Street Calls of the Week

Introduction & Market Context

Antero Midstream Corp (NYSE:AM) presented its second quarter 2025 earnings on July 31, highlighting strong financial performance and strategic positioning amid growing demand for natural gas infrastructure. Despite the positive results, the stock fell 2.07% in aftermarket trading to $18.38, reflecting broader market sentiment rather than company-specific concerns.

The midstream operator continues to benefit from its strategic position in the Appalachian Basin, with particular focus on supporting growing LNG exports and regional demand from data centers. The company’s presentation emphasized its operational efficiency and capital discipline as key drivers of financial performance.

Quarterly Performance Highlights

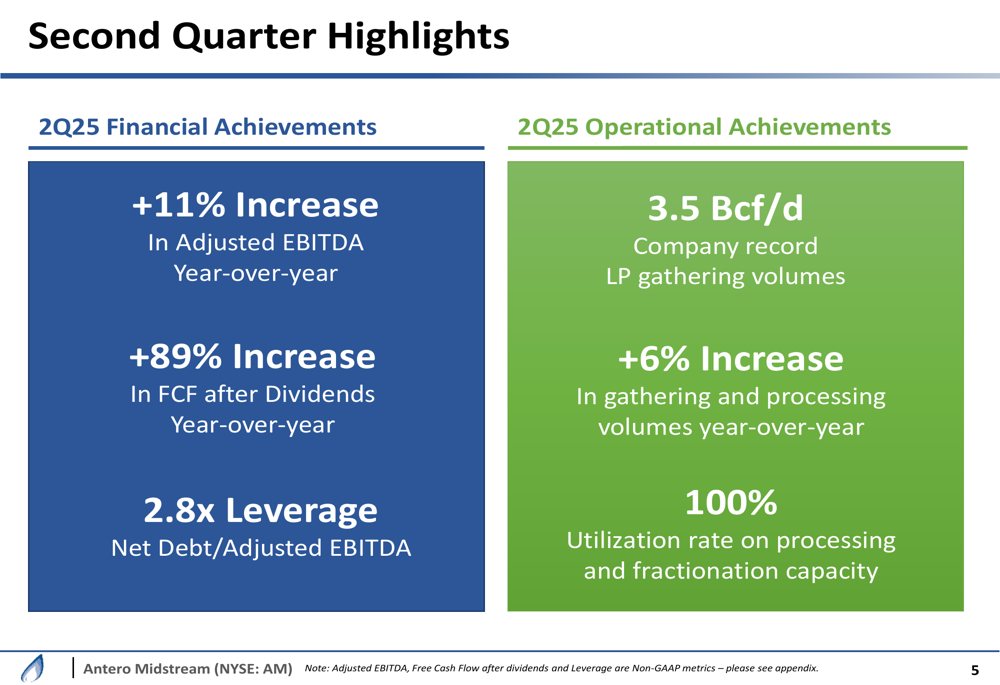

Antero Midstream reported substantial year-over-year improvements across key financial and operational metrics for the second quarter of 2025. The company achieved an 11% increase in Adjusted EBITDA and an impressive 89% jump in free cash flow after dividends compared to Q2 2024.

As shown in the following quarterly highlights slide, the company maintained strong financial discipline while delivering record operational performance:

The financial achievements were supported by robust operational performance, including company record low-pressure gathering volumes of 3.5 Bcf/d and a 6% year-over-year increase in gathering and processing volumes. The company also reported 100% utilization of its processing and fractionation capacity, indicating strong demand for its services.

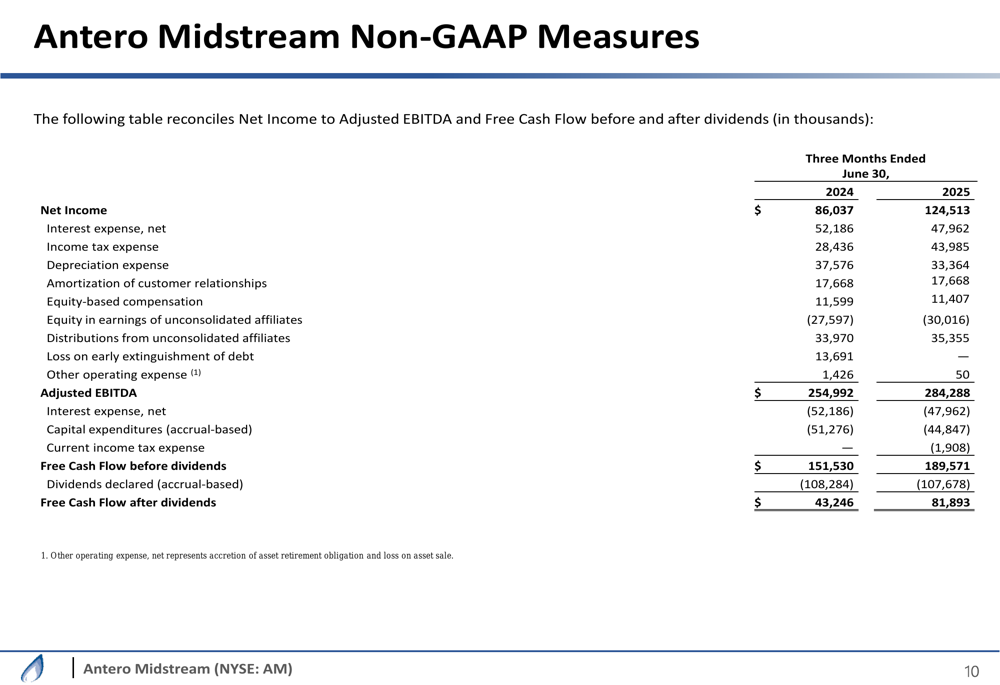

The detailed reconciliation of financial metrics shows net income increased from $86.0 million in Q2 2024 to $124.5 million in Q2 2025, while Adjusted EBITDA rose from $255.0 million to $284.3 million over the same period:

Capital Allocation and Financial Guidance

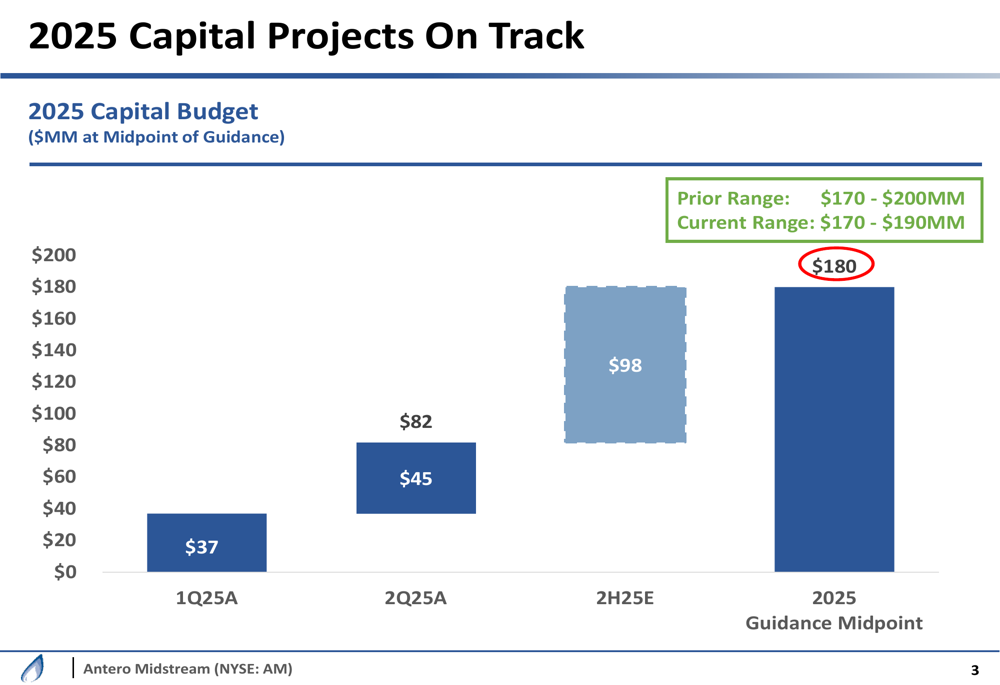

Antero Midstream demonstrated disciplined capital management by tightening its 2025 capital budget range from $170-200 million to $170-190 million, maintaining the $180 million midpoint. This reflects the company’s ongoing focus on capital efficiency while supporting growth initiatives.

The capital budget breakdown by quarter shows controlled spending throughout the year:

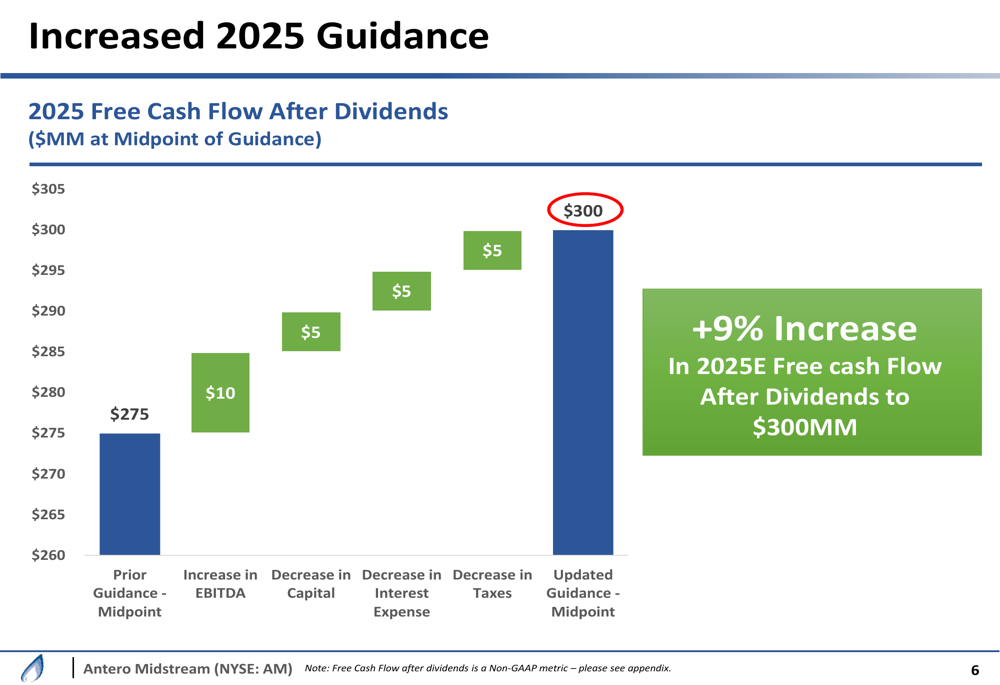

In a significant development, Antero Midstream raised its 2025 free cash flow after dividends guidance by 9% to $300 million, up from the previous guidance of $275 million. This increase is attributed to multiple factors including higher EBITDA, lower capital expenditures, reduced interest expense, and decreased taxes:

The company’s balance sheet continues to strengthen, with leverage reduced to 2.8x net debt to adjusted EBITDA as of June 30, 2025, positioning Antero Midstream as one of the lowest leveraged midstream operators in the sector.

Strategic Growth Initiatives

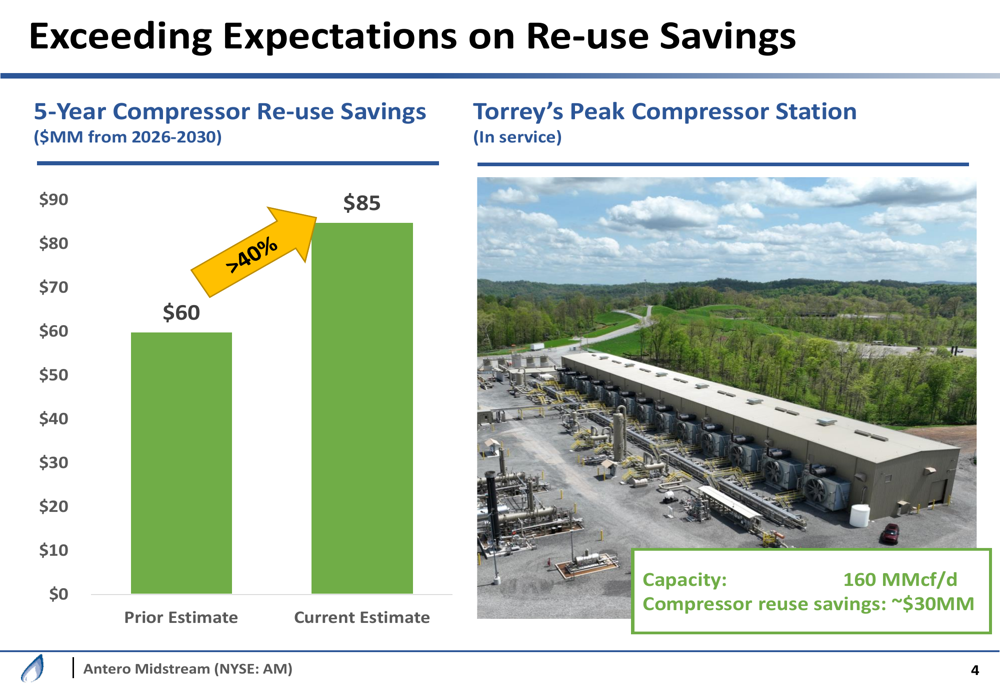

Antero Midstream highlighted its strategic focus on cost efficiency through infrastructure reuse. The company increased its projected 5-year compressor reuse savings for 2026-2030 by over 40%, from $60 million to $85 million, demonstrating its commitment to capital efficiency:

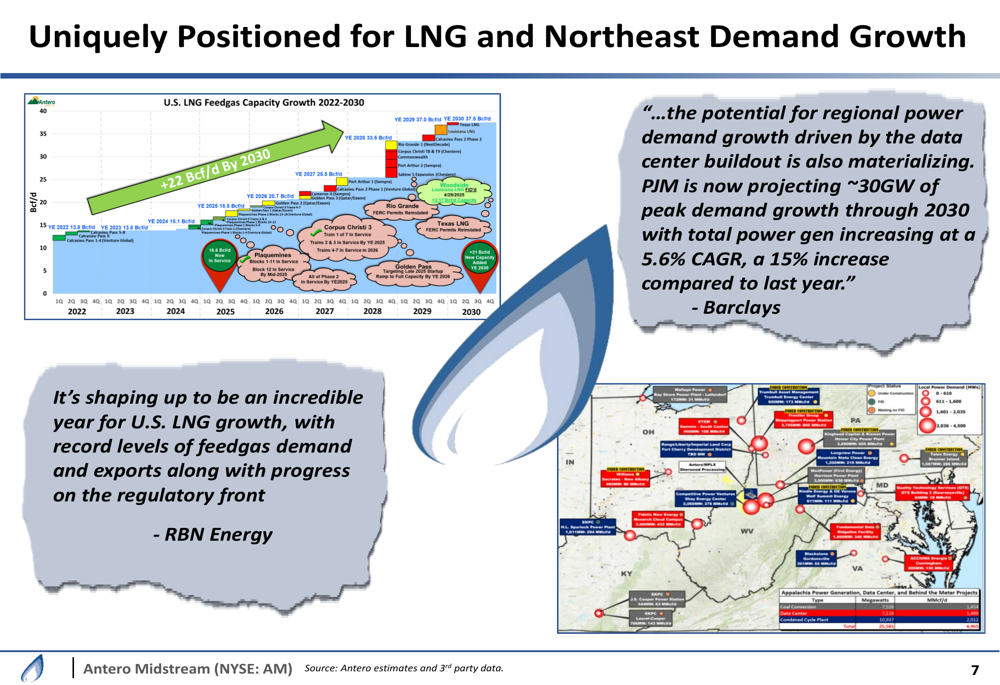

Looking ahead, the company is strategically positioning itself to benefit from significant growth in U.S. LNG export capacity and increasing regional demand, particularly from data centers in the Northeast. The presentation highlighted projections for LNG feedgas capacity to increase by 22 Bcf/d by 2030:

During the earnings call, management confirmed ongoing assessments of bolt-on acquisition opportunities and discussed processing capacity utilization, indicating room for growth beyond current capabilities. CEO Paul Rady emphasized the company’s "commitment to its organic growth plan, consistently delivering predictable earnings and peer-leading capital efficiency."

Forward-Looking Statements

Antero Midstream’s increased guidance reflects management’s confidence in the company’s operational strategy and market positioning. With no material cash taxes expected through 2028 and a strong financial health profile, the company appears well-positioned to continue its growth trajectory.

The company’s focus on supporting LNG exports and regional demand growth, particularly from data centers, provides a clear strategic direction. However, potential challenges remain, including market volatility, regulatory changes in the energy sector, and competition in the midstream space.

CFO Brendan Krueger highlighted the company’s financial advantage during the earnings call, noting, "We’re the lowest levered midstream name in the space, and we think that debt pay down does accrue to the equity still as we look at that today."

With its disciplined capital allocation, operational efficiency, and strategic positioning for future growth, Antero Midstream continues to demonstrate strong financial performance while maintaining a clear vision for long-term value creation.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.