U.S. stocks rise on Fed cut bets; earnings continue to flow

Introduction & Market Context

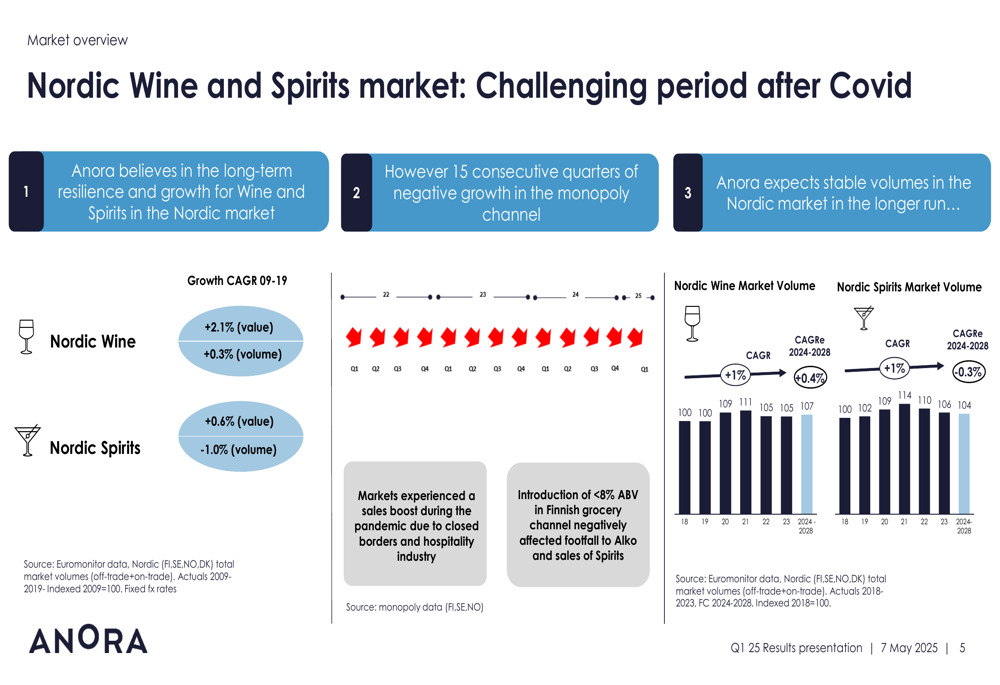

Anora Group Oyj presented its first quarter 2025 results on May 7, 2025, highlighting a challenging Nordic wine and spirits market that continues to face headwinds. CEO Kirsi Puntila and CFO Stein Eriksen delivered the presentation, noting that the company has experienced 15 consecutive quarters of negative growth in the monopoly channel, though they maintain belief in the long-term resilience of the Nordic market.

The company operates in a market expected to show modest growth in the coming years, with Nordic wine market volume projected at a CAGR of +1% from 2024-2028, and Nordic spirits at the same rate. However, current market conditions remain difficult, as reflected in the quarterly results.

As shown in the following overview of the Nordic wine and spirits market:

Quarterly Performance Highlights

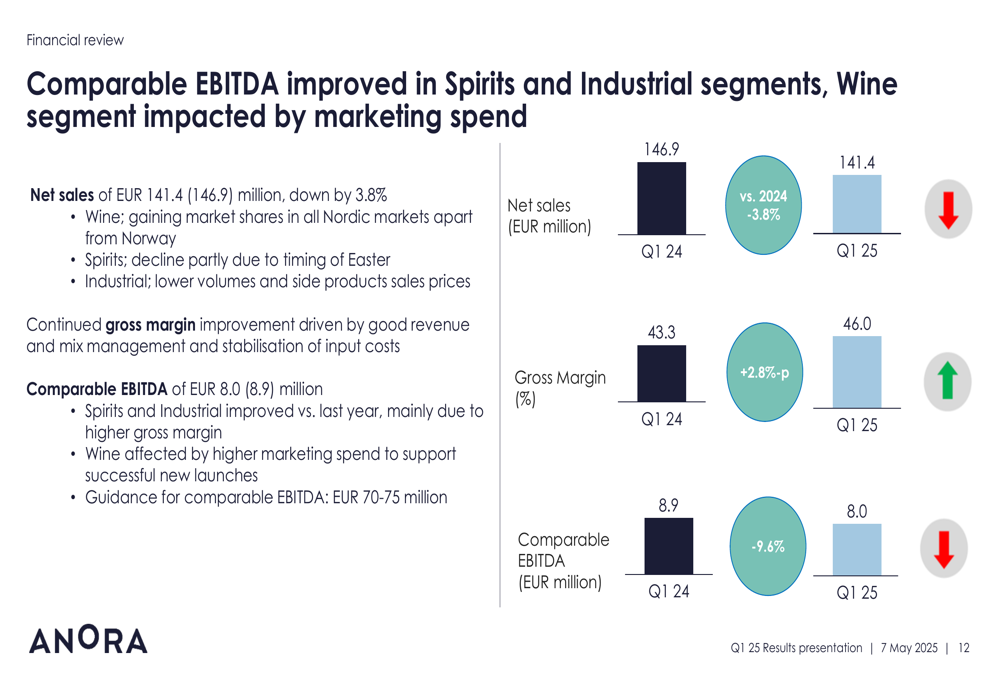

Anora reported net sales of €141.4 million for Q1 2025, representing a 3.8% decrease compared to €146.9 million in Q1 2024. Despite this decline, the company achieved a significant improvement in gross margin, which rose to 46.0% from 43.3% in the previous year, driven by revenue management and stabilization of input costs.

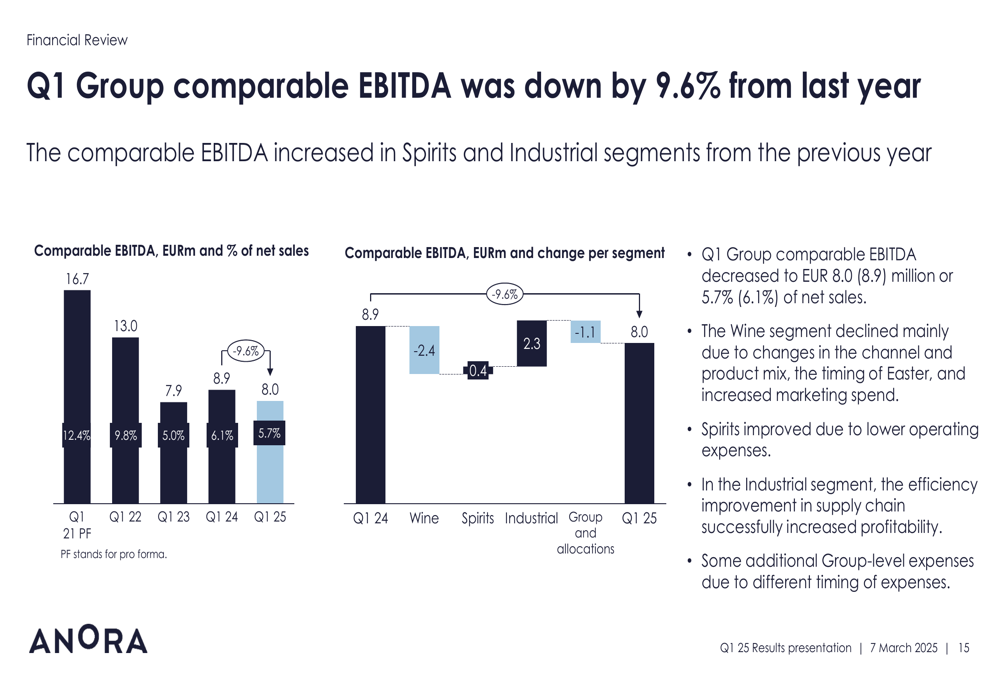

Comparable EBITDA decreased to €8.0 million (down 9.6% year-over-year), with a margin of 5.7% compared to 6.1% in Q1 2024. The company maintained its full-year 2025 guidance for comparable EBITDA at €70-75 million.

The following chart illustrates the company’s key financial metrics for the quarter:

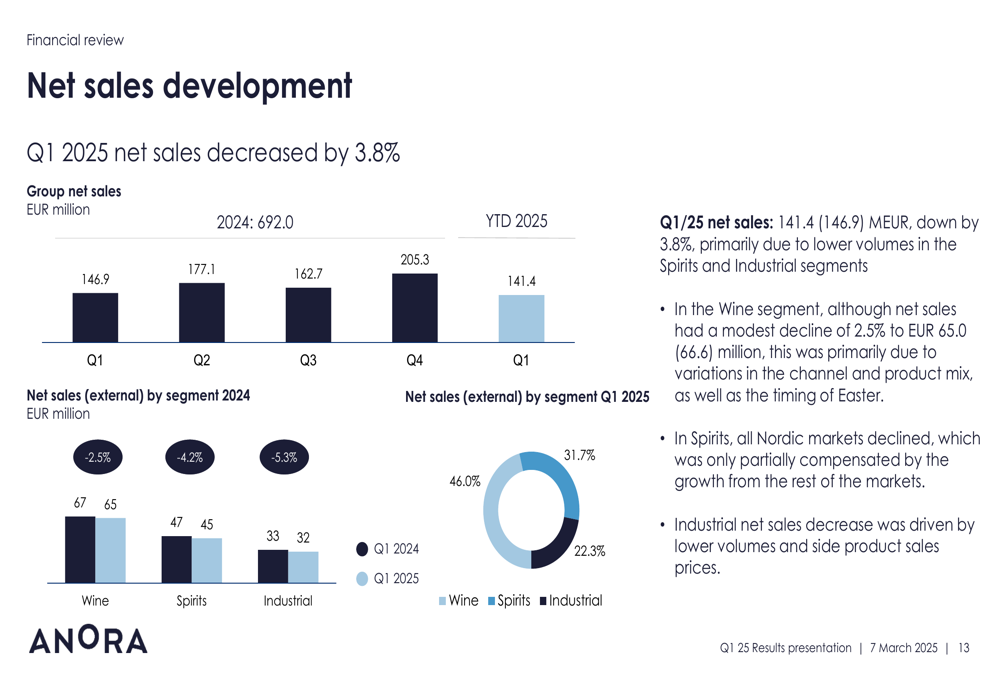

Net sales development showed declines across all segments, with the timing of Easter cited as a partial explanation for lower spirits sales. The quarterly breakdown reveals the continuing challenges in generating top-line growth:

Segment Performance Analysis

Anora’s performance varied significantly across its three business segments:

The Wine segment experienced a modest 2.5% decline in net sales to €65.0 million, with stable sales volume. However, comparable EBITDA fell dramatically to €0.2 million (0.4% margin) from €2.6 million (4.0% margin) in Q1 2024, primarily due to increased marketing spend for new product launches. The company did highlight market share gains in three of four Nordic markets as a positive development.

The Spirits segment saw net sales decrease by 4.5% to €44.9 million, with declines across all Nordic markets. Despite this, comparable EBITDA improved to €7.2 million (16.0% margin) from €6.8 million (14.5% margin), benefiting from lower operating expenses. Notably, Koskenkorva’s net sales grew year-over-year, now representing over 17% of total Spirits sales, and international markets showed increased sales.

The Industrial segment reported a 5.3% decline in external net sales to €31.5 million, with total net sales (including internal) falling to €50.6 million. Despite lower volumes and side product sales prices, comparable EBITDA increased significantly to €3.1 million (6.2% margin) from €0.8 million (1.5% margin).

The following chart shows the quarterly comparable EBITDA performance:

Financial Position and Outlook

Anora’s financial position showed some strain in Q1 2025. The operational cash flow deteriorated to -€76 million from -€45 million in the same period of 2024. Interest-bearing net debt increased to €208 million from €177 million, resulting in a leverage ratio (Net Debt/Comparable EBITDA) of 3.1x, up from 2.6x.

Liquidity reserves decreased to €267 million from €336 million year-over-year, while net working capital remained at a relatively low level of 1% of net sales (€8.7 million).

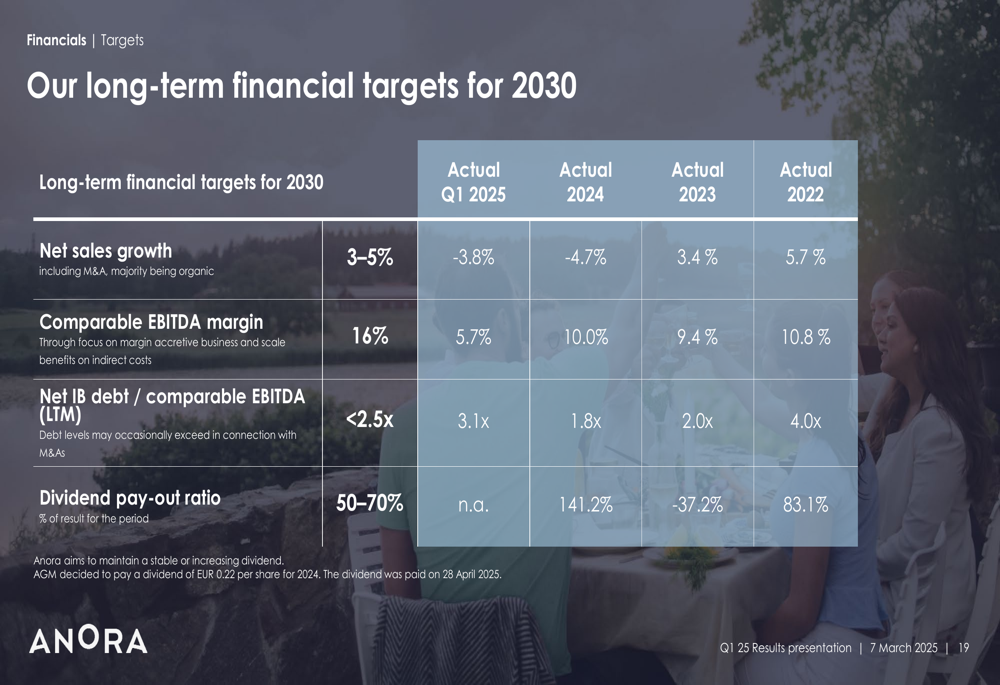

The company’s current performance remains significantly below its long-term financial targets for 2030, which include net sales growth of 3-5% (vs. -3.8% in Q1 2025), comparable EBITDA margin of 16% (vs. 5.7%), and net interest-bearing debt/comparable EBITDA of less than 2.5x (vs. 3.1x).

As shown in the following comparison of targets versus actual performance:

Strategic Initiatives and Priorities

Anora highlighted several strategic initiatives and priorities for 2025 and beyond. The company is focusing on gaining market share in challenging markets, as evidenced by the successful launch of Koskenkorva long drinks and Chill Out brand products. In the Industrial segment, Anora announced plans to invest in a new biomass boiler for the Koskenkorva Distillery to transition to fossil-emission-free fuels, underscoring its commitment to sustainability.

For 2025, the company expects volumes to remain flat, with priorities centered on improving profitability, strengthening cash position and balance sheet, and restoring organic net sales growth. Management emphasized the continued strong development in gross margin as a positive sign amid challenging market conditions.

The following slide summarizes the company’s key takeaways and future priorities:

Anora’s next financial update will come with its Half-year Report for Q2 2025, scheduled for August 15, 2025, where investors will be watching closely for signs of improvement in sales trends and continued margin expansion.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.