Street Calls of the Week

Introduction & Market Context

Andritz AG (WBAG:ANDR) reported its second quarter and first half 2025 financial results on July 31, showing a significant increase in order intake despite experiencing a revenue decline. The industrial engineering group maintained stable profitability margins through improved project execution and a growing service business, which reached an all-time high share of total revenue.

The company’s stock closed at €66.70 on July 30, down slightly by 0.6% ahead of the earnings presentation, but has shown resilience following a 10.62% surge after Q1 results. The stock has maintained most of those gains, reflecting continued investor confidence despite revenue challenges.

Quarterly Performance Highlights

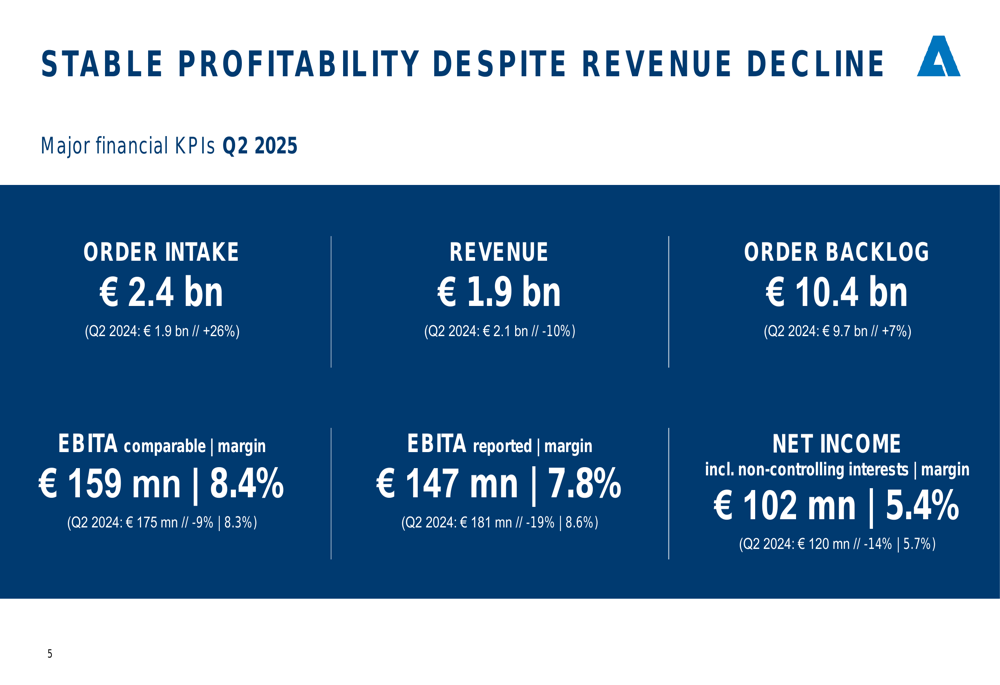

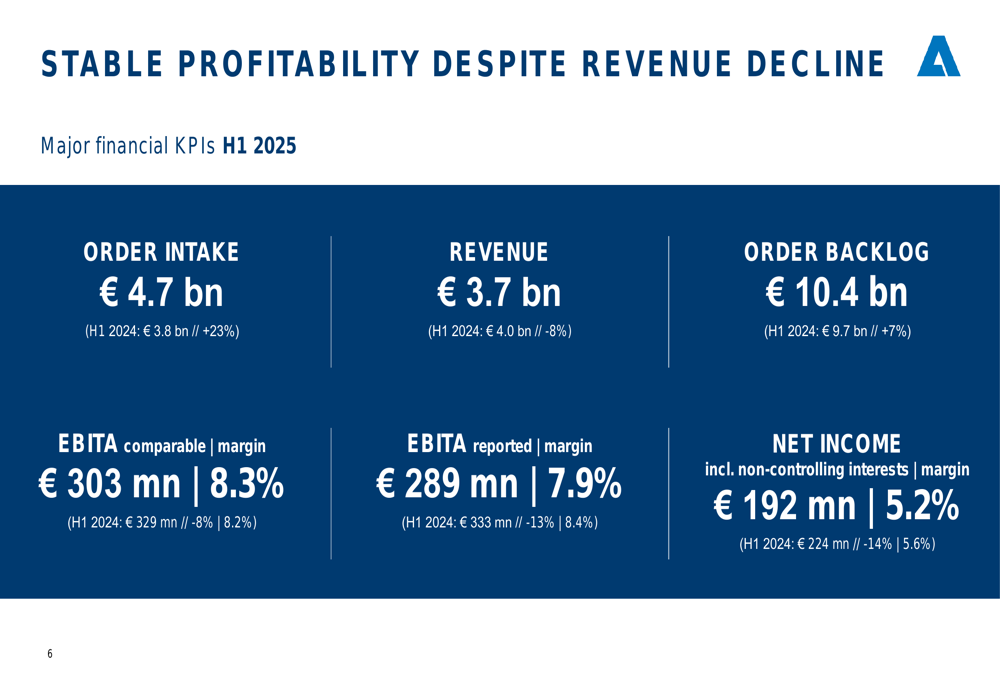

Andritz reported a substantial 26% year-over-year increase in Q2 2025 order intake to €2.4 billion, driven primarily by strong growth in the Metals and Hydropower business areas. For the first half of 2025, order intake grew 23% to €4.7 billion compared to H1 2024.

As shown in the following comprehensive overview of Q2 2025 key performance indicators:

Revenue declined by 10% to €1.9 billion in Q2 2025 compared to €2.1 billion in Q2 2024. The company attributed this decrease to a high revenue base in the previous year and a moderately negative foreign exchange impact of -2% in H1, with no significant impact from tariffs recorded yet.

Despite the revenue decline, Andritz maintained a stable comparable EBITA margin of 8.4% in Q2 2025 (vs. 8.3% in Q2 2024), though reported EBITA decreased to €147 million with a 7.8% margin (vs. €181 million and 8.6% in Q2 2024). Net income for Q2 2025 was €102 million, representing a 5.4% margin, down from €120 million (5.7% margin) in the same period last year.

The first half performance shows similar trends as illustrated in this comprehensive H1 2025 financial overview:

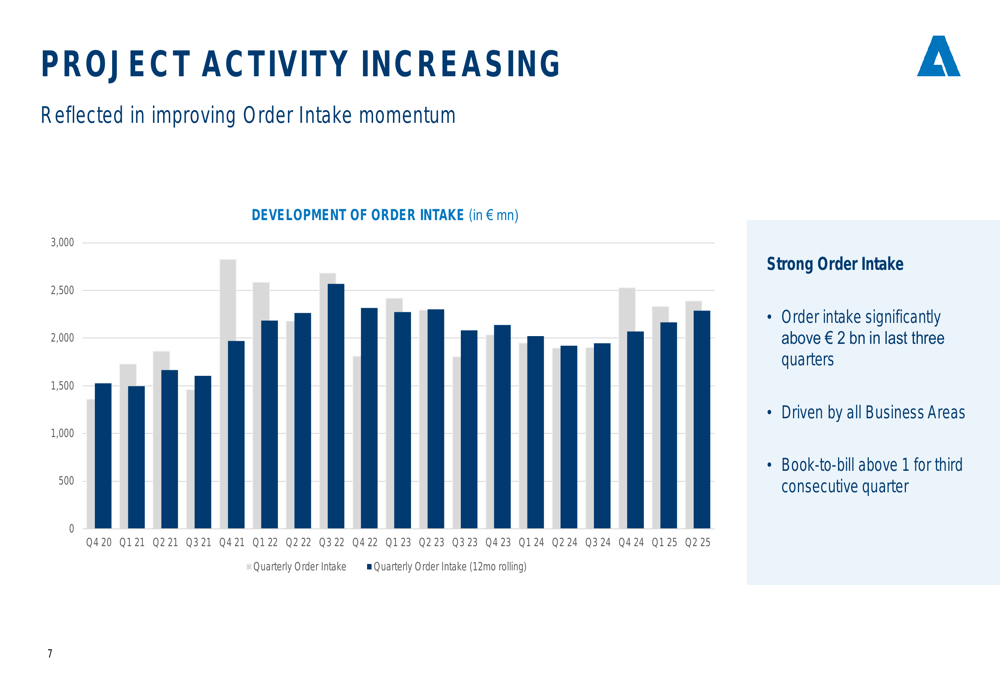

The company’s order backlog continued to strengthen, reaching €10.4 billion at the end of Q2 2025, a 7% increase from €9.7 billion in Q2 2024. This marks the third consecutive quarter with a book-to-bill ratio above 1, indicating potential for future revenue growth.

The order intake momentum has been improving steadily as shown in this development chart:

Business Area Performance

Performance varied across Andritz’s four business segments. The Metals business area saw significant order intake growth fueled by large orders in Metals Processing in China and the US in Q2, while Hydropower benefited from several mid-sized and large orders in plant rehabilitation and modernization, as well as two major pumped storage projects in India.

The Pulp & Paper segment, which accounts for the largest share of revenue, experienced a decline compared to the previous year but maintained improved profitability due to better project management and a higher service share. The Environment & Energy business achieved record high revenue in H1 2025, with solid growth in its service business.

Strategic Initiatives

Andritz has continued its strategy of acquiring complementary businesses, with several significant acquisitions in 2025 including LDX (USA), a provider of emission reduction technologies; A. Celli Paper (Italy), a global supplier of machinery for tissue and paper production; Diamond Power (USA), strengthening the service business for recovery and power boilers; and Salico Group (Italy), providing equipment for strip and plate finishing.

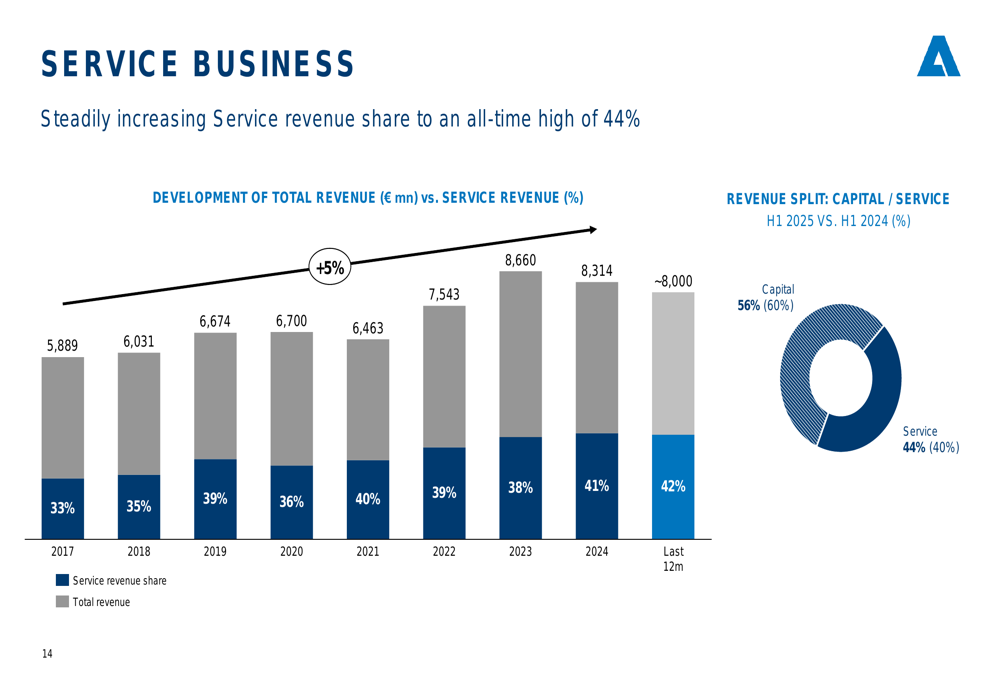

The company’s service business has shown steady growth, reaching an all-time high of 44% of total revenue, up from 40% previously. This increasing service revenue share has helped stabilize margins despite the overall revenue decline.

As shown in the following chart illustrating the growth of service business:

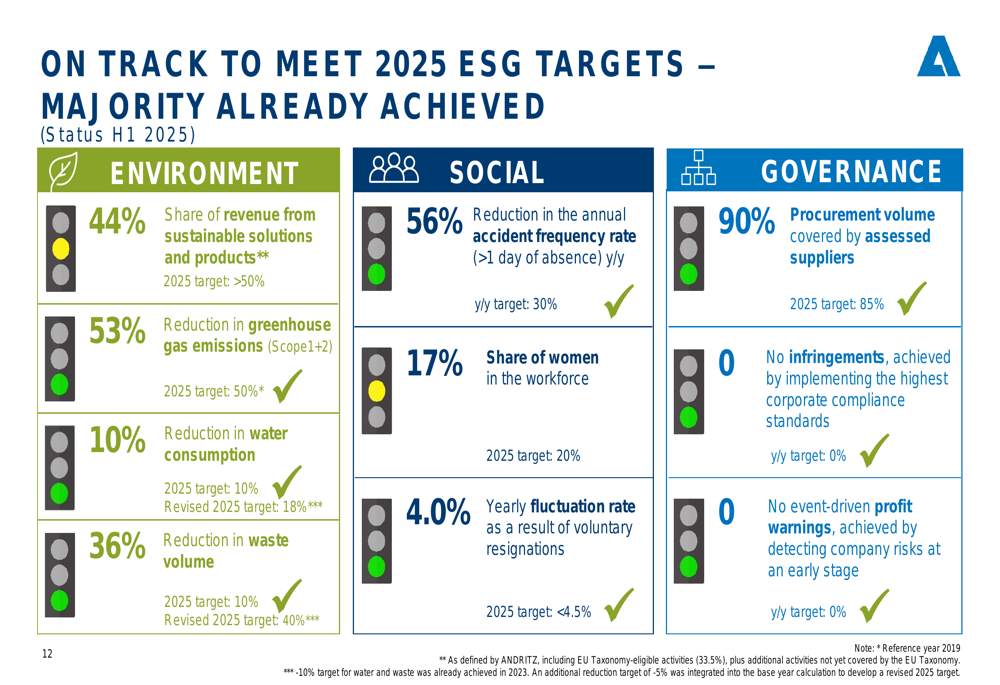

Andritz has made significant progress on its ESG (Environmental, Social, and Governance) targets for 2025, with the majority already achieved. Notable achievements include a 53% reduction in greenhouse gas emissions (against a target of 50%) and a 56% reduction in the annual accident frequency rate (against a target of 30%).

The company’s comprehensive ESG target achievements are illustrated here:

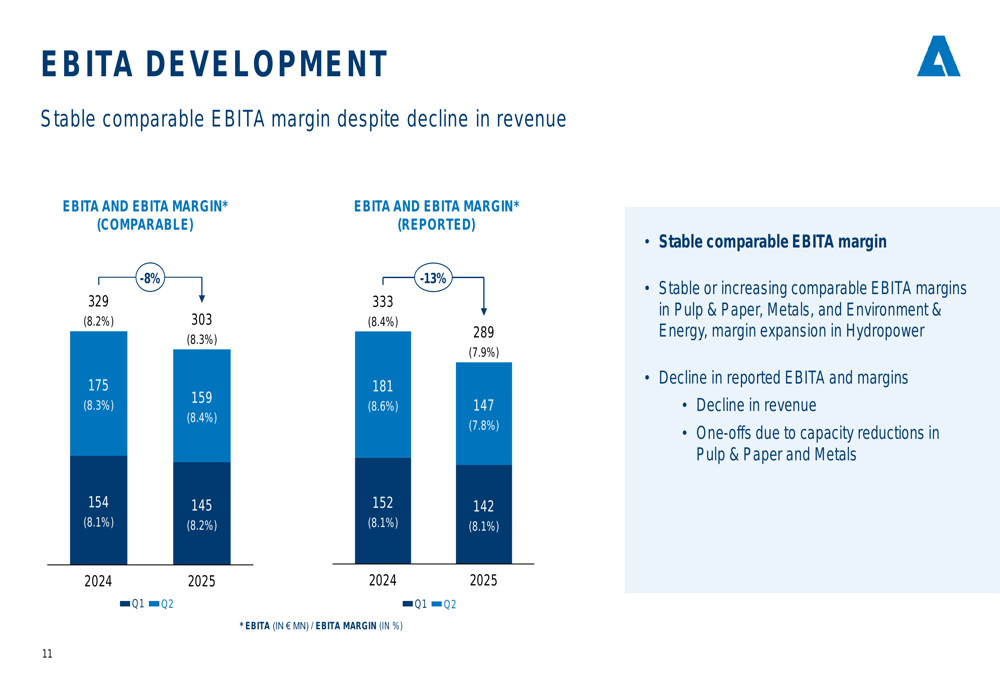

Financial Analysis

Despite the revenue decline, Andritz maintained a strong financial position with solid profitability. The company’s EBITA development shows stable comparable margins despite lower volumes:

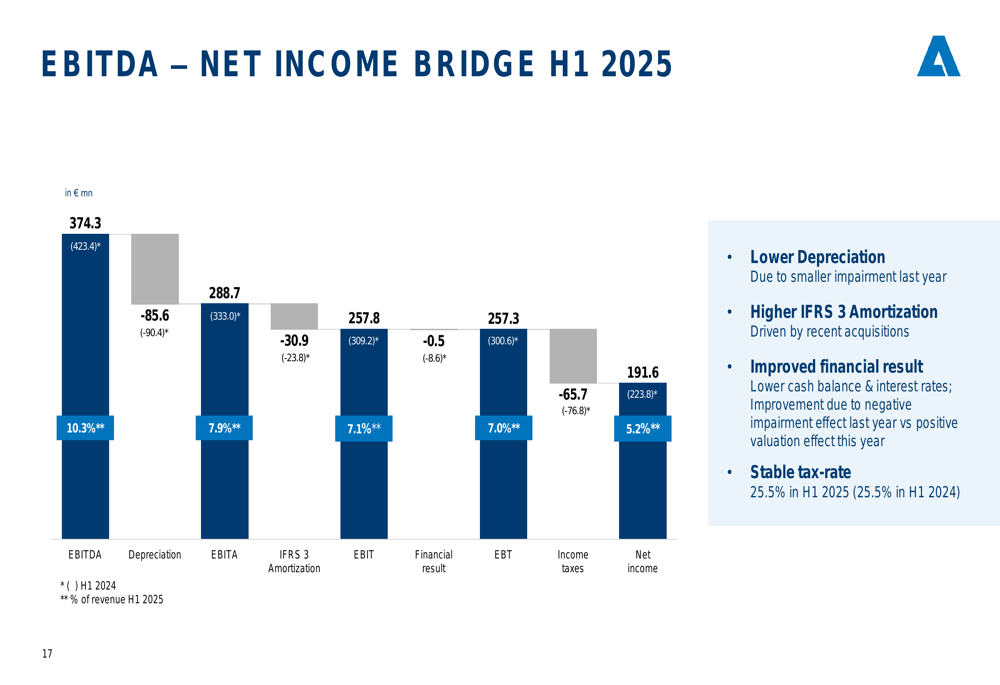

The company’s financial position remains strong, with substantial liquid funds and net liquidity. The ROIC (Return on Invested Capital) stood above 20% in H1 2025, significantly exceeding the company’s WACC (Weighted Average Cost of Capital) and implying significant value generation.

The bridge from EBITDA to net income for H1 2025 provides insight into the company’s profitability structure:

Andritz has maintained its policy of gradual dividend increases with a target payout ratio above 50%. The company’s capital allocation remains balanced between capital expenditure, dividends, share buybacks, and M&A activities.

Forward-Looking Statements

Andritz reaffirmed its guidance for 2025, projecting revenue between €8.0-8.3 billion and a comparable EBITA margin of 8.6%-9.0%. The company noted that while no adverse impact from increasing trade barriers has been observed yet, a significant negative translation impact in the low triple-digit Euro million amount is possible in 2025 due to recent strengthening of the Euro against Andritz’s major operating currencies.

The company’s 2025 guidance and market outlook are presented here:

Looking further ahead, Andritz has set mid-term targets for 2027, aiming for revenue between €9-10 billion (representing a CAGR of 4.5% to the mid-point) and a comparable EBITA margin exceeding 9%. These targets are based on assumptions of growth in capital sales, expansion of service share, increasing demand for green technologies, and continued bolt-on M&A activity.

Conclusion

Andritz’s Q2 and H1 2025 results present a mixed picture, with strong order intake and backlog growth suggesting potential future revenue recovery, while current revenue faces headwinds. The company has successfully maintained stable profitability margins through improved project execution, a higher service revenue share, and strategic acquisitions.

The focus on green technologies and service business expansion, combined with the company’s strong financial position and growing order backlog, positions Andritz to navigate current challenges while pursuing its mid-term growth targets. However, potential risks include foreign exchange impacts and uncertain global market conditions that could affect future performance.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.