Paul Tudor Jones sees potential market rally after late October

Introduction & Market Context

Ag Growth International Inc (TSX:AFN) presented its Q2 2025 earnings results on August 1, 2025, revealing a tale of two segments as the company navigates divergent market conditions. The agricultural equipment and systems provider reported relatively stable overall revenue despite significant headwinds in its Farm segment, with its Commercial business providing crucial offsetting strength.

The company’s stock has faced pressure in recent months, trading at $41.84 as of July 31, 2025, well below its 52-week high of $57.10 but recovering from its low of $30.81. This quarterly presentation comes at a critical time as AGI works to demonstrate its resilience amid challenging North American farm conditions.

Quarterly Performance Highlights

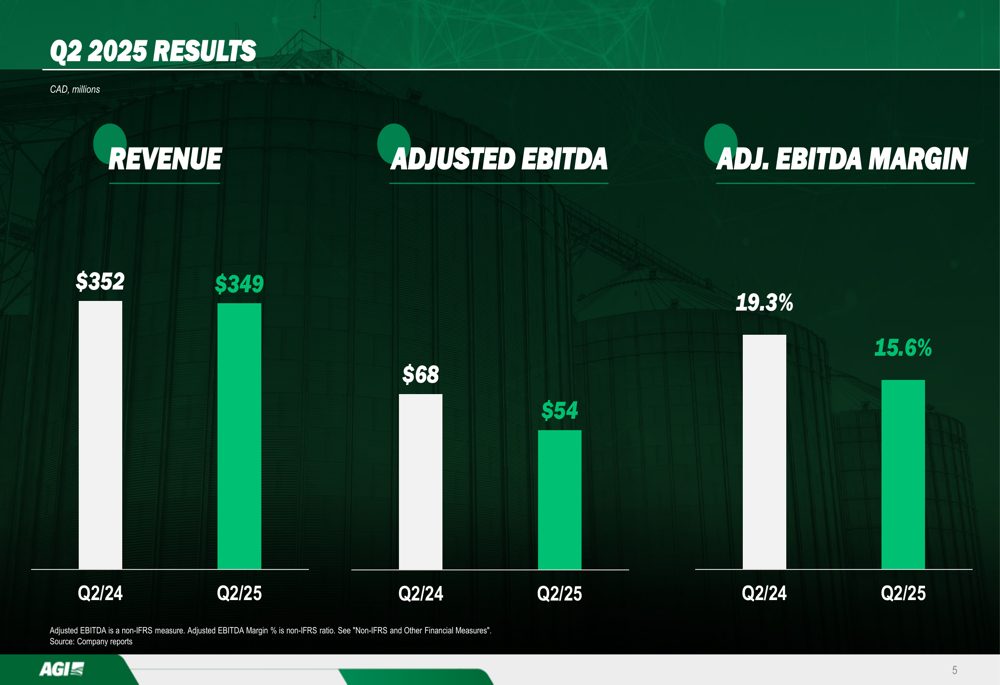

AGI reported Q2 2025 revenue of $349 million, representing a slight decrease of 0.9% compared to $352 million in Q2 2024. However, profitability metrics showed more significant pressure, with adjusted EBITDA falling 20.6% to $54 million from $68 million in the prior year. Consequently, the adjusted EBITDA margin contracted to 15.6% from 19.3% a year earlier.

As shown in the following chart of AGI’s quarterly financial performance:

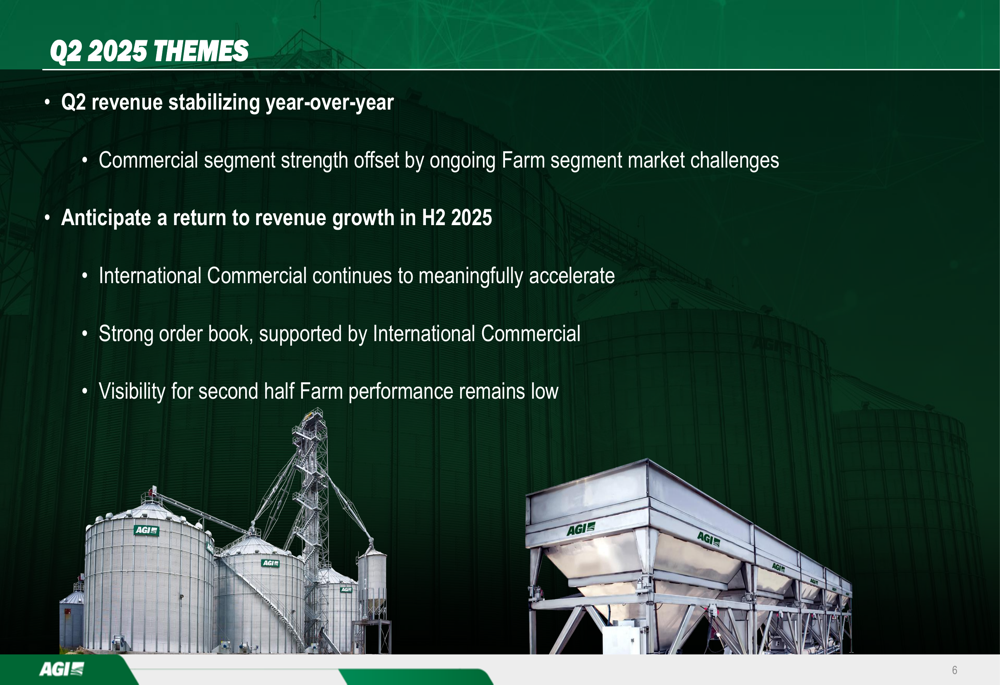

The company highlighted several key themes for the quarter, including stabilizing revenue year-over-year, anticipated return to revenue growth in the second half of 2025, and meaningful acceleration in International Commercial business. However, management acknowledged that visibility for second-half Farm performance remains low due to ongoing market challenges.

Segment Analysis: Commercial vs Farm

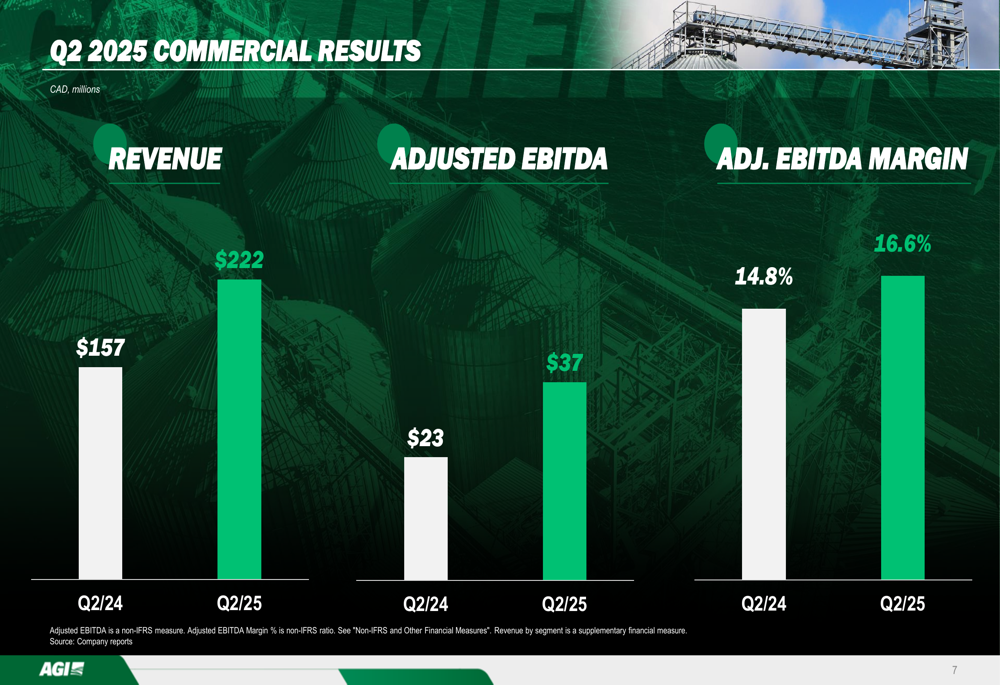

The stark contrast between AGI’s two primary segments was perhaps the most notable aspect of the Q2 results. The Commercial segment delivered impressive growth, with revenue increasing 41.4% to $222 million compared to $157 million in Q2 2024. This segment’s adjusted EBITDA surged 60.9% to $37 million, with margins expanding to 16.6% from 14.8% in the prior year.

The following chart illustrates the Commercial segment’s strong performance:

Management attributed the Commercial segment’s success to increased capabilities leading to large-scale international projects, expanding margins due to comprehensive project work, and a strong order book in both international regions and North America. The company noted that its "differentiated strategy is delivering favorable financial results" in this segment.

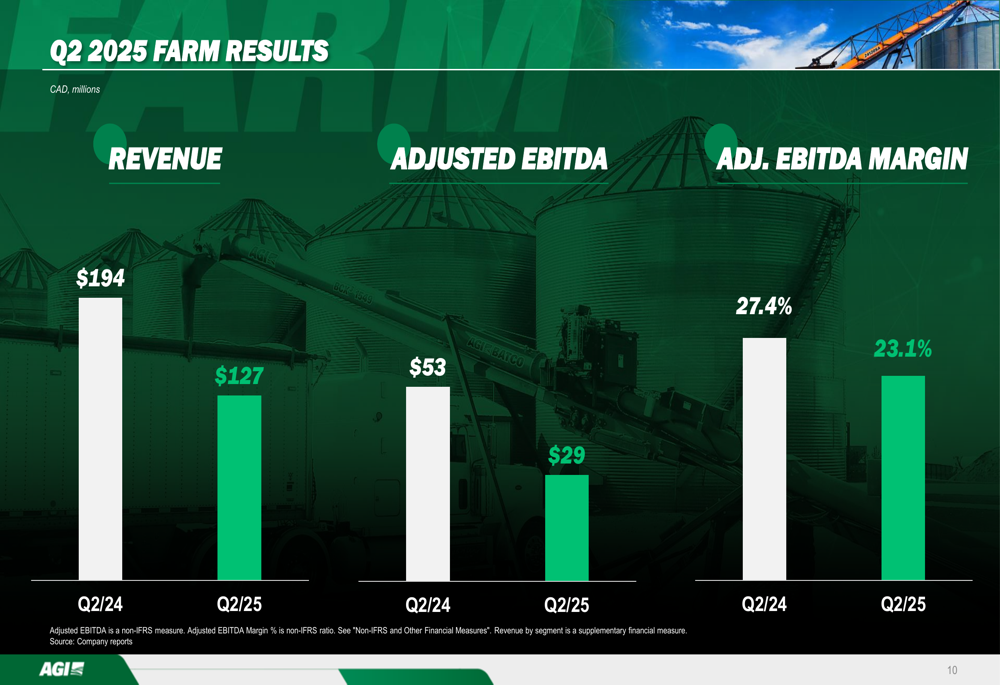

In stark contrast, the Farm segment continued to face significant headwinds. Revenue declined 34.5% to $127 million from $194 million in Q2 2024, while adjusted EBITDA fell 45.3% to $29 million. Despite the revenue decline, the Farm segment maintained relatively strong margins at 23.1%, though this represented a decrease from 27.4% in the prior year.

The following chart details the Farm segment’s challenging quarter:

Management cited persistent challenging conditions in the North American Farm market, with limited visibility into the second half of 2025. The company is focusing on cost optimization while noting that "tariffs and trade regulations add complexity and uncertainty to a Farm market recovery." A successful harvest season could potentially serve as a catalyst to prompt demand.

International Growth Focus

AGI’s international expansion, particularly in Brazil, emerged as a bright spot in the quarterly results. The company highlighted significant growth opportunities in the Brazilian market, including value-added processing capacity investments, grain handling and movement needs, and on-farm storage capacity deficits.

The company’s order book grew 4% year-over-year to $660 million, with the Commercial segment showing particularly strong momentum with 15% growth. Notably, Commercial now accounts for over 85% of AGI’s total order book, with Brazil serving as the primary driver in International Commercial business.

The following chart illustrates AGI’s growing order book:

Management revealed that subsequent to the quarter, the company secured "several notable order commitments" across various geographies with an aggregate value exceeding $100 million, demonstrating continued momentum in international markets despite broader agricultural market challenges.

Balance Sheet and Cash Flow Management

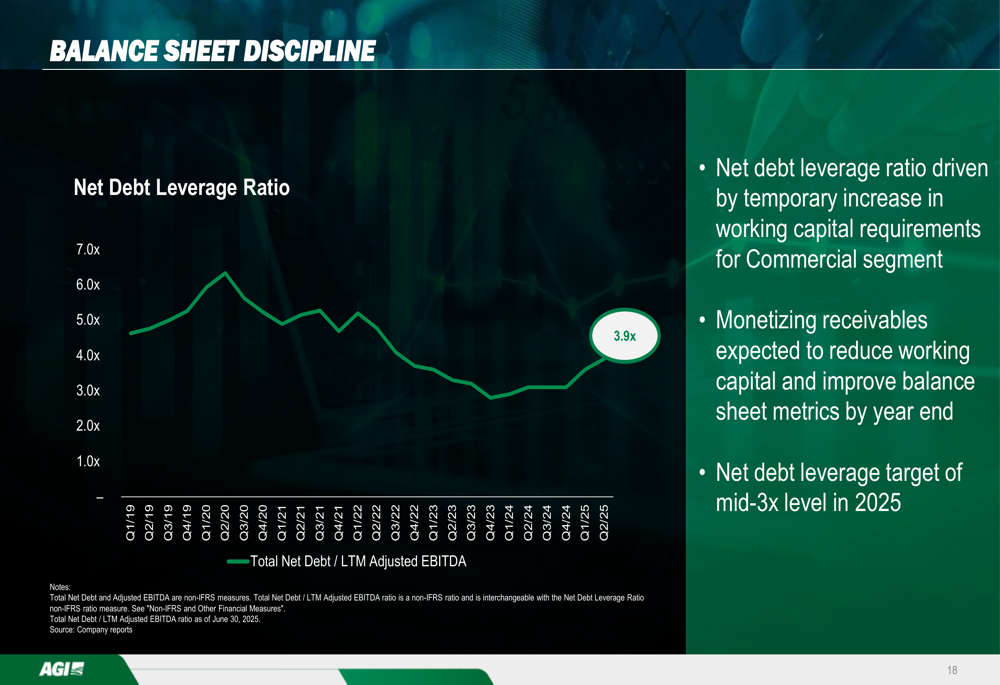

AGI’s financial position showed some pressure, with the Net Debt Leverage Ratio at 3.9x as of Q2 2025. Management attributed this to a temporary increase in working capital requirements for the Commercial segment and expects to reduce working capital and improve balance sheet metrics by year-end through monetizing receivables. The company is targeting a mid-3x leverage level by the end of 2025.

The following chart shows the evolution of AGI’s Net Debt Leverage Ratio:

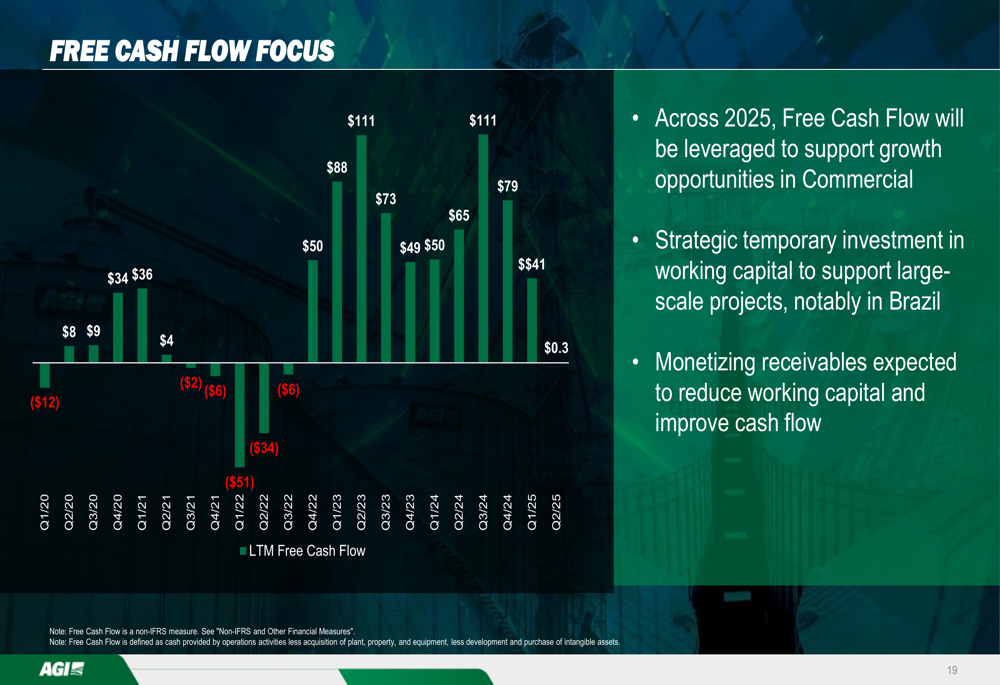

Free Cash Flow has been trending downward, with the Last Twelve Months (LTM) figure at $41 million in Q2 2025. Management explained that throughout 2025, Free Cash Flow will be leveraged to support growth opportunities in the Commercial segment, with strategic temporary investments in working capital to support large-scale projects, particularly in Brazil.

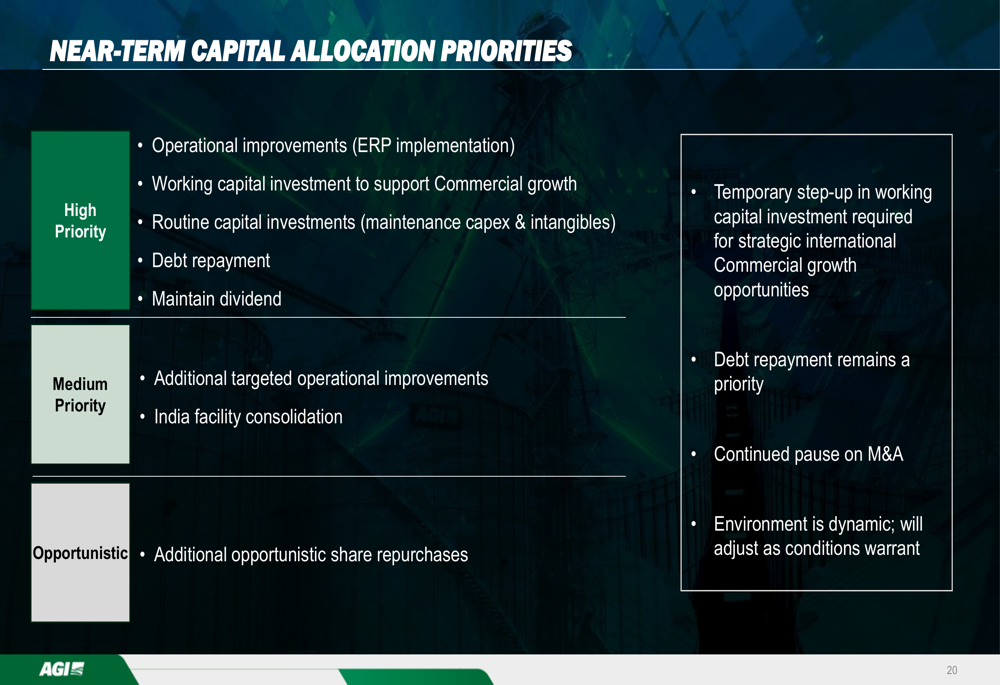

The company outlined its near-term capital allocation priorities, with high-priority items including operational improvements (ERP implementation), working capital investment to support Commercial growth, routine capital investments, debt repayment, and maintaining dividends. Medium-priority initiatives include additional targeted operational improvements and India facility consolidation, while opportunistic share repurchases were listed as a lower priority.

Outlook and Guidance

Despite the challenges in the Farm segment, AGI reiterated its full-year 2025 adjusted EBITDA guidance of at least $225 million. The company expressed confidence in its Commercial segment outlook for the second half of 2025, supported by a healthy order book. However, management continued to emphasize limited visibility into the Farm segment’s second-half performance due to challenging market conditions.

On the topic of tariffs, AGI noted that it continues to monitor evolving policies closely and has made several tactical adjustments in recent months, including negotiations with steel suppliers in the U.S. and Canada as well as pricing actions. The company estimates a "relatively minor direct cost impact" in 2025 but acknowledged that tariff and trade policies could ultimately impact its financial outlook should they further hamper farmer sentiment, aggregate equipment demand, and the global economy.

This Q2 2025 presentation reveals a company navigating a complex agricultural market by leveraging its diversified business model and international growth opportunities while managing through a cyclical downturn in its traditional North American Farm business. The contrast between segment performances underscores the value of AGI’s strategic diversification efforts as it works to maintain financial stability and position itself for recovery in challenging markets.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.