Street Calls of the Week

Advanced Micro Devices (NASDAQ:AMD) reported record first-quarter revenue and substantial growth across its key business segments, according to the company’s Q1 2025 financial results presentation released on May 6, 2025. The semiconductor giant also completed its acquisition of ZT Systems while warning of a significant inventory charge in the coming quarter due to new export controls.

Quarterly Performance Highlights

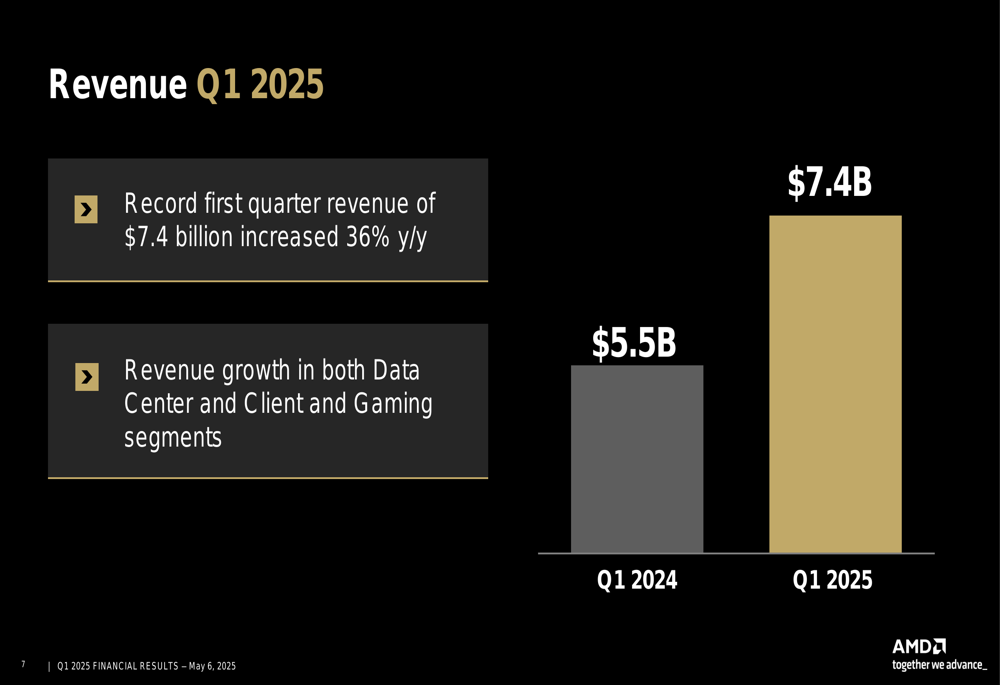

AMD delivered record first-quarter revenue of $7.4 billion, representing a 36% year-over-year increase from $5.5 billion in Q1 2024. This strong performance was primarily driven by significant growth in the company’s Data Center and Client & Gaming segments.

As shown in the following revenue chart, AMD’s Q1 2025 performance continues its growth trajectory:

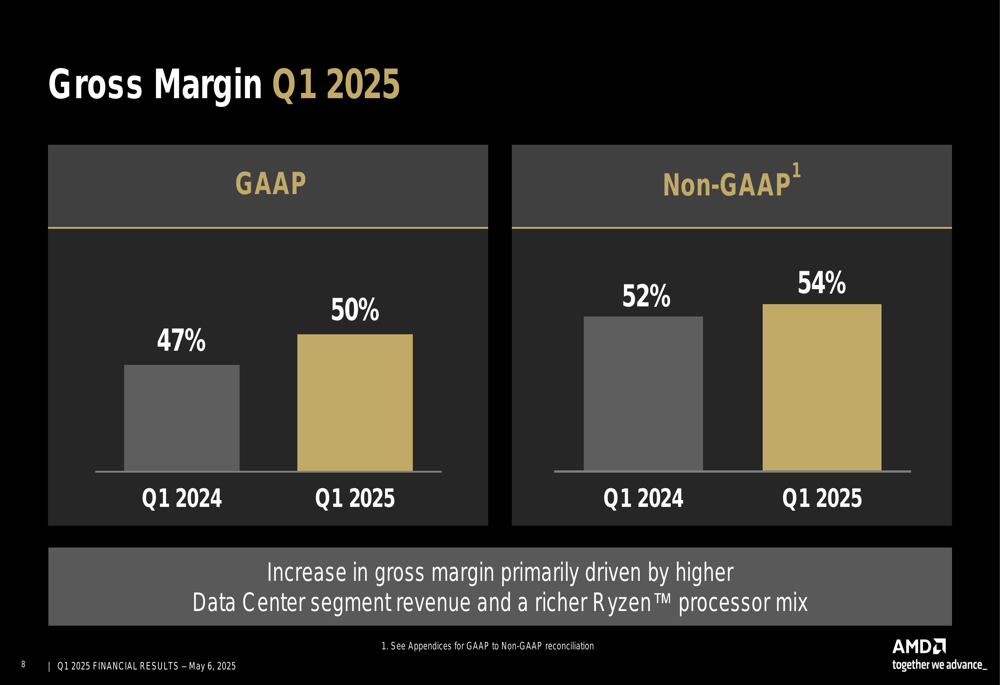

The company’s profitability metrics also showed substantial improvement. AMD reported a GAAP gross margin of 50%, up 3 percentage points year-over-year, while non-GAAP gross margin reached 54%, up 2 percentage points from the prior year. This margin expansion was attributed to higher Data Center segment revenue and a richer Ryzen processor mix.

The following chart illustrates AMD’s gross margin improvement:

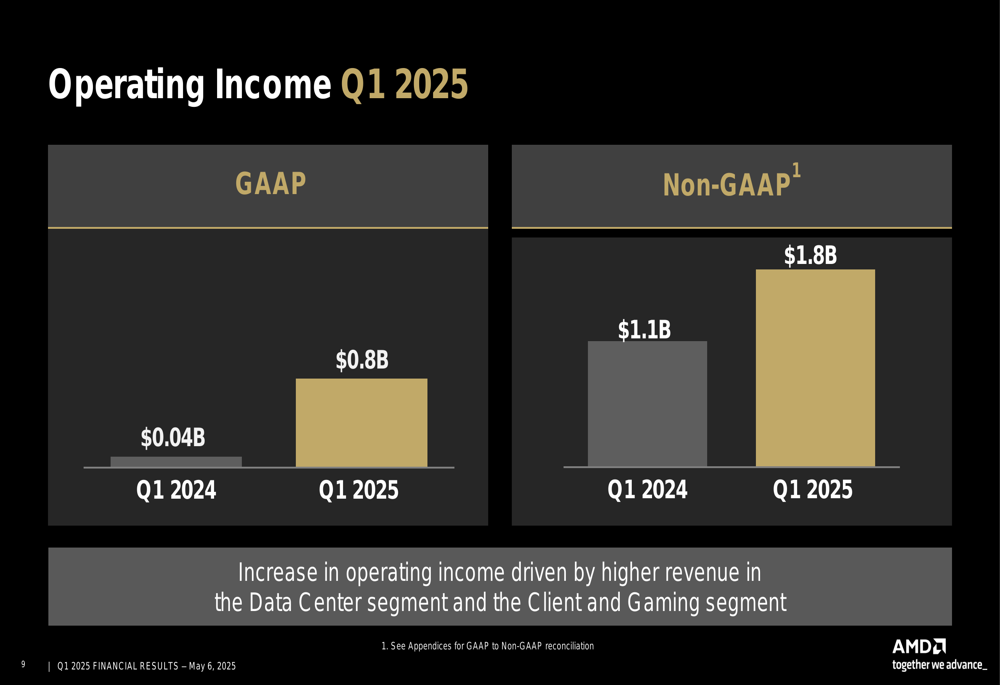

Operating income saw dramatic improvement, with GAAP operating income reaching $806 million, up 2,139% year-over-year, while non-GAAP operating income increased 57% to $1.779 billion. This growth was primarily driven by higher revenue in both the Data Center and Client & Gaming segments.

The operating income growth is visualized in the following chart:

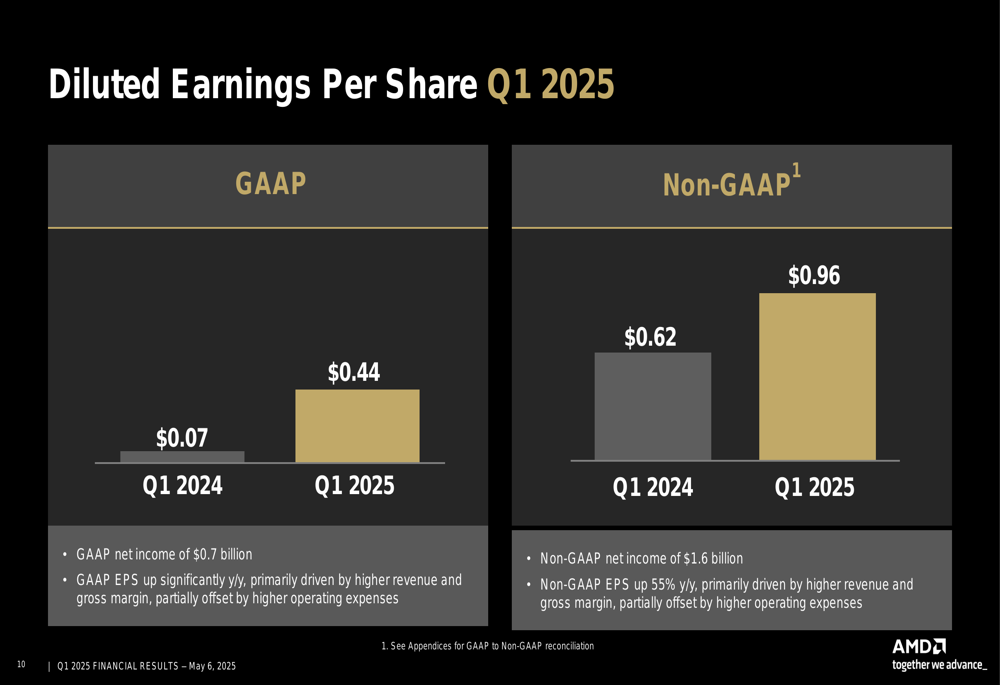

Earnings per share also showed remarkable growth, with GAAP diluted EPS of $0.44, up 529% year-over-year, and non-GAAP diluted EPS of $0.96, up 55% from Q1 2024.

The following chart demonstrates AMD’s EPS performance:

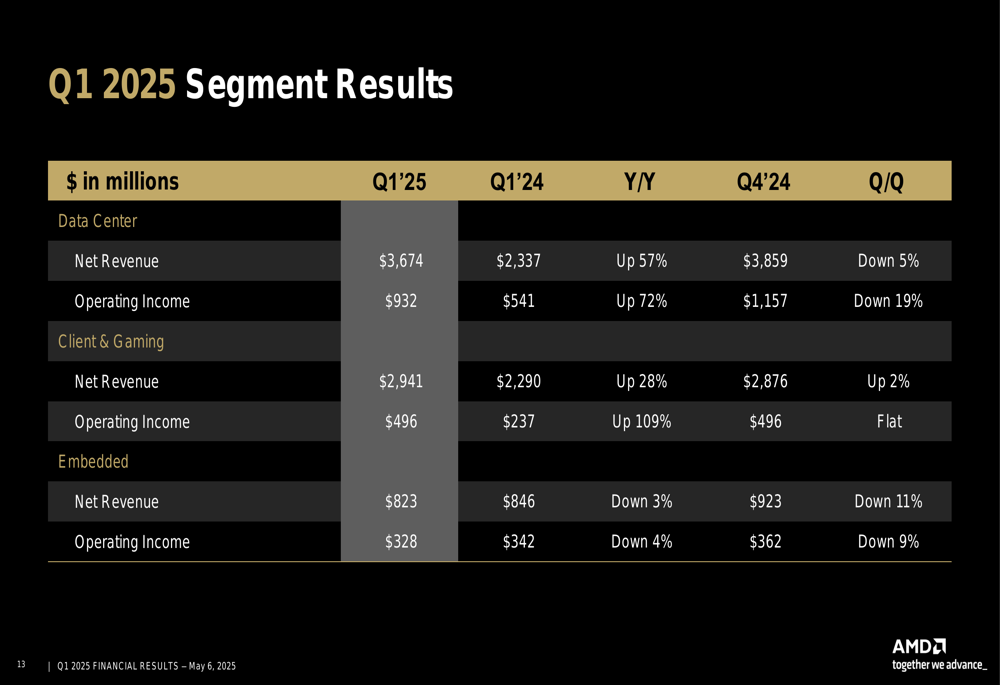

Segment Analysis

AMD’s performance varied across its three business segments, with Data Center and Client & Gaming showing strong growth while the Embedded segment experienced a slight decline.

The following segment breakdown provides a detailed view of AMD’s performance across its business units:

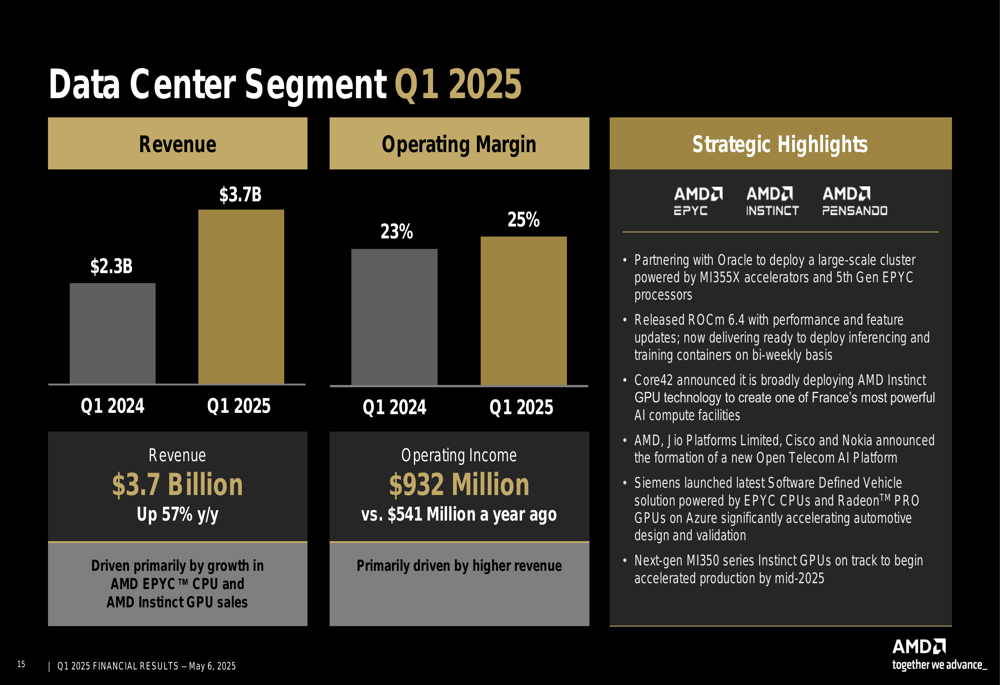

Data Center Segment

The Data Center segment was AMD’s standout performer, with revenue of $3.674 billion, up 57% year-over-year, and operating income of $932 million, up 72% from Q1 2024. The segment’s operating margin improved from 23% to 25%, driven primarily by growth in AMD EPYC CPU and AMD Instinct GPU sales.

Strategic highlights for the Data Center segment included partnerships with Oracle (NYSE:ORCL) to deploy a large-scale cluster powered by MI355X accelerators and 5th Gen EPYC processors, and with Core42 to create one of France’s most powerful AI compute facilities. AMD also announced that its next-generation M1350 series Instinct GPUs are on track to begin accelerated production by mid-2025.

The following slide details the Data Center segment’s performance and initiatives:

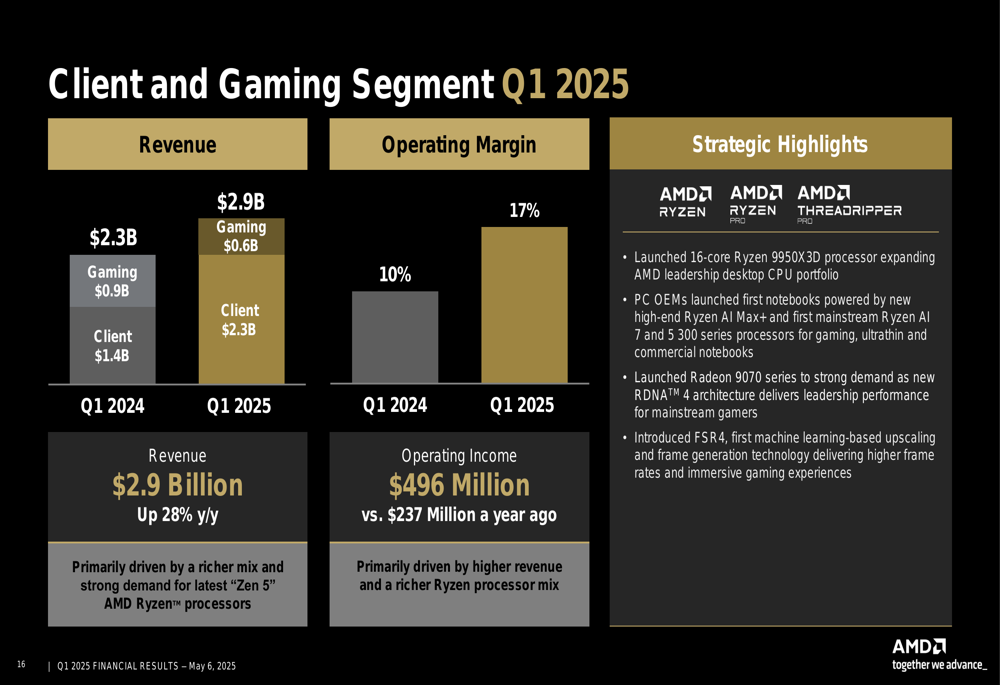

Client and Gaming Segment

The Client and Gaming segment also delivered strong results, with revenue of $2.941 billion, up 28% year-over-year, and operating income of $496 million, more than double the $237 million reported in Q1 2024. The segment’s operating margin improved significantly from 10% to 17%, primarily driven by a richer mix and strong demand for the latest "Zen 5" AMD Ryzen processors.

Key product launches in this segment included the 16-core Ryzen 9950X3D processor and the Radeon 9070 series, which reportedly saw strong demand. AMD also introduced FSR4, its first machine learning-based upscaling and frame generation technology for gaming.

The following slide highlights the Client and Gaming segment’s performance:

Embedded Segment

The Embedded segment was the only area showing a slight decline, with revenue of $823 million, down 3% year-over-year, and operating income of $328 million, down 4% from Q1 2024. The segment’s operating margin decreased slightly from 41% to 40%, primarily due to mixed end market demand.

Despite the revenue decline, AMD highlighted several strategic initiatives in this segment, including AWS launching new FPGA-accelerated instances powered by EPYC processors with AMD Virtex FPGAs, and the launch of EPYC Embedded 9005 series processors.

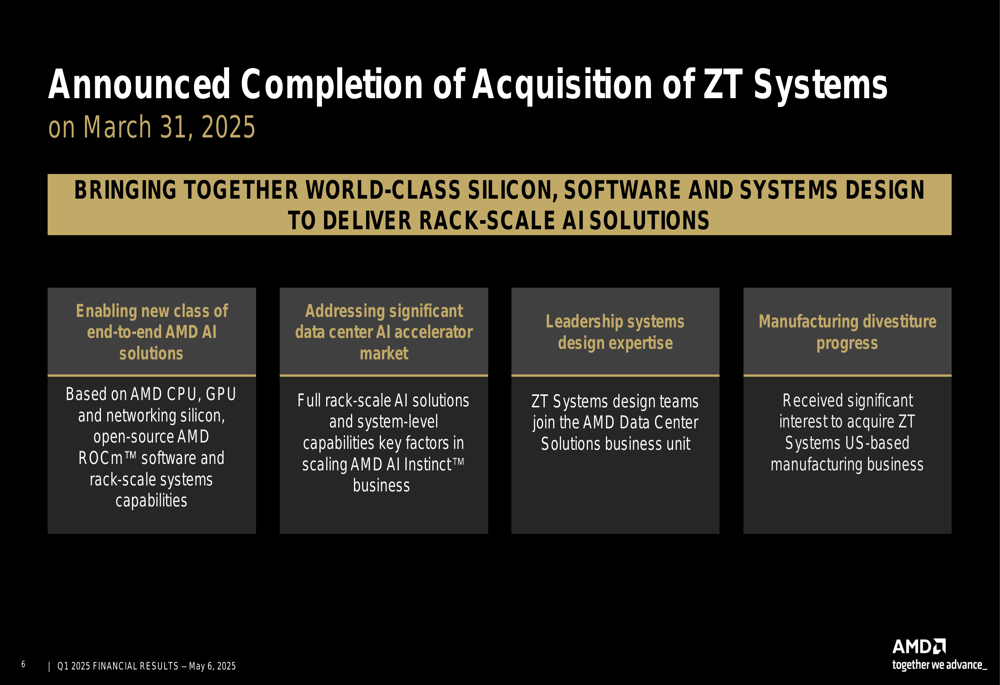

Strategic Initiatives and Acquisition

A significant development in Q1 2025 was AMD’s completion of the ZT Systems acquisition on March 31, 2025. This acquisition aims to bring together world-class silicon, software, and systems design to deliver rack-scale AI solutions.

According to AMD, the acquisition will enable a new class of end-to-end AMD AI solutions based on AMD CPU, GPU, networking silicon, open-source AMD ROCM software, and rack-scale systems capabilities. It will also help AMD address the significant data center AI accelerator market with full rack-scale AI solutions and system-level capabilities.

The following slide outlines the strategic rationale for the ZT Systems acquisition:

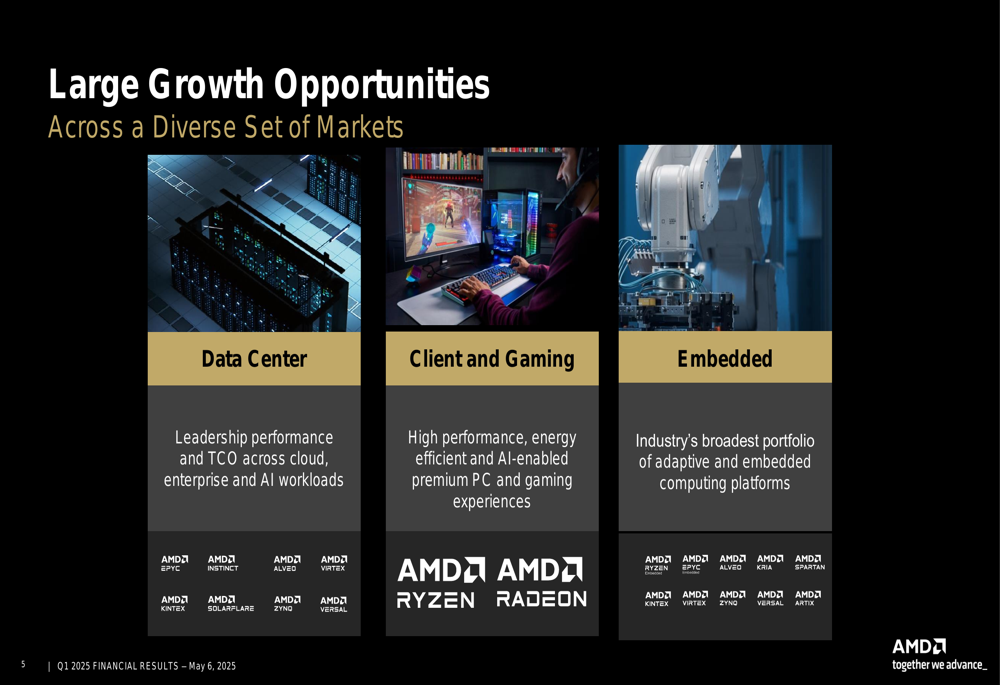

AMD also highlighted its broader strategic focus on high-performance and adaptive computing leadership, emphasizing four key areas: leadership foundational IP, breadth and depth of portfolio, open and proven software ecosystem, and deep collaborative partnerships.

The company sees large growth opportunities across diverse markets, as illustrated in the following slide:

Forward Guidance and Challenges

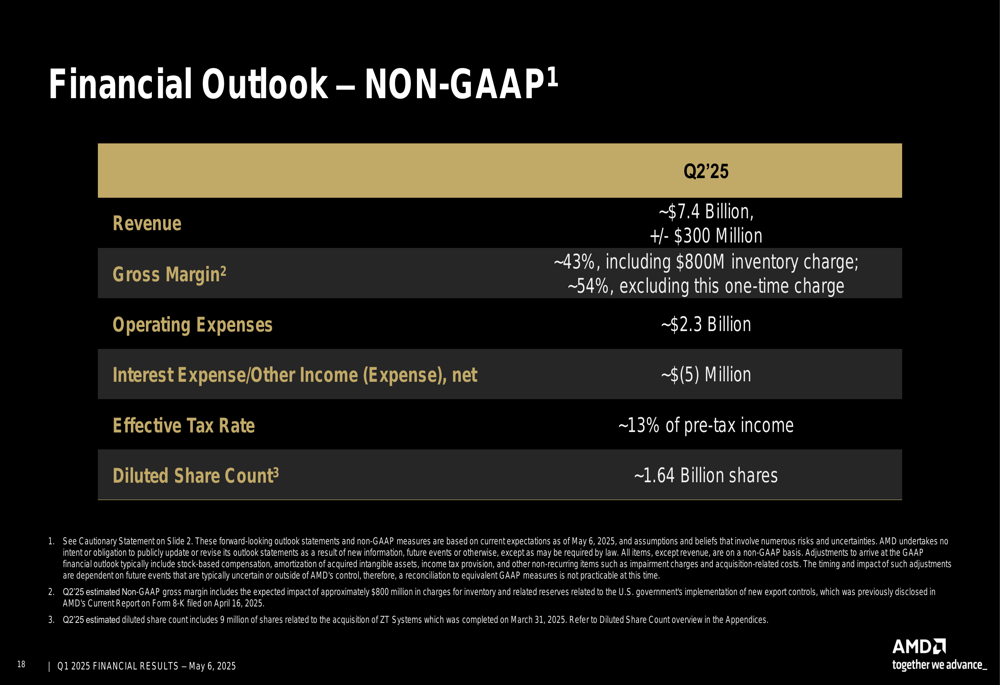

Looking ahead to Q2 2025, AMD provided a non-GAAP financial outlook with revenue projected at approximately $7.4 billion (±$300 million). However, the company warned of a significant impact on gross margin due to new export controls, with an expected $800 million charge for inventory and related reserves.

Excluding this one-time charge, AMD expects a non-GAAP gross margin of approximately 54%, but including the charge, the gross margin is projected to be around 43%. Operating expenses are expected to be approximately $2.3 billion, with an effective tax rate of about 13% of pre-tax income.

The following slide details AMD’s financial outlook for Q2 2025:

After the earnings release, AMD’s stock rose 5.09% in after-hours trading, suggesting that investors responded positively to the company’s strong performance despite the warning about the inventory charge.

AMD’s Q1 2025 results demonstrate the company’s continued momentum in the high-performance computing and AI markets, with particularly strong performance in the Data Center segment. While the company faces challenges related to export controls and mixed demand in the Embedded segment, its overall trajectory remains positive, supported by strategic acquisitions and product innovations.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.