US stock futures steady with China trade talks, Q3 earnings in focus

Introduction & Market Context

Americana Restaurants International PLC (ADX:AMR) released its Q1 2025 earnings presentation on April 29, showcasing strong performance across key metrics despite a challenging market environment. The company, which operates popular fast-food brands across the Middle East, North Africa, and elsewhere, saw its stock close at $2.05 on April 30, down 2.17% for the day, trading closer to the lower end of its 52-week range of $1.78-$3.40.

The presentation, delivered by CEO Amarpal Sandhu and CFO Harsh Bansal, highlighted Americana’s continued market leadership as a top YUM franchise globally, with significant growth in both store count and financial performance.

Quarterly Performance Highlights

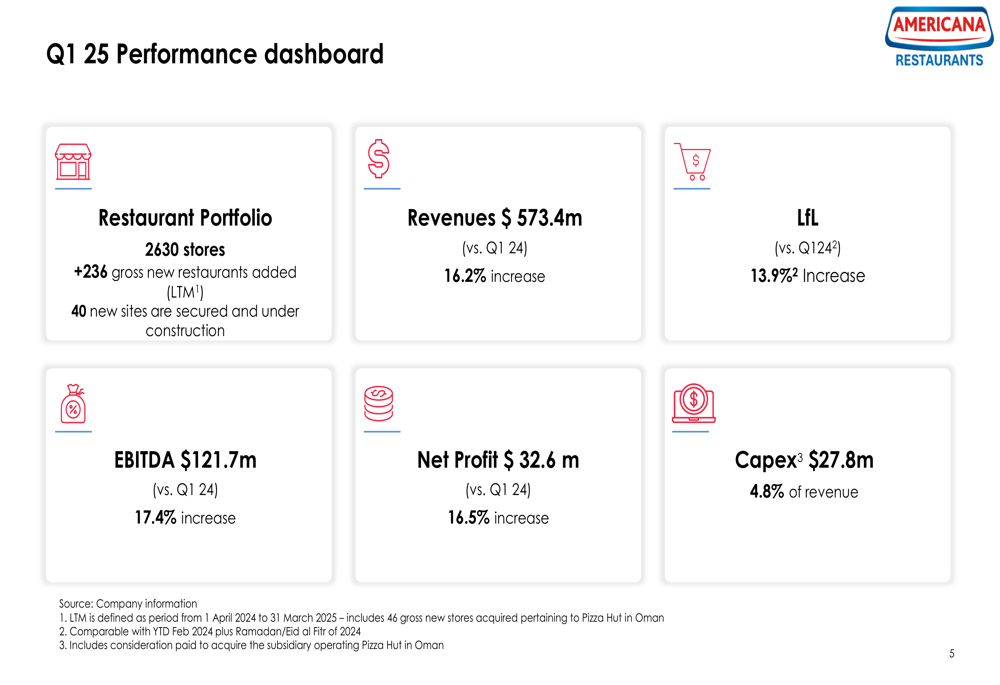

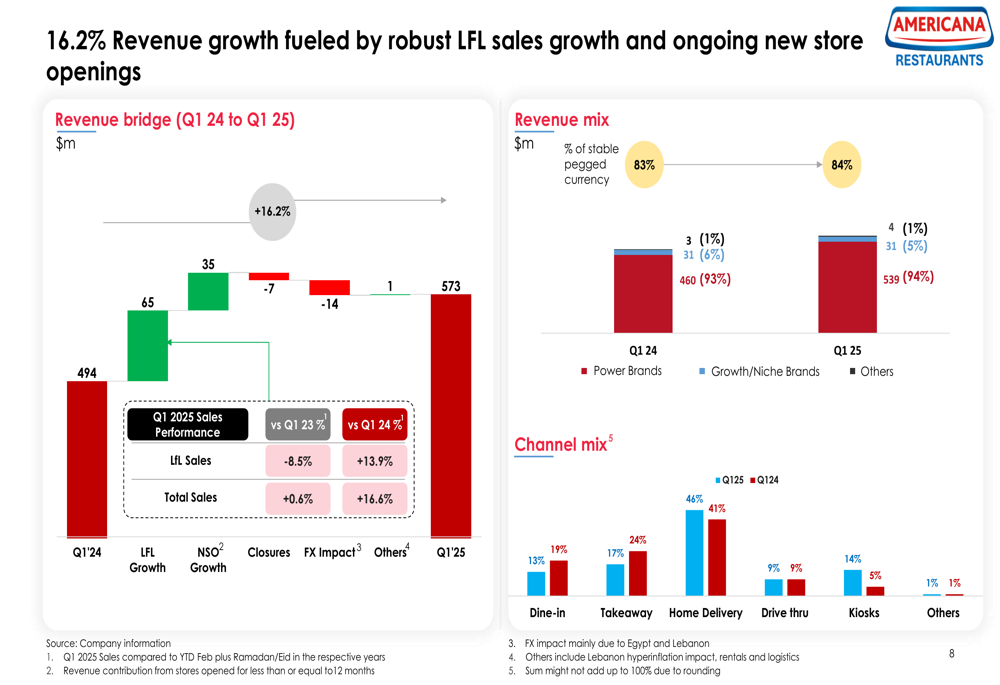

Americana Restaurants reported impressive growth across all key financial metrics for Q1 2025. Revenue reached $573.4 million, representing a 16.2% increase compared to Q1 2024. This growth was primarily driven by a 13.9% increase in like-for-like sales, demonstrating strong performance in existing locations.

As shown in the following performance dashboard, the company’s profitability metrics were equally impressive, with EBITDA rising 17.4% to $121.7 million and net profit increasing 16.5% to $32.6 million:

The company’s revenue growth was analyzed in detail, with the presentation breaking down the various contributors. Like-for-like growth contributed $65 million to the revenue increase, while new store openings added $35 million. These positive factors were partially offset by closures (-$7 million) and foreign exchange impacts (-$14 million).

As illustrated in the revenue bridge and channel mix analysis:

Particularly noteworthy is the significant shift in channel mix, with home delivery increasing from 41% to 46% of total sales and drive-thru growing from 9% to 14%. Meanwhile, dine-in decreased from 19% to 13%, reflecting changing consumer preferences that accelerated during and after the pandemic.

Expansion Strategy and Store Growth

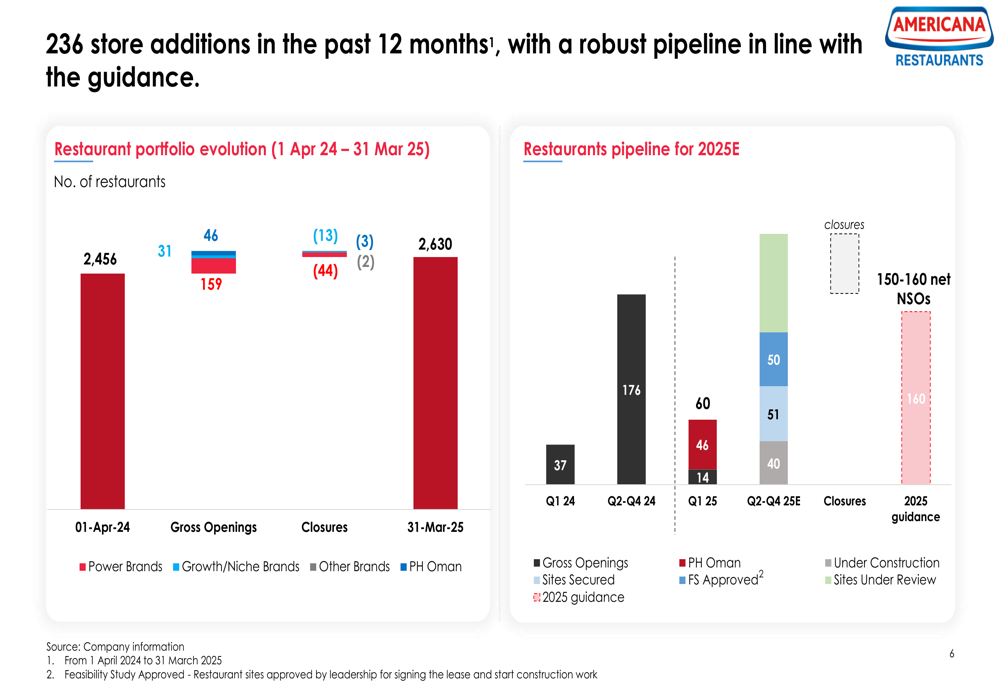

Americana Restaurants continues to execute an aggressive expansion strategy. The company’s restaurant portfolio grew to 2,630 stores by March 31, 2025, representing a net addition of 174 restaurants over the last 12 months. During Q1 2025 alone, the company opened 46 new restaurants while closing 13.

The following chart illustrates the company’s store growth trajectory and pipeline:

The company has secured 40 new sites that are currently under construction, and management reaffirmed its guidance of 150-160 net new store openings for the full year 2025. This expansion strategy is supported by a capital expenditure of $27.8 million in Q1, representing 4.8% of revenue, slightly up from 4.4% in the same period last year.

Financial Analysis and Profitability

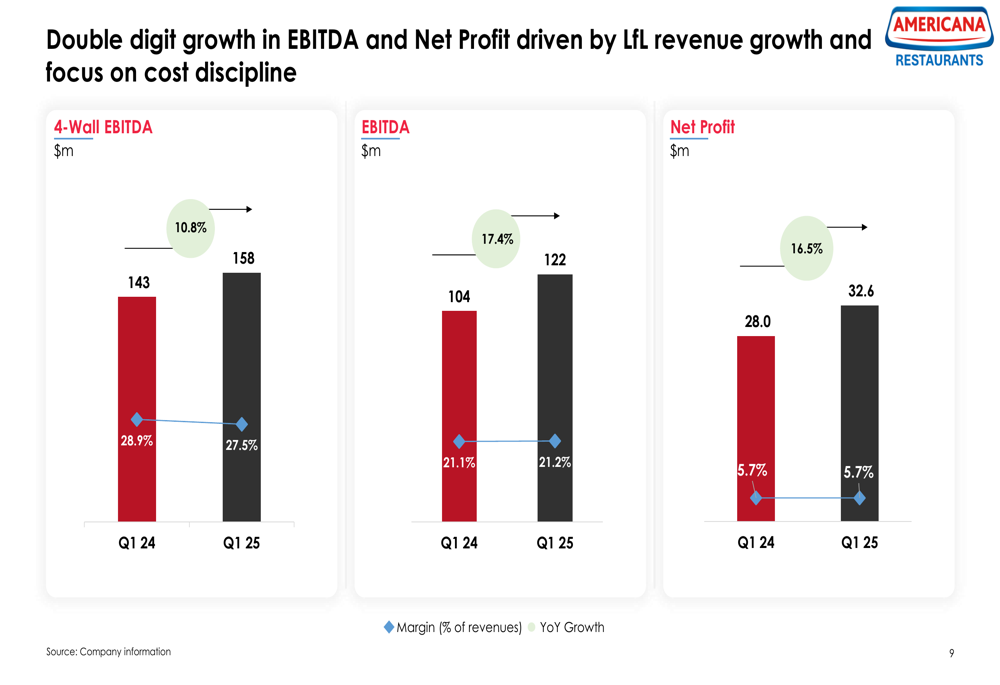

Americana’s profitability metrics showed solid improvement in Q1 2025. The company’s EBITDA increased by 17.4% year-over-year to $121.7 million, with the EBITDA margin expanding slightly to 21.2% from 21.0% in Q1 2024.

The following chart illustrates the growth in EBITDA and net profit:

Net profit increased by 16.5% to $32.6 million, with the net profit margin improving by 1.5 percentage points compared to Q1 2024. This improvement was primarily driven by revenue growth, which contributed $22.9 million to the bottom line, partially offset by Pillar II Tax of $3.5 million and other factors totaling $7.4 million.

The company’s working capital management remained efficient, with net working capital at -8.9% of revenues, indicating strong operational efficiency and favorable payment terms with suppliers.

Brand Performance and Geographic Distribution

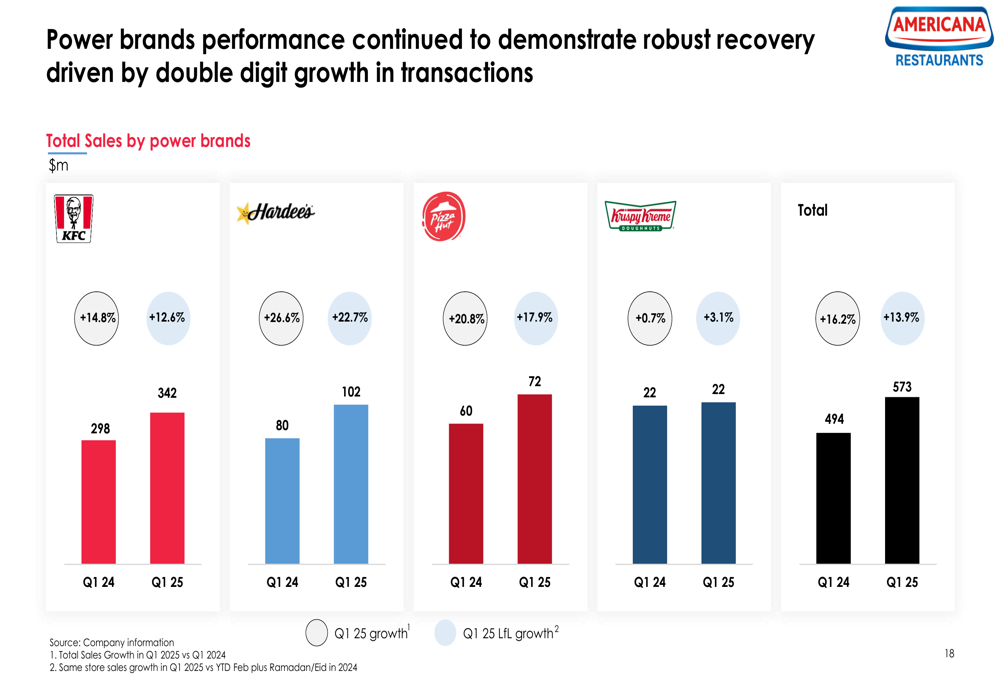

Americana Restaurants operates several "power brands" across its markets, with KFC being the largest contributor to sales. The performance of these brands in Q1 2025 compared to Q1 2024 is illustrated below:

KFC remains the dominant brand in the portfolio, generating $342 million in sales during Q1 2025, up from $298 million in the same period last year. Hardee’s and Pizza Hut also showed strong growth, with sales increasing to $102 million and $72 million, respectively. Krispy Kreme (NASDAQ:DNUT) sales remained flat at $22 million.

Geographically, the company maintains a strong presence across the Middle East and North Africa. Saudi Arabia hosts the largest number of restaurants (730), followed by the UAE (605), Egypt (448), and Kuwait (262).

Forward-Looking Statements

Looking ahead, Americana Restaurants outlined its strategic priorities for 2025, focusing on six key areas: revenue recovery, growth, new store openings, innovation, profitability, and digital leadership.

Management reaffirmed its guidance for 150-160 net new store openings in 2025 and emphasized its continued focus on transaction recovery and maintaining value leadership. The company also highlighted its digital transformation efforts, including the planned launch of Americana loyalty programs and a 200% increase in kiosk transactions.

The company’s 2025 guidance emphasizes both organic growth and potential inorganic opportunities, suggesting that acquisitions may play a role in its expansion strategy. Management also stressed its commitment to enhancing store efficiency and optimizing the channel mix to adapt to evolving consumer preferences.

As Americana Restaurants continues to execute its growth strategy, investors will be watching closely to see if the company can maintain its strong performance in an increasingly competitive quick-service restaurant market while navigating regional economic challenges and changing consumer behaviors.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.