Domino’s Pizza Australia rejects Bain Capital takeover report after share surge

Introduction & Market Context

Antero Resources Corp (NYSE:AR) presented its second quarter 2025 earnings on July 31, 2025, highlighting significant financial improvements and strategic positioning in the natural gas market. The company’s stock responded positively, rising 2.54% to close at $33.82, with additional gains of 1.15% in pre-market trading.

This quarter marks a substantial turnaround from Q1 2025, when Antero missed earnings expectations with EPS of $0.66 against forecasts of $0.77. The Q2 presentation demonstrates how the company has leveraged operational efficiencies and strategic market positioning to improve its financial performance.

Quarterly Performance Highlights

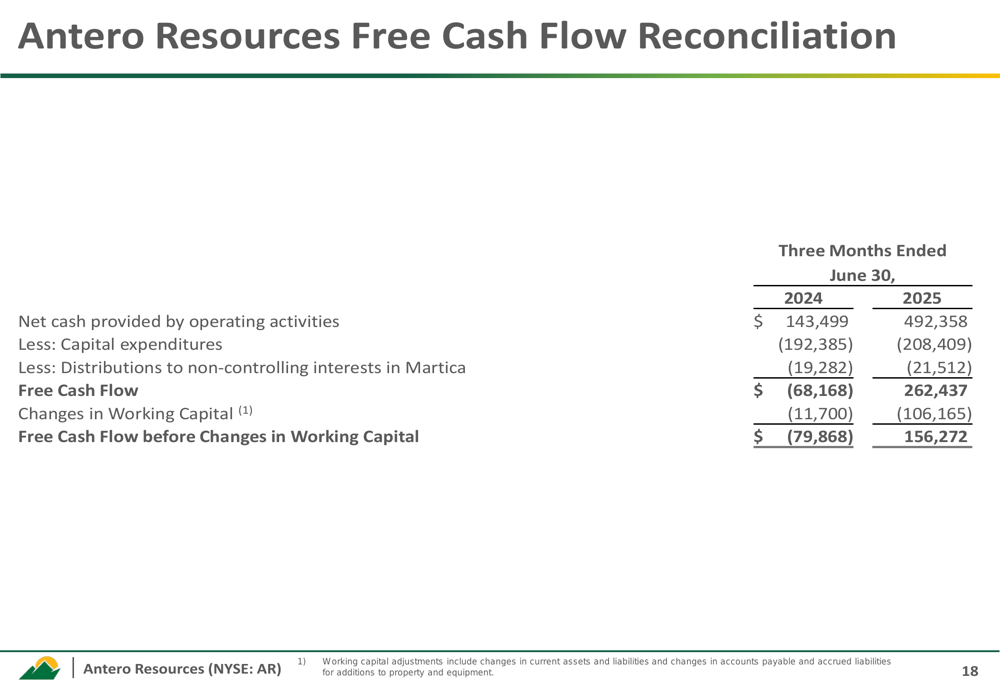

Antero Resources reported a dramatic improvement in its financial results compared to the same period last year. The company posted net income of $156.6 million for Q2 2025, a significant recovery from the $79.8 million loss recorded in Q2 2024.

Free cash flow showed a remarkable turnaround, reaching $262.4 million in Q2 2025 compared to negative $68.2 million in the same quarter last year. This improvement reflects both stronger operational performance and more favorable market conditions.

As shown in the following chart of the company’s free cash flow reconciliation:

Adjusted EBITDAX more than doubled year-over-year, increasing from $151.4 million in Q2 2024 to $379.5 million in Q2 2025, demonstrating the company’s enhanced operational efficiency and improved pricing environment.

Operational Efficiencies

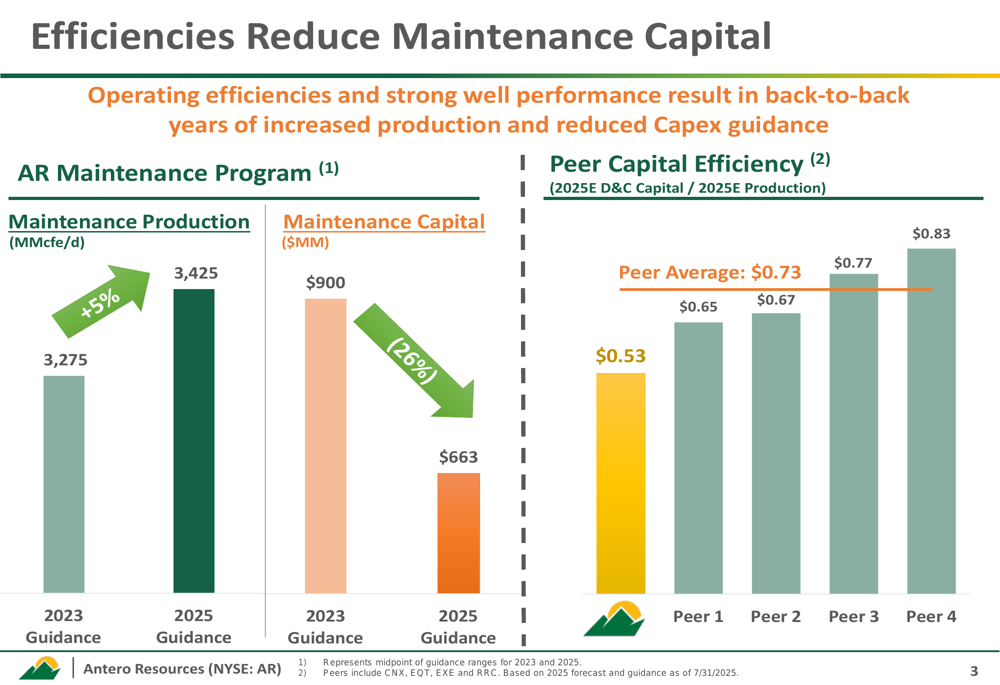

A key driver of Antero’s improved performance has been its focus on operational efficiencies, which have significantly reduced maintenance capital requirements while increasing production.

The company’s presentation highlights how maintenance production increased by 5% from 2023 guidance to 2025 guidance, while maintenance capital decreased by 26% over the same period. This efficiency translates to a capital efficiency metric of $0.53, substantially better than the peer average of $0.73.

As illustrated in the following efficiency metrics comparison:

For 2025, Antero has provided guidance of 3.40-3.45 Bcfe/d in net production, with capital expenditures of $650-675 million for drilling and completion activities. The company plans to operate with an average of 2.0 rigs and 1.0-2.0 completion crews, drilling 50-55 net wells and completing 60-65 net wells during the year.

Strategic Positioning for Future Growth

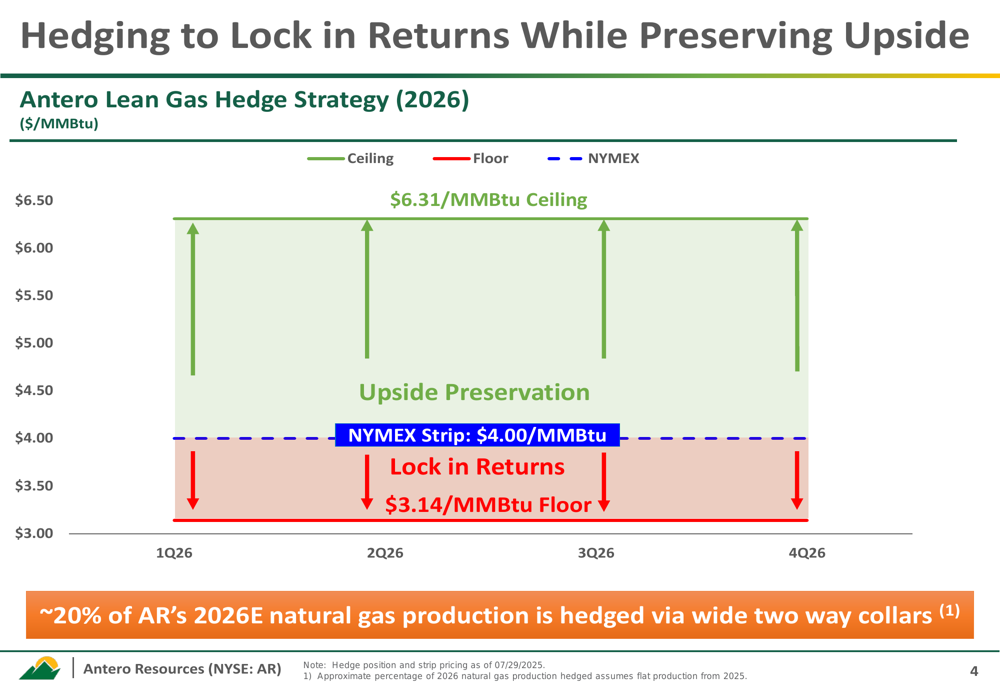

Antero has implemented a strategic hedging approach to lock in returns while preserving upside potential. Approximately 20% of the company’s 2026E natural gas production is hedged via wide two-way collars, with a ceiling at $6.31/MMBtu and a floor at $3.14/MMBtu, providing downside protection while allowing for significant upside participation.

The company’s hedging strategy is visualized in this chart:

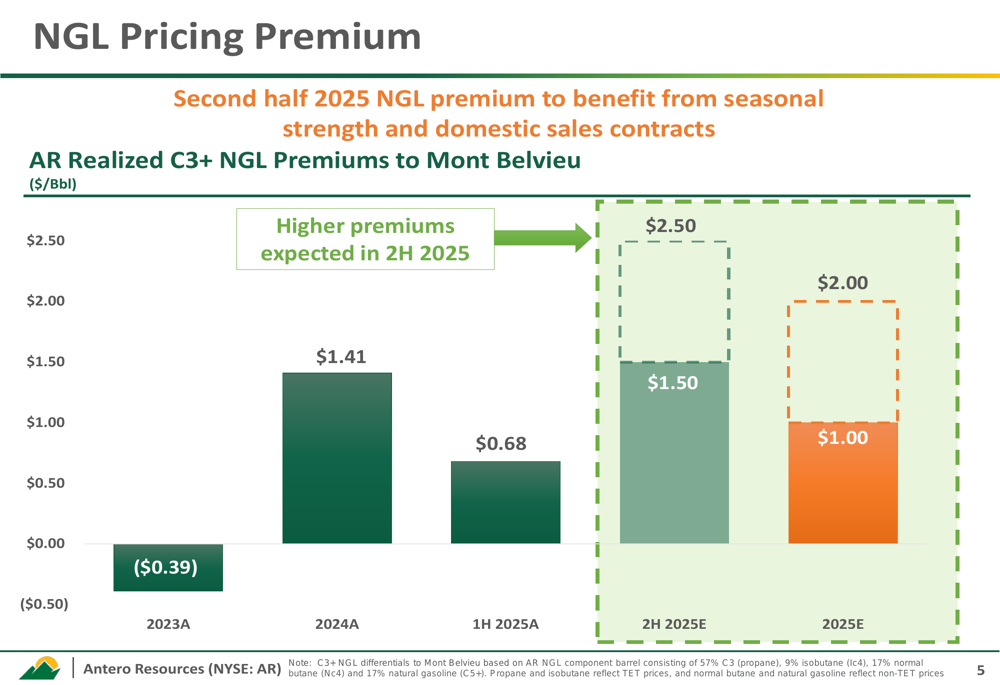

Antero has positioned itself to benefit from premium NGL pricing, projecting a $1.00/Bbl premium to Mont Belvieu for 2025E, with higher premiums expected in the second half of 2025 due to seasonal strength and domestic sales contracts.

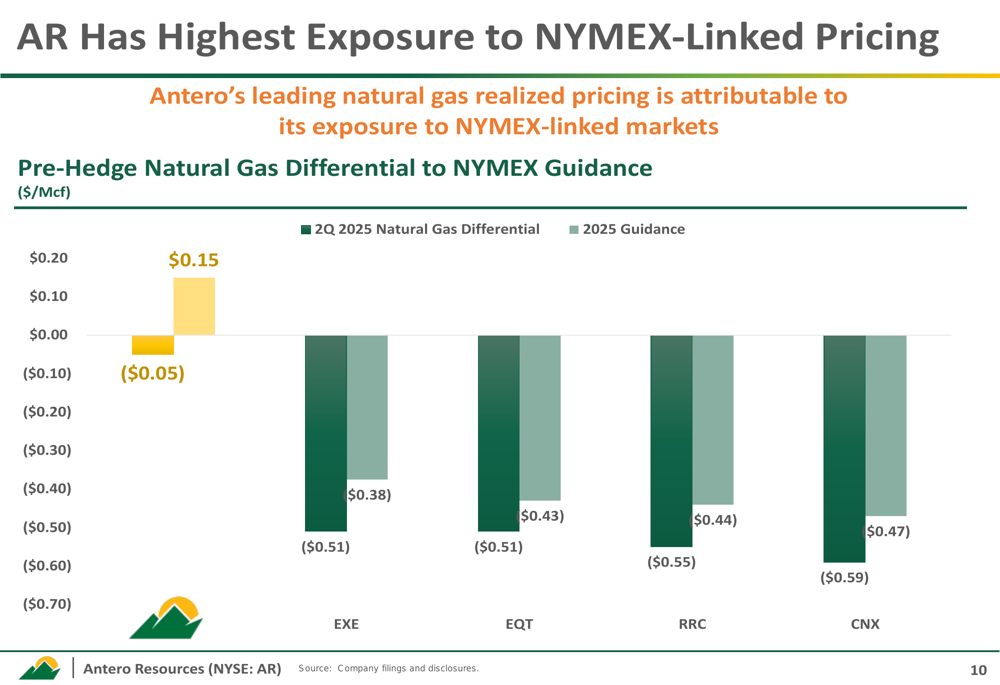

The company also highlighted its advantageous position regarding NYMEX-linked pricing, showing the best differential to NYMEX among its peer group for both Q2 2025 and full-year 2025 guidance.

Antero is strategically positioned to benefit from upcoming LNG capacity additions, with 8 Bcf/d of new capacity expected by the end of 2027. This aligns with statements from CFO Mike Kennedy in the Q1 earnings call, where he noted, "We’ve never really seen a better setup from a natural gas demand growth over the coming quarters, years versus supply."

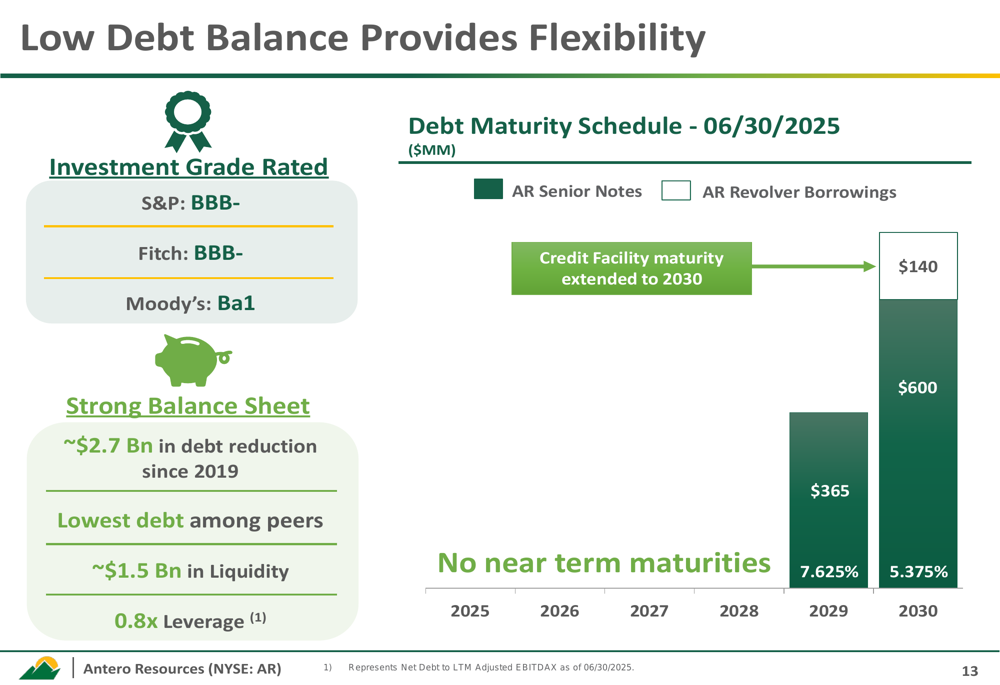

Balance Sheet Strength and Debt Reduction

Antero continues to strengthen its balance sheet, reducing net debt to $1.1 billion as of June 30, 2025, down from $1.5 billion at the end of 2024. This represents a continuation of the company’s long-term debt reduction strategy, with approximately $2.7 billion in debt reduction since 2019.

The company maintains investment grade ratings (S&P:BBB-, Fitch: BBB-, Moody’s: Ba1) and has a strong liquidity position of approximately $1.5 billion with a leverage ratio of 0.8x.

As shown in the following debt maturity schedule:

This debt reduction aligns with statements made during the Q1 earnings call, where the company emphasized its balanced approach between debt reduction and share buybacks. In Q1, Antero reduced debt by over $200 million and repurchased $92 million in stock, representing nearly 1% of shares outstanding.

Forward-Looking Statements

Looking ahead, Antero is well-positioned to capitalize on increasing regional natural gas demand, particularly from power generation and data centers. The company projects approximately 5.0 Bcf/d of power demand increase from 2026 to 2030 and beyond.

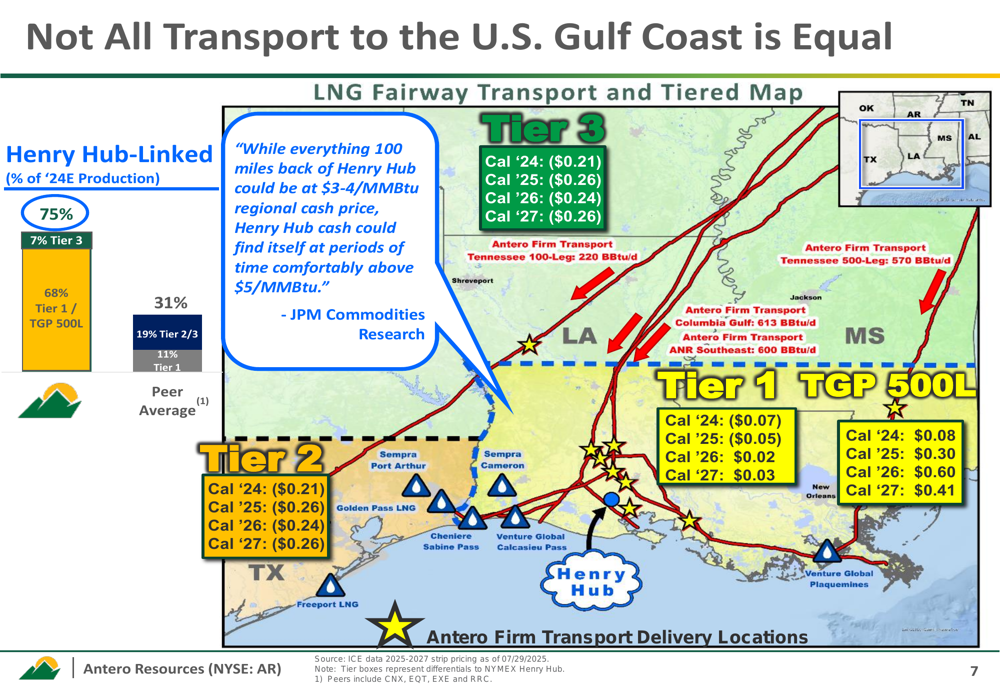

The company’s transportation infrastructure provides a competitive advantage, with 75% of 2024E production being Henry Hub-linked. Antero’s tiered transportation map shows how its strategic positioning allows for favorable pricing differentials compared to peers.

New LNG capacity additions and export infrastructure developments are expected to support stronger pricing in the coming years. New Gulf Coast LPG export capacity coming online in Q3 2025 is anticipated to alleviate export constraints, potentially strengthening benchmark NGL prices.

With its operational efficiencies, strategic market positioning, and strengthened balance sheet, Antero Resources appears well-equipped to navigate market challenges while capitalizing on emerging opportunities in the natural gas sector.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.