Street Calls of the Week

Introduction & Market Context

Americold Realty Trust (NYSE:COLD) presented its Q2 2025 corporate deck on August 7, showcasing its position as a global leader in temperature-controlled warehousing while navigating challenging market conditions. The presentation comes as the company’s stock trades near 52-week lows, with premarket trading showing a 4.01% decline to $15.55.

The cold storage specialist emphasized its extensive infrastructure and strategic partnerships, even as recent financial results reveal cooling performance metrics. This contrast highlights the tension between Americold’s long-term growth strategy and near-term operational challenges in an inflationary environment with depressed consumer confidence.

Financial Performance Highlights

Americold’s Q2 2025 results showed concerning trends in same-store performance, with same-store revenue declining 1.5% and same-store NOI dropping 4.2%. These metrics align with the company’s disappointing Q1 2025 results, where earnings per share came in at -$0.06 against a forecast of $0.05, and revenue of $628.98 million fell short of the projected $667.18 million.

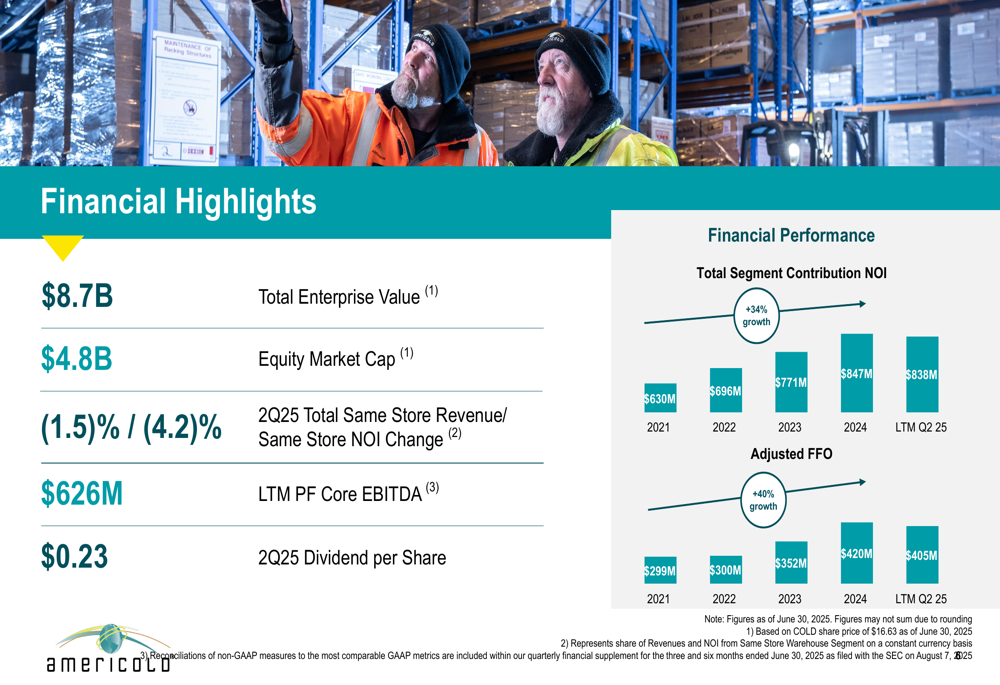

Despite these headwinds, the company maintained its quarterly dividend at $0.23 per share and reported a total enterprise value of $8.7 billion with an equity market cap of $4.8 billion.

As shown in the following financial performance chart, Americold has demonstrated significant growth in recent years, though with signs of plateauing in the most recent period:

The company’s Total (EPA:TTEF) Segment Contribution NOI grew steadily from $630 million in 2021 to $847 million in 2024, before slightly declining to $838 million for the LTM Q2 2025 period. Similarly, Adjusted FFO increased from $299 million in 2021 to $420 million in 2024, before dipping to $405 million in the most recent LTM period.

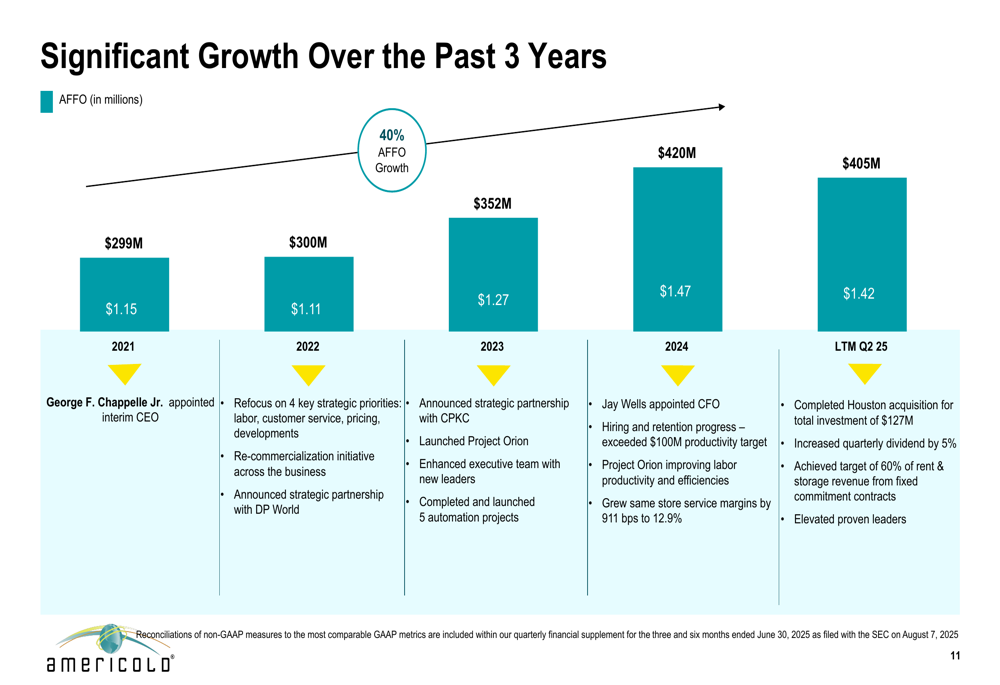

This historical growth trajectory is further illustrated in the company’s AFFO per share development:

While the presentation highlights this multi-year growth story, it’s worth noting that Americold recently revised its full-year 2025 AFFO per share guidance to $1.42-$1.52, as mentioned in its Q1 earnings call, reflecting more modest expectations going forward.

Global Scale & Strategic Positioning

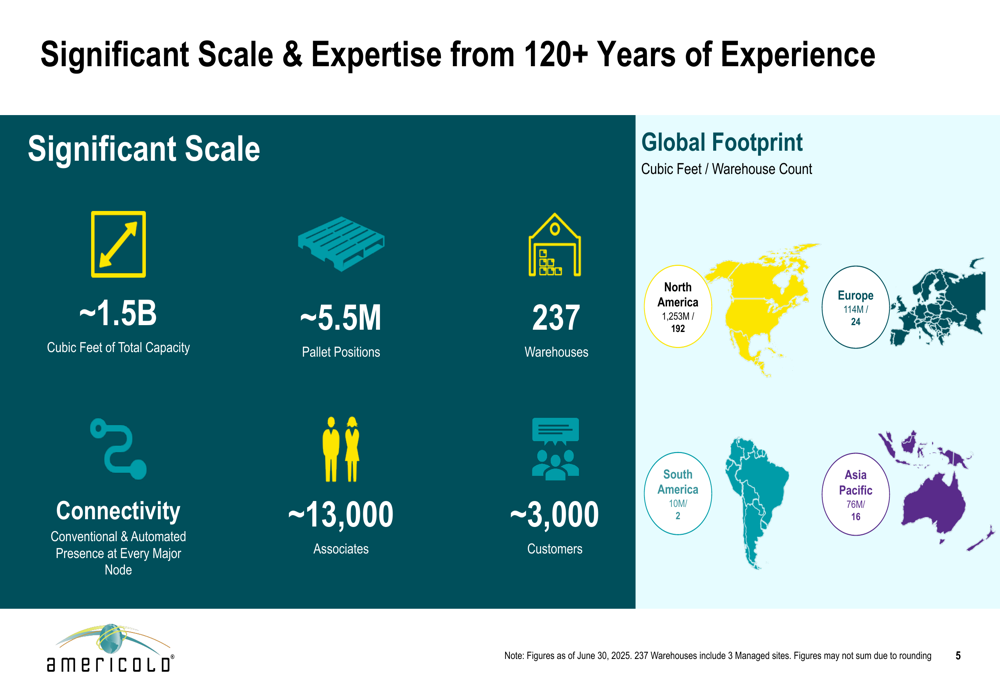

Americold emphasized its extensive global footprint and operational scale as key competitive advantages. With approximately 1.5 billion cubic feet of total capacity across 237 warehouses globally, the company serves around 3,000 customers with a workforce of approximately 13,000 associates.

The following slide illustrates the company’s significant global presence:

This infrastructure spans four continents, with the majority concentrated in North America (192 warehouses with 1,253 million cubic feet), followed by Europe (24 warehouses), Asia Pacific (16 warehouses), and South America (2 warehouses).

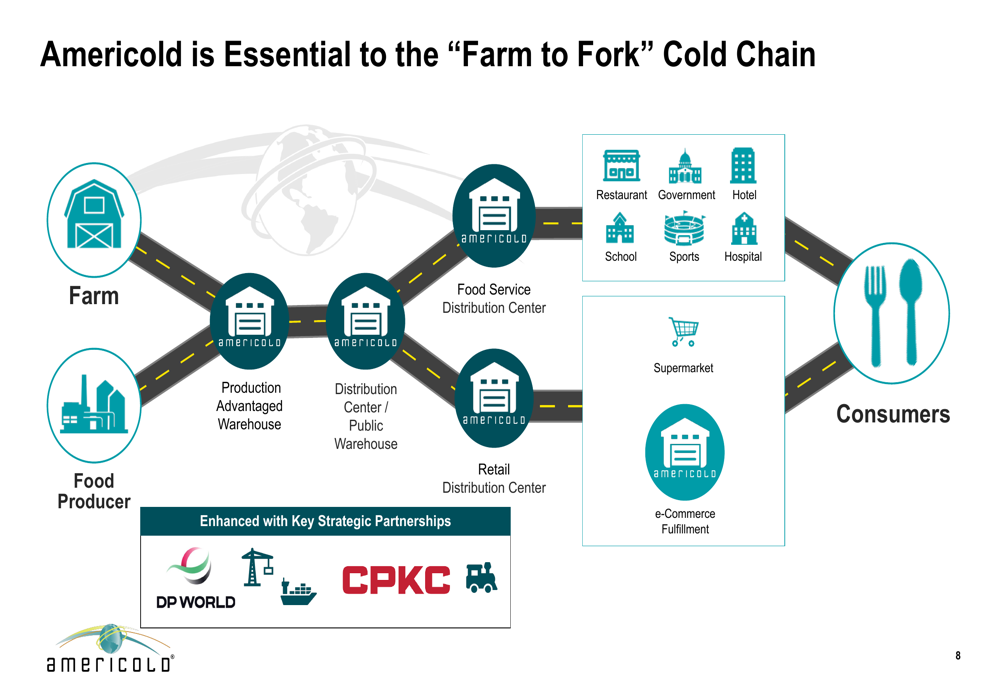

Americold’s strategic position in the food supply chain represents another core strength. The company highlighted its integral role connecting various stages from production to consumption:

This "Farm to Fork" integration positions Americold as a critical infrastructure provider in the global food supply chain, with strategic partnerships with DP World and CPKC enhancing its logistics capabilities. These partnerships, announced in 2023, are part of the company’s strategy to strengthen its market position despite current headwinds.

Customer Relationships & Operating Model

Americold’s presentation emphasized the depth and longevity of its customer relationships as a foundation for stability and growth. The company’s top 25 customers represent approximately 50% of warehouse revenues, with an impressive average tenure of 38 years.

The following slide details these relationships and their strategic importance:

These statistics highlight notable customer loyalty, with 100% of top customers using multiple facilities (averaging 17 sites) and over 90% utilizing committed contracts or leases. Additionally, 13 of these top customers maintain investment-grade credit ratings, providing revenue stability.

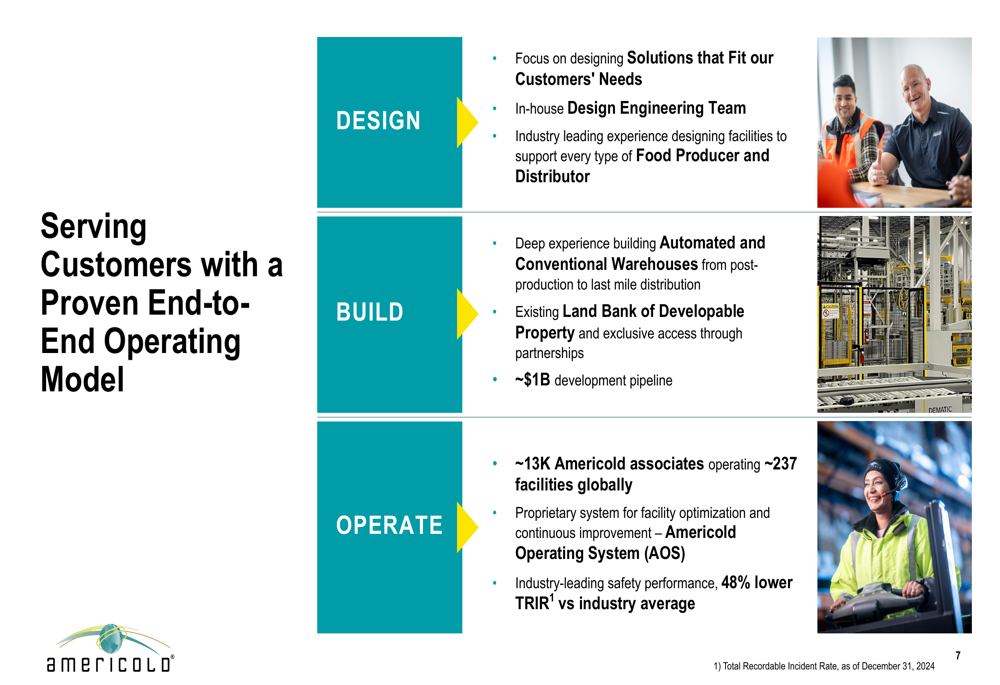

The company’s operating model follows a "Design, Build, Operate" framework that leverages its extensive industry experience:

This integrated approach includes an in-house design engineering team, experience building both automated and conventional warehouses, and a development pipeline of approximately $1 billion. The company also highlighted its proprietary Americold Operating System (AOS) and industry-leading safety performance, with a Total Recordable Incident Rate 48% lower than the industry average.

Market Challenges & Forward Outlook

While Americold’s presentation focused on its strengths and growth opportunities, the company faces significant market challenges that have impacted recent performance. As noted in its Q1 earnings call, these headwinds include tariffs, inflation fears, historically low consumer confidence, and inventory reductions across the food industry.

The gap between the presentation’s growth narrative and current market realities is reflected in the stock’s performance, trading near its 52-week low of $15.45. The premarket decline of 4.01% on the day of the presentation further suggests investor concerns about near-term prospects.

Management’s outlook, as communicated in the Q1 earnings call, anticipates flat to slight growth in same-store constant currency revenue and modest improvement in NOI growth for the remainder of 2025. The company expects a muted seasonal inventory build in the second half of the year, continuing to pressure results.

Despite these challenges, CEO George Chappelle has emphasized that "Our business foundation remains strong," while President Rob Chambers noted, "We deliver far more value as the best operator in the industry," underscoring the company’s focus on operational excellence as it navigates the current environment.

Americold’s presentation makes a compelling case for its long-term strategic positioning in the essential cold storage industry, even as it works to overcome the near-term operational and market challenges reflected in its recent financial performance.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.