BETA Technologies launches IPO of 25 million shares priced $27-$33

Introduction & Market Context

American Axle & Manufacturing (NYSE:AXL) shares surged 15.07% on August 8, 2025, following the release of its second-quarter results, which showed improved profitability metrics despite a year-over-year revenue decline. The automotive supplier reported progress on its strategic initiatives, including the pending combination with Dowlais and new electric vehicle (EV) contracts, which appeared to bolster investor confidence in the company’s future direction.

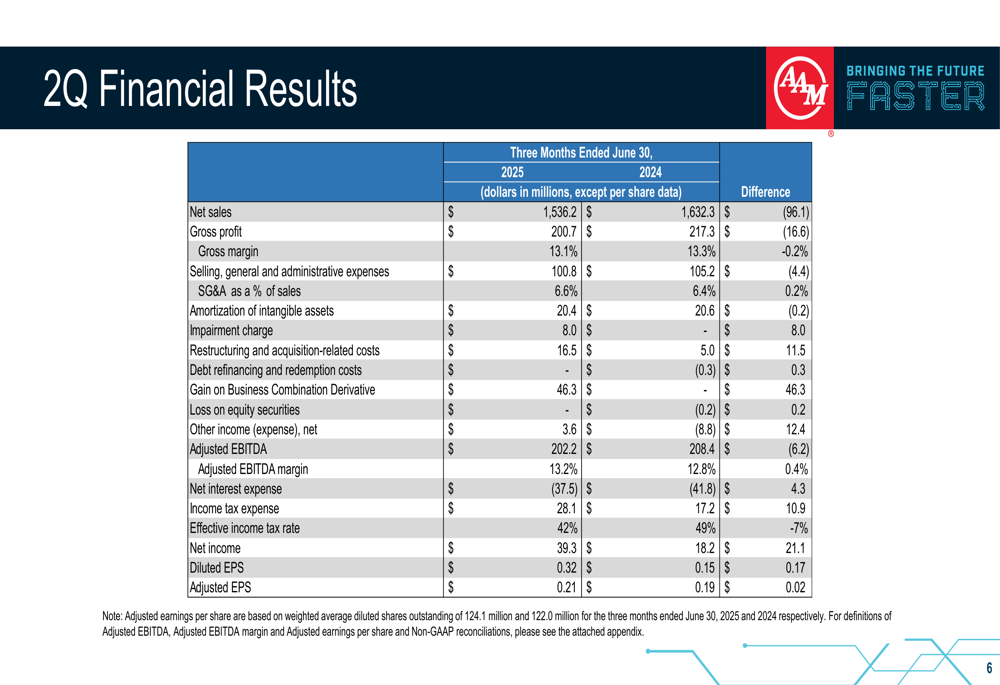

The strong market reaction came as AXL reported a significant improvement in net income, which more than doubled year-over-year to $39.3 million, while adjusted EBITDA margin expanded to 13.2% from 12.8% in the same period last year.

Quarterly Performance Highlights

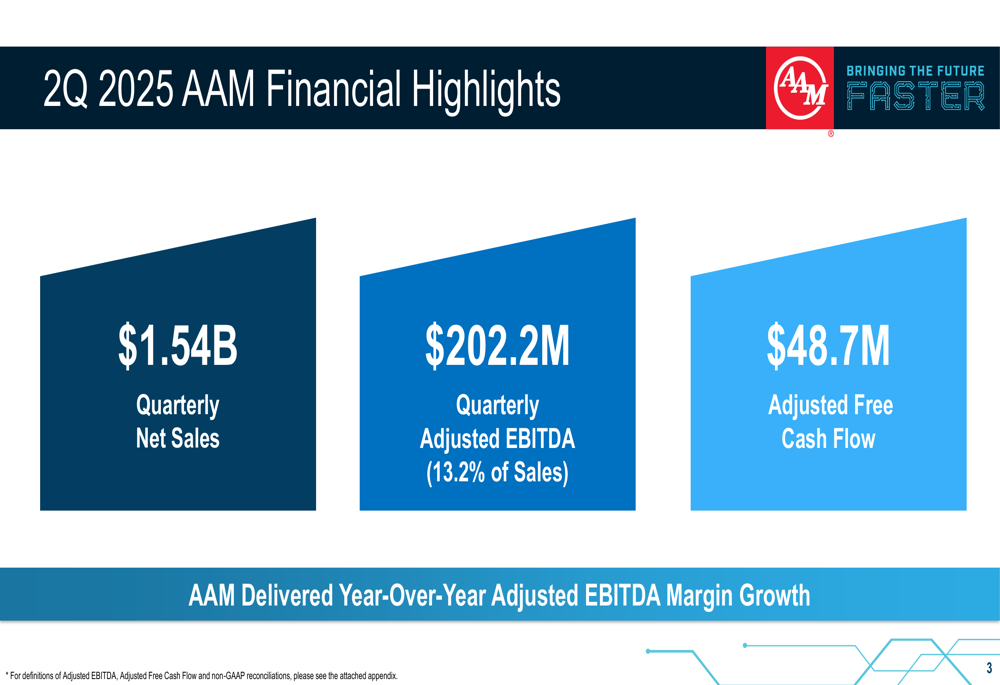

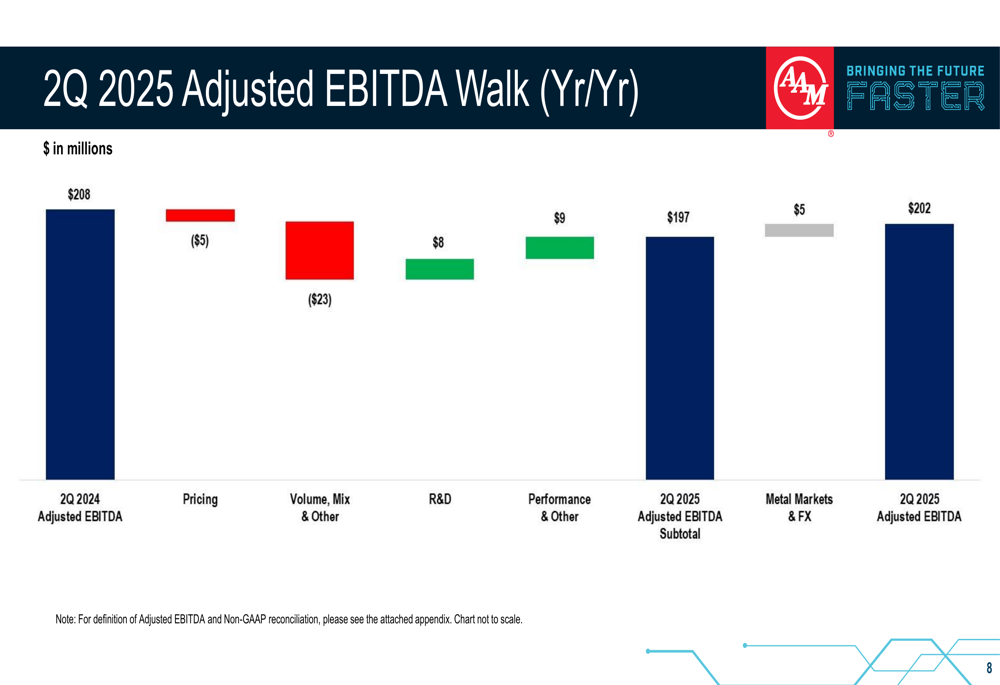

American Axle reported second-quarter 2025 net sales of $1.54 billion, down from $1.63 billion in the same period of 2024. Despite the revenue decline, the company delivered adjusted EBITDA of $202.2 million, representing 13.2% of sales – an improvement from the 12.8% margin achieved in Q2 2024.

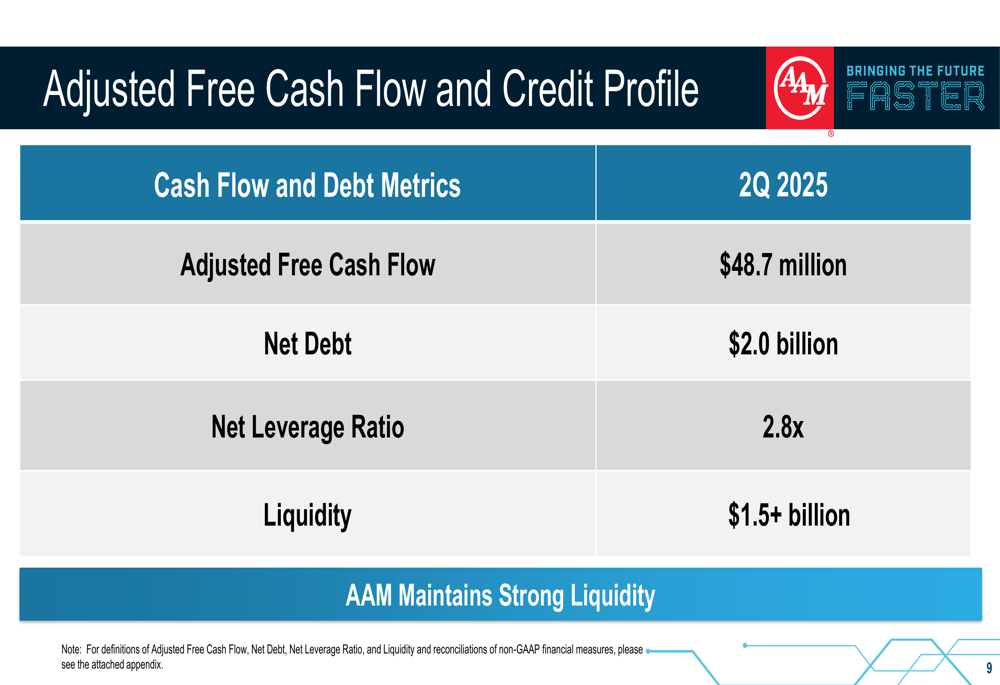

As shown in the following financial highlights slide, the company generated $48.7 million in adjusted free cash flow during the quarter:

The detailed financial results reveal significant improvements in profitability metrics. Net income rose to $39.3 million from $18.2 million in Q2 2024, while diluted earnings per share more than doubled to $0.32 from $0.15. Adjusted EPS also improved to $0.21 from $0.19 year-over-year.

Strategic Initiatives

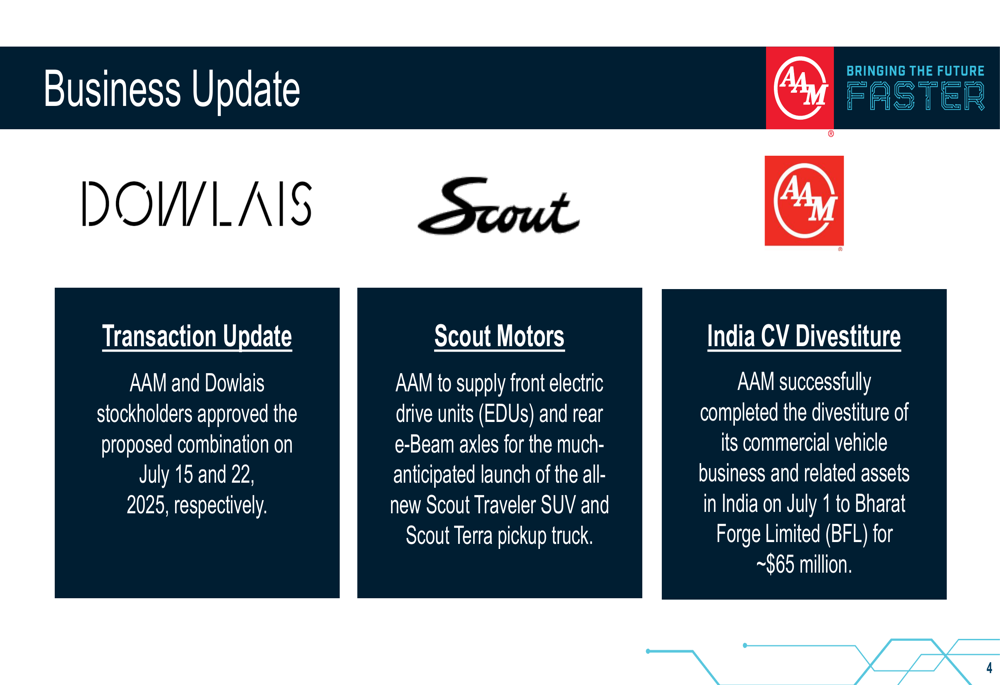

The company highlighted several strategic developments that position it for future growth, particularly in the electric vehicle segment. Most notably, AAM and Dowlais stockholders approved their proposed combination in July 2025, a transaction that will strengthen the company’s position in the automotive supply chain.

Additionally, AAM secured a significant new business win with Scout Motors, agreeing to supply front electric drive units and rear e-Beam axles for the upcoming Scout Traveler SUV and Scout Terra pickup truck. This agreement reinforces the company’s commitment to electrification, which CEO David Dauk emphasized in the previous quarter’s call when he stated, "Electrification is here. It’s only going to grow."

The company also completed the divestiture of its commercial vehicle business in India to Bharat Forge (NSE:BFRG) Limited for approximately $65 million on July 1, further streamlining its operations.

Detailed Financial Analysis

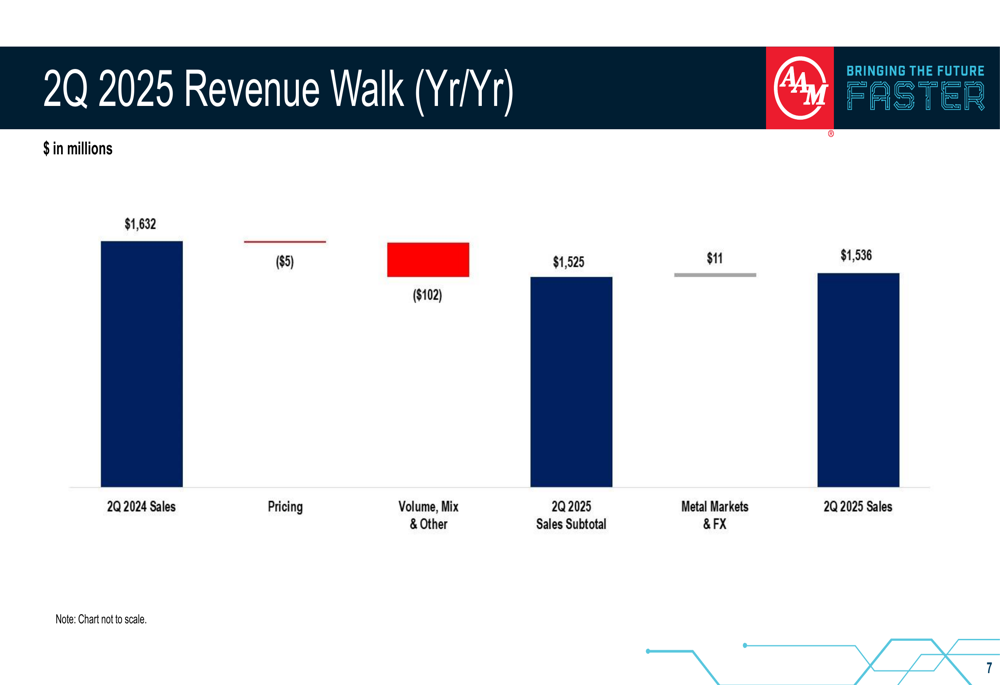

A closer examination of AAM’s quarterly performance reveals the factors driving both the revenue decline and margin improvement. The revenue walk analysis shows that while pricing had a modest negative impact of $5 million, volume, mix and other factors contributed to a more substantial $102 million decrease. These declines were partially offset by a positive $11 million contribution from metal markets and foreign exchange effects.

On the profitability side, the adjusted EBITDA walk demonstrates how the company managed to maintain strong margins despite lower revenue. While pricing and volume/mix negatively impacted EBITDA by $28 million combined, the company achieved $17 million in improvements through R&D efficiencies and operational performance, plus an additional $5 million benefit from metal markets and foreign exchange.

AAM’s financial position remains solid, with net debt of $2.0 billion and a net leverage ratio of 2.8x. The company maintains strong liquidity of over $1.5 billion, providing financial flexibility as it pursues its strategic initiatives.

Forward-Looking Statements

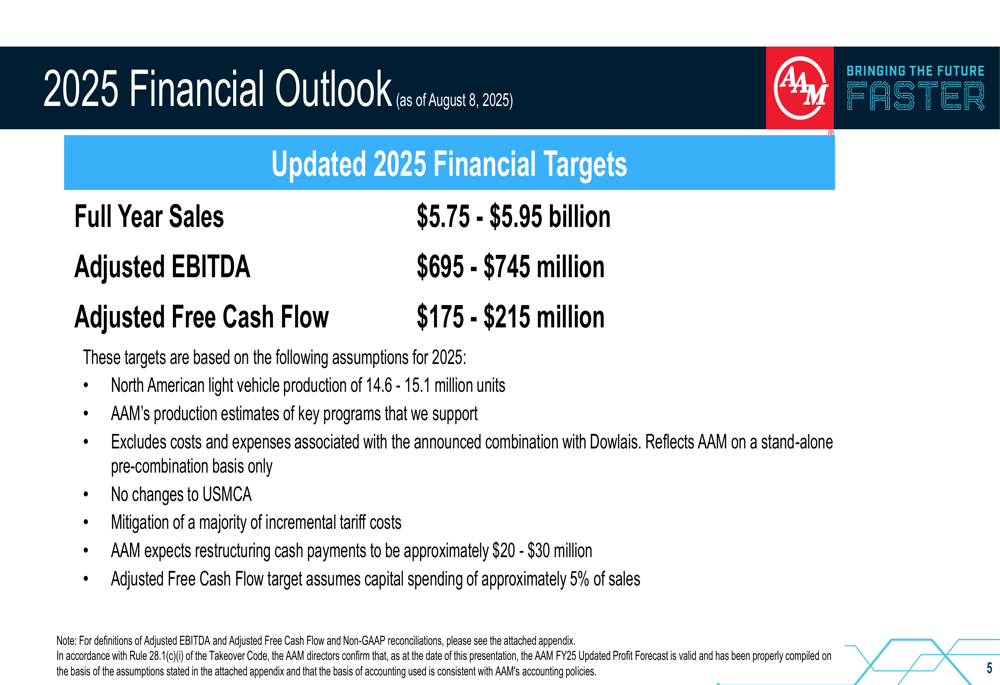

American Axle maintained its full-year 2025 financial outlook, projecting sales between $5.75 billion and $5.95 billion, adjusted EBITDA between $695 million and $745 million, and adjusted free cash flow between $175 million and $215 million.

This guidance is based on North American light vehicle production of 14.6 to 15.1 million units and excludes costs associated with the pending Dowlais combination. The outlook reflects a standalone AAM and assumes the company will successfully mitigate most incremental tariff costs.

The maintained guidance suggests management confidence in the company’s ability to navigate industry challenges while executing on its strategic initiatives. This outlook is consistent with the company’s Q1 2025 projections, though the upper end of the sales range was slightly adjusted upward from the previous $5.65-$5.95 billion range.

Conclusion

American Axle’s second-quarter 2025 results demonstrate the company’s ability to enhance profitability despite revenue headwinds, largely through operational improvements and strategic positioning. The pending Dowlais combination, new EV contracts, and divestiture of non-core assets reflect a focused strategy to capitalize on the industry’s shift toward electrification.

With a stable financial outlook and improved margins, AAM appears well-positioned to navigate the evolving automotive landscape. The market’s strongly positive reaction to the results suggests investors are endorsing the company’s strategic direction and operational execution as it prepares for its next chapter of growth.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.