Nvidia and TSMC to unveil first domestic wafer for Blackwell chips, Axios reports

Introduction & Market Context

Andritz AG (VIE:ANDR) presented its Q2/H1 2025 financial results on July 31, 2025, revealing a mixed performance characterized by strong order intake growth despite revenue declines. The industrial technology group saw its stock close at €60.70 following the presentation, up 0.41% for the day, continuing a strong year-to-date performance with a 99% price return according to available market data.

The company highlighted significant growth in new orders while managing through revenue challenges with stable profitability, supported by an increasing service business share and strategic acquisitions. Despite global economic uncertainties and potential tariff concerns, Andritz maintained its full-year guidance while confirming its ambitious 2027 targets.

Quarterly Performance Highlights

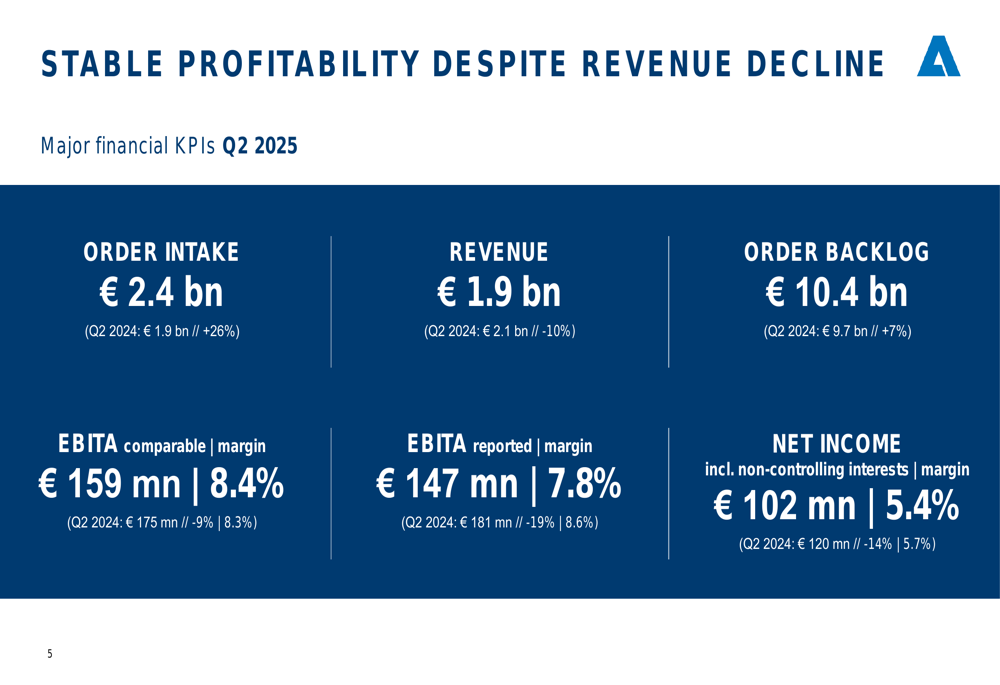

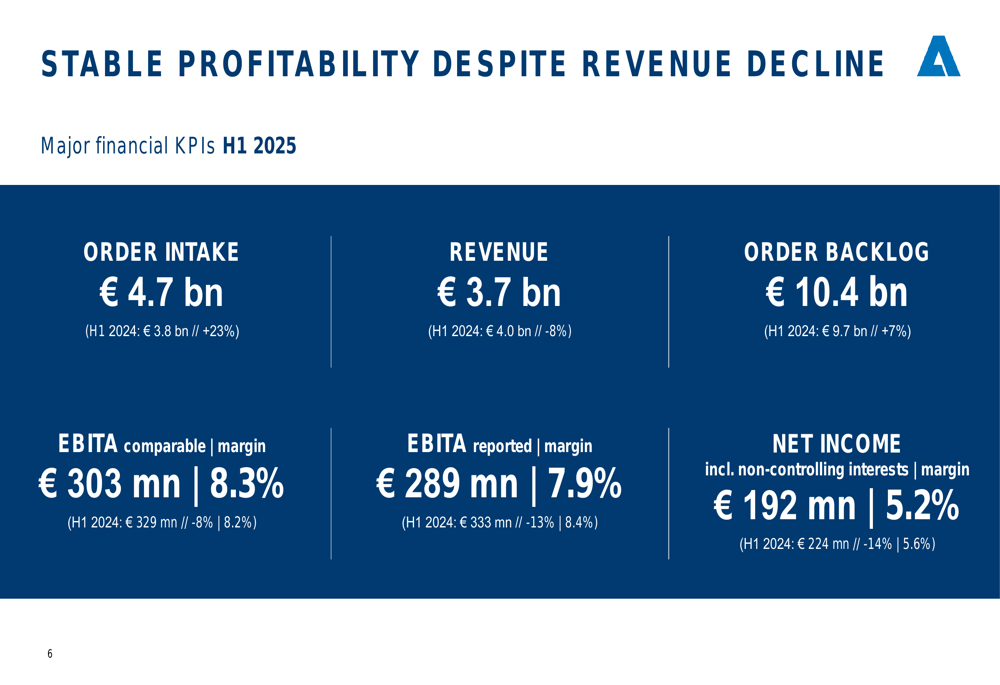

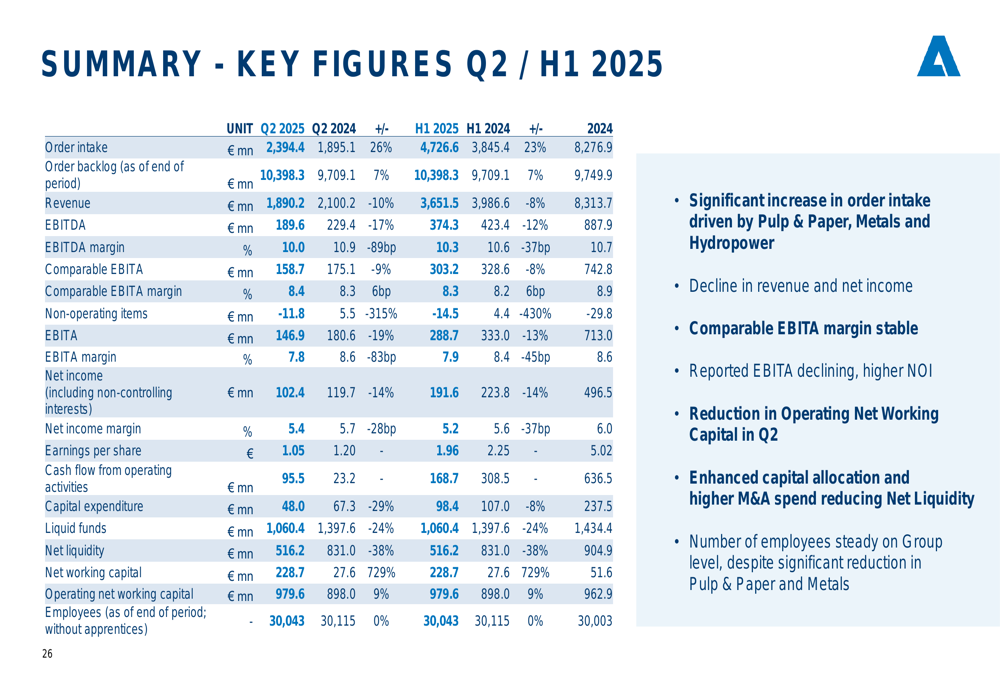

Andritz reported substantial growth in order intake for Q2 2025, reaching €2.4 billion, a 26% increase compared to Q2 2024. For the first half of 2025, order intake grew by 23% to €4.7 billion. This growth was primarily driven by strong performance in the Metals and Hydropower business areas, with satisfactory levels in Pulp & Paper.

As shown in the following chart of Q2 2025 key financial figures:

Despite the strong order intake, revenue decreased by 10% to €1.9 billion in Q2 2025 and by 8% to €3.7 billion for H1 2025 compared to the same periods in 2024. The company attributed this decline to a high revenue base in the previous year and a moderately negative foreign exchange impact of -2% in H1. Nevertheless, Andritz maintained stable profitability with a comparable EBITA margin of 8.4% in Q2 2025, slightly improving from 8.3% in Q2 2024.

The H1 2025 performance showed similar trends:

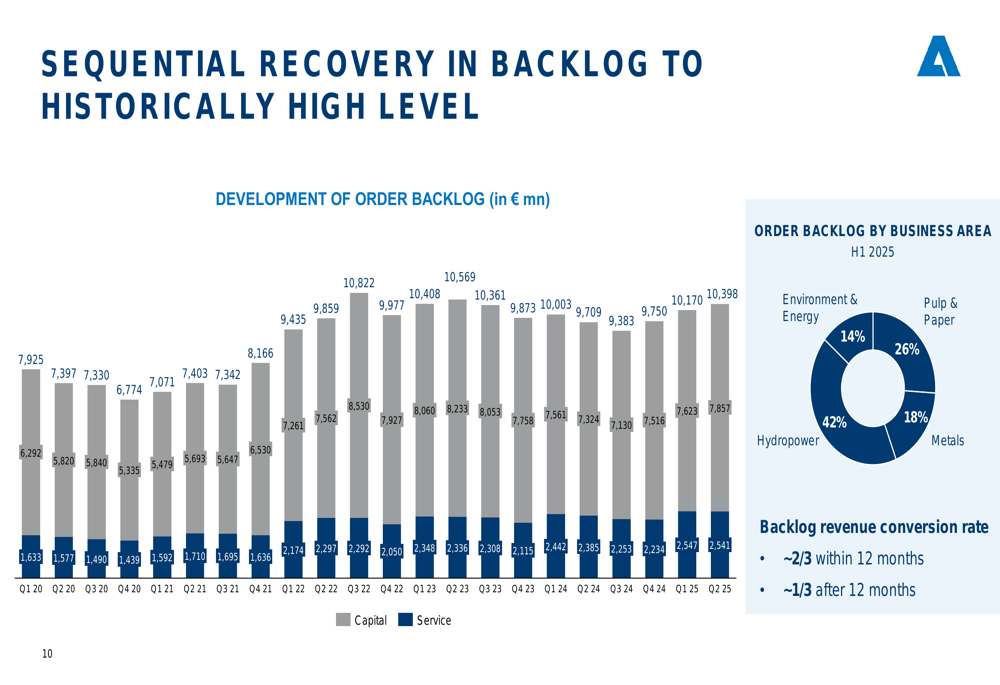

The company’s order backlog continued to strengthen, reaching €10.4 billion, a 7% increase compared to Q2 2024. This represents the third consecutive quarter with a book-to-bill ratio above 1, indicating continued growth momentum. The order backlog is diversified across business areas, with approximately two-thirds expected to convert to revenue within the next 12 months.

As illustrated in the following chart showing the sequential recovery in order backlog:

Business Area Performance

Performance varied across Andritz’s four business areas. The Hydropower segment showed particularly strong results, with significant order intake growth driven by renewable energy projects, including two major pumped storage projects in India. The segment’s revenue increased, and its comparable EBITA margin expanded due to improved project execution and pricing.

The Metals segment experienced significant order intake growth fueled by large orders in China and the US, though revenue declined due to low order intake in 2024. The company implemented capacity reductions while maintaining stable operational profitability through restructuring measures.

The Pulp & Paper business saw strong order intake growth driven by orders in both pulp and paper sectors, primarily from the US and Asia. Despite revenue decline, the segment improved profitability through better project management and a higher service share.

The Environment & Energy segment experienced a decline in order intake compared to record levels in H1 2024 due to weaker markets, though it achieved all-time high revenue in H1 2025 with solid growth in service business.

Strategic Initiatives

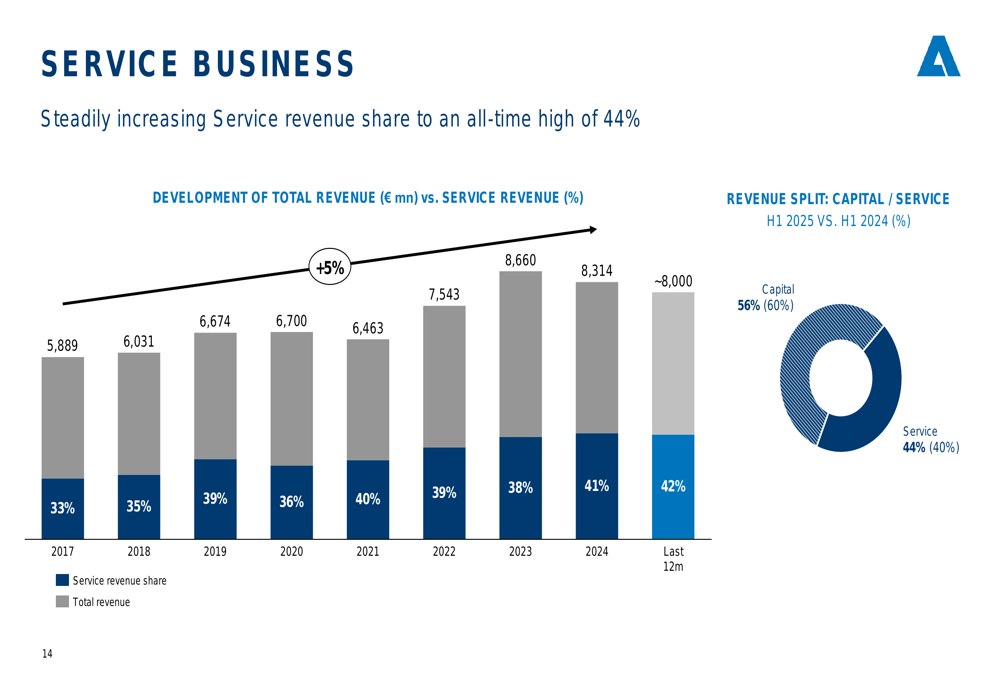

Andritz continued to execute its strategic initiatives focused on service business growth and complementary acquisitions. The service revenue share reached an all-time high of 44% in H1 2025, up from 40% in H1 2024, contributing to stable profitability despite revenue challenges.

As shown in the following chart of service business growth:

The company completed four major acquisitions in the first half of 2025:

- LDX (USA) in the Environment & Energy segment with annual revenue of approximately $100 million

- A. Celli Paper (Italy) in the Pulp & Paper segment with annual revenue of approximately €70 million

- Diamond Power (USA) in the Pulp & Paper segment with annual revenue of approximately €100 million

- Salico Group (Italy) in the Metals segment with annual revenue of approximately €100 million

These acquisitions align with Andritz’s strategy of complementary business expansion through M&A activities, particularly in service, digitalization, and decarbonization areas.

Financial Analysis

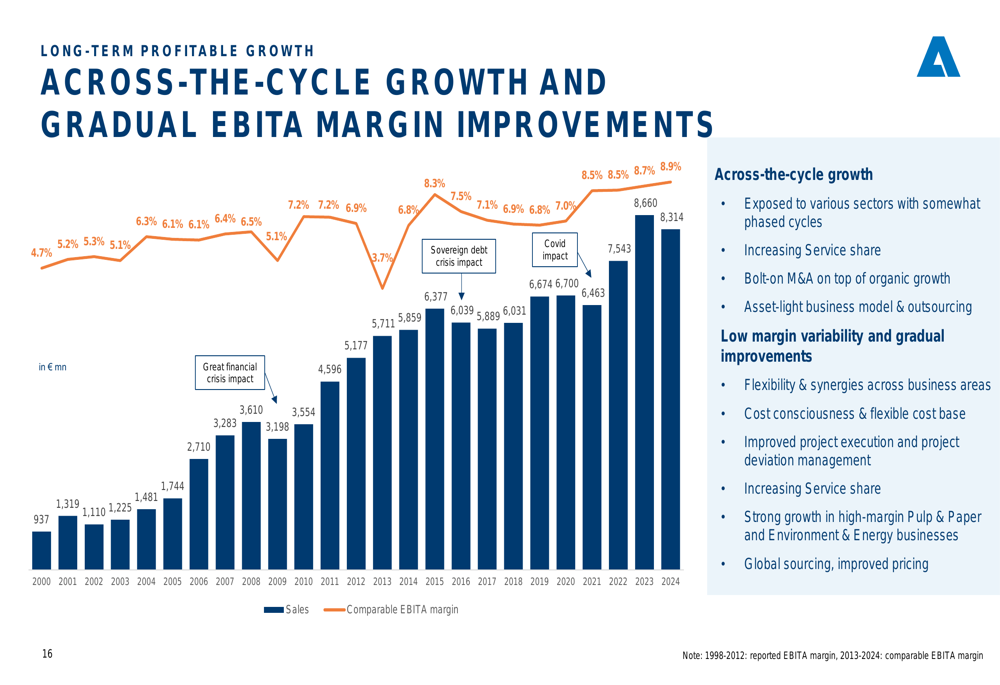

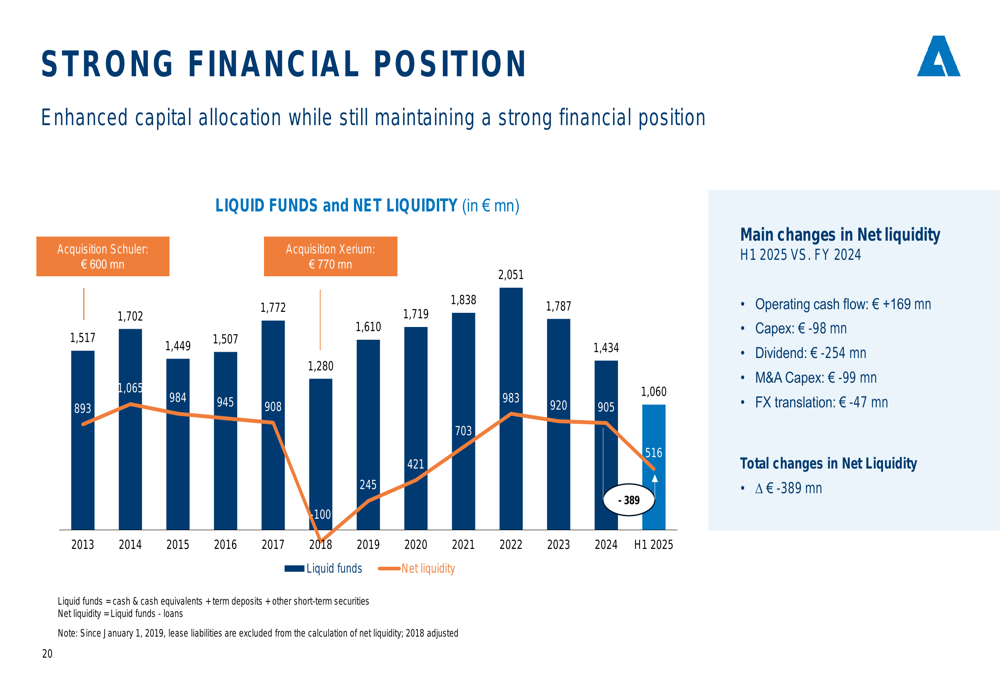

Despite the revenue decline, Andritz maintained a strong financial position. The company’s long-term profitable growth trajectory demonstrates resilience across business cycles, supported by exposure to various sectors with phased cycles and an increasing service share.

As illustrated in the following chart of long-term profitable growth:

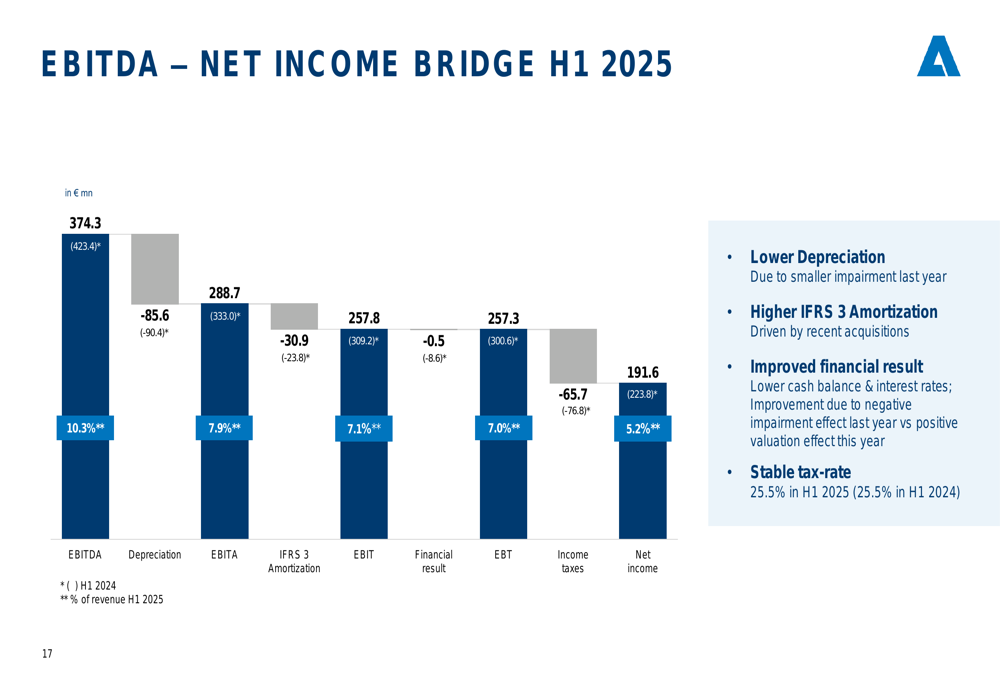

The company’s EBITDA to net income bridge for H1 2025 shows the components contributing to the final result:

Andritz maintained a strong financial position with positive net liquidity, though it decreased compared to FY 2024 due to operating cash flow (+€169 million), offset by capital expenditure (-€98 million), dividend payments (-€254 million), M&A investments (-€99 million), and FX translation effects (-€47 million).

The company’s return on invested capital (ROIC) remained significantly above its weighted average cost of capital (WACC), at over 20% compared to approximately 8%, indicating substantial value generation despite a slight decrease due to lower EBITA in H1 2025.

Forward-Looking Statements

Andritz confirmed its guidance for 2025, expecting revenue between €8.0-8.3 billion and a comparable EBITA margin of 8.6-9.0%, though management indicated they expect to achieve the lower end of these ranges. The company has not observed any adverse impact from increasing trade barriers on its major markets yet, with limited foreign exchange impact in H1 2025.

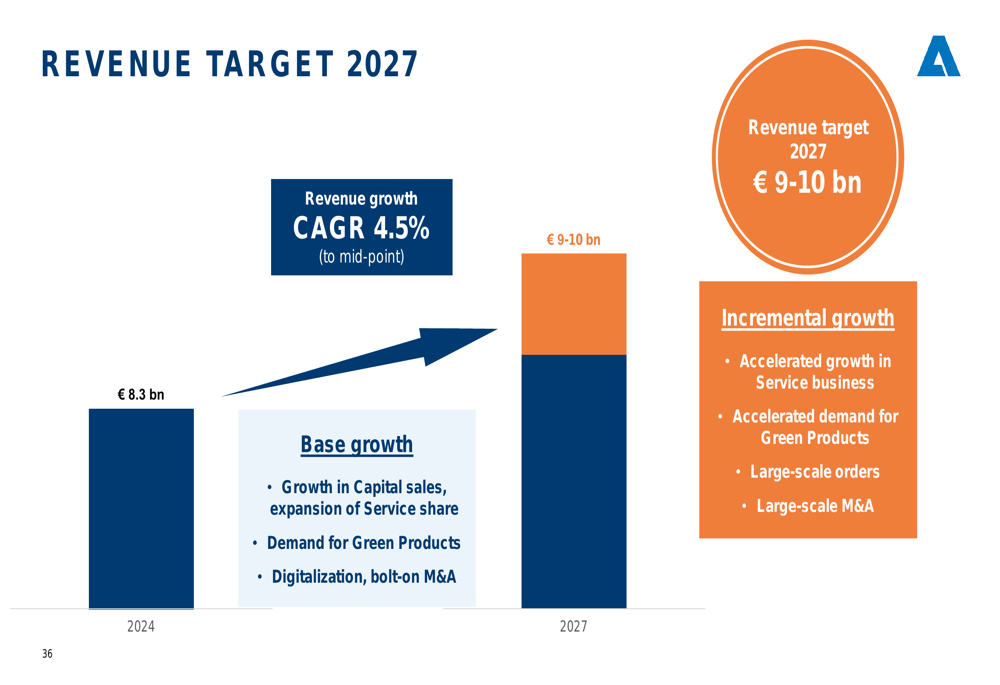

For the medium term, Andritz confirmed its 2027 targets of €9-10 billion in revenue and a comparable EBITA margin exceeding 9%. The revenue growth is expected to come from both base growth (expansion of service share, demand for green products, digitalization, and bolt-on acquisitions) and incremental growth opportunities (accelerated service business growth, increased demand for green products, large-scale orders, and major acquisitions).

As shown in the following chart of revenue targets for 2027:

The company also provided specific comparable EBITA margin targets for each business area by 2027:

- Pulp & Paper: 11-13%

- Metals: 6-8%

- Hydropower: 7-9%

- Environment & Energy: 10-13%

Summary

Andritz’s Q2/H1 2025 financial results present a mixed but generally positive picture, with strong order intake growth offsetting revenue declines while maintaining stable profitability. The company’s strategic focus on increasing its service business share and complementary acquisitions appears to be yielding results, contributing to resilience in challenging market conditions.

The comprehensive summary of key figures provides a clear overview of the company’s performance:

While facing near-term challenges including revenue declines and restructuring costs, Andritz’s growing order backlog, stable margins, and strategic initiatives position the company well for future growth. Management’s confirmation of both 2025 guidance and 2027 targets reflects confidence in the company’s long-term strategy and market positioning.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.