Wall St futures flat amid US-China trade jitters; bank earnings in focus

Introduction & Market Context

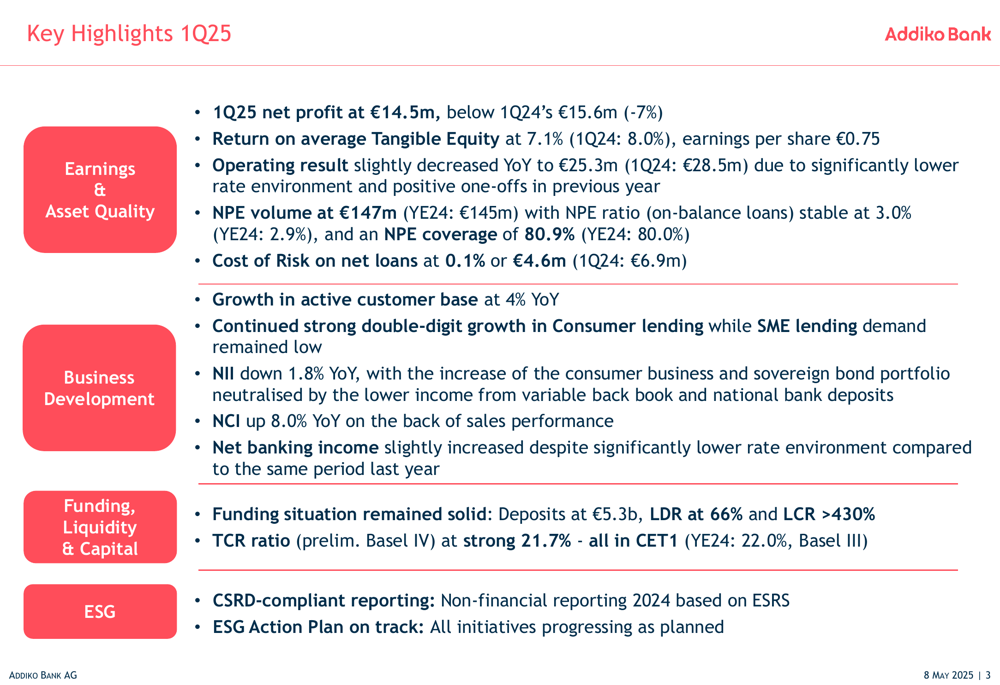

Addiko Bank AG (WBAG:VIE:ADKO) presented its first quarter 2025 results on May 8, 2025, revealing a mixed performance with declining profitability despite continued strength in consumer lending. The Central and South-Eastern Europe (CSEE) focused specialist bank reported a net profit of €14.5 million, down 7% from €15.6 million in the same period last year.

The bank’s stock closed at €20.10 on May 7, 2025, trading well above its 52-week low of €15.60 but below its 52-week high of €21.60. This positions Addiko within a relatively stable trading range despite the quarterly profit decline.

As shown in the following key highlights from the presentation, Addiko maintained stable asset quality while experiencing mixed results across business segments:

Quarterly Performance Highlights

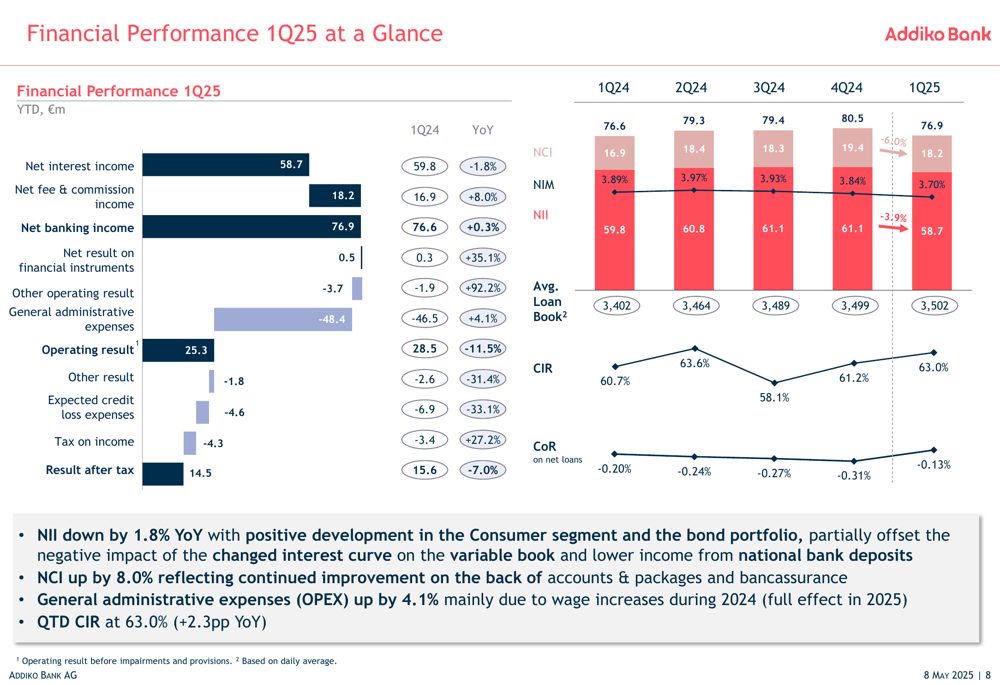

Addiko Bank reported a Return on Average Tangible Equity (ROATE) of 7.1% for Q1 2025, down from 8.0% in Q1 2024. The bank’s net interest income (NII) decreased by 1.8% year-over-year, while net fee and commission income (NCI) increased by 8.0%, demonstrating strength in the fee-generating business lines.

The bank’s funding situation remained solid with deposits at €5.3 billion and a loan-to-deposit ratio (LDR) of 66%. The Total (EPA:TTEF) Capital Ratio (TCR) stood at a robust 21.7%, indicating a strong capital position despite challenging market conditions.

The following slide provides a comprehensive overview of Addiko’s financial performance for the quarter:

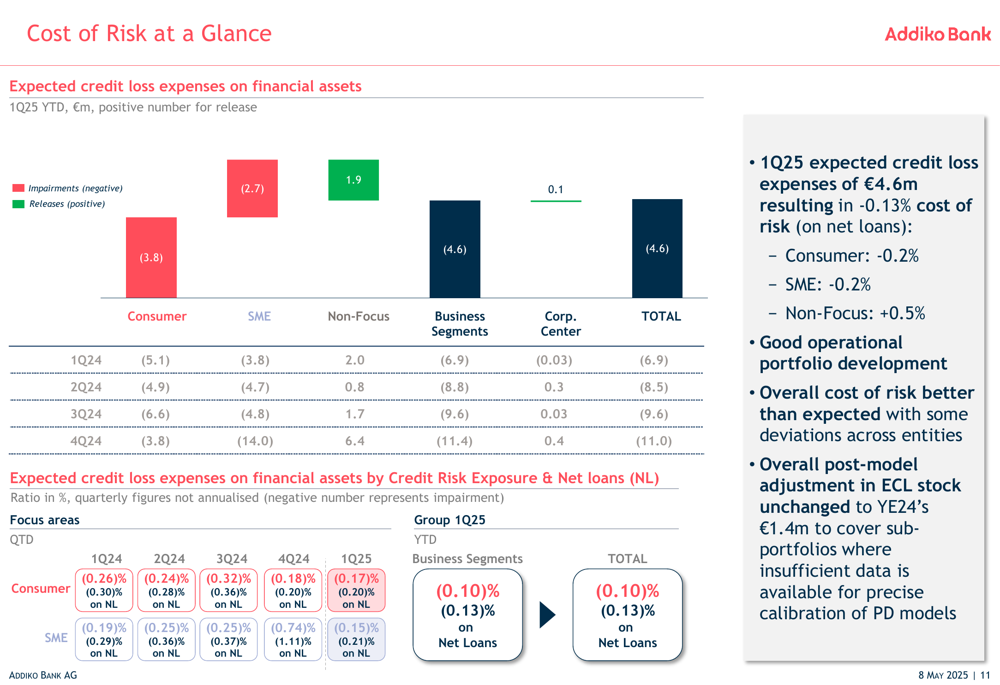

Asset quality remained stable with the non-performing exposure (NPE) ratio at 3.0% and NPE volume at €147 million. The cost of risk was positive at -0.13% (on net loans), indicating a net release of provisions during the quarter.

The cost of risk breakdown by segment shows varying performance across the portfolio:

Strategic Initiatives

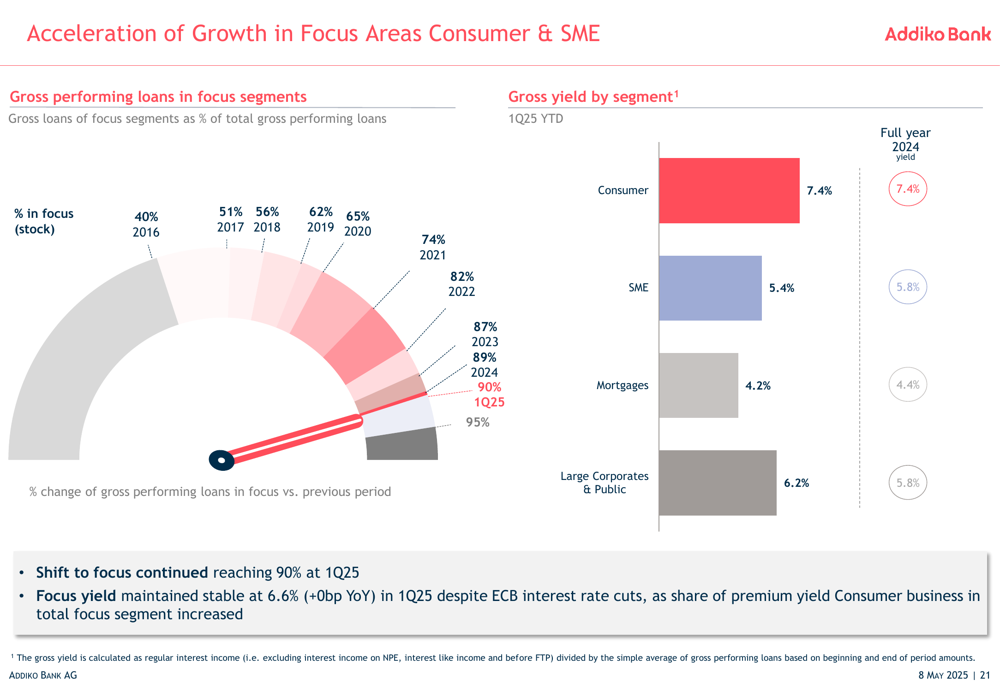

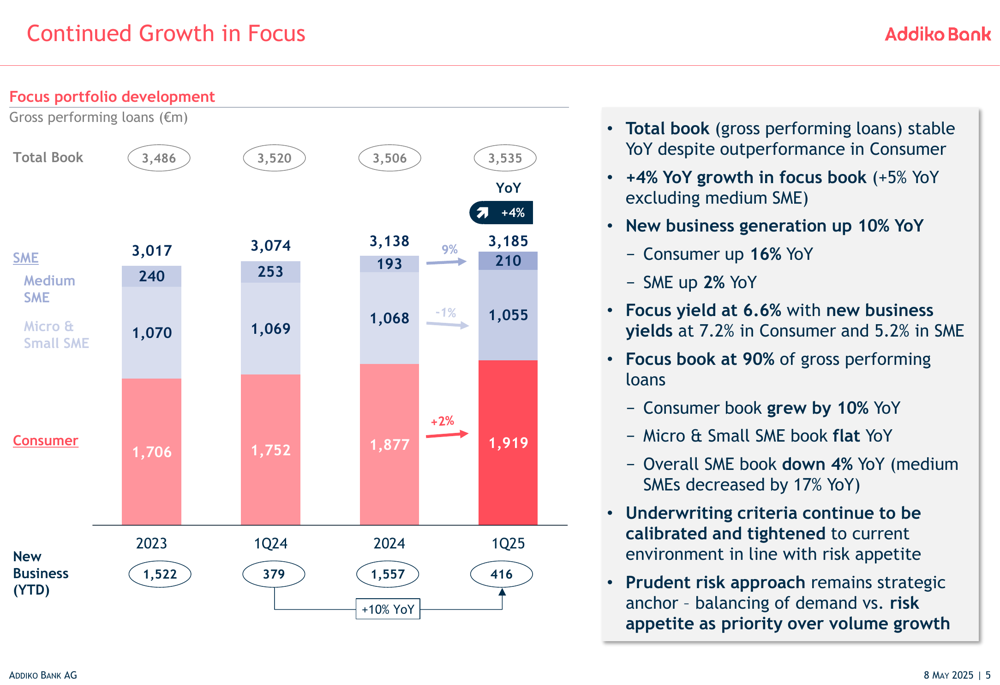

Addiko Bank continues to execute its strategy of focusing on consumer and SME lending while reducing non-focus areas. The bank reported that 90% of its gross performing loans are now in focus areas, up from 40% in 2016, demonstrating the successful transformation of its portfolio.

The following chart illustrates this strategic shift toward focus areas:

Consumer lending showed particularly strong performance with gross performing loans up 10% year-over-year and new business generation up 16% YoY with premium pricing at 7.2%. However, the SME segment experienced weakness with new business slowdown due to weaker market demand.

The bank’s focus portfolio development shows continued growth in consumer lending while maintaining stable overall book size:

Digital transformation remains a key strategic priority for Addiko. The bank successfully launched a "Fully E2E Digital Online Consumer Loan" in Romania at the end of Q1 2025. Mobile banking users increased by 8% year-over-year to 322,000, while total digital users grew by 7% to 329,000, highlighting the bank’s progress in digital adoption.

Detailed Financial Analysis

Addiko’s operating result decreased by 11.5% year-over-year to €25.3 million, reflecting the challenging market environment. General administrative expenses increased by 4.1%, contributing to a cost-income ratio of 63.0% for the quarter.

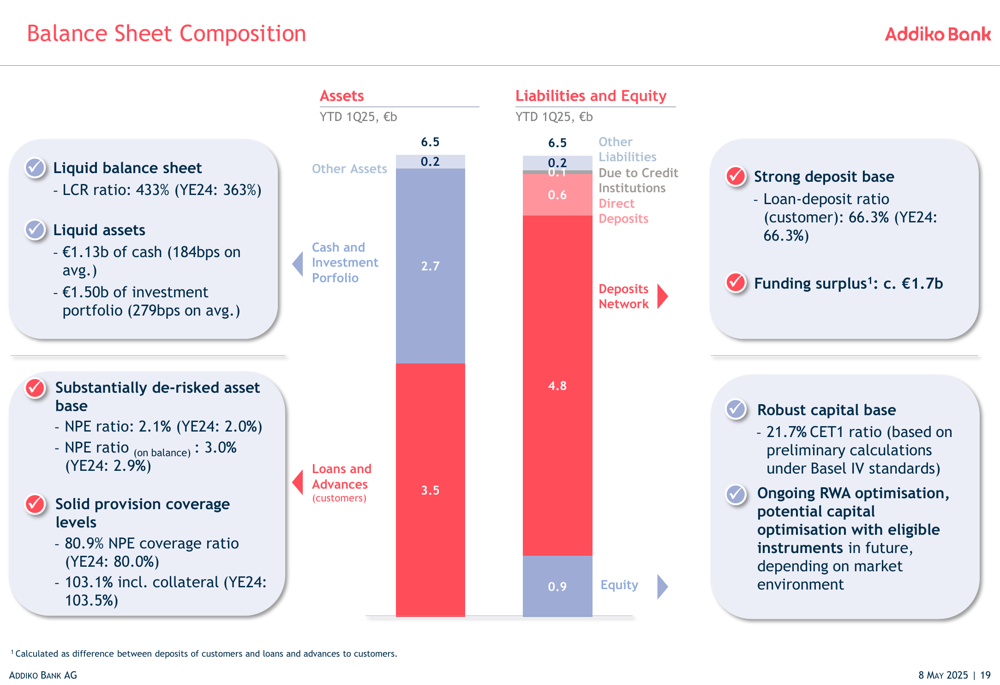

The bank’s balance sheet composition shows a solid liquidity position with €1.13 billion in cash and €1.50 billion in investment portfolio. The loan-to-deposit ratio stands at 66.3%, indicating a conservative funding approach:

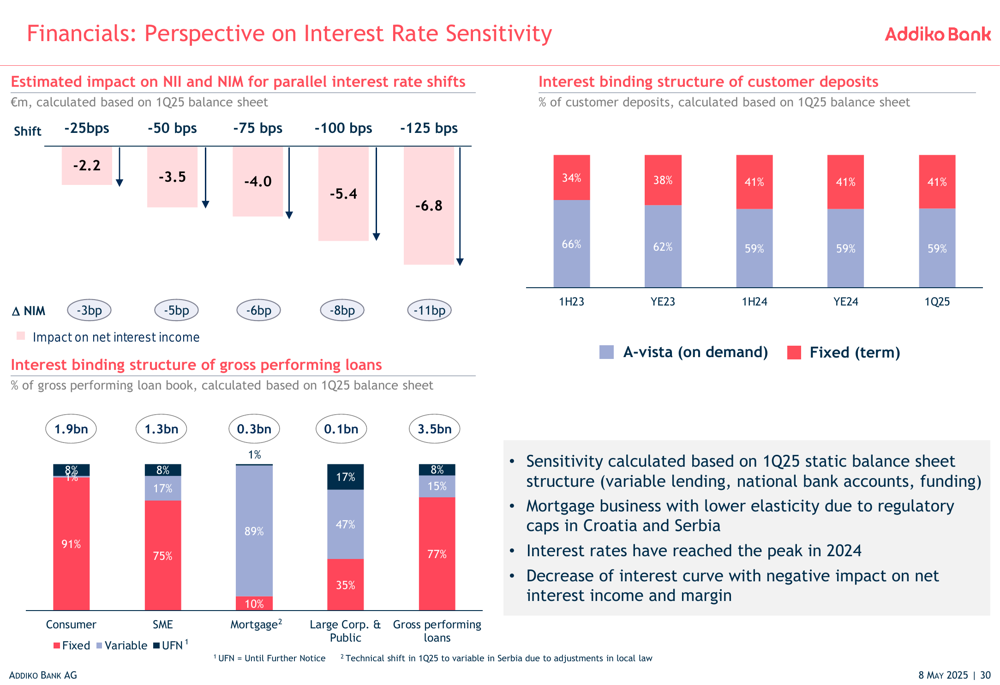

Interest rate sensitivity analysis suggests that Addiko is well-positioned to benefit from potential rate changes, with a detailed breakdown of how different rate scenarios would impact the bank’s income:

Forward-Looking Statements

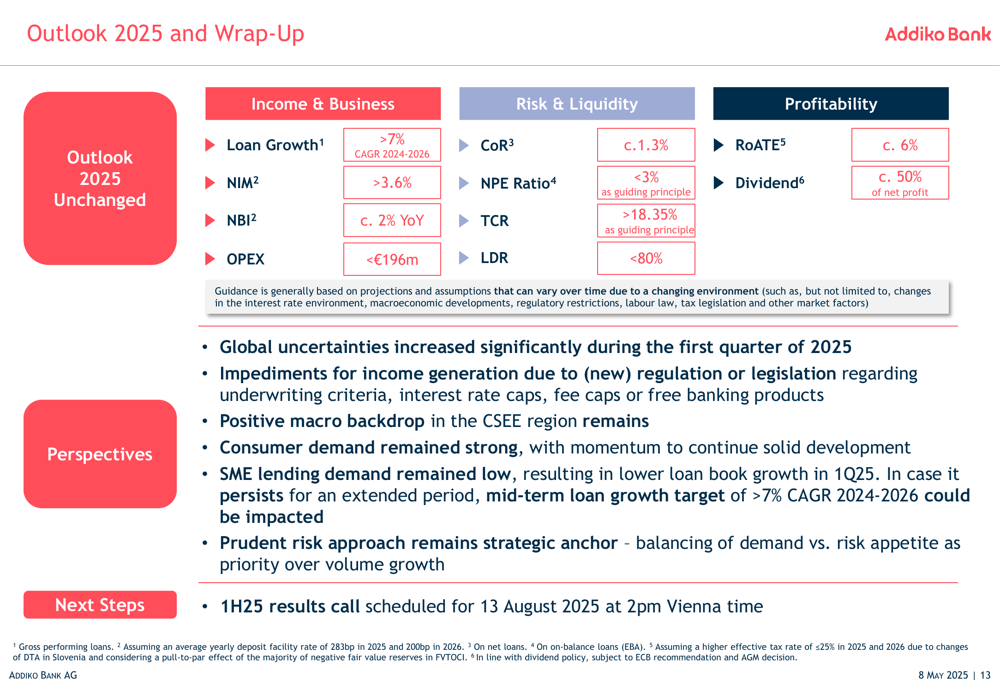

Despite the challenging start to 2025, Addiko Bank maintained its positive outlook for the full year and beyond. The bank projects loan growth of more than 7% CAGR from 2024 to 2026, a net interest margin above 3.6%, and an NPE ratio below 3%.

The bank expects cost of risk to be around 1.3% and plans to distribute approximately 50% of net profit as dividends, although it noted that no dividend will be paid for 2024 due to a recommendation from the European Central Bank.

The following slide outlines Addiko’s outlook for 2025 and beyond:

Addiko’s management highlighted that while global uncertainties persist, the CSEE region continues to provide a positive macroeconomic backdrop for the bank’s operations. The bank remains committed to its prudent risk approach as a strategic anchor while pursuing growth opportunities, particularly in consumer lending and digital transformation.

The bank announced that its half-year 2025 results call is scheduled for August 13, 2025, at 2:00 PM Vienna time, where investors and analysts will receive further updates on the bank’s performance and strategic initiatives.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.