Wall St futures flat amid US-China trade jitters; bank earnings in focus

Ag Growth International Inc (TSX:AFN) reported mixed first-quarter results on May 6, 2025, with strong performance in its Commercial segment counterbalancing significant challenges in its Farm business. Despite the overall revenue and EBITDA decline, the company maintained its full-year guidance, highlighting the resilience of its diversified business model.

Quarterly Performance Highlights

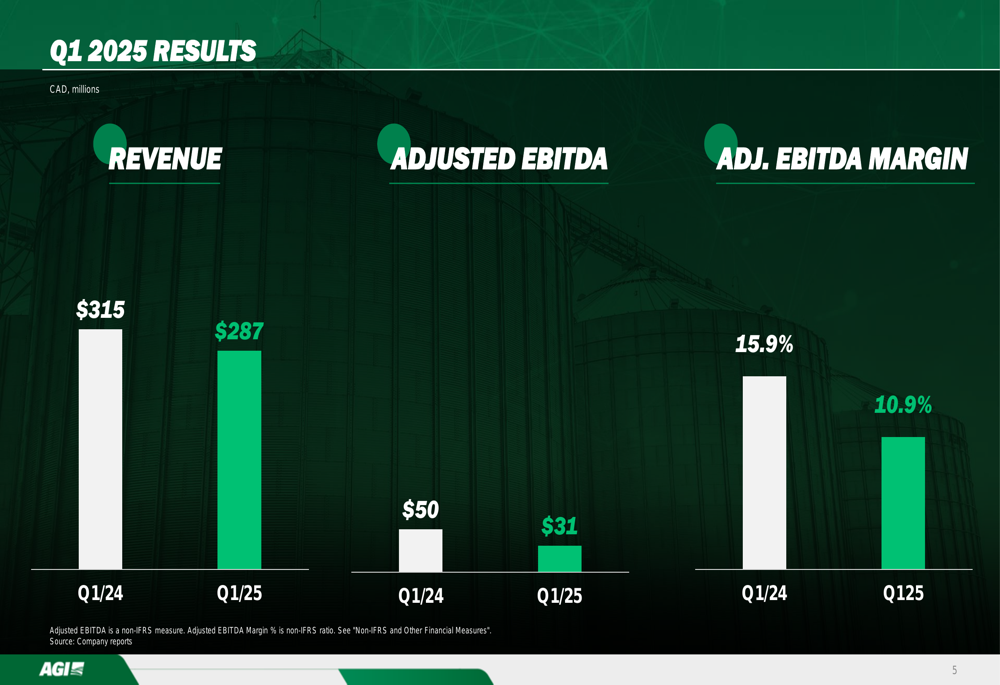

Ag Growth reported Q1 2025 revenue of $287 million, down from $315 million in the same period last year. Adjusted EBITDA fell to $31 million from $50 million, with margins contracting to 10.9% from 15.9% in Q1 2024.

The company’s overall performance was impacted by a challenging North American farm equipment market, though management emphasized that international commercial growth is providing crucial diversification benefits.

As shown in the following financial results chart:

"Commercial segment strength offset anticipated Farm segment market challenges," noted Paul Householder, President and CEO, adding that "International Commercial continues to meaningfully accelerate."

Segment Analysis: Commercial vs. Farm

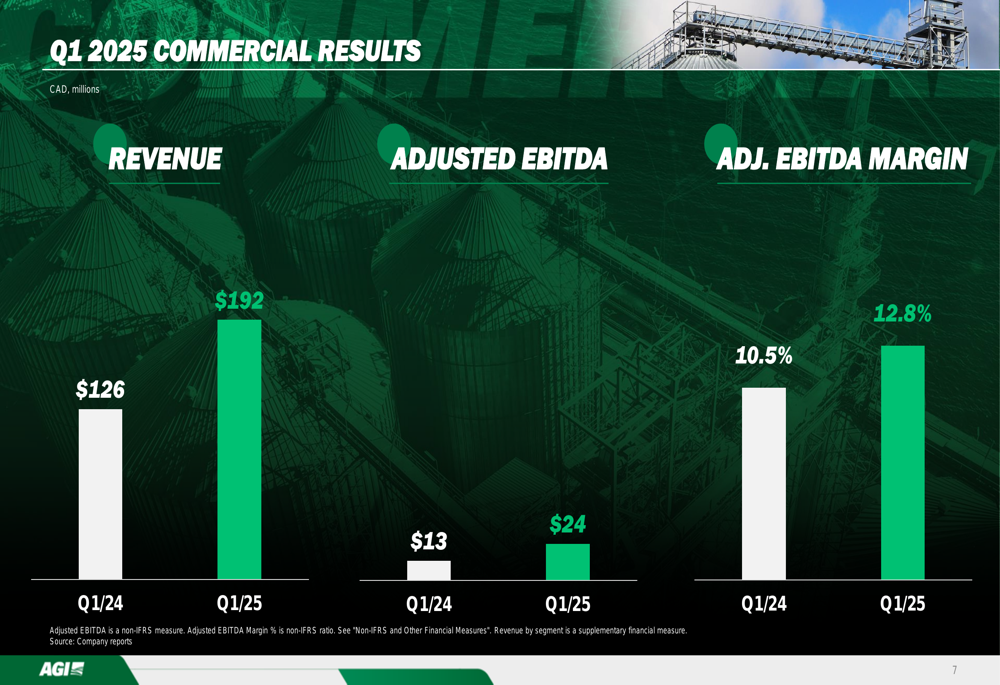

The divergence between Ag Growth’s two main segments was stark in Q1 2025. The Commercial segment, which includes larger infrastructure projects, posted revenue of $192 million, up significantly from $126 million in Q1 2024. Adjusted EBITDA for this segment nearly doubled to $24 million from $13 million, with margins expanding to 12.8% from 10.5%.

The following chart illustrates the Commercial segment’s strong performance:

Management attributed the Commercial segment’s success to "increased capabilities leading to several large turn-key projects in International Commercial" and noted that the expanding margins were "in part due to large turn-key projects."

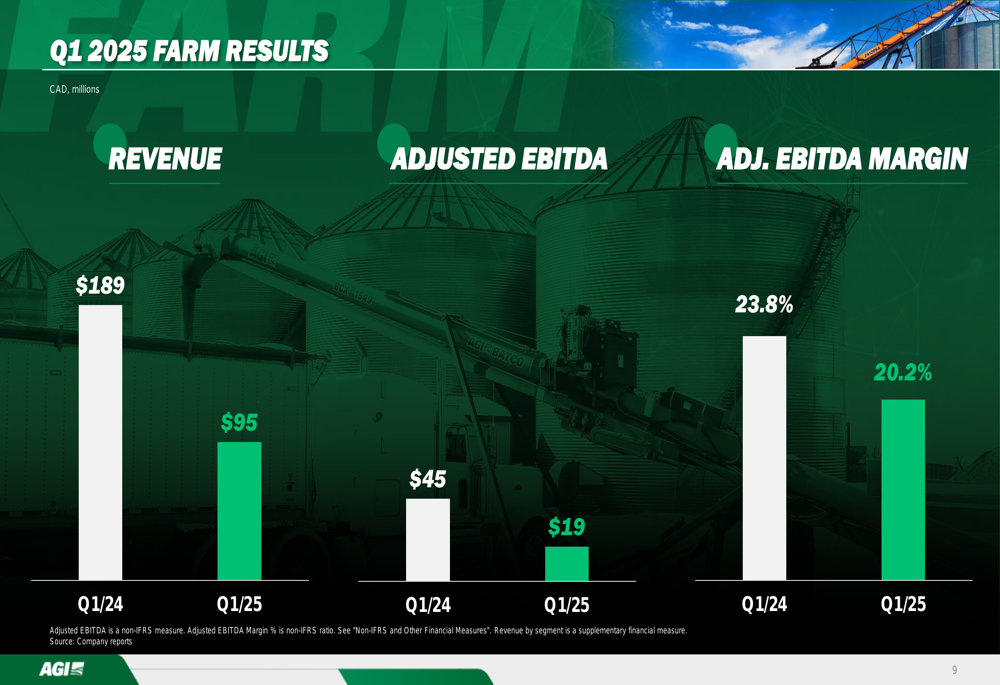

In contrast, the Farm segment faced substantial headwinds. Revenue fell sharply to $95 million from $189 million in Q1 2024, while Adjusted EBITDA dropped to $19 million from $45 million. Despite the revenue decline, the segment maintained relatively strong margins at 20.2%, though down from 23.8% in the prior year.

The Farm segment’s performance is illustrated in this chart:

Householder explained that "challenging conditions in North American Farm persist" and are "expected to last through at least the first half of 2025 with limited visibility to the second half of 2025." He added that "progressing through the growing season towards harvest is a potential catalyst to stir demand."

The company also noted that "tariffs and trade regulations add complexity and uncertainty to the path towards a Farm market recovery."

Order Book and Outlook

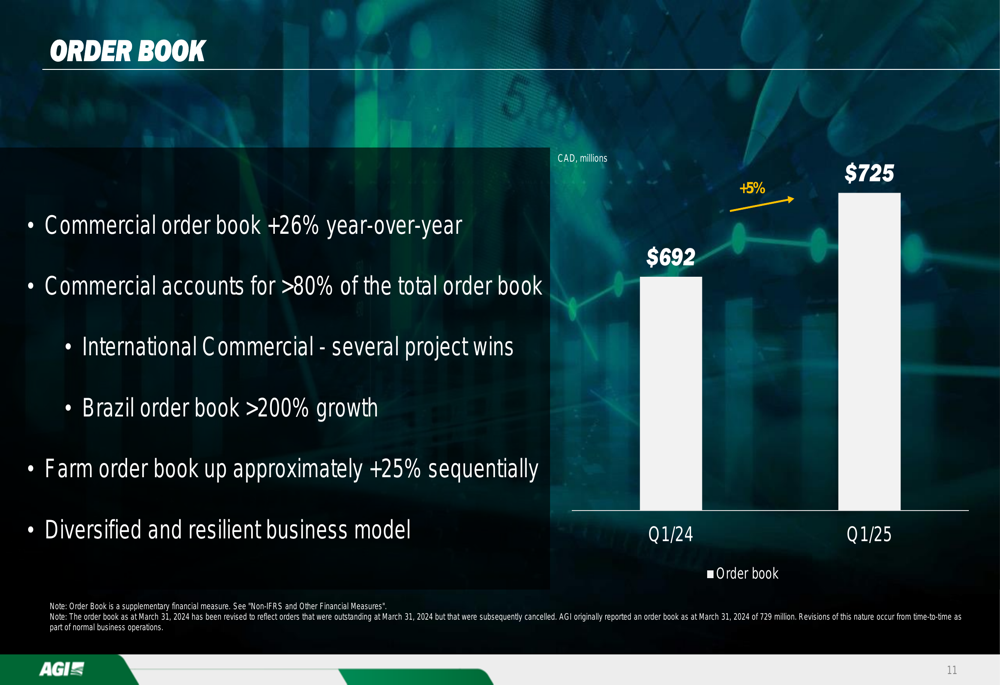

Despite the challenges, Ag Growth reported a growing order book of $725 million, up 5% from $692 million in Q1 2024. The Commercial segment order book increased 26% year-over-year and now accounts for over 80% of the total order book.

Particularly impressive was the growth in Brazil, where the order book expanded by more than 200%. The Farm segment order book showed signs of recovery with approximately 25% sequential growth.

The following chart shows the overall order book trend:

Based on these trends, Ag Growth reiterated its full-year 2025 Adjusted EBITDA guidance of at least $225 million and provided second-quarter 2025 Adjusted EBITDA guidance in the range of $50-$55 million.

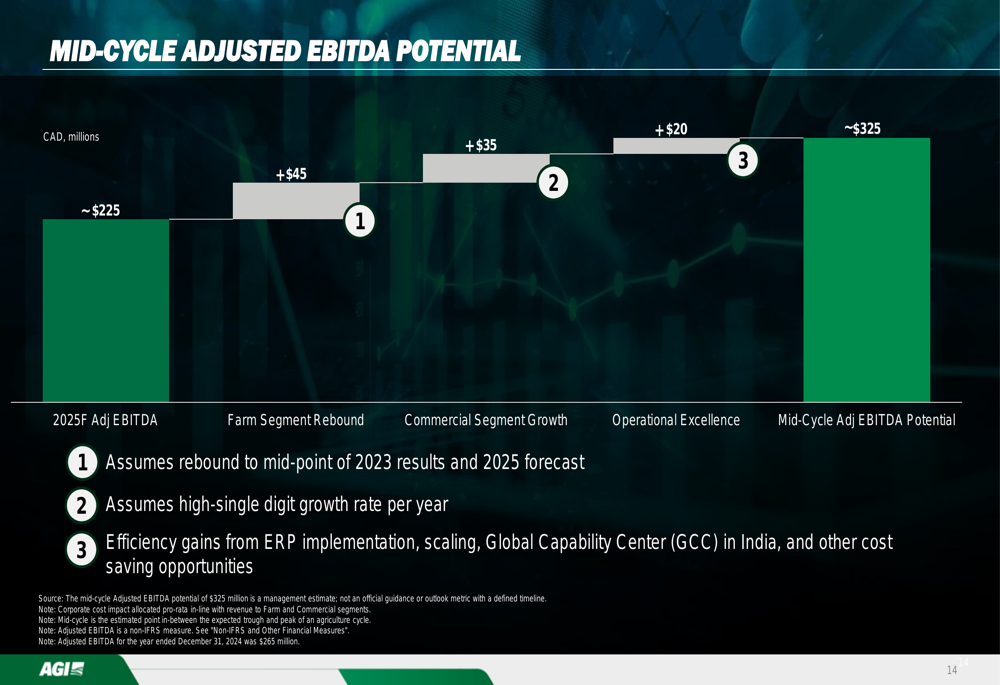

Looking further ahead, the company outlined its mid-cycle Adjusted EBITDA potential of approximately $325 million, based on a rebound to the mid-point of 2023 results and 2025 forecast (+$45 million), high-single digit growth rate per year (+$35 million), and efficiency gains from ERP implementation, scaling, and other cost-saving opportunities (+$20 million).

This growth potential is illustrated in the following chart:

Balance Sheet and Capital Allocation Strategy

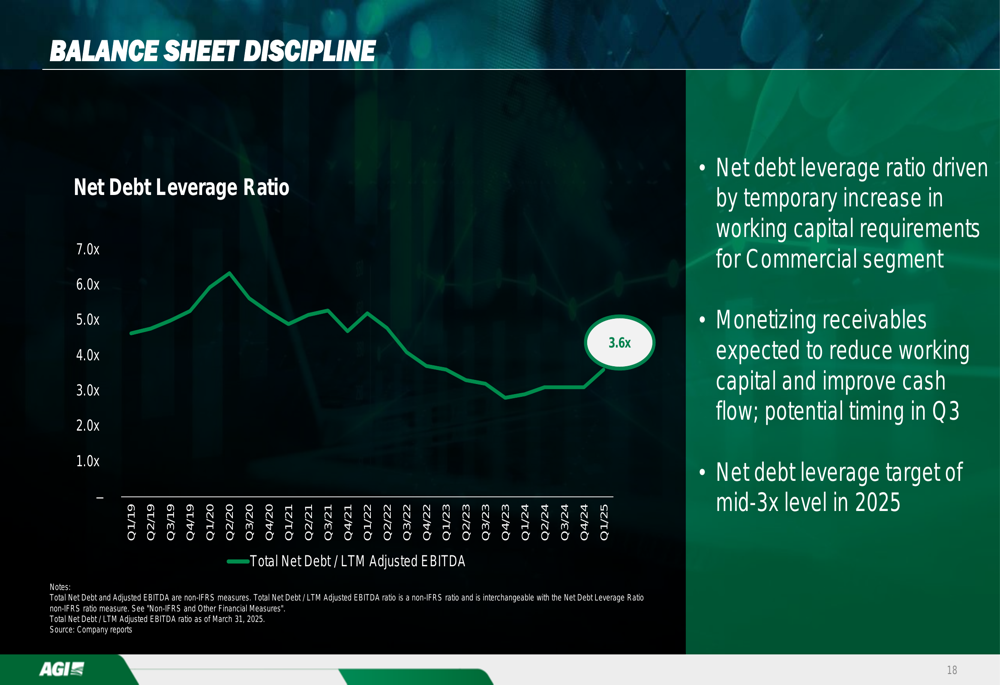

CFO Jim Rudyk addressed the company’s financial position, noting a temporary increase in the net debt leverage ratio due to working capital requirements for the Commercial segment. The company expects to monetize receivables to reduce working capital and improve cash flow, with potential timing in Q3, targeting a mid-3x net debt leverage level in 2025.

The following chart shows the net debt leverage ratio trend:

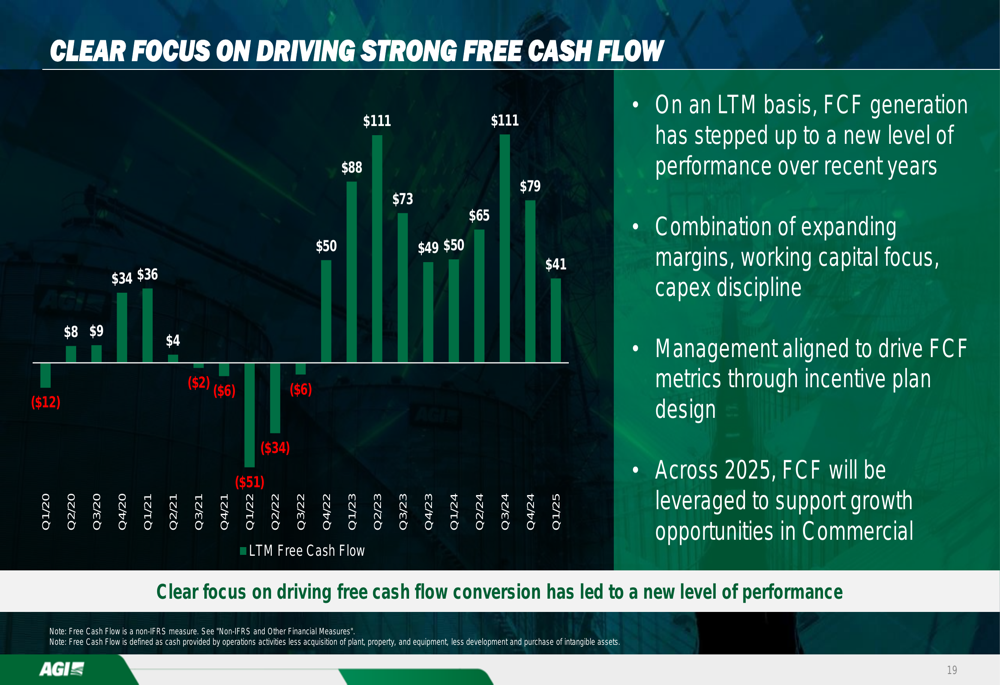

Rudyk highlighted the company’s improved free cash flow generation, stating that "on an LTM basis, FCF generation has stepped up to a new level of performance over recent years" due to "a combination of expanding margins, working capital focus, and capex discipline."

The free cash flow improvement is illustrated here:

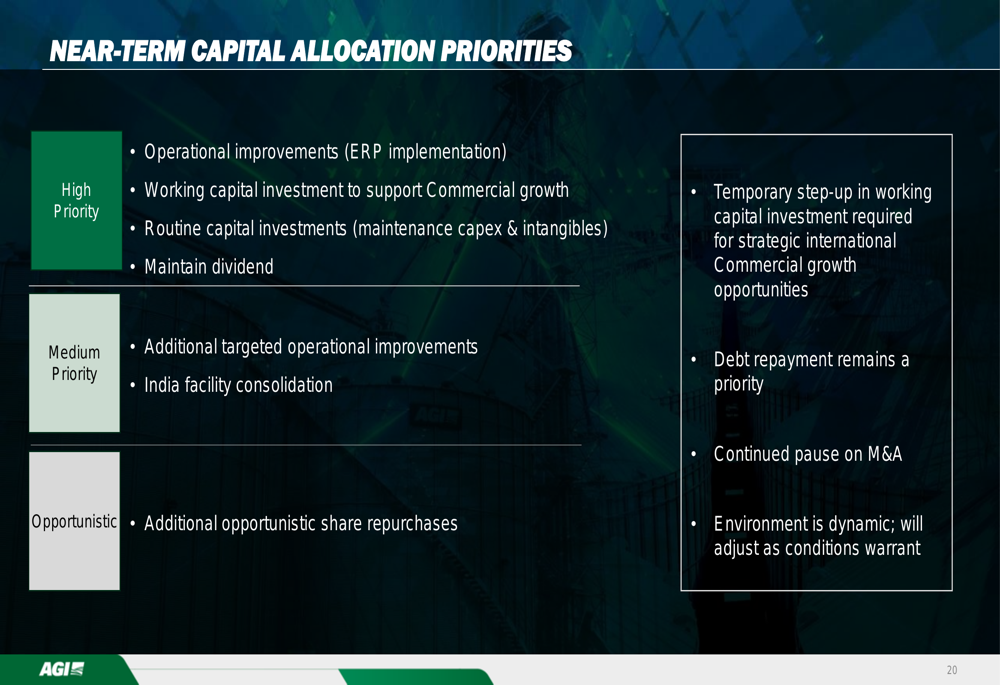

Regarding capital allocation, Ag Growth outlined its priorities, with high-priority items including operational improvements (ERP implementation), working capital investment to support Commercial growth, routine capital investments, maintaining the dividend, and temporary working capital investment for strategic international Commercial growth opportunities.

The company’s detailed capital allocation strategy is shown below:

Ag Growth International’s stock closed at $33.79 on May 5, 2025, down 3.4% ahead of the earnings release, and has traded between $30.81 and $58.14 over the past 52 weeks.

The company’s ability to maintain its full-year guidance despite Farm segment challenges reflects confidence in its diversified business model and international growth strategy, particularly as it continues to expand its Commercial segment presence in high-growth markets like Brazil.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.