Trump administration authorizes CIA for covert action in Venezuela - Bloomberg

Introduction & Market Context

Alphatec Holdings Inc (NASDAQ:ATEC), a pure-play spine technology company, presented its Q2 2025 financial results on July 31, 2025, highlighting significant achievements in both growth and profitability. The company’s stock closed at $13.24, up 4.38% in regular trading on the day of the announcement, though it experienced a slight 1.06% decline to $13.10 in aftermarket trading.

ATEC’s presentation revealed the company has achieved multiple financial milestones, including its first quarter of non-GAAP net income profitability and positive free cash flow, while maintaining surgical revenue growth that significantly outpaces the broader spine market.

Quarterly Performance Highlights

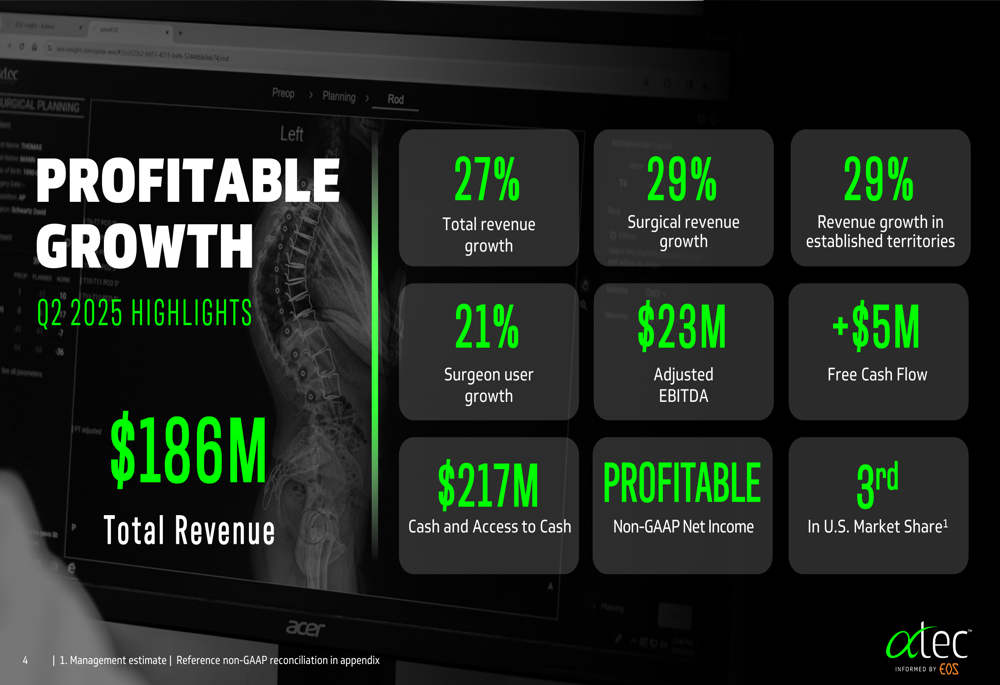

ATEC reported robust financial results for Q2 2025, with total revenue reaching $186 million, representing a 27% year-over-year increase. Surgical revenue, which accounts for the bulk of the company’s business, grew even faster at 29% compared to the same quarter last year.

As shown in the following financial highlights slide, the company achieved surgical revenue growth approximately six times faster than the overall market while significantly improving profitability metrics:

The company provided a more detailed breakdown of its Q2 performance metrics, revealing strong growth across multiple dimensions. Particularly notable was the 21% growth in surgeon users, indicating expanding market adoption of ATEC’s technologies. The company also confirmed its position as the third-largest player in the U.S. spine market.

As illustrated in this comprehensive metrics overview:

Detailed Financial Analysis

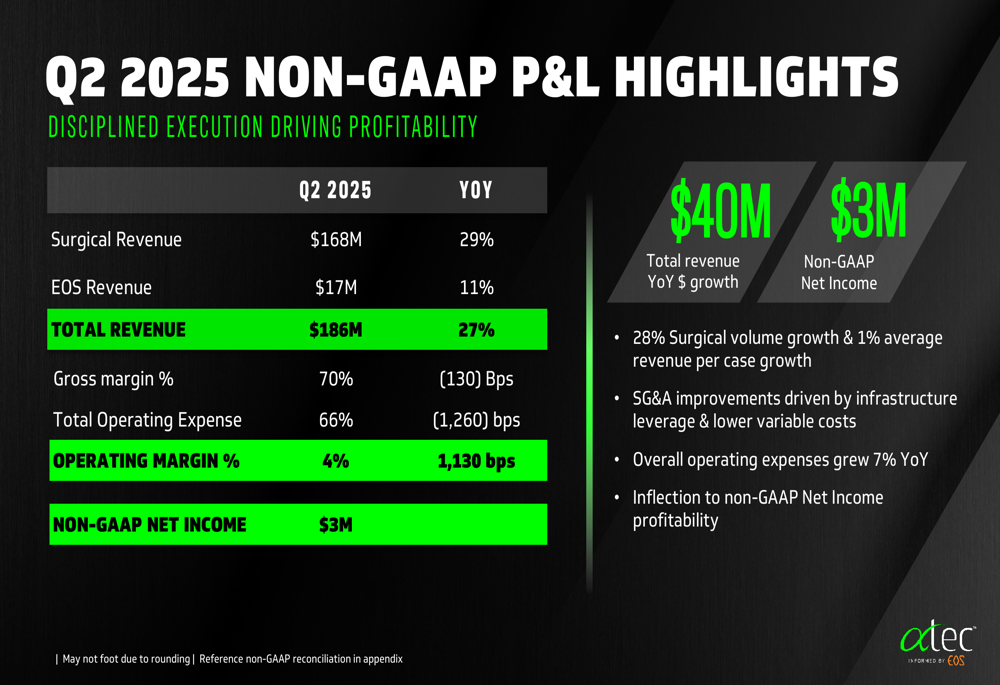

ATEC’s financial performance demonstrated disciplined execution driving profitability. The company reported its first quarter of non-GAAP net income at $3 million, while operating margin improved by 1,130 basis points year-over-year to reach 4%.

The presentation highlighted that total operating expenses grew by only 7% year-over-year, despite the 27% revenue growth, demonstrating significant operational leverage. This efficiency was attributed to infrastructure leverage and lower variable costs.

The detailed profit and loss statement reveals the company’s progress toward sustainable profitability:

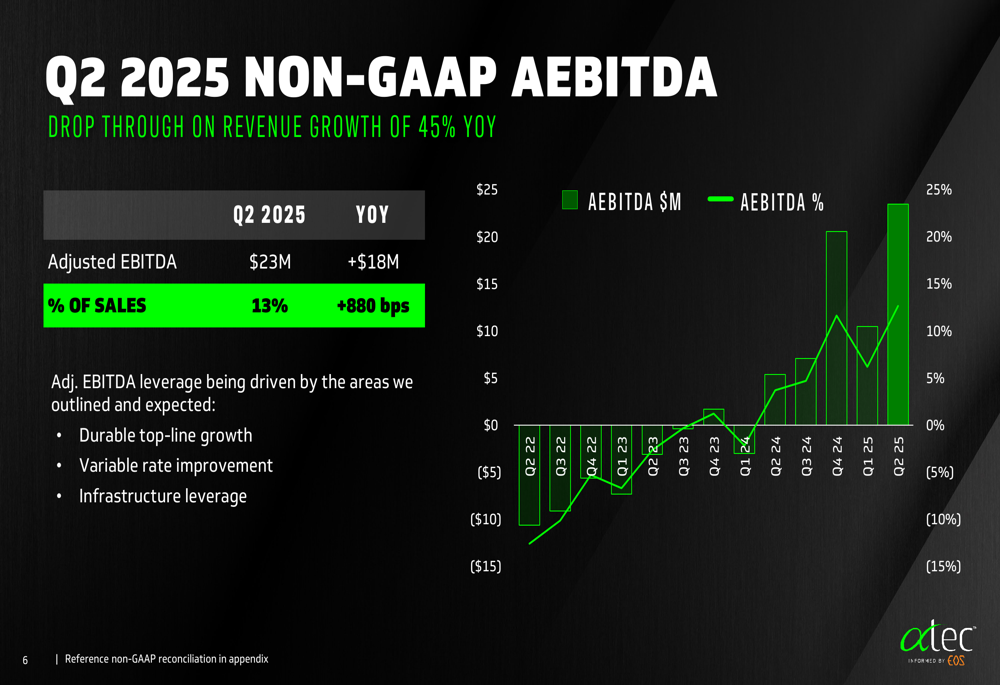

Adjusted EBITDA showed remarkable improvement, reaching $23 million or 13% of sales, an 880 basis point improvement year-over-year. The company reported a 45% drop-through on revenue growth to adjusted EBITDA, indicating efficient conversion of additional revenue into profit.

The following graph illustrates ATEC’s adjusted EBITDA trajectory:

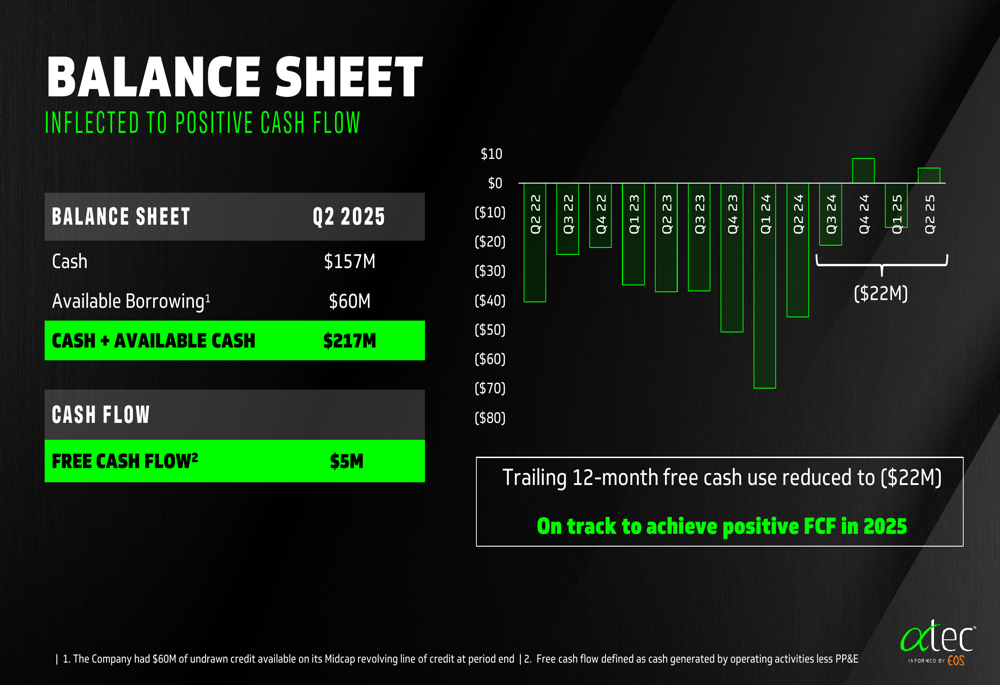

Perhaps most significantly, ATEC achieved positive free cash flow of $5 million in Q2 2025, marking a critical inflection point in the company’s financial journey. The company reported a strong cash position of $157 million, with an additional $60 million in available borrowing, bringing total cash and available cash to $217 million.

The cash flow trends are visualized in this slide:

Strategic Initiatives

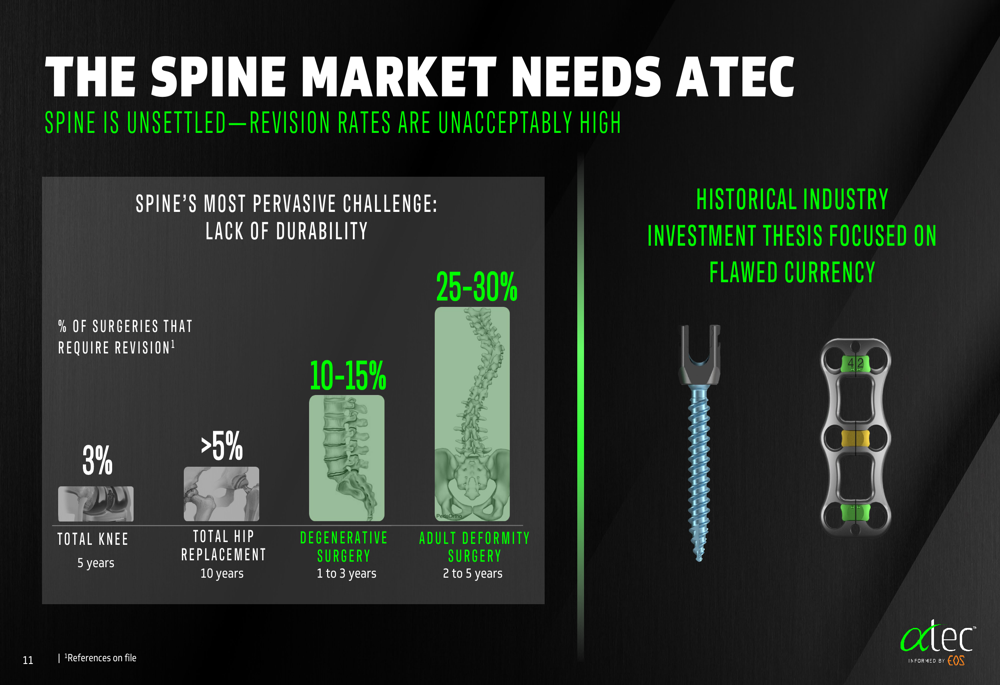

ATEC’s presentation emphasized its strategic focus on addressing what it describes as "spine’s most pervasive challenge" – the high revision rates in spine surgery compared to other orthopedic procedures. According to the company, 25-30% of adult deformity surgeries and 10-15% of degenerative surgeries require revision within 2-5 years and 1-3 years, respectively.

The company highlighted this market need through the following comparison:

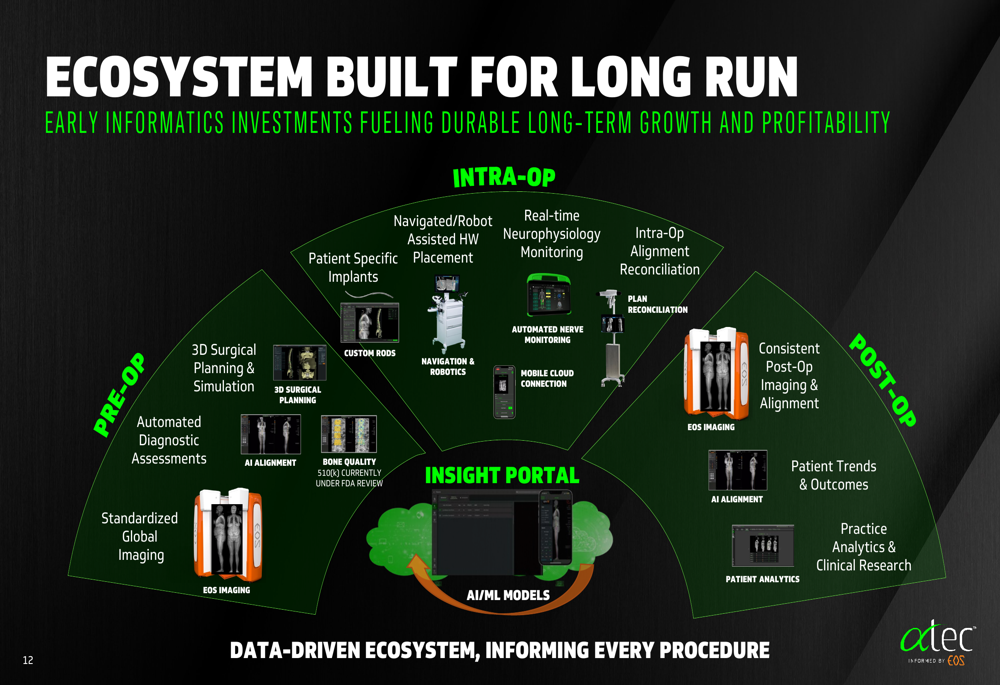

To address these challenges, ATEC has developed an integrated technology ecosystem spanning pre-operative, intra-operative, and post-operative phases of spine surgery. This ecosystem includes 3D surgical planning, automated diagnostic assessments, custom implants, navigation, and robotics, all designed to improve surgical outcomes.

The comprehensive nature of this ecosystem is illustrated here:

CEO Pat Miles emphasized the company’s differentiation through its 100% spine focus, contrasting with competitors who may have broader orthopedic portfolios. According to the earnings call transcript, Miles stated, "The spine market needs ATEC," and "We are just getting started. Our ecosystem has years to reflect in improvement and our best is truly yet to come."

Forward-Looking Statements

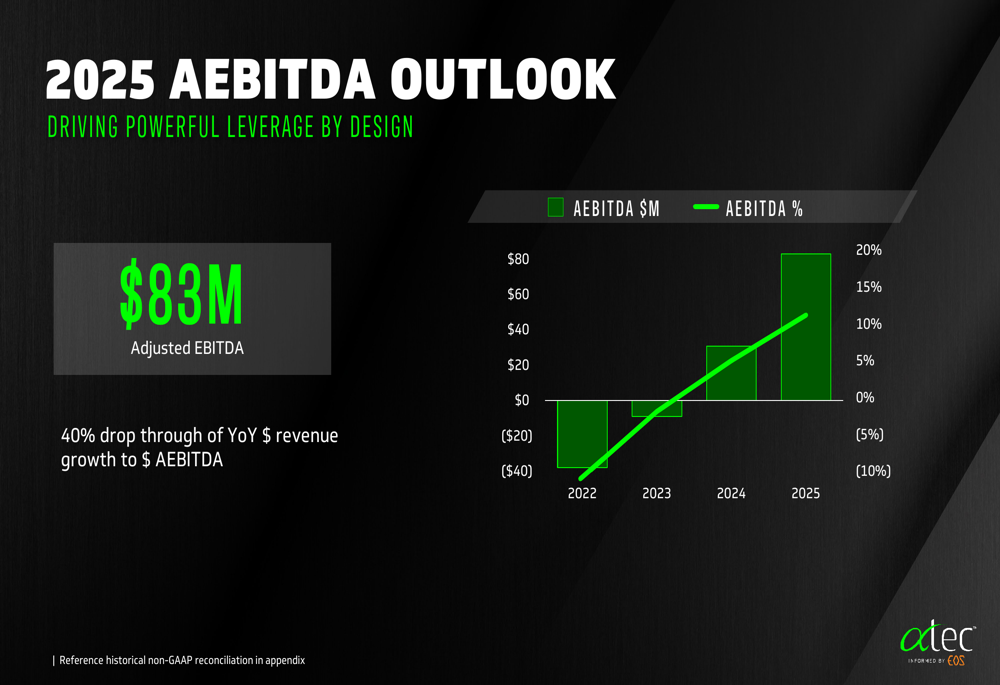

Looking ahead, ATEC provided a robust outlook for 2025, projecting total revenue of $742 million and adjusted EBITDA of $83 million, while maintaining positive free cash flow for the full year.

The company’s 2025 guidance is summarized in the following slide:

The adjusted EBITDA outlook shows continued improvement, with the company targeting a 40% drop-through of year-over-year revenue growth to adjusted EBITDA. This trajectory suggests ongoing operational efficiency and margin expansion:

According to the earnings article, ATEC has raised its full-year revenue guidance to $742 million, with surgical revenue projected at $666 million and EOS revenue at $76 million. The company has set a longer-term target of achieving an 18% adjusted EBITDA margin by 2027, with an ambitious goal of $1 billion in revenue.

Analyst sentiment appears positive, with price targets ranging from $14 to $23 per share, and four analysts recently revising earnings estimates upward. With year-to-date returns exceeding 50% and a market capitalization of $2.03 billion, ATEC has demonstrated significant momentum in the spine technology sector.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.