United Homes Group stock plunges after Nikki Haley, directors resign

Introduction & Market Context

Albemarle Corporation (NYSE:ALB) released its Q2 2025 earnings presentation on July 31, 2025, revealing sequential improvement in financial performance despite year-over-year declines. The specialty chemicals company, a global leader in lithium production, continues to navigate a challenging price environment while positioning itself for long-term growth in the electric vehicle and energy storage markets.

The company’s stock closed at $71.60 on July 30, 2025, and moved up 0.42% in after-hours trading to $71.90. This represents a significant recovery from earlier in the year when the stock was trading closer to $60, though still well below its 52-week high of $113.91.

Quarterly Performance Highlights

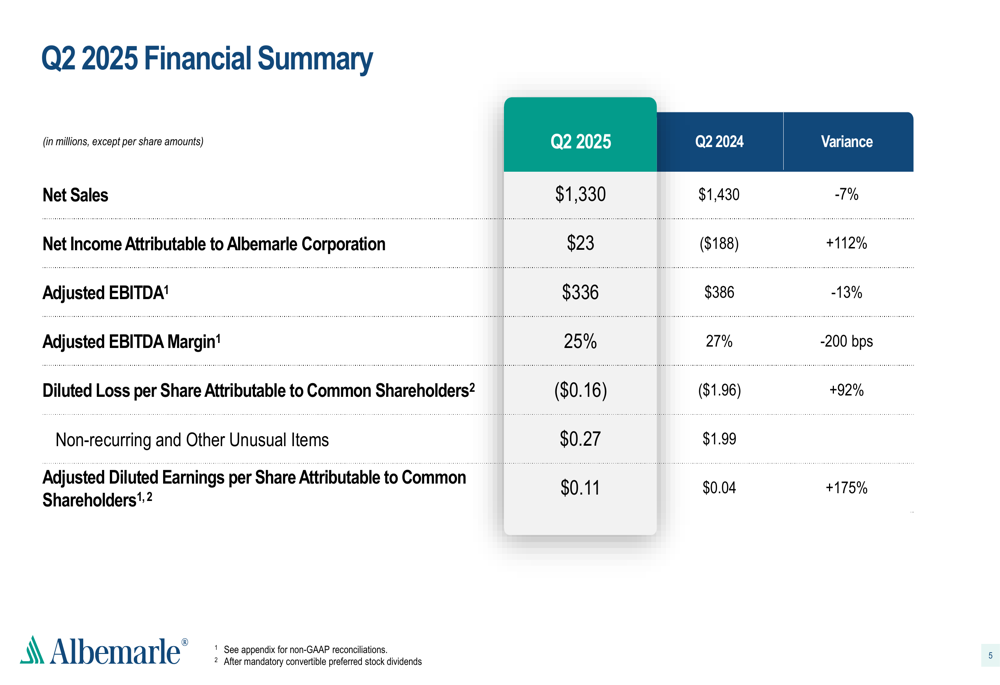

Albemarle reported Q2 2025 net sales of $1.33 billion, down 7% compared to Q2 2024, but showing sequential improvement from Q1 2025’s $1.1 billion. Adjusted EBITDA came in at $336 million, representing a 13% year-over-year decline but a significant improvement from the previous quarter’s $267 million.

As shown in the following financial summary table, the company returned to profitability with net income of $23 million, a substantial improvement from the $188 million loss in the same quarter last year:

Adjusted diluted earnings per share reached $0.11, up 175% from $0.04 in Q2 2024, and marking a significant turnaround from Q1 2025’s loss of $0.18 per share. This improvement came despite continued pressure on lithium prices, which remain around $9/kg, well below historical highs.

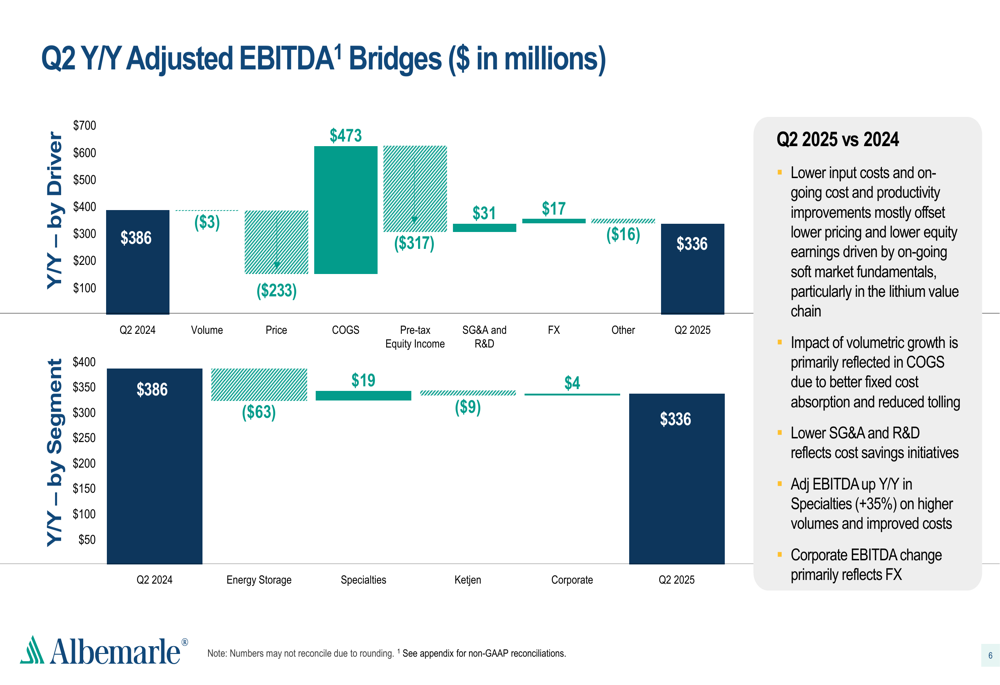

The company’s year-over-year performance was impacted by lower pricing, but partially offset by lower input costs and successful cost reduction initiatives, as illustrated in this bridge analysis:

Strategic Initiatives & Cost Management

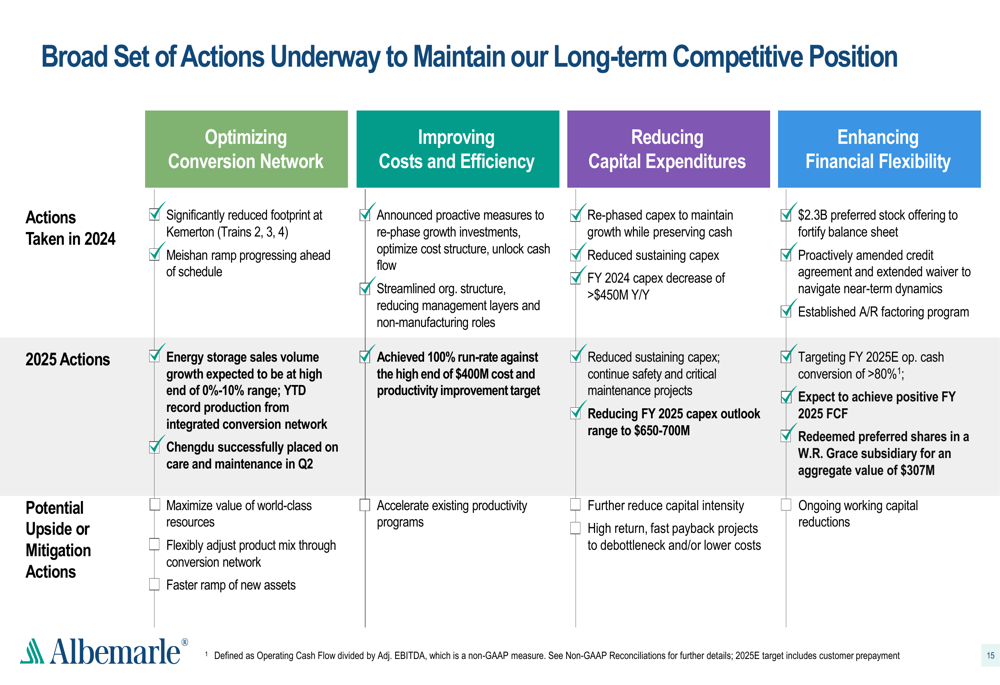

Albemarle has implemented aggressive cost-cutting measures and operational improvements to counter the challenging pricing environment. The company announced it has achieved 100% of its $400 million cost and productivity improvement target, which has been crucial in maintaining profitability despite lower lithium prices.

Capital expenditure plans have been significantly scaled back, with the 2025 outlook reduced to $650-700 million, representing a reduction of approximately 60% year-over-year. The company has also optimized its conversion network, including significantly reducing the footprint at its Kemerton facility.

The following chart outlines Albemarle’s comprehensive approach to maintaining long-term competitiveness:

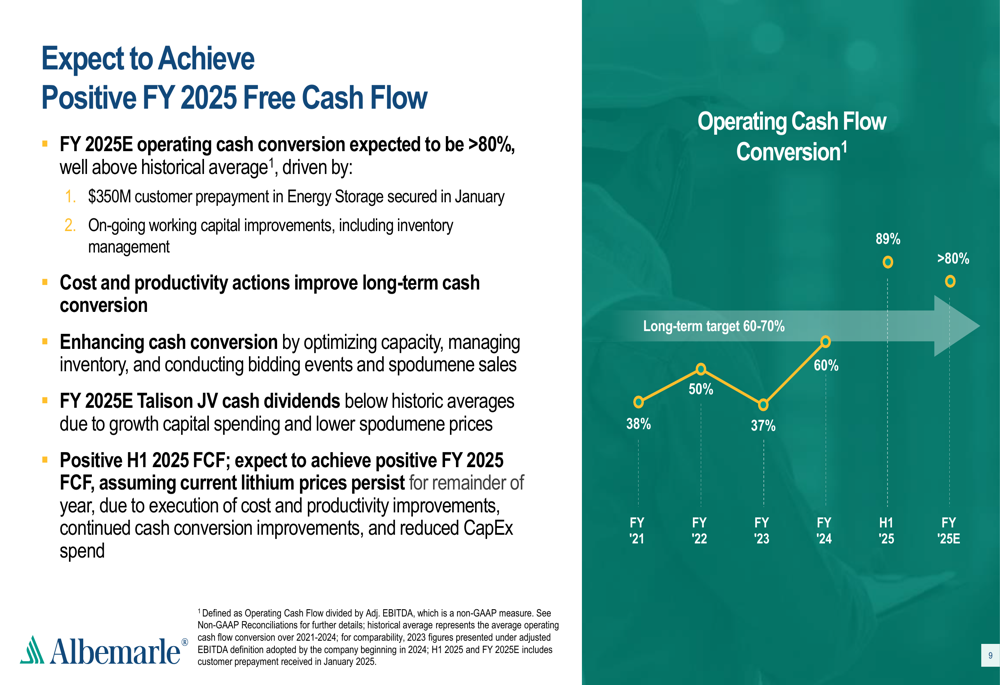

Cash flow management has been a key focus area, with operating cash flow conversion improving dramatically from 38% in FY 2021 to 89% in the first half of 2025. The company expects to maintain this momentum with a full-year 2025 conversion rate exceeding 80%, as shown in this progression:

Lithium Market Outlook

Despite current pricing challenges, Albemarle remains optimistic about the long-term fundamentals of the lithium market. The company projects that global lithium demand will more than double between 2024 and 2030, driven primarily by electric vehicle adoption and energy storage systems.

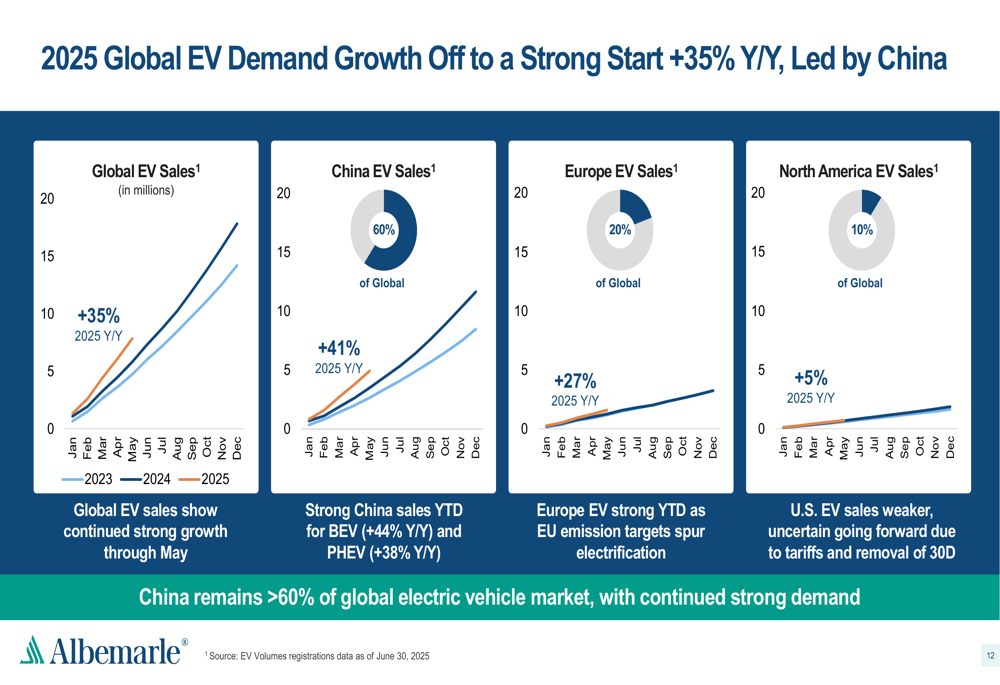

Global EV sales continue to show strong growth, particularly in China and Europe, as illustrated in the following regional breakdown:

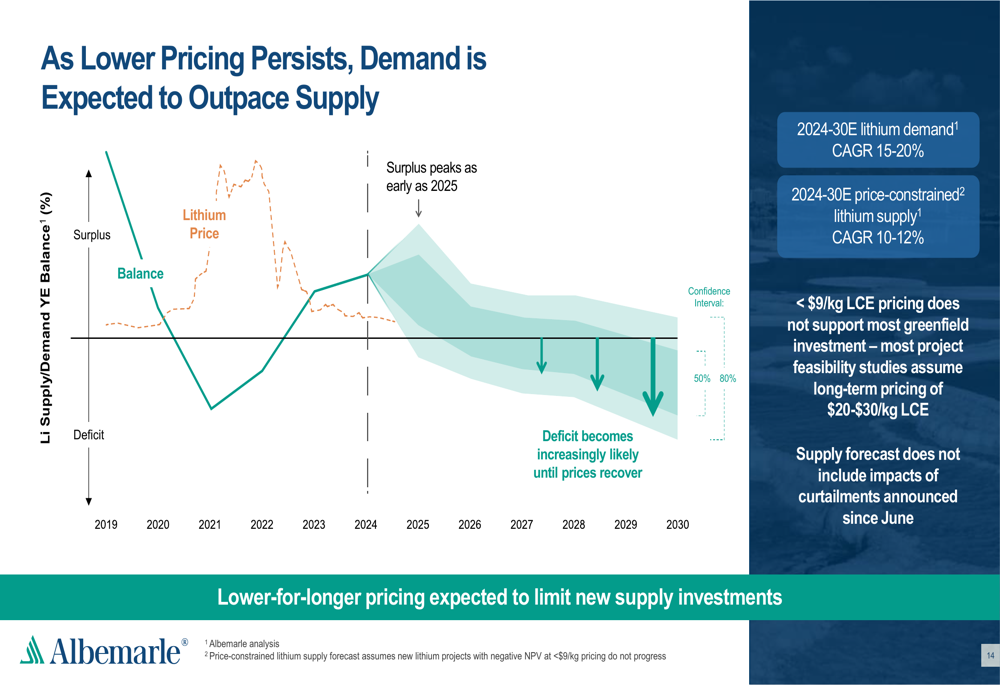

Perhaps most significantly, Albemarle’s analysis suggests that the current supply surplus in lithium is likely to peak as early as 2025, with a growing deficit expected in subsequent years as demand outpaces supply. This supply-demand imbalance is illustrated in the following forecast:

The company notes that current lithium prices around $9/kg are insufficient to support greenfield investments, which could further constrain future supply growth. Albemarle projects 2024-2030 lithium demand to grow at a CAGR of 15-20%, while price-constrained supply is expected to grow at just 10-12%.

Financial Position & Outlook

Albemarle maintains a strong financial position with $3.4 billion in liquidity, including $1.8 billion in cash and cash equivalents. The company’s net debt to adjusted EBITDA ratio stands at 2.3x, well below the Q2 covenant limit of 5.75x, providing significant financial flexibility.

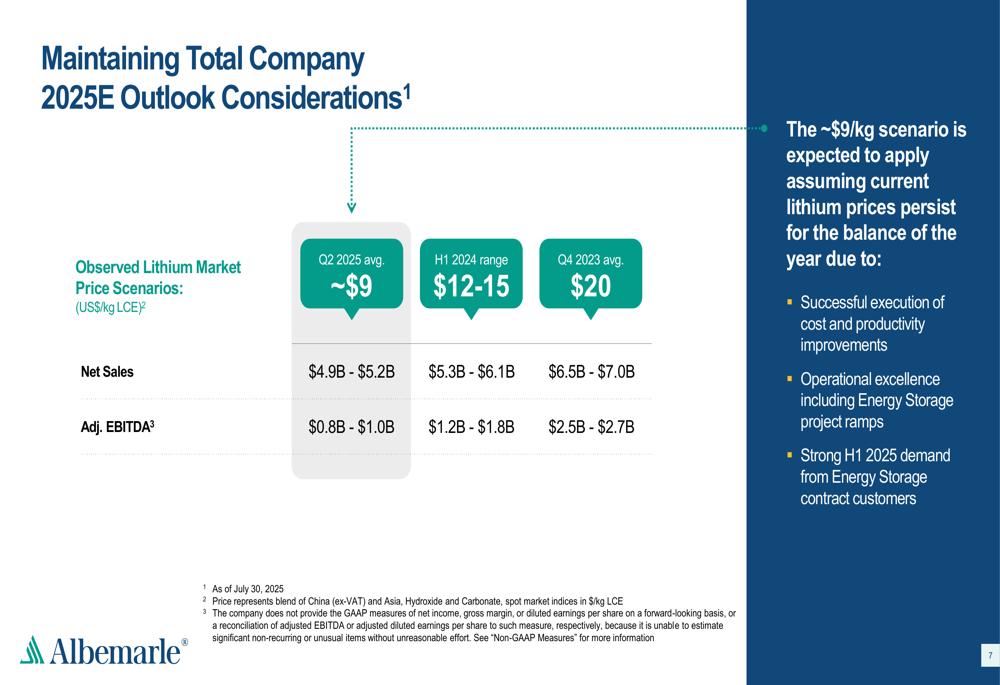

For the full year 2025, Albemarle has provided scenario-based guidance tied to lithium pricing. At the current price level of approximately $9/kg, the company projects:

The company expects to achieve positive free cash flow for the full year 2025 if current lithium prices persist, thanks to its cost reduction initiatives and improved cash conversion. Energy Storage segment volumes are projected to grow near the high end of the 0-10% year-over-year range, with approximately 50% of 2025 salt volumes sold under long-term agreements.

Albemarle’s management remains focused on navigating the near-term challenges while positioning the company to capitalize on the expected long-term growth in lithium demand, leveraging its world-class resources, process chemistry expertise, and customer-centric approach to maintain its competitive position in the market.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.