Street Calls of the Week

Introduction & Market Context

Alta Equipment Group Inc. (NYSE:ALTG) presented its first quarter 2025 earnings results on May 7, 2025, revealing a period of revenue challenges but highlighting improvements in service profitability and a significant shift in capital allocation strategy. The industrial equipment dealer, which operates across construction and material handling segments, reported results amid a challenging market environment that saw its stock decline 4.61% during regular trading hours, with after-market trading showing an additional 1.32% decrease.

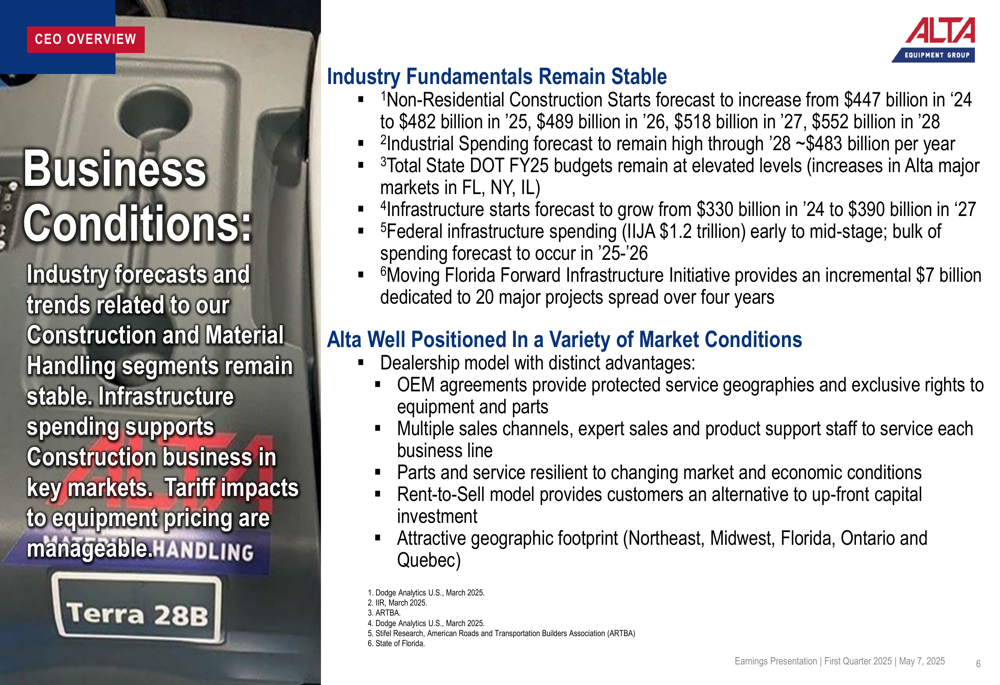

The company operates in a market with stable industry fundamentals, citing forecasts for non-residential construction starts to increase from $447 billion in 2024 to $552 billion by 2028, while industrial spending is expected to remain elevated at approximately $483 billion annually through 2028.

As shown in the following slide detailing business conditions, Alta believes it is well-positioned due to its dealership model, OEM agreements, multiple sales channels, and strategic geographic footprint:

Quarterly Performance Highlights

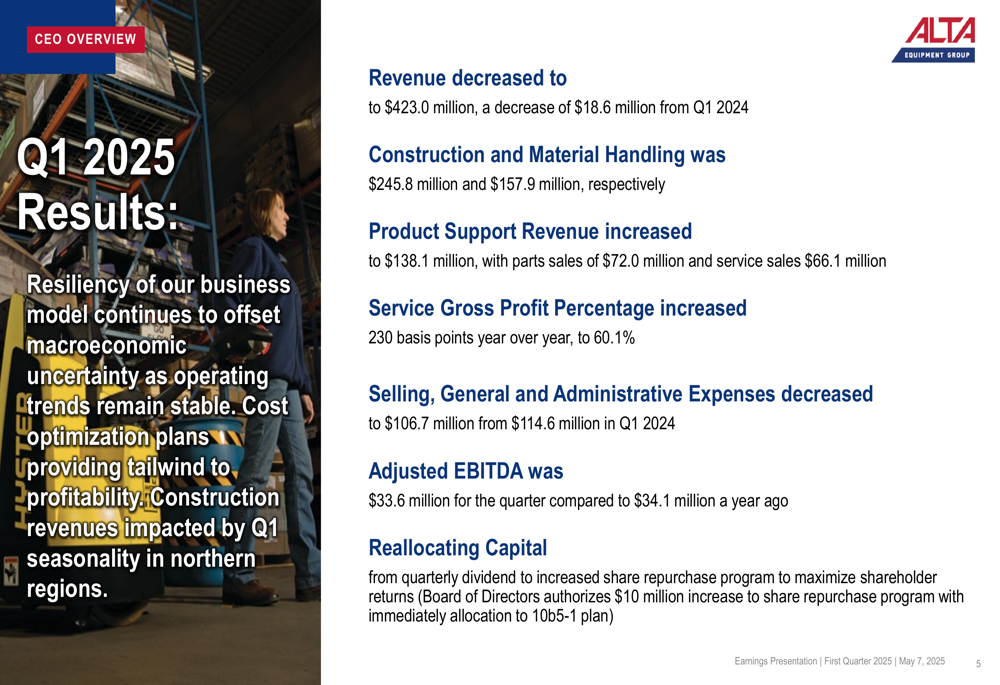

Alta Equipment reported total revenue of $423.0 million for Q1 2025, representing a decrease from the same period last year. Despite the overall revenue decline, the company achieved notable improvements in service profitability, with service gross profit percentage increasing 230 basis points to 60.1%. Product support revenue grew to $138.1 million, while selling, general and administrative expenses decreased to $106.7 million. The company reported adjusted EBITDA of $33.6 million for the quarter.

The following slide summarizes the key financial results for the first quarter:

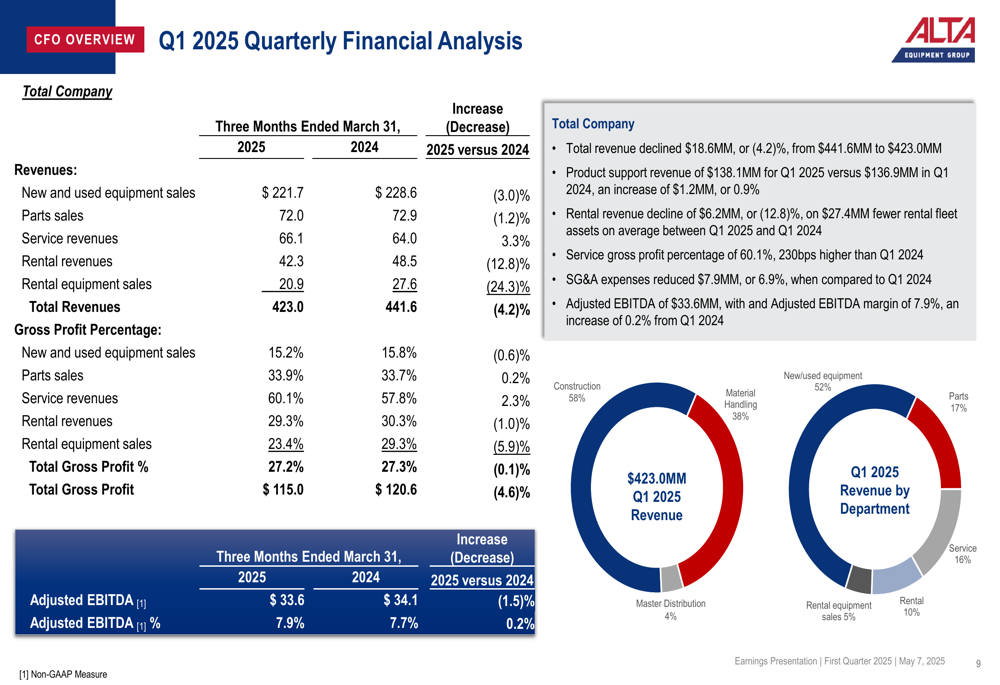

A more detailed breakdown of the quarterly financial performance shows the revenue distribution across different departments, with construction equipment representing 52% of total revenue, followed by material handling at 38%:

Segment Performance Analysis

Alta’s business is divided into three primary segments: Construction Equipment, Material Handling, and Master Distribution. Each segment showed varying performance during the quarter.

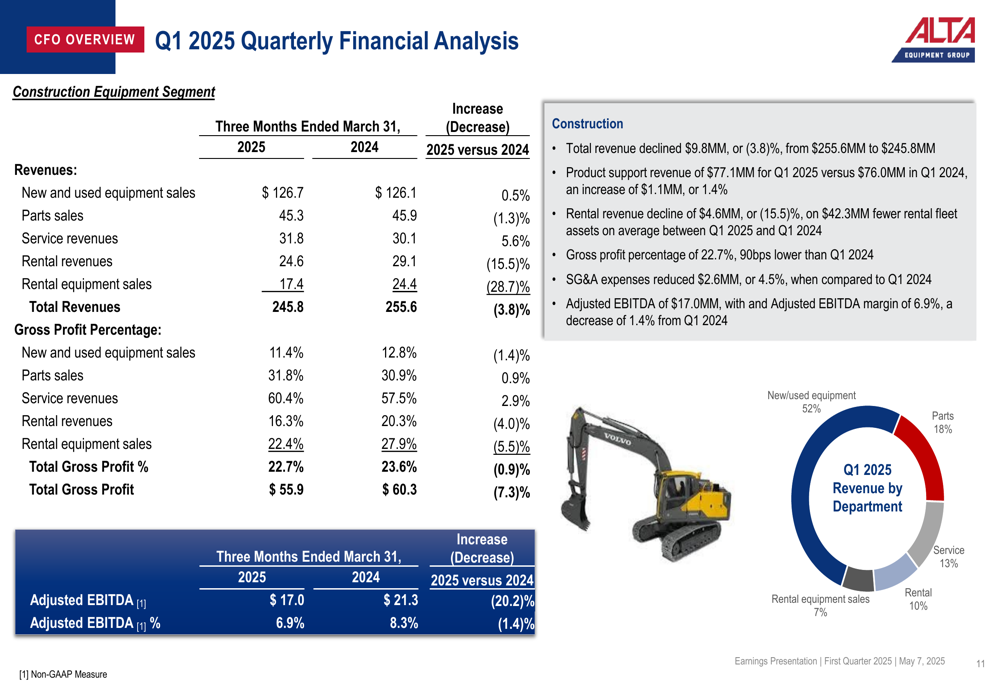

The Construction Equipment segment reported revenue of $245.8 million, a decline of $9.8 million compared to Q1 2024. This segment’s adjusted EBITDA was $17.0 million, with a gross profit percentage of 22.7%. New and used equipment sales accounted for 52% of this segment’s revenue, followed by parts (18%), service (13%), rental (10%), and rental equipment sales (7%).

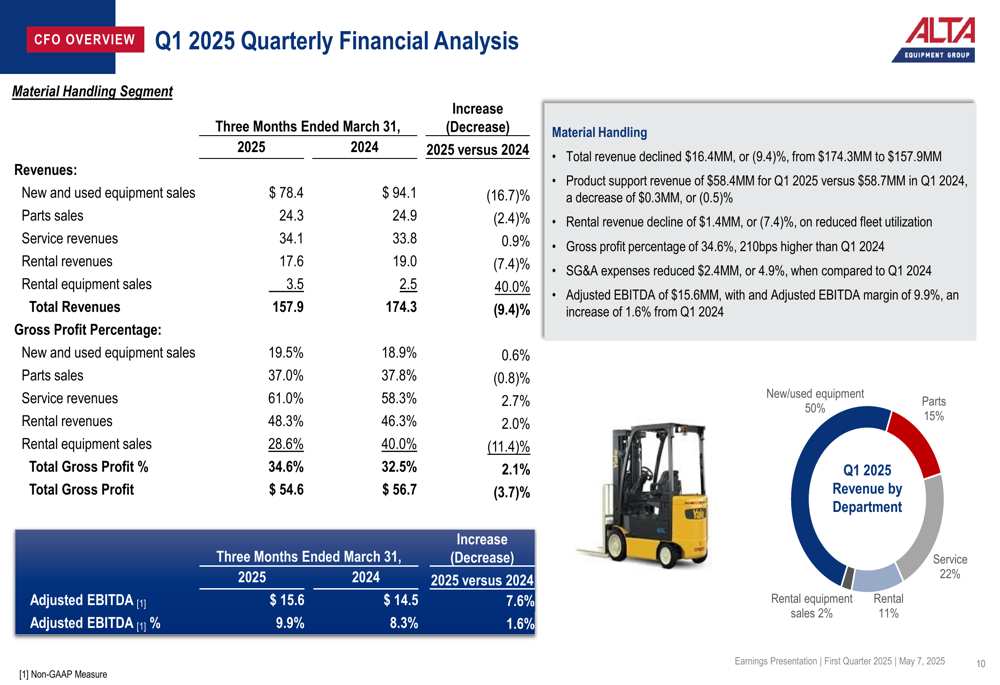

The Material Handling segment experienced a more significant revenue decline of $16.4 million to $157.9 million. However, this segment showed improved profitability with gross profit percentage increasing to 34.6%. Adjusted EBITDA for this segment was $15.6 million. The revenue breakdown shows new/used equipment sales at 50%, service at 22%, parts at 15%, rental at 11%, and rental equipment sales at 2%.

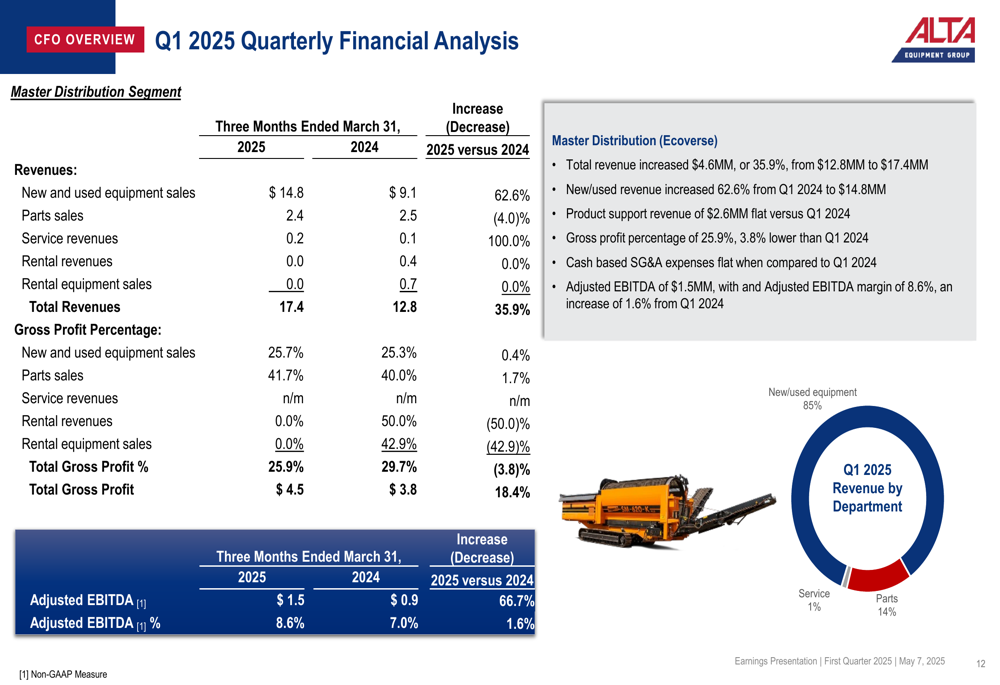

The Master Distribution segment was a bright spot, with total revenue increasing by $4.6 million to $17.4 million. New and used equipment revenue in this segment grew by an impressive 62.6% to $14.8 million, though gross profit percentage decreased to 25.9%. Adjusted EBITDA for this segment was $1.5 million.

Capital Structure and Allocation Strategy

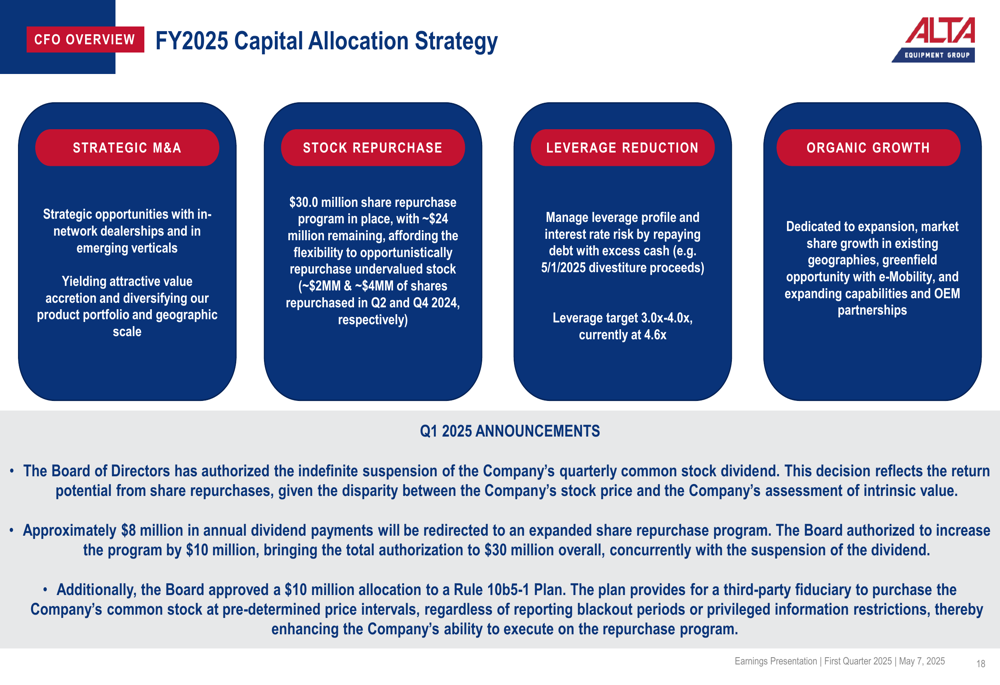

One of the most significant announcements in the presentation was Alta’s decision to indefinitely suspend its quarterly common stock dividend to redeploy approximately $8 million into an expanded stock repurchase program. The Board authorized a $10 million increase to the share repurchase program, signaling a strategic shift in capital allocation priorities.

The company’s capital allocation strategy for FY2025 focuses on four key areas: strategic M&A, stock repurchase, leverage reduction, and organic growth, as illustrated in the following slide:

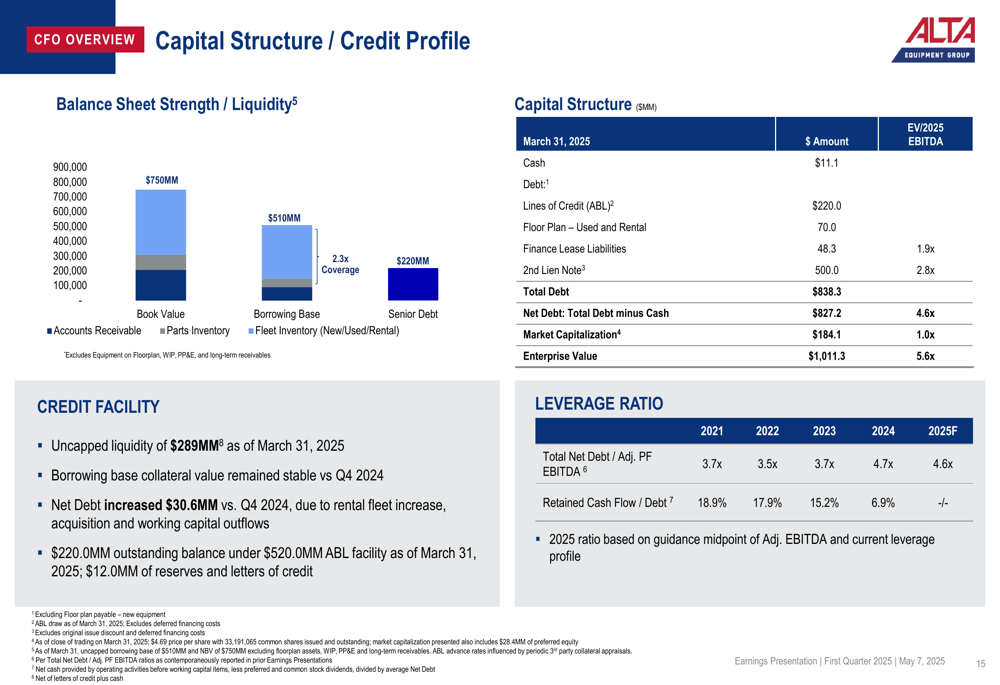

Alta’s capital structure includes total debt of $838.3 million as of March 31, 2025, with cash of $11.1 million. The company reported net debt increased by $30.6 million compared to Q4 2024. The following slide details the company’s capital structure and credit profile:

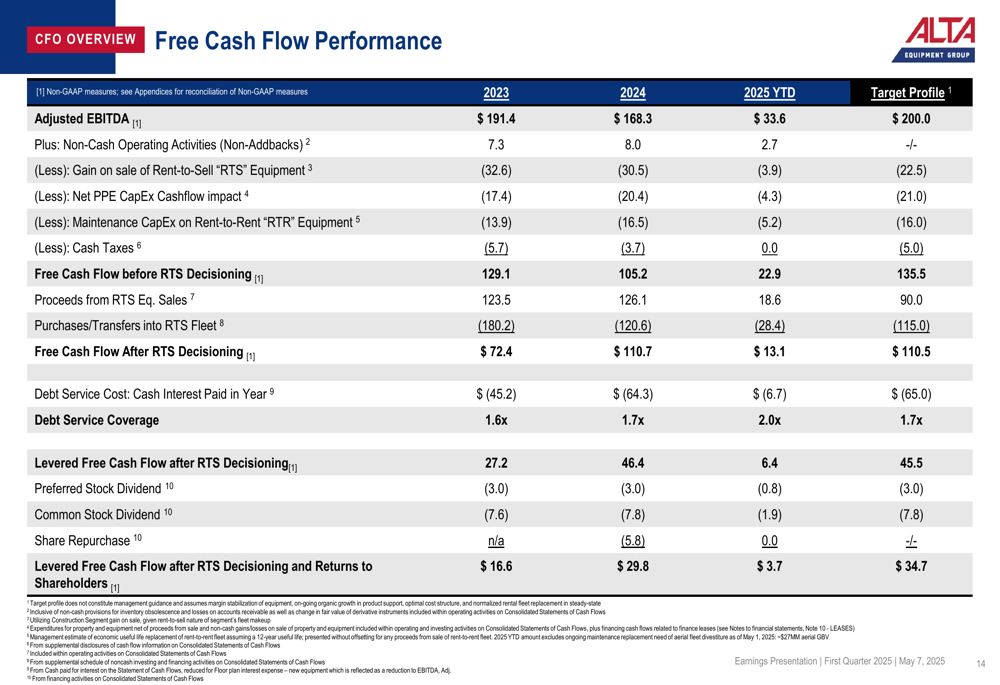

The company also highlighted its free cash flow performance, showing $13.1 million in free cash flow after RTS (Rent-to-Sell) decisioning for Q1 2025, compared to $110.7 million for the full year 2024:

Forward-Looking Statements

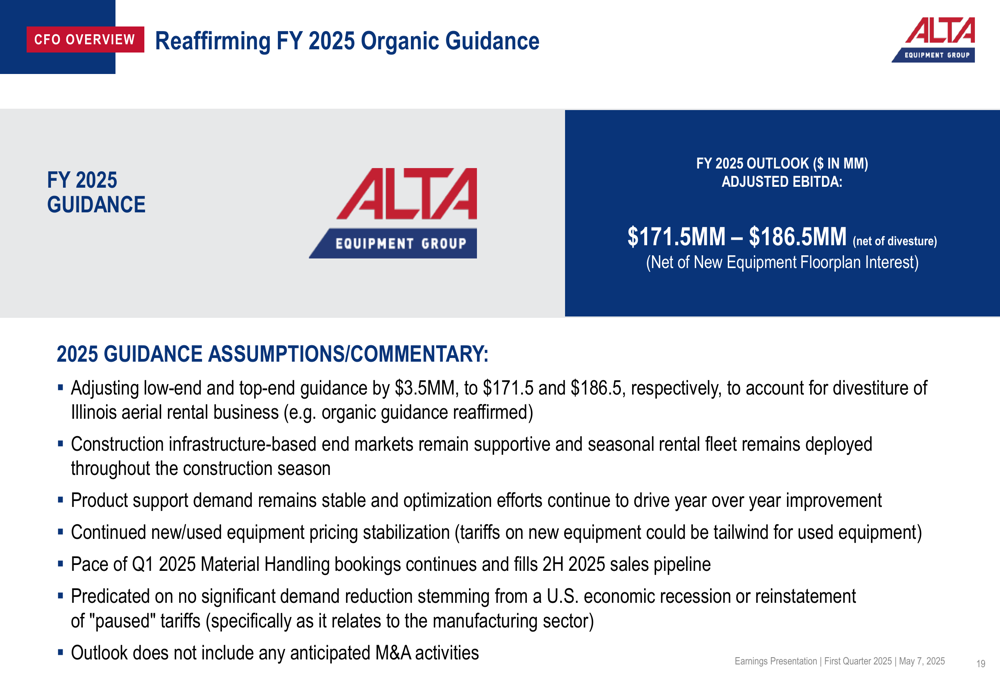

Alta Equipment Group reaffirmed its FY 2025 organic guidance, projecting adjusted EBITDA between $171.5 million and $186.5 million (net of divestiture and new equipment floorplan interest). This guidance is based on several assumptions, including supportive end markets, stable product support demand, continued pricing stabilization, and no significant demand reduction.

The company’s projections represent a modest improvement from the $168.3 million in adjusted EBITDA reported for 2024, suggesting cautious optimism about recovery in the coming quarters despite current challenges.

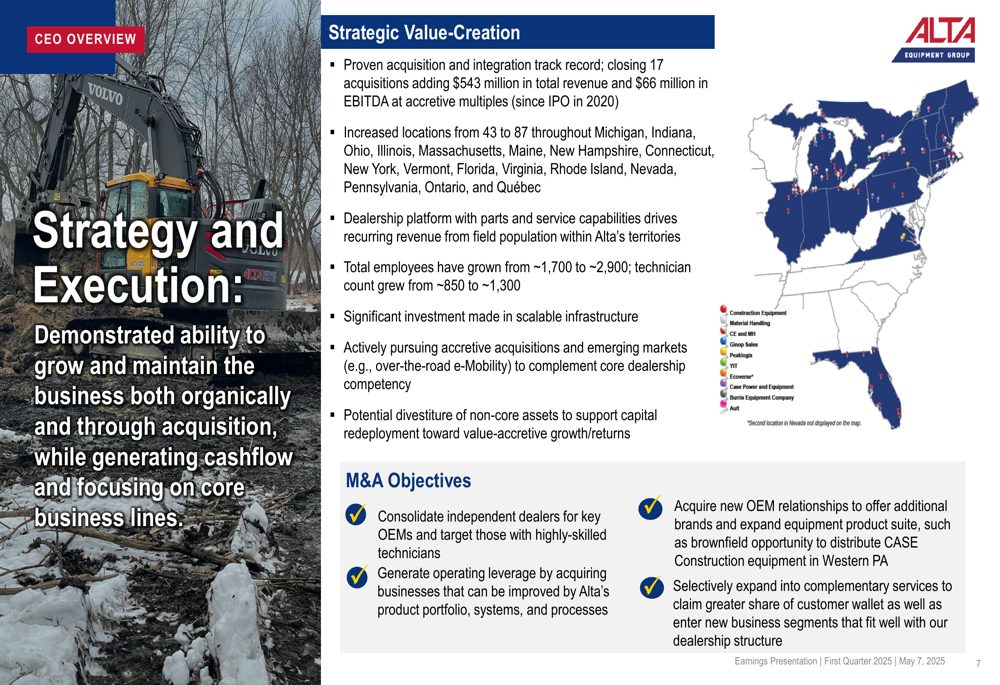

Alta’s strategy for long-term value creation continues to emphasize its proven acquisition and integration track record, with 17 acquisitions completed to date and an expansion from 43 to 87 locations. The company remains focused on consolidating independent dealers, generating operating leverage, acquiring new OEM relationships, and expanding into complementary services.

Despite the revenue challenges in Q1 2025, Alta Equipment Group’s presentation emphasized its diversified business model, improved service profitability, and strategic capital allocation as key factors that position the company to navigate the current market environment while pursuing long-term growth opportunities.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.