United Homes Group stock plunges after Nikki Haley, directors resign

Introduction & Market Context

Alkami Technology Inc (NASDAQ:ALKT), a cloud-based digital banking platform provider serving U.S. financial institutions, presented strong second quarter 2025 results on July 30, showing continued momentum in its core business and strategic expansion through acquisition. The company operates in an estimated $14 billion total addressable market, focusing on community, regional, and super-regional financial institutions with assets between $100 million and $450 billion.

Despite the positive financial results, Alkami’s stock experienced a slight decline in premarket trading, dropping 0.61% to $23, according to market data. The company currently has a market capitalization of approximately $2.4 billion.

As shown in the following overview of Alkami’s business model and market positioning:

Q2 2025 Performance Highlights

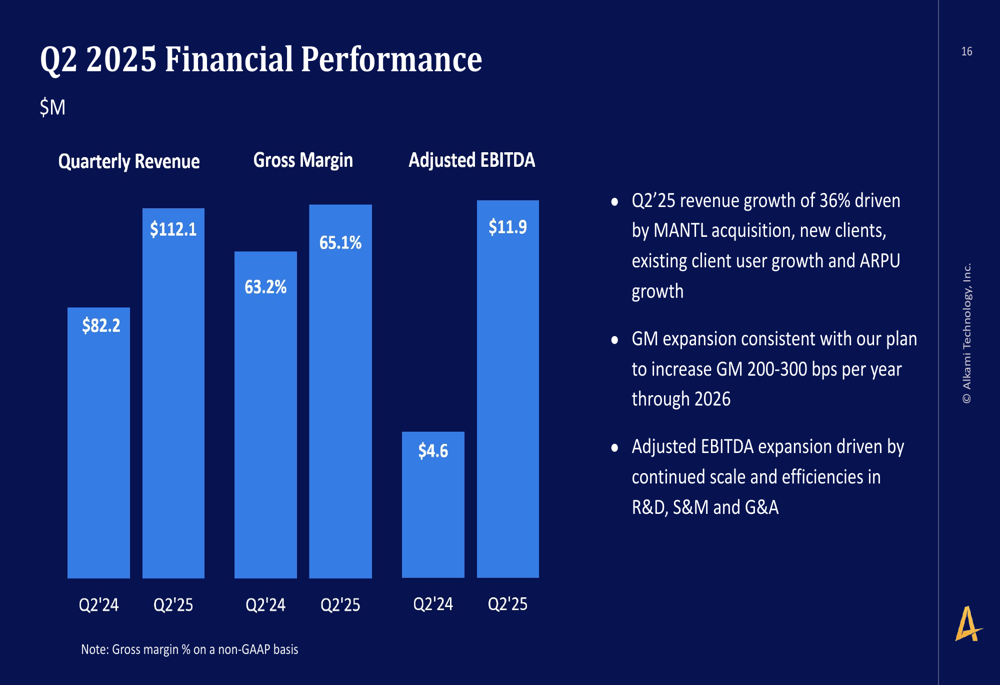

Alkami reported Q2 2025 revenue of $112.1 million, representing a 36% increase compared to Q2 2024. This growth was driven by the MANTL acquisition, new client additions, existing client user growth, and increased average revenue per user (ARPU). The company’s adjusted EBITDA reached $11.9 million, a significant improvement from $4.6 million in the same period last year. Gross margin expanded to 65.1%, up from 63.2% in Q2 2024, consistent with the company’s plan to increase gross margin by 200-300 basis points annually through 2026.

The following chart illustrates these key financial metrics:

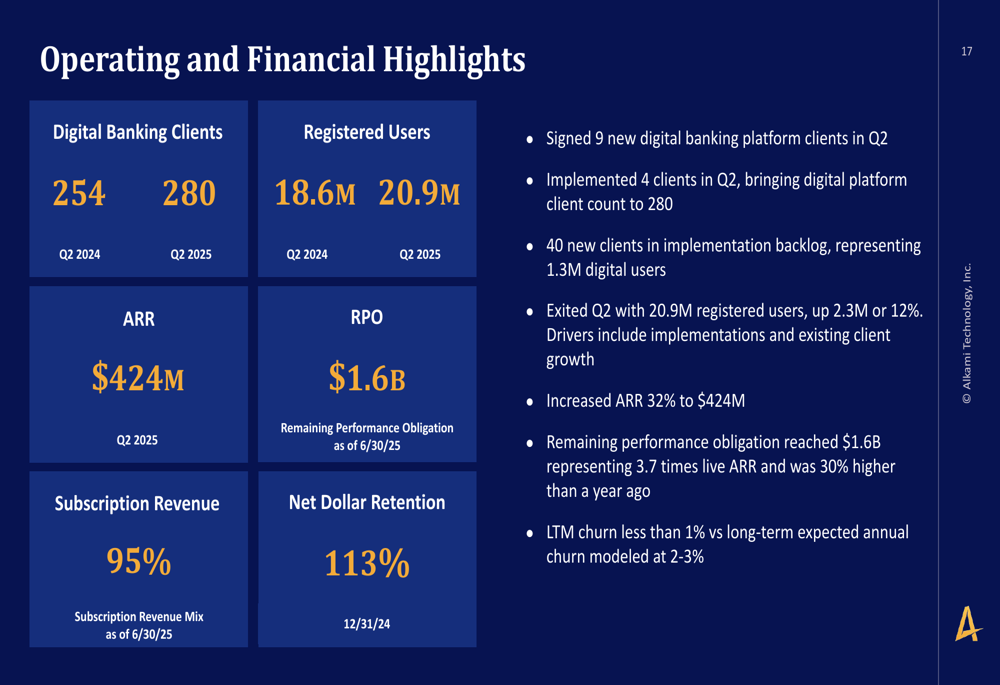

Operational highlights for the quarter included signing 9 new digital banking platform clients and implementing 4 clients, bringing the total digital platform client count to 280, up from 254 in Q2 2024. Registered users increased to 20.9 million, compared to 18.6 million in the prior year period. The company’s annual recurring revenue (ARR) grew 32% to $424 million, while remaining performance obligations reached $1.6 billion. Subscription revenue accounted for 95% of total revenue, and net dollar retention stood at 113% as of December 31, 2024.

The following chart provides a comprehensive view of these operating and financial highlights:

Strategic Initiatives and MANTL Acquisition

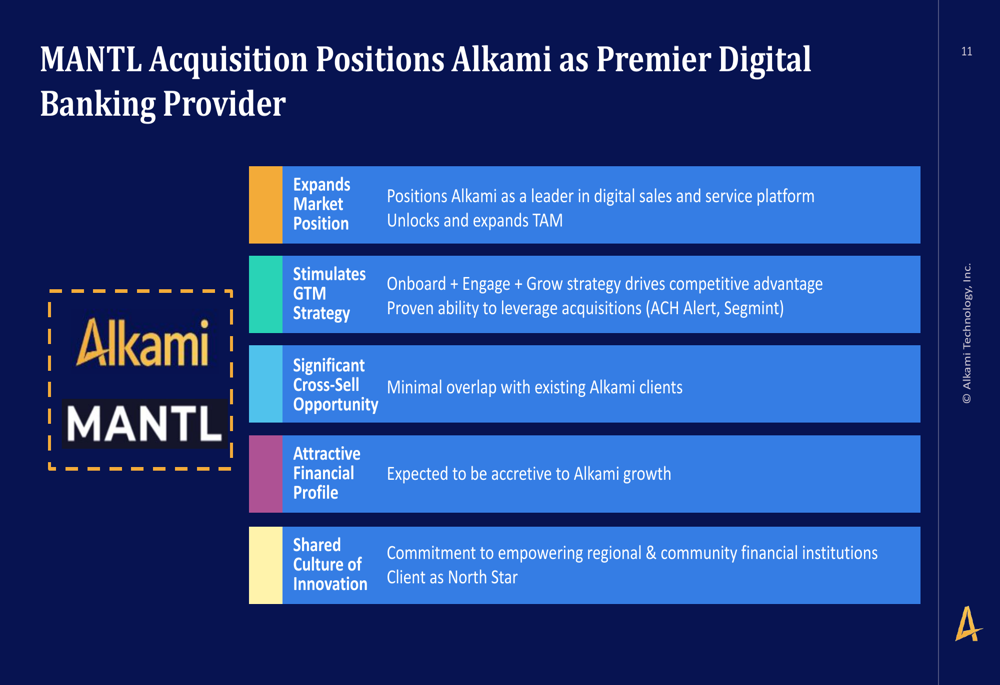

A significant strategic development highlighted in the presentation was Alkami’s acquisition of MANTL, which positions the company as a premier digital banking provider with expanded capabilities in digital account opening and loan origination. This acquisition extends Alkami’s total addressable market and creates significant cross-selling opportunities with minimal overlap among existing clients.

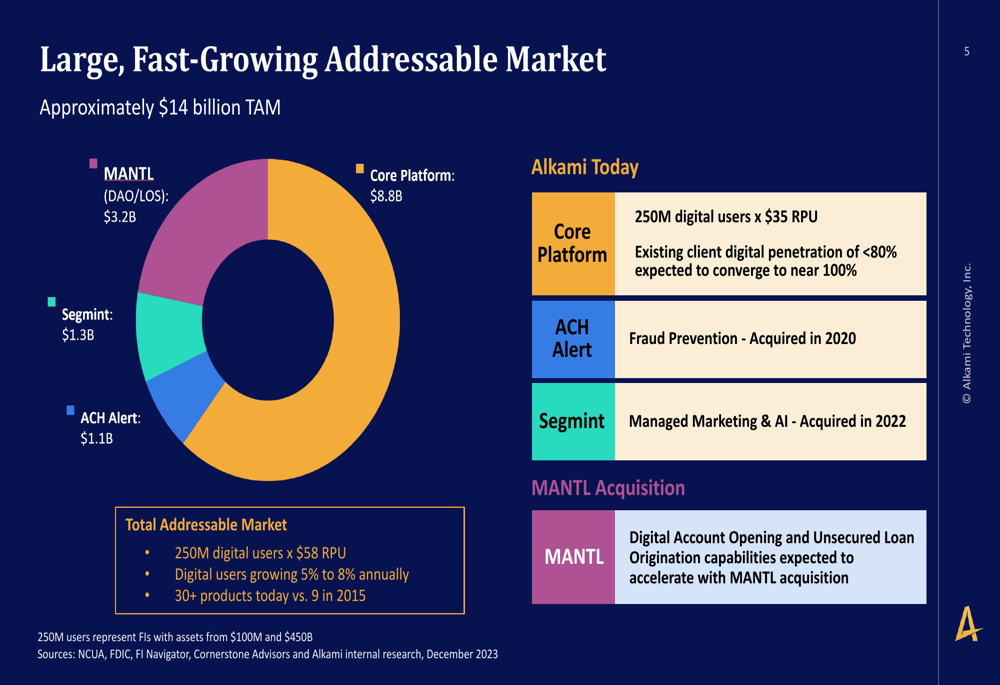

The company’s addressable market of approximately $14 billion is broken down into core platform ($8.8B), MANTL (digital account opening/loan origination system) ($3.2B), Segmint (data and marketing) ($1.3B), and ACH Alert (fraud prevention) ($1.1B).

As shown in the following chart of Alkami’s addressable market:

The MANTL acquisition is expected to be accretive to Alkami’s growth and enhances the company’s "Onboard + Engage + Grow" strategy. Management emphasized the shared culture of innovation between the companies and their commitment to empowering regional and community financial institutions.

The following slide details the strategic benefits of the MANTL acquisition:

Long-Term Financial Outlook

Alkami provided 2025 financial guidance projecting annual revenue of $445 million, representing 33% growth compared to 2024, and annual adjusted EBITDA of $52.8 million. According to the earnings call, the actual guidance range for 2025 revenue is $443 million to $447 million.

The company’s guidance is illustrated in the following chart:

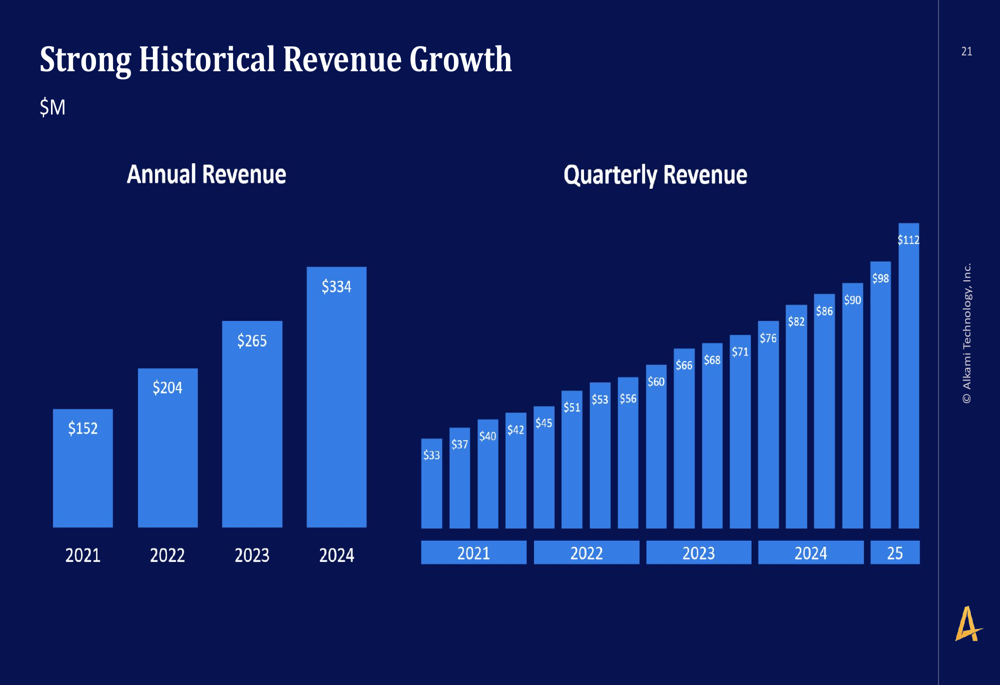

Alkami’s historical revenue growth has been strong and consistent, as shown in the following chart tracking both annual and quarterly revenue trends:

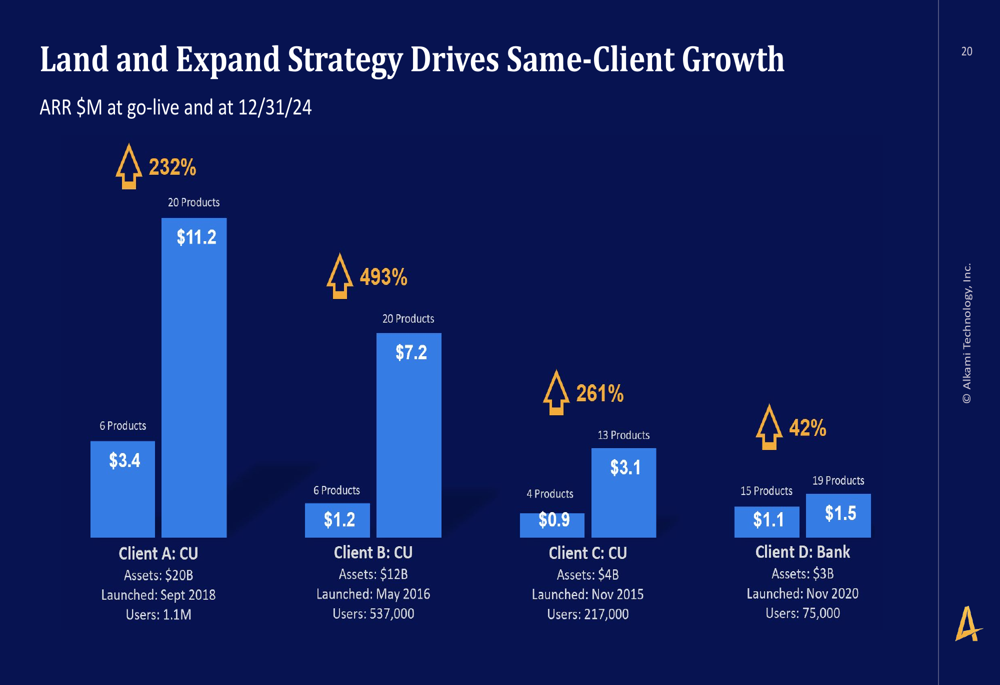

The company’s "land and expand" strategy has been successful in driving same-client growth, with several examples showing significant ARR expansion after initial implementation. For instance, Client A (a credit union with $20B in assets) saw ARR growth of 232% from $3.4 million at go-live to $11.2 million by the end of 2024, while expanding from 6 products to 20 products.

The following chart illustrates the success of this strategy with specific client examples:

Market Position and Competitive Landscape

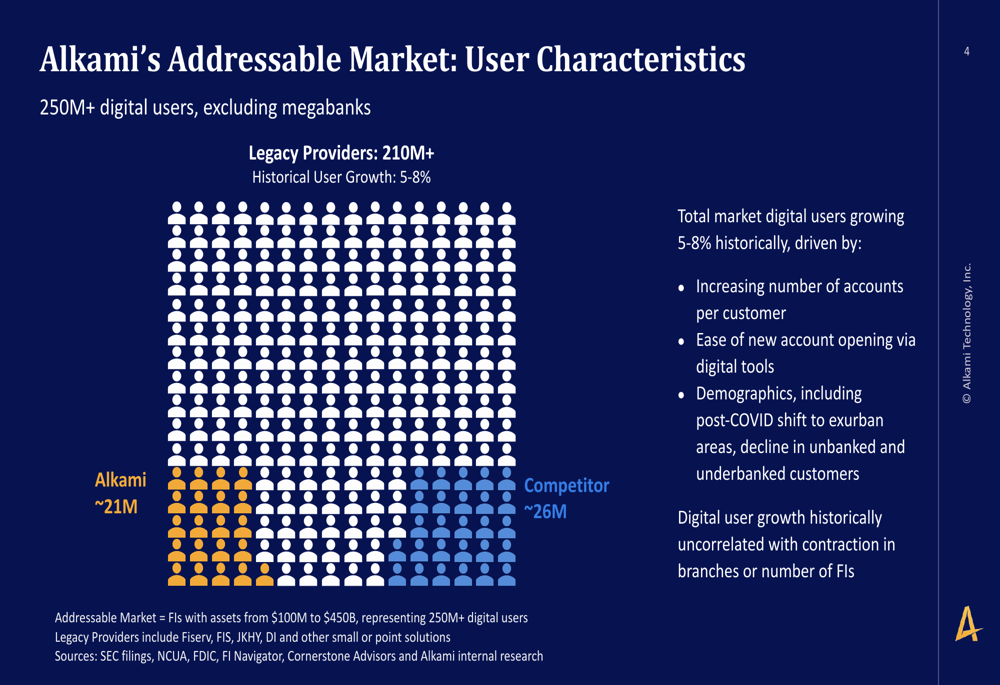

Alkami positions itself in a digital banking market that serves over 250 million users, excluding megabanks. The company currently serves approximately 21 million of these users, while its main competitor serves around 26 million, and legacy providers like Fiserv, FIS, JKHY, and DI account for over 210 million users.

The following chart illustrates this market distribution:

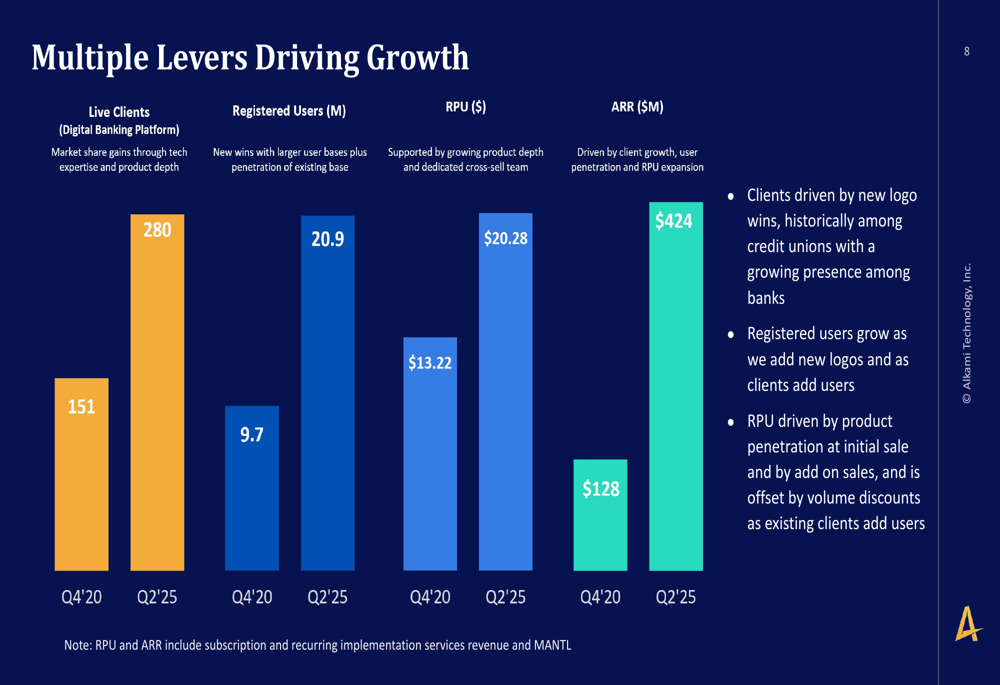

Alkami’s growth strategy leverages multiple levers, including expanding its client base, increasing registered users, and growing revenue per user (RPU). Since Q4 2020, the company has grown its live clients from 151 to 280, registered users from 9.7 million to 20.9 million, and RPU from $13.22 to $20.28, resulting in ARR growth from $128 million to $424 million.

The company’s multiple growth levers are illustrated in the following chart:

Looking ahead, Alkami aims to achieve a long-term financial profile with gross margins reaching 65% by 2026 and adjusted EBITDA margins approaching 19%. The company expects to benefit from continued scale and efficiency improvements in R&D, sales and marketing, and G&A expenses, with sales and marketing projected to decrease to 15% of revenue by 2026.

CEO Alex Schutman emphasized during the earnings call that "digital banking is a mandatory innovation" and highlighted the company’s focus on integrating various platforms to create a unified digital sales and service platform. The company faces potential challenges including JPMorgan’s data access fee impact, competition from mega banks and fintechs, and economic uncertainties that could affect technology spending in the banking sector.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.