Street Calls of the Week

Introduction & Market Context

Albemarle Corporation (NYSE:ALB) released its second quarter 2025 earnings presentation on July 31, showing the company’s efforts to navigate a challenging lithium pricing environment through operational efficiencies and cost improvements. Despite year-over-year declines in key metrics, Albemarle maintained its full-year outlook and highlighted sequential improvements in its financial performance.

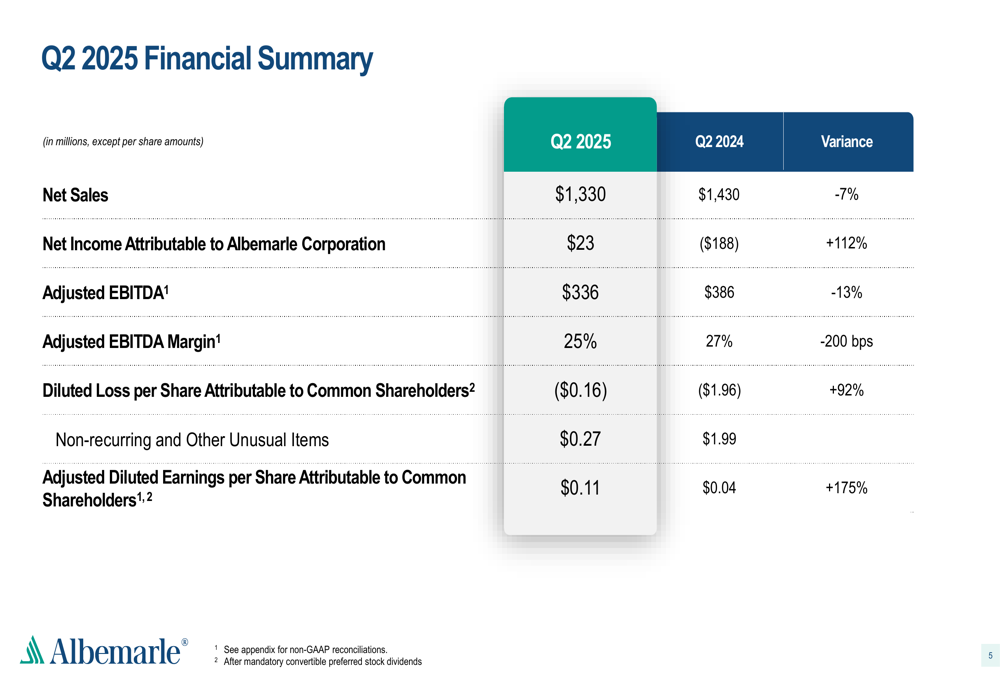

The specialty chemicals producer reported Q2 2025 net sales of $1.3 billion, down 7% from $1.43 billion in the same period last year, primarily due to lower lithium prices. The stock declined 2.69% in after-hours trading to $93.75, reflecting investor concerns about continued pricing pressures in the lithium market.

Quarterly Performance Highlights

Albemarle’s Q2 2025 results showed mixed performance across key financial metrics. While year-over-year comparisons reflected the impact of lower lithium pricing, the company achieved sequential improvements and made significant progress on cost-saving initiatives.

As shown in the following financial summary from the presentation:

Net income attributable to Albemarle Corporation was $23 million, representing a 112% improvement from a loss of $188 million in Q2 2024. Adjusted EBITDA came in at $336 million, down 13% from $386 million in the prior year, with adjusted EBITDA margin contracting 200 basis points to 25%. Adjusted diluted earnings per share attributable to common shareholders was $0.11, up 175% from $0.04 in Q2 2024.

The company experienced volume growth in key segments, with Energy Storage volumes up 15% and Specialties volumes increasing by 6% year-over-year. This volume growth, combined with improved fixed cost absorption and cost savings, helped offset some of the pricing pressure.

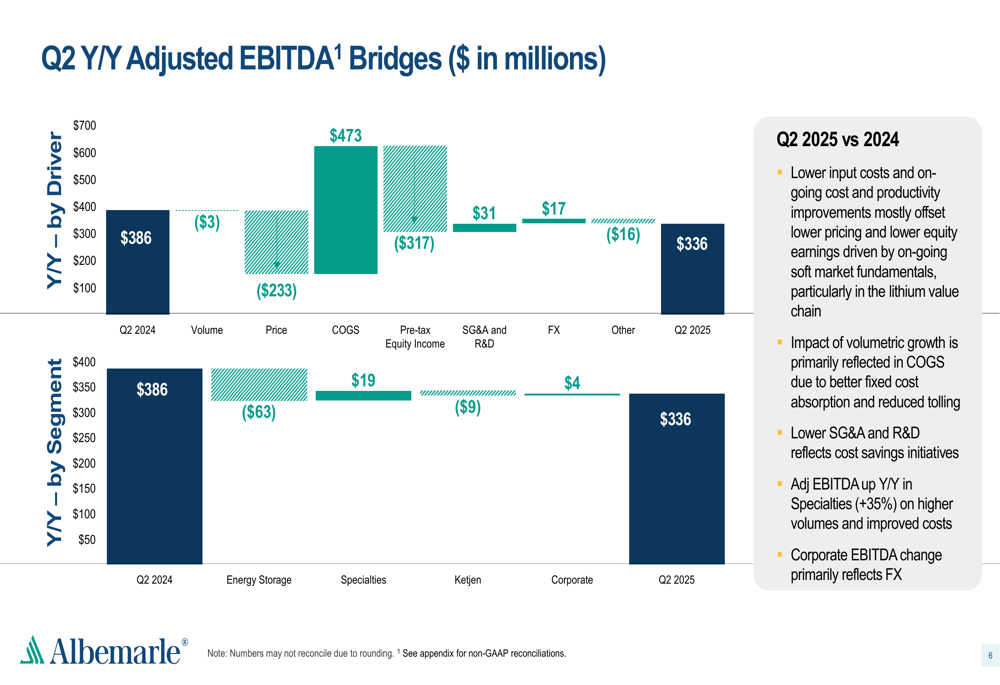

The following bridge chart illustrates the factors affecting Albemarle’s adjusted EBITDA performance:

As the chart demonstrates, lower pricing had a significant negative impact of $233 million on adjusted EBITDA, but this was largely offset by COGS improvements of $473 million. Pre-tax equity income declined by $317 million, while SG&A and R&D improvements contributed $31 million and favorable foreign exchange added $17 million.

Strategic Initiatives

Albemarle has implemented a comprehensive strategy to maintain competitiveness amid challenging market conditions. The company achieved 100% run-rate against its $400 million cost and productivity improvement target ahead of schedule, demonstrating strong execution of its efficiency initiatives.

Capital expenditure for full-year 2025 has been reduced to a range of $650-700 million, down approximately 60% year-over-year, as the company prioritizes cash preservation and returns. This disciplined approach to capital allocation is part of Albemarle’s broader strategy to enhance financial flexibility.

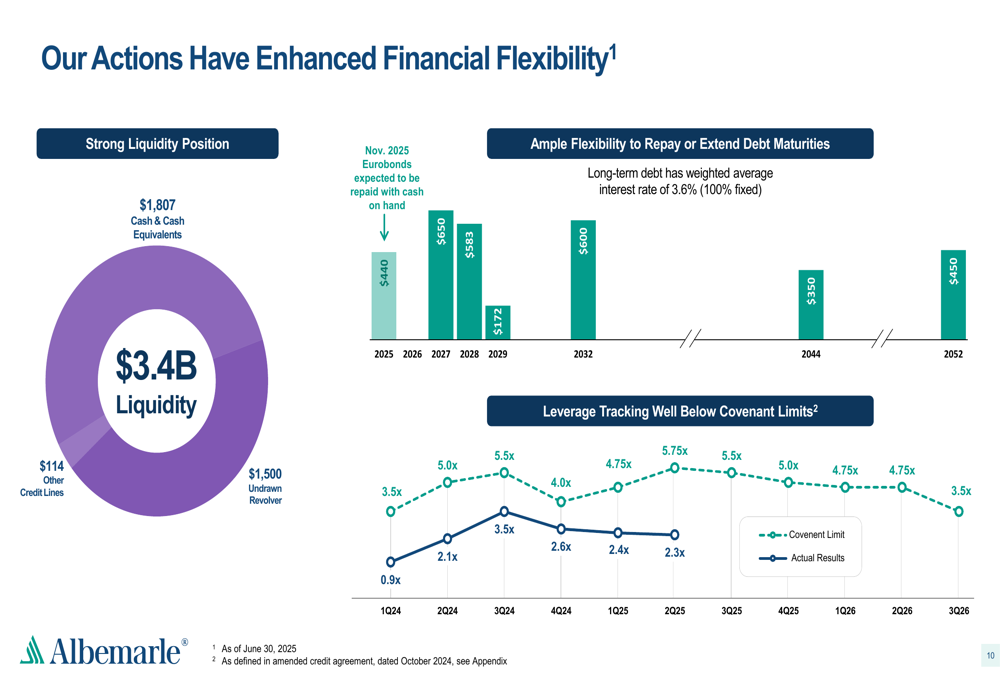

The company’s financial position remains solid, with $3.4 billion in liquidity, including $1.8 billion in cash and equivalents. The net debt to adjusted EBITDA ratio stood at 2.3x, well below the Q2 covenant limit of 5.75x.

As illustrated in the following chart showing the company’s debt maturity profile and leverage ratio:

Albemarle has maintained significant financial flexibility, with ample capacity to repay or extend debt maturities. The November 2025 Eurobonds are expected to be repaid with cash on hand, and the company’s long-term debt carries a weighted average interest rate of 3.6%, which is 100% fixed.

Lithium Market Dynamics

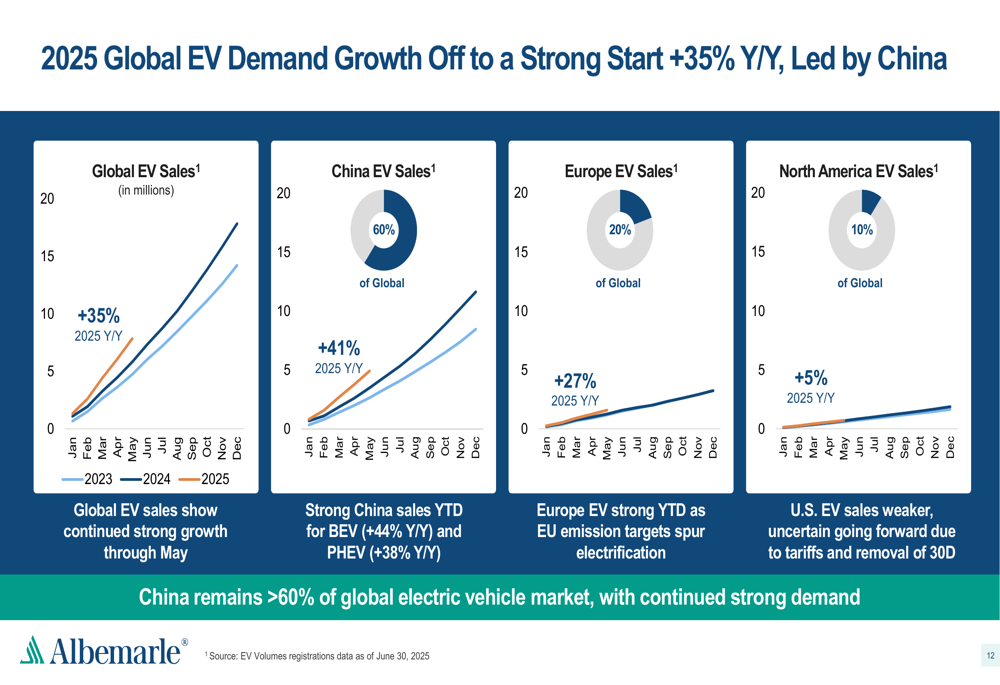

Despite near-term pricing pressures, Albemarle remains optimistic about the long-term fundamentals of the lithium market. Global electric vehicle demand has shown strong growth, increasing 35% year-over-year through May 2025, led by China at 41% growth.

The following chart illustrates regional EV demand trends:

China continues to dominate the global electric vehicle market, representing over 60% of global demand. Europe has also shown robust growth at 27% year-over-year, while North America has experienced more modest growth of 5%, affected by tariffs and the removal of certain incentives.

Beyond electric vehicles, energy storage systems (ESS) have emerged as a significant growth driver for lithium demand, with global ESS battery demand increasing by 126% year-over-year through May 2025.

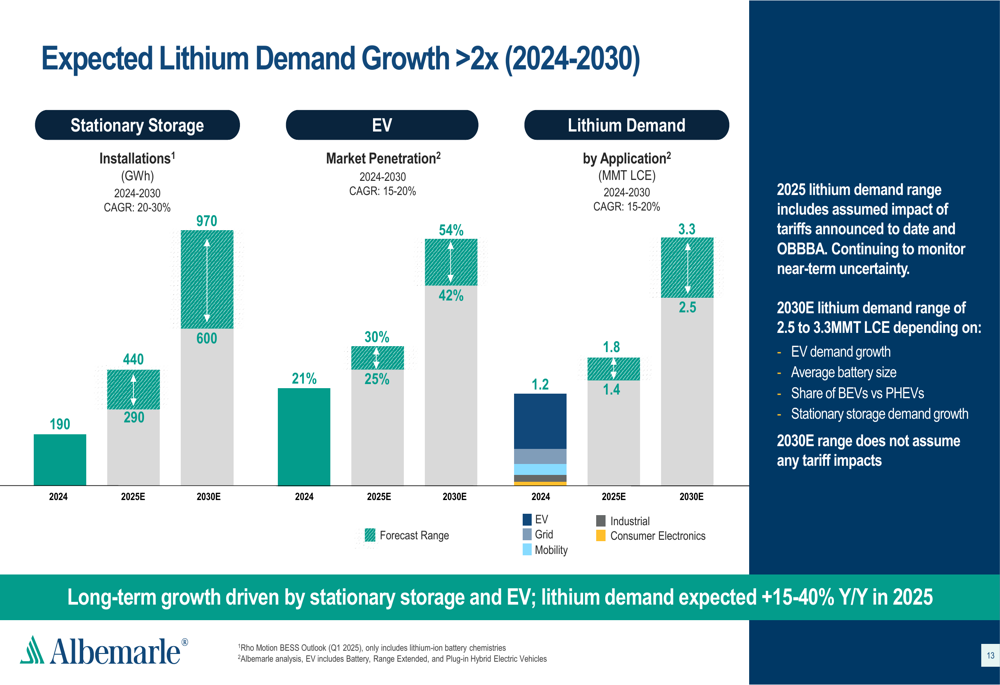

Albemarle projects substantial long-term growth in lithium demand, as illustrated in the following chart:

The company expects lithium demand to more than double between 2024 and 2030, driven by increasing EV market penetration and rapid growth in stationary storage installations. EV market penetration is projected to reach 54% by 2030, up from 21% in 2024, while stationary storage installations are expected to grow from 190 GWh in 2024 to 970 GWh by 2030.

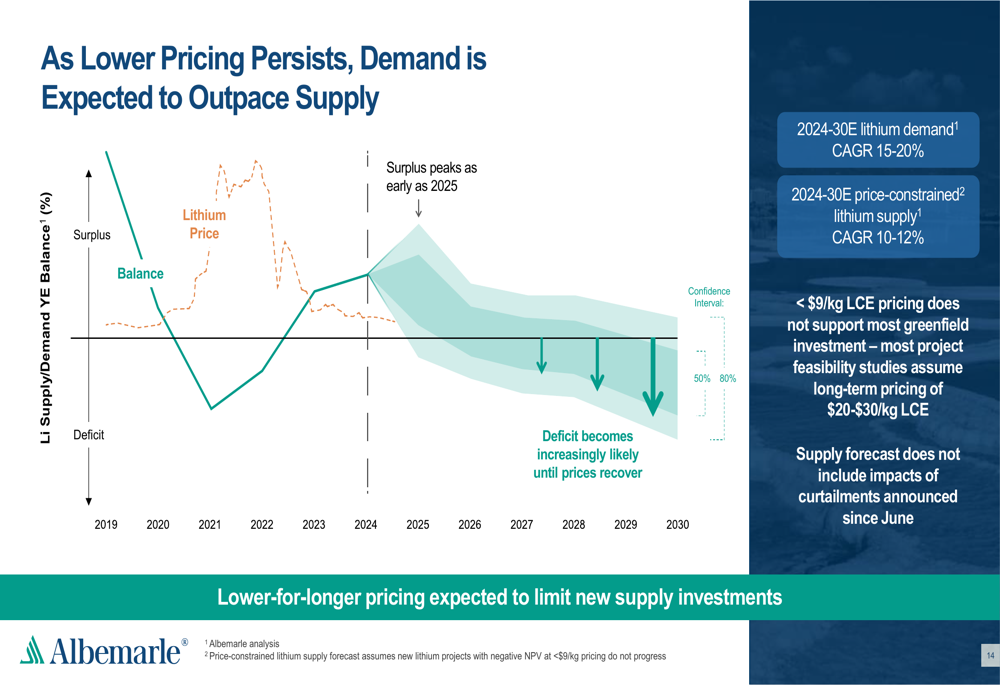

Looking at the supply-demand balance, Albemarle anticipates that lower lithium prices will constrain new supply investments, potentially leading to a supply deficit in the coming years:

The company projects that lithium demand will grow at a CAGR of 15-20% between 2024 and 2030, outpacing the expected supply growth of 10-12%. This imbalance suggests that current pricing levels may not be sustainable in the long term.

Forward-Looking Statements

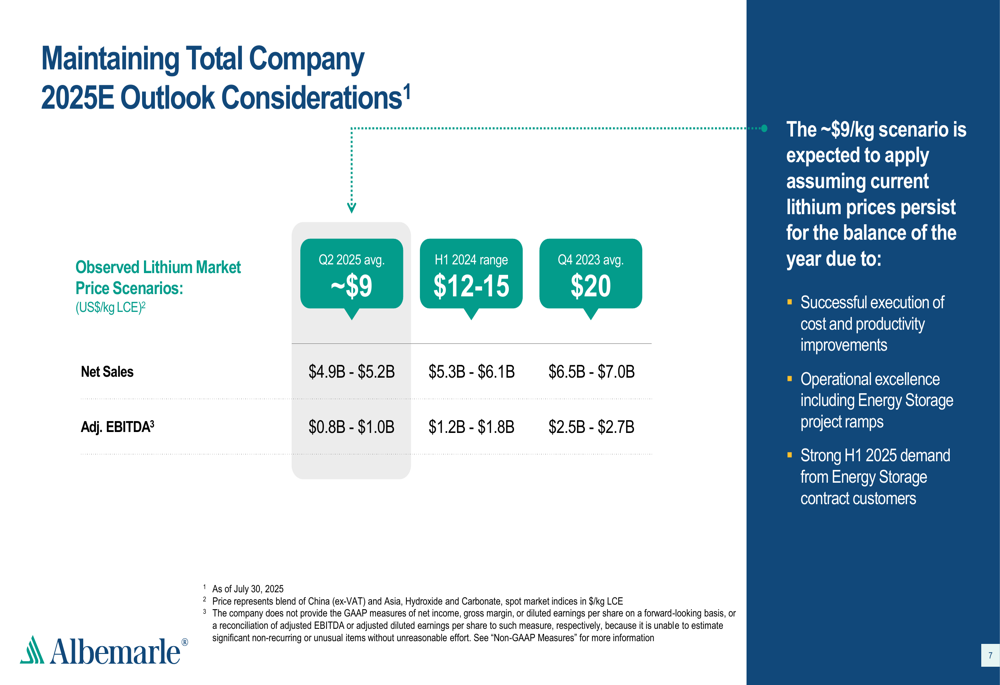

Albemarle has maintained its full-year 2025 outlook considerations, with financial projections based on a lithium market price scenario of approximately $9/kg. Under this scenario, the company expects:

At the current lithium price of approximately $9/kg, Albemarle projects total company net sales of $4.9-5.2 billion and adjusted EBITDA of $0.8-1.0 billion for full-year 2025. This outlook reflects the company’s successful cost execution, operational excellence, and strong demand from Energy Storage contract customers in the first half of 2025.

The company expects Energy Storage sales volume growth to be at the high end of the 0-10% range for the full year. Margins in this segment are projected to average in the mid-teens percentage range in the second half of 2025, with second-half revenue expected to be flat to slightly up compared to the first half.

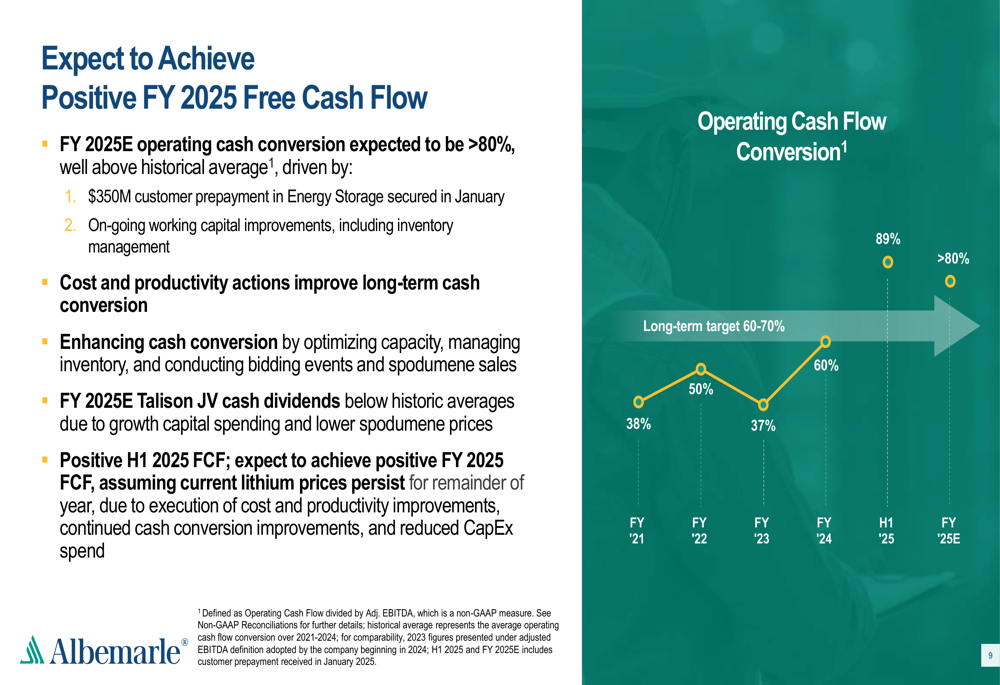

Notably, Albemarle expects to achieve positive free cash flow in 2025, supported by improved operating cash conversion of over 80%:

The company’s cash conversion has shown consistent improvement over the years, from 38% in FY2021 to a projected >80% in FY2025. This improvement is driven by a $350 million customer prepayment in Energy Storage secured in January, ongoing working capital improvements, and the successful implementation of cost and productivity initiatives.

In conclusion, while Albemarle faces near-term challenges from lower lithium prices, the company’s strategic initiatives to reduce costs, optimize operations, and enhance financial flexibility position it well to navigate the current market environment while capitalizing on the long-term growth opportunities in the lithium market.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.