asset (RWA) growth reflects changes in risk-weighting requirements under Basel IV and a new interpretation of an EBA guideline on structural FX published in 2Q25.

Strategic Initiatives

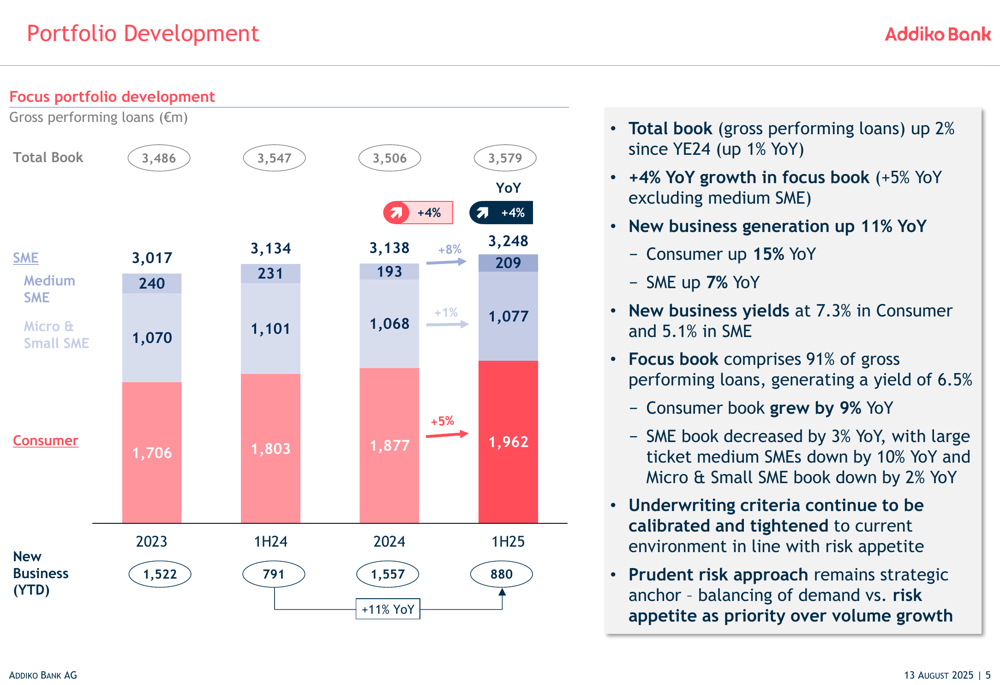

Addiko Bank continues to execute its strategy of focusing on consumer and SME lending in the CSEE region. The loan portfolio development shows strong growth in the consumer segment while SME lending has faced challenges:

The total loan book increased by 2% since year-end 2024 and showed 4% year-over-year growth in the focus book. The bank emphasized that it is calibrating and tightening underwriting criteria while maintaining a prudent risk approach as its strategic anchor.

In the consumer segment, Addiko delivered solid new business growth of 15% year-over-year with premium pricing at 7.3%. The bank has made significant progress in digital transformation, launching fully digital end-to-end lending processes in Slovenia, Croatia, Romania, and a "Postman" digital lending process in Bosnia and Herzegovina.

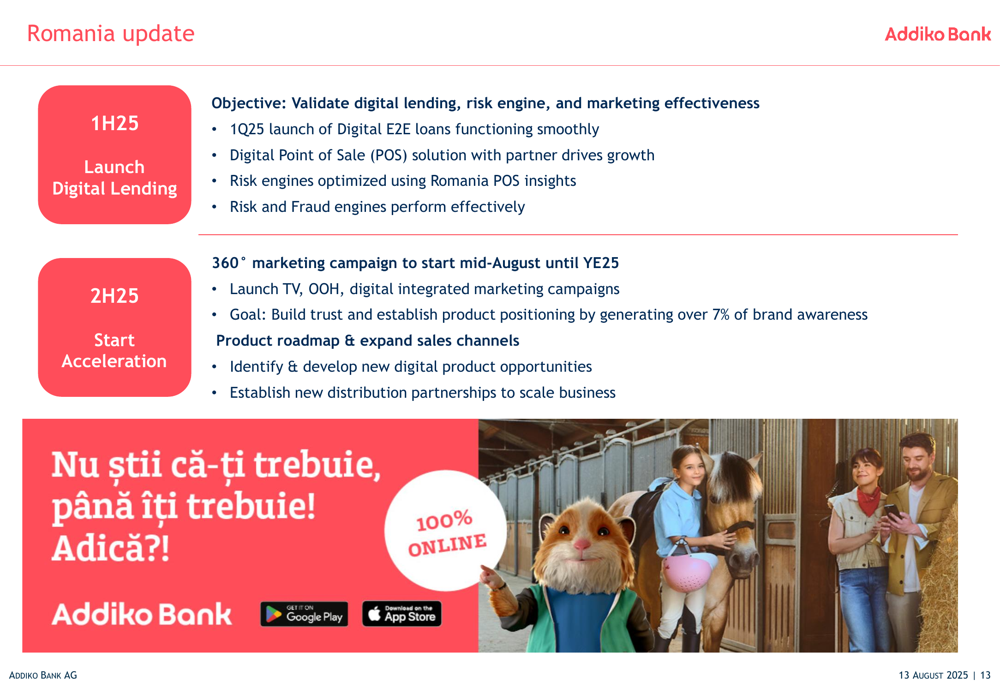

The bank’s expansion in Romania is progressing with the launch of digital lending in the first half of 2025, as outlined in this strategic update:

For the second half of 2025, Addiko plans to accelerate its Romanian operations with a 360° marketing campaign starting mid-August and running until year-end, along with expanding its product roadmap and sales channels.

Forward-Looking Statements

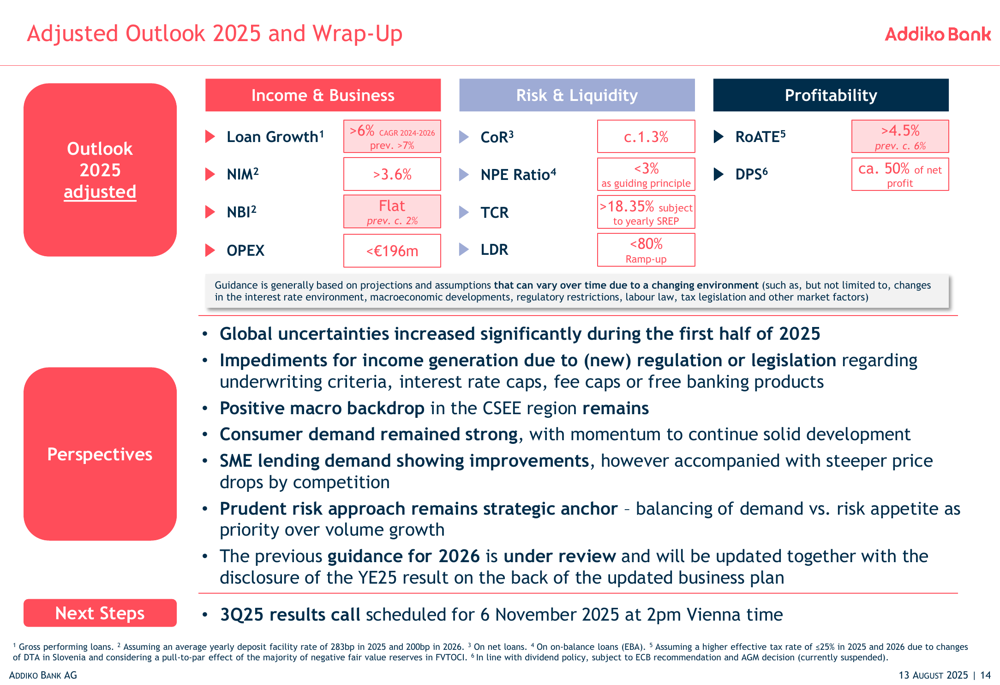

Addiko Bank has adjusted its outlook for 2025 and announced that guidance for 2026 is under review. The bank cited global uncertainties, impediments for income generation, but also noted a positive macro backdrop in CSEE and strong consumer demand.

The following slide details the adjusted outlook:

Key targets include loan growth exceeding 6% CAGR for 2024-2026, maintaining a net interest margin above 3.6%, flat net banking income, and operating expenses below €196 million. On the risk and liquidity front, the bank aims to keep cost of risk around 1.3%, NPE ratio below 3%, and total capital ratio above 18.35%.

For profitability, Addiko targets a return on average tangible equity above 4.5% and a dividend payout of approximately 50% of net profit. However, the bank noted that its previous guidance for 2026 is under review and will be updated with the disclosure of the year-end 2025 results based on an updated business plan.

The bank’s balanced approach to non-performing exposure management continues, as illustrated in the following chart:

NPE volume decreased in the second quarter of 2025, and the bank has introduced a short-term NPE initiative to further improve asset quality.

In conclusion, Addiko Bank’s first half 2025 results demonstrate resilience in its consumer business amid challenges in the SME segment. While the bank has maintained stable net banking income and strong capital position, the adjusted outlook for 2025 and review of 2026 guidance suggest caution regarding future performance. Investors will be watching closely for signs of improvement in the SME business and the success of digital initiatives in driving growth.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.