Moody’s downgrades Senegal to Caa1 amid rising debt concerns

Amerant Bancorp Inc. (NASDAQ:NYSE:AMTB) presented its second-quarter 2025 earnings results on July 24, showing significant improvement across key performance metrics compared to the previous quarter. The bank’s shares closed at $20.12 on July 23, up 0.85% ahead of the presentation, and have recovered substantially from their post-Q1 earnings decline when the stock dropped 11.5% after missing EPS expectations.

Quarterly Performance Highlights

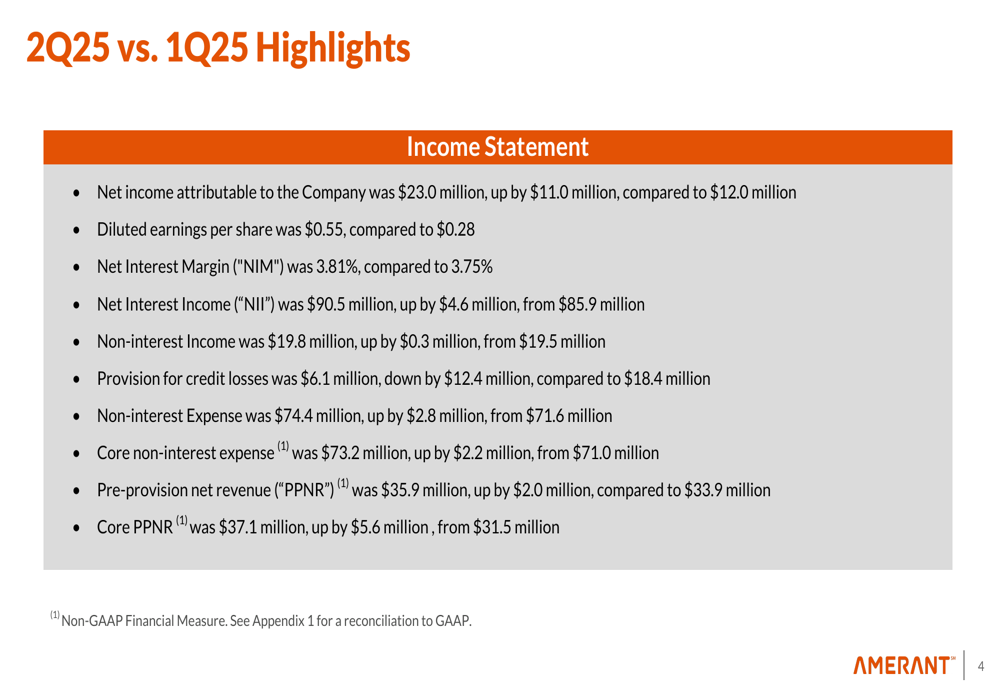

Amerant reported net income of $23.0 million for Q2 2025, nearly doubling from $12.0 million in Q1. Diluted earnings per share reached $0.55, a dramatic improvement from $0.28 in the previous quarter, demonstrating the bank’s strong recovery after missing analyst expectations in Q1.

As shown in the following income statement highlights, the bank improved across multiple performance metrics:

Net interest income increased to $90.5 million, up $4.6 million from Q1, while the net interest margin expanded to 3.81% from 3.75%. This outperformed the bank’s previous guidance of NIM in the "mid-360s" for Q2 that was mentioned in their Q1 earnings call.

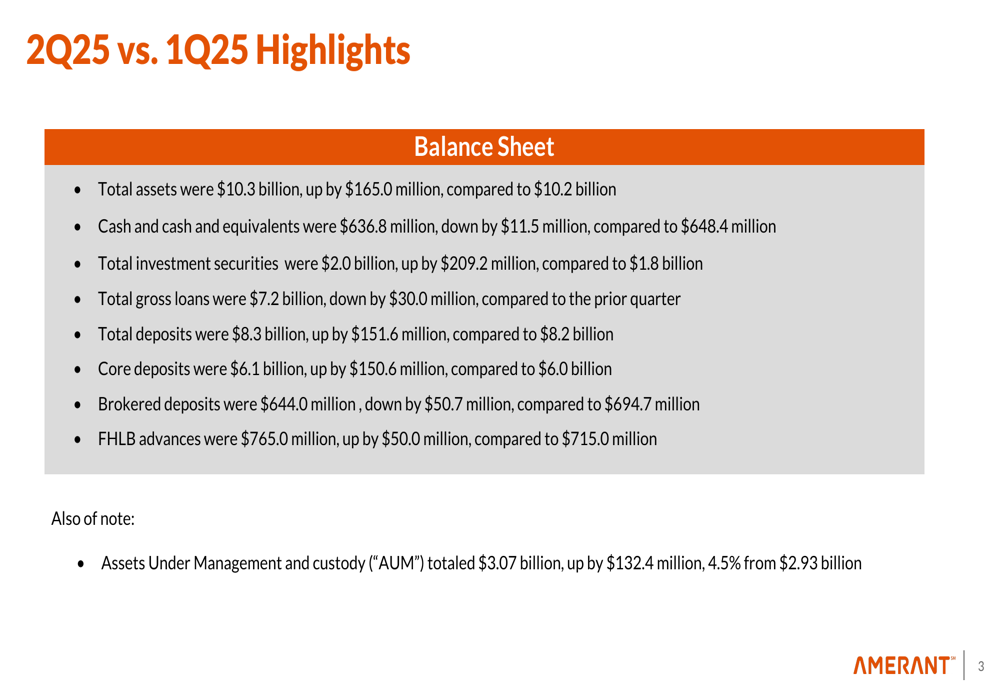

The bank’s balance sheet also showed positive trends, with total assets growing to $10.3 billion, up $165 million from the previous quarter:

Notably, total deposits increased by $151.6 million to $8.3 billion, with core deposits growing by $150.6 million to $6.1 billion. This deposit growth is particularly important as the bank continues to focus on relationship banking and reducing reliance on brokered deposits, which decreased by $50.7 million during the quarter.

Asset Quality Improvements

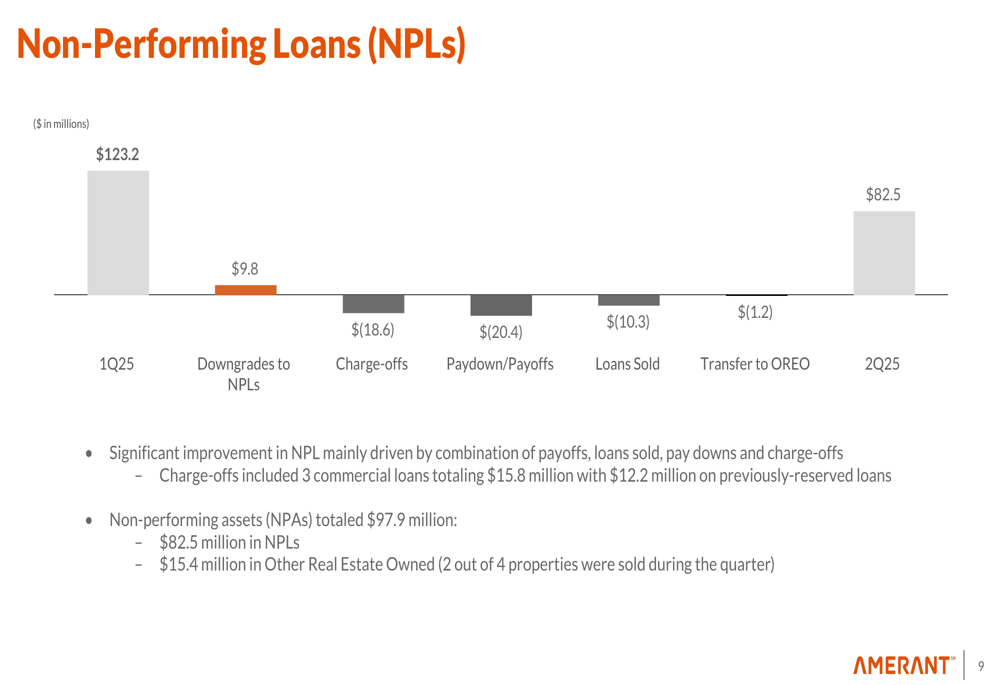

One of the most significant improvements in Q2 was the substantial reduction in non-performing loans, which decreased by $40.7 million to $82.5 million:

This improvement was driven by a combination of payoffs, loans sold, paydowns, and charge-offs. The bank’s provision for credit losses decreased significantly to $6.1 million from $18.4 million in Q1, reflecting improved credit conditions.

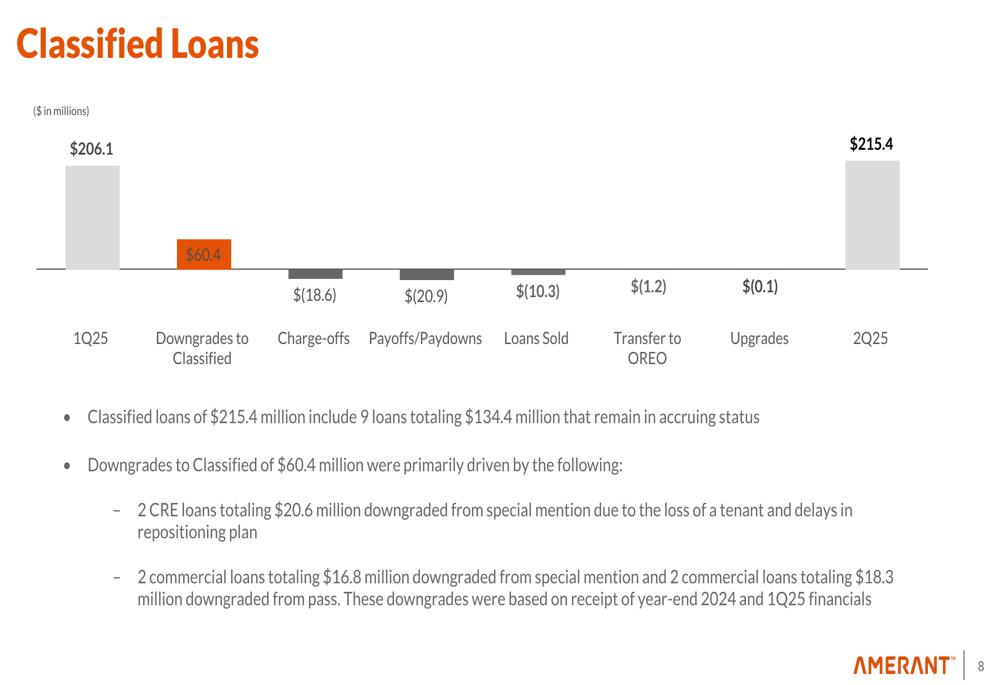

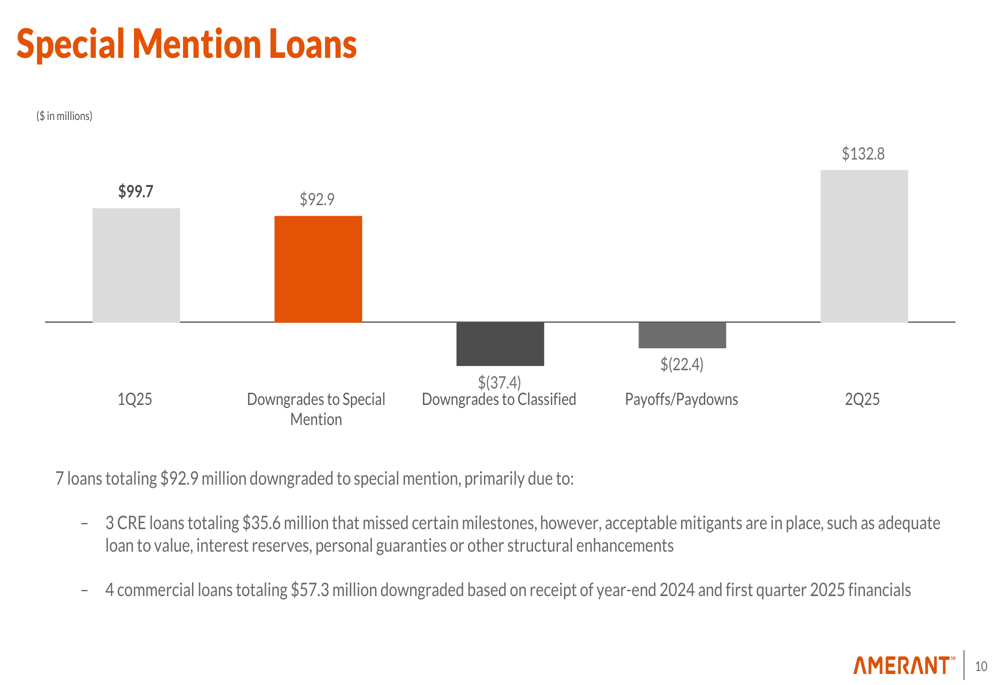

However, classified loans increased slightly to $215.4 million from $206.1 million, primarily due to downgrades:

Special mention loans also increased to $132.8 million from $99.7 million, with seven loans totaling $92.9 million downgraded to special mention during the quarter:

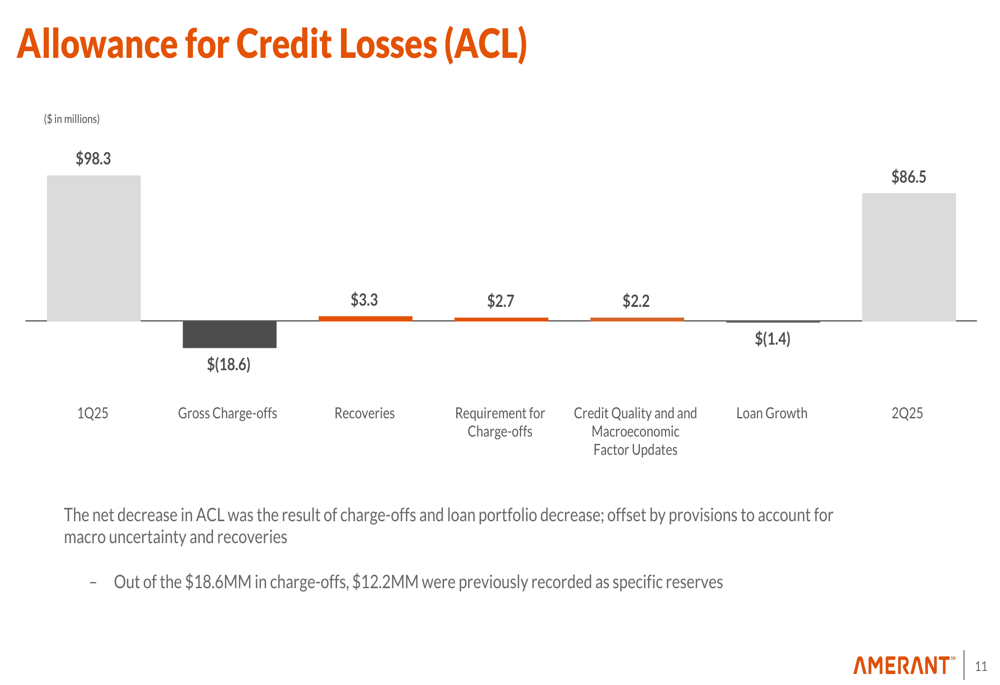

The allowance for credit losses decreased to $86.5 million from $98.3 million, primarily due to charge-offs and loan portfolio decrease, partially offset by provisions for macroeconomic uncertainty and recoveries:

Capital and Profitability Metrics

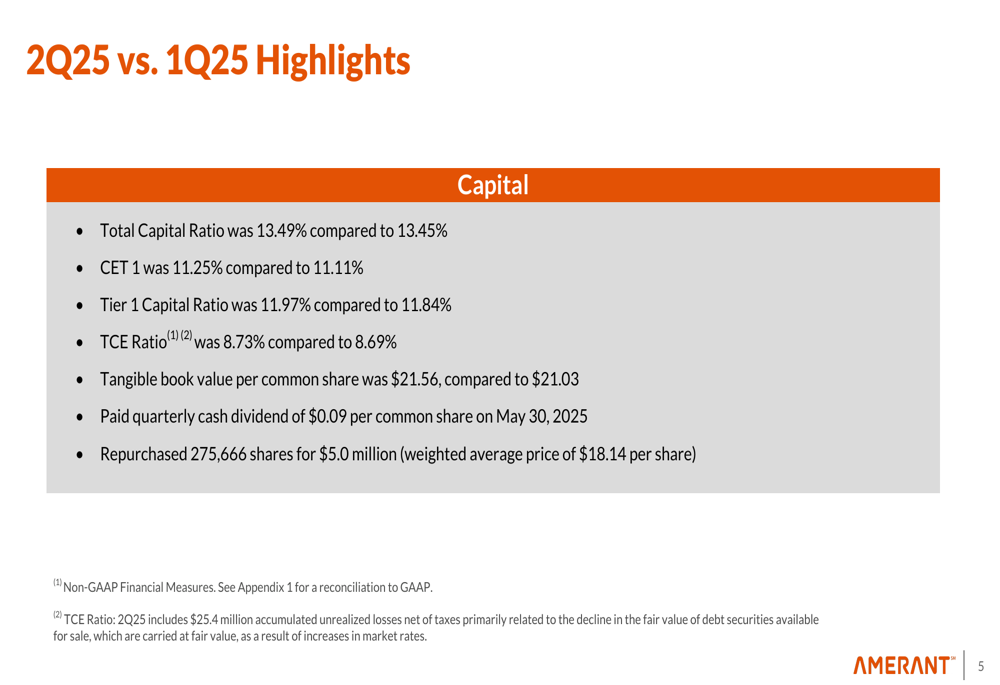

Amerant’s capital position strengthened during the quarter, with all key capital ratios showing improvement:

The bank’s tangible book value per common share increased to $21.56 from $21.03, while maintaining its quarterly cash dividend of $0.09 per share. Additionally, the bank repurchased 275,666 shares for $5.0 million at an average price of $18.14 per share, demonstrating confidence in its financial position.

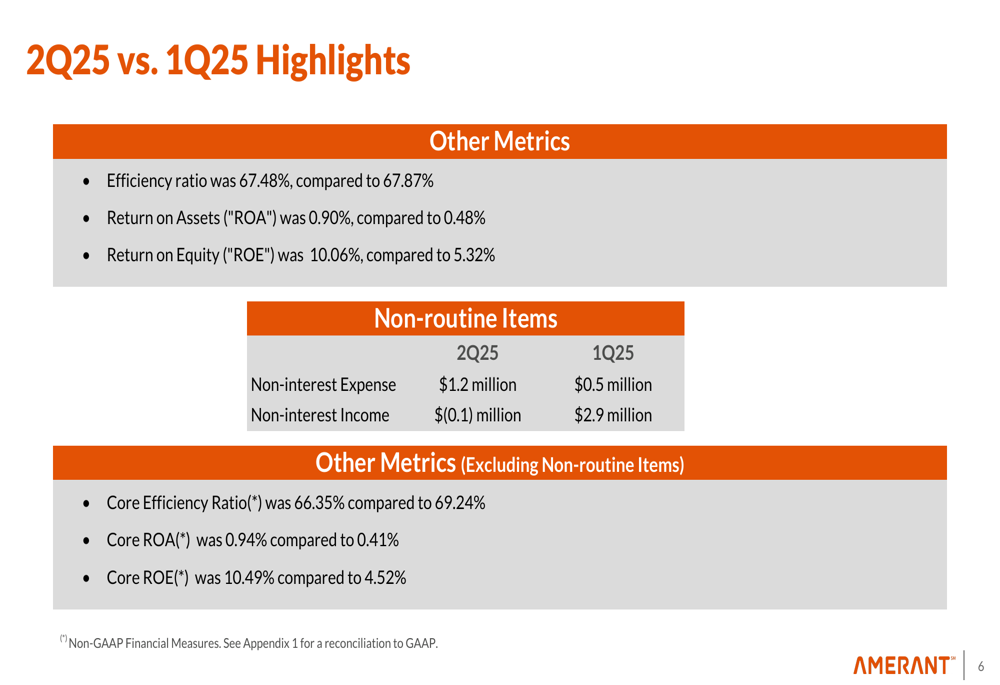

Profitability metrics showed substantial improvement, with return on assets (ROA) nearly doubling to 0.90% from 0.48% and return on equity (ROE) increasing to 10.06% from 5.32%:

This improvement brings the bank closer to its previously stated goal of achieving a 1% ROA in the latter half of 2025, as mentioned in their Q1 earnings call.

Strategic Initiatives and Expansion

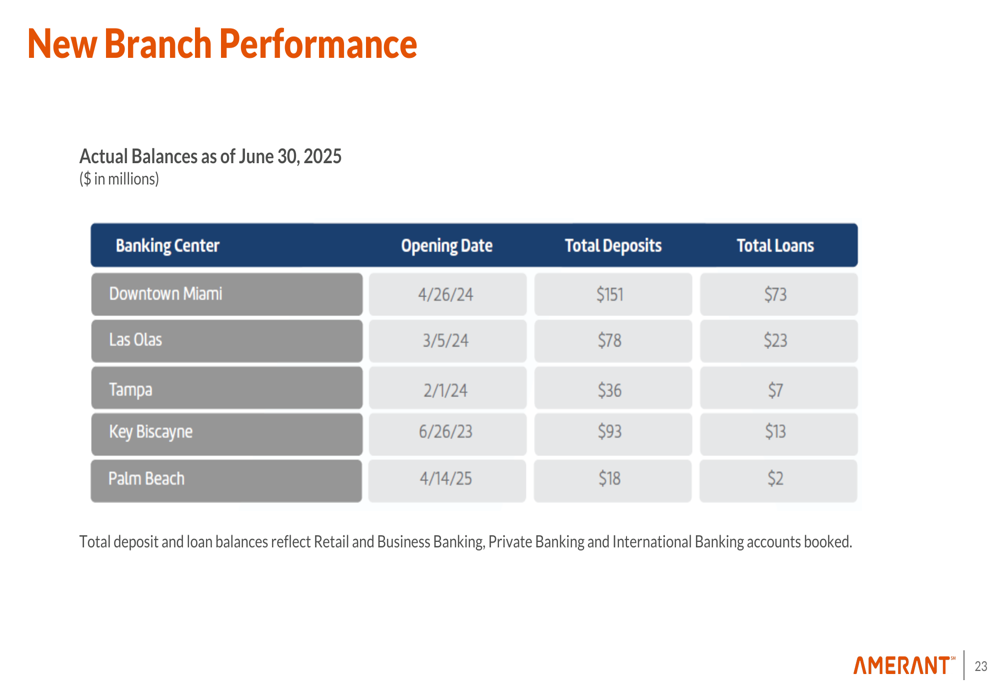

Amerant continues to focus on its strategic expansion in Florida, with new branches showing promising results:

The bank’s presentation highlighted its branch opening schedule, with new locations planned in Miami Beach and Downtown Tampa in Q3 2025, Bay Harbor Islands in Q4 2025, and Central Ave St. Petersburg in Q2 2026, along with an expansion of its Key Biscayne space.

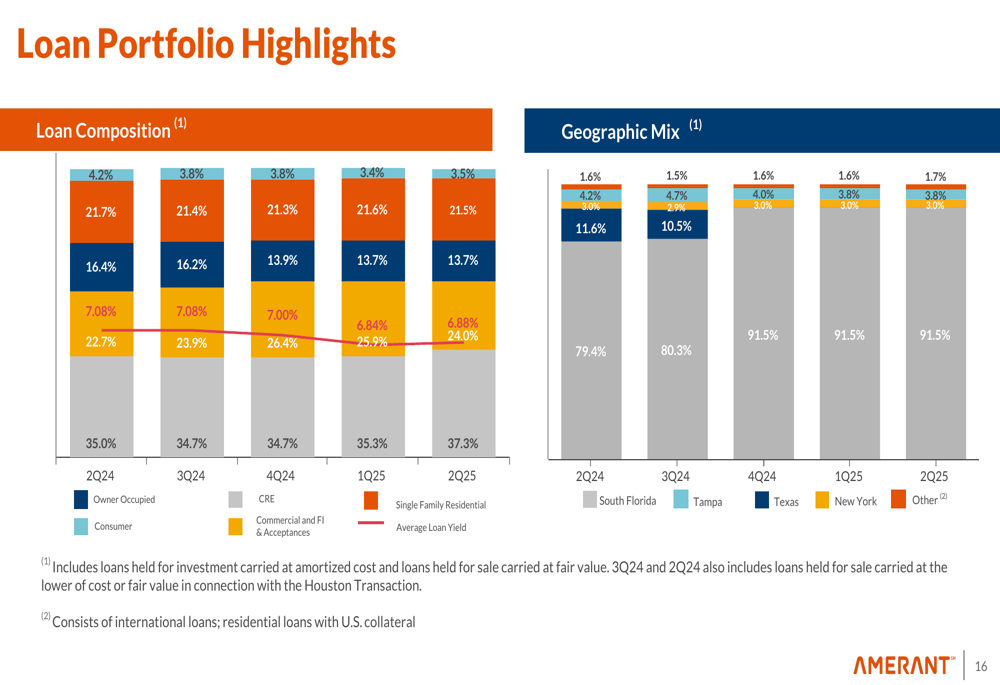

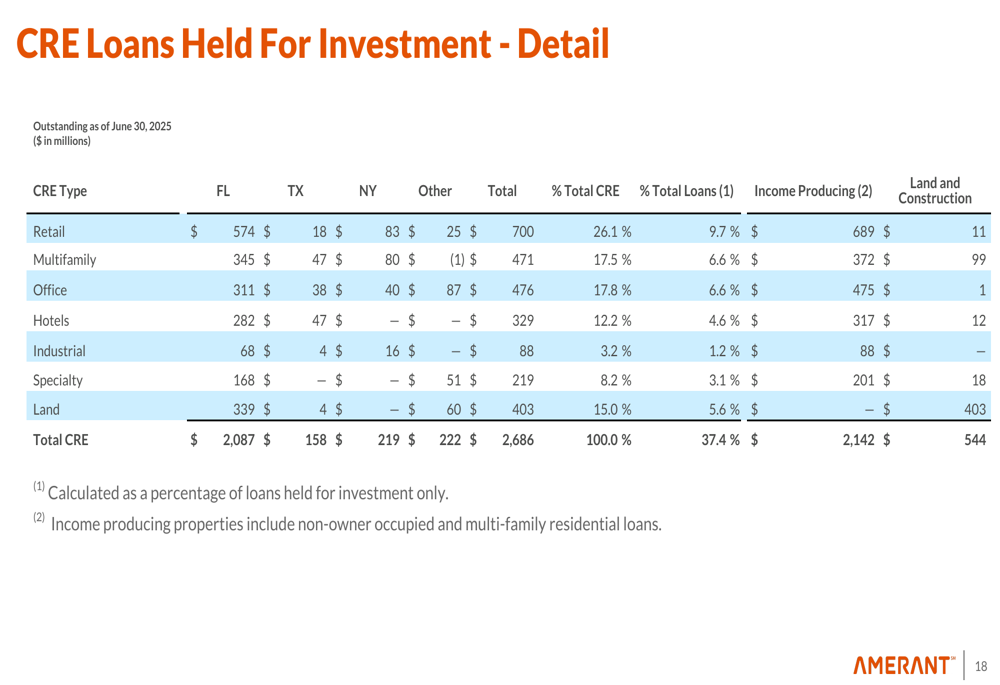

The bank’s loan portfolio remains diversified, with a significant focus on commercial real estate:

Within the CRE portfolio, retail properties represent the largest segment at 26.1%, followed by office at 17.8% and multifamily at 17.5%:

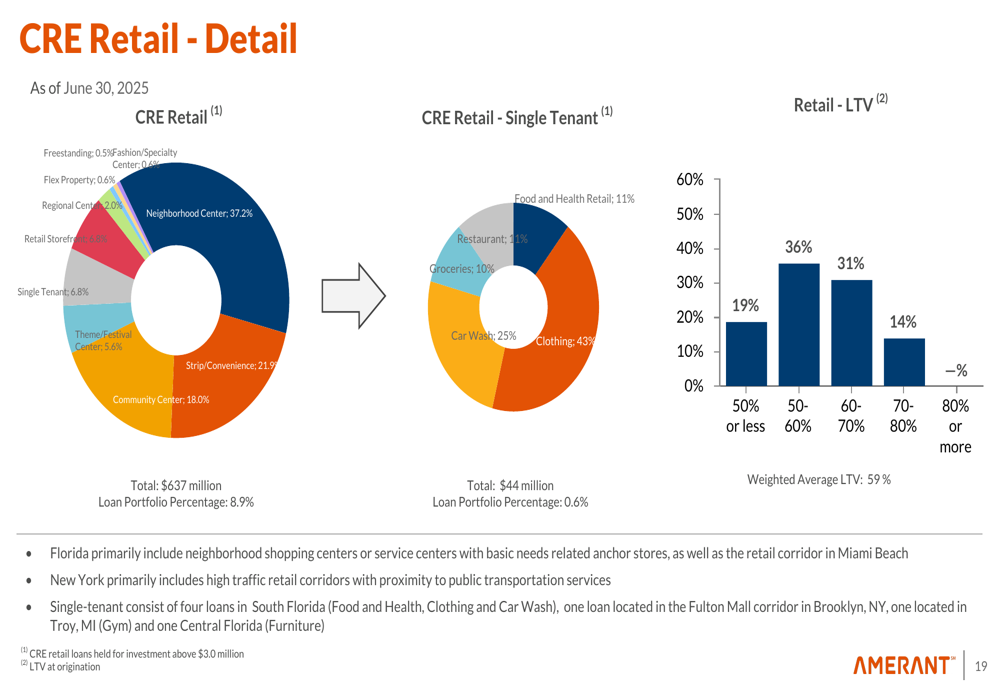

The retail CRE portfolio is further diversified across different property types, with neighborhood centers representing the largest segment:

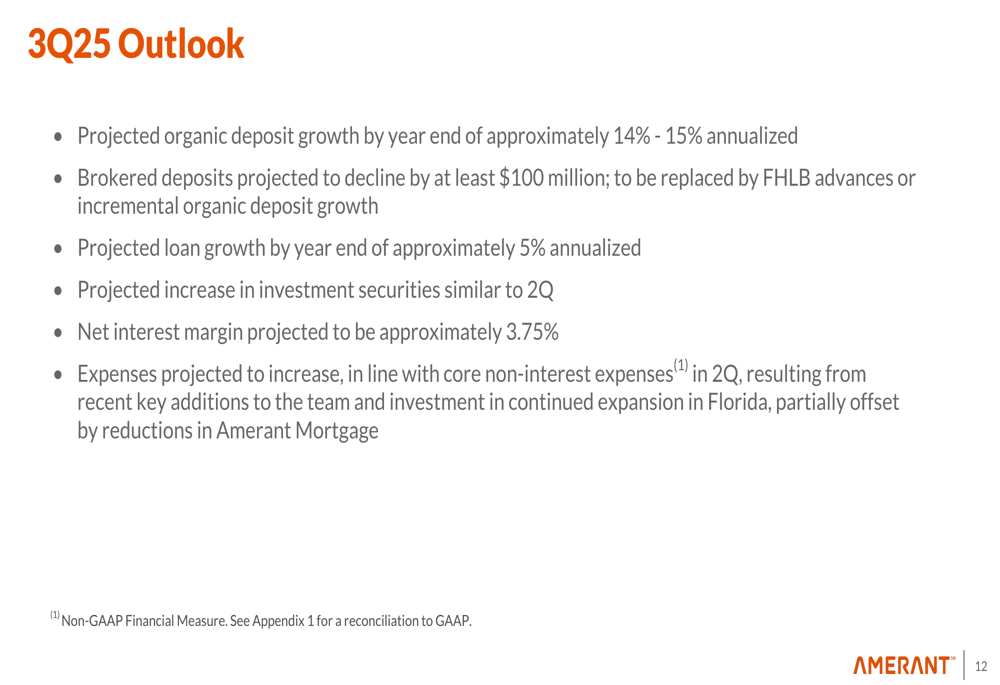

Forward Outlook

Looking ahead to Q3 2025, Amerant provided the following guidance:

The bank expects organic deposit growth of approximately 14-15% annualized by year-end, while brokered deposits are projected to decline by at least $100 million. Loan growth is expected to be more modest at approximately 5% annualized by year-end.

Net interest margin is projected to be approximately 3.75% in Q3, slightly below the 3.81% achieved in Q2. Expenses are expected to increase, reflecting recent key additions to the team and investment in continued expansion in Florida, partially offset by reductions in Amerant Mortgage.

The significant improvement in Amerant’s Q2 results demonstrates a strong recovery from its disappointing Q1 performance. With doubled EPS, improved asset quality, and continued strategic expansion in Florida, the bank appears to be executing effectively on its relationship-focused banking model while maintaining a cautious approach to growth in an uncertain economic environment.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.