Futures slip, bank earnings ahead, Powell to speak - what’s moving markets

Introduction & Market Context

Aramis Group (EPA:ARAMI) reported a 3% year-over-year increase in revenue for the third quarter of 2025, reaching €591 million despite a broader market slowdown. The European used car specialist demonstrated resilience in a challenging environment where the overall market for used cars under 8 years old declined by 6% across its six operating geographies.

The company’s shares responded positively to the results, trading up 3.38% following the July 25 presentation, as investors appeared to appreciate Aramis Group’s ability to outperform the market and maintain its growth trajectory.

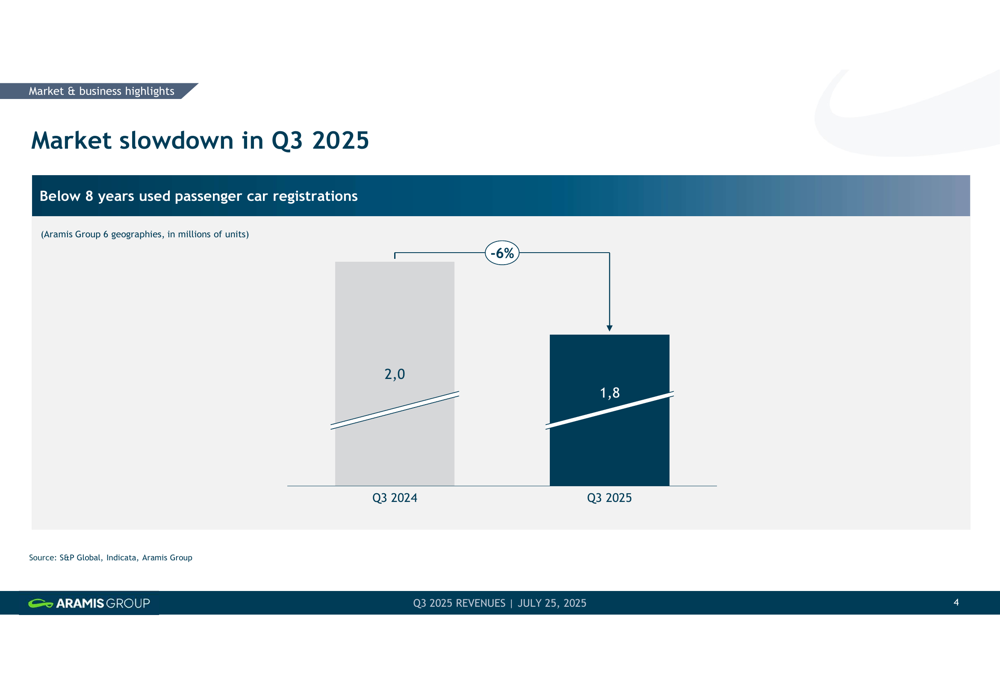

As shown in the following chart illustrating the market conditions, Aramis Group faced significant headwinds with the used car market contracting from 2.0 million units in Q3 2024 to 1.8 million units in Q3 2025:

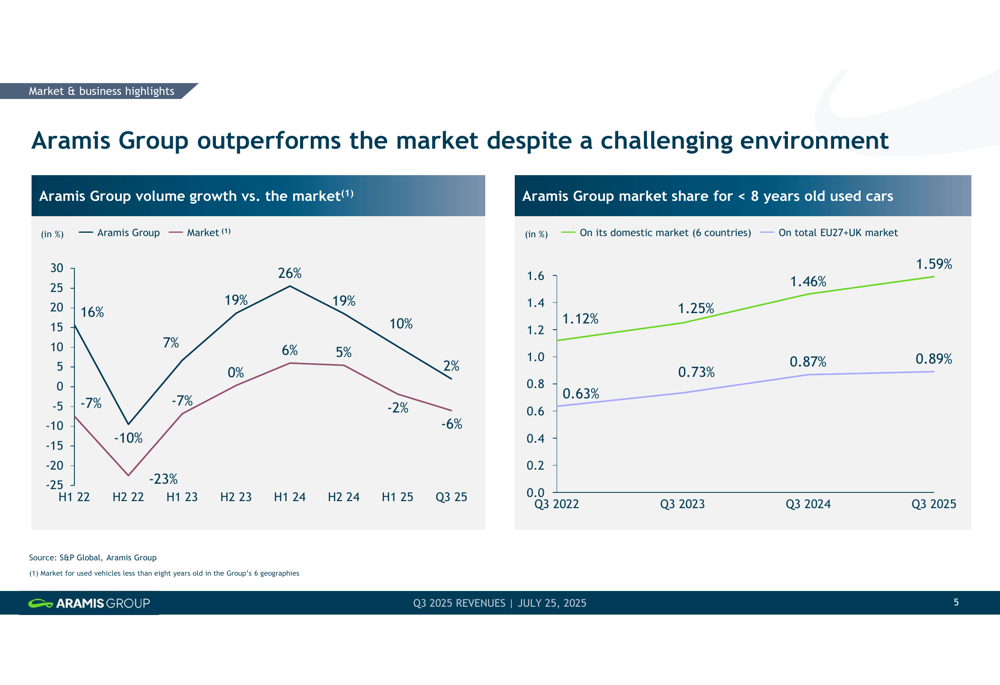

Despite these challenging conditions, Aramis Group managed to increase its B2C volumes by 2% year-over-year, representing an 8 percentage point outperformance compared to the broader market. This outperformance has become a consistent pattern for the company, as demonstrated in the following chart showing both volume growth compared to the market and increasing market share:

Quarterly Performance Highlights

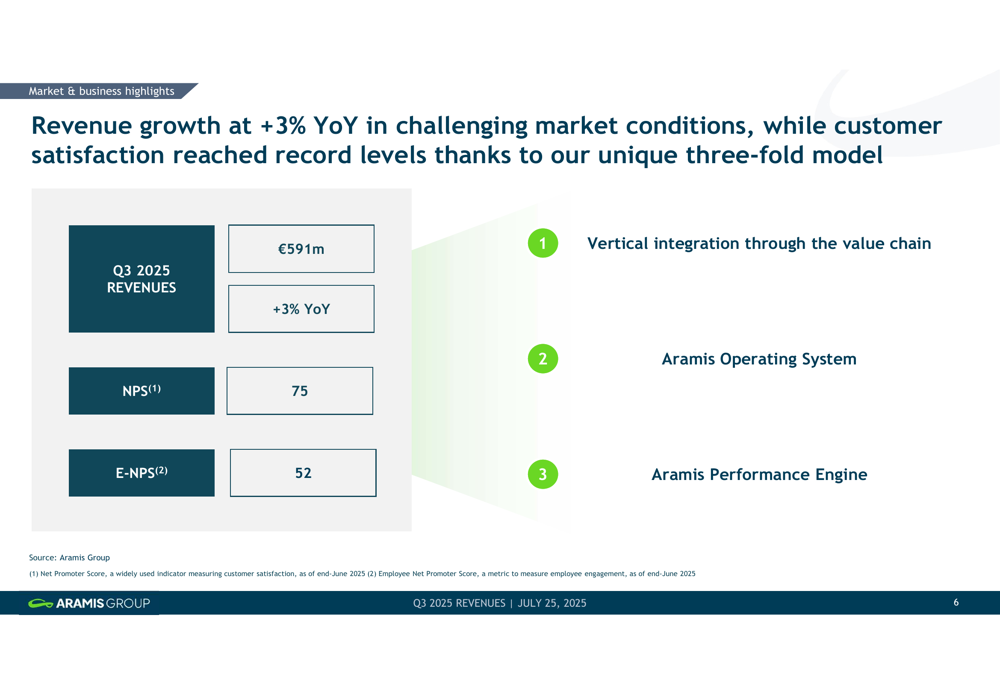

Aramis Group’s revenue growth was accompanied by strong customer satisfaction metrics, with the company achieving a Net Promoter Score (NPS) of 75 and an employee Net Promoter Score (eNPS) of 52, both at record levels. The company attributes its performance to three key strategic elements: vertical integration through the value chain, its proprietary Aramis Operating System, and the Aramis Performance Engine.

The following slide highlights these achievements and strategic pillars:

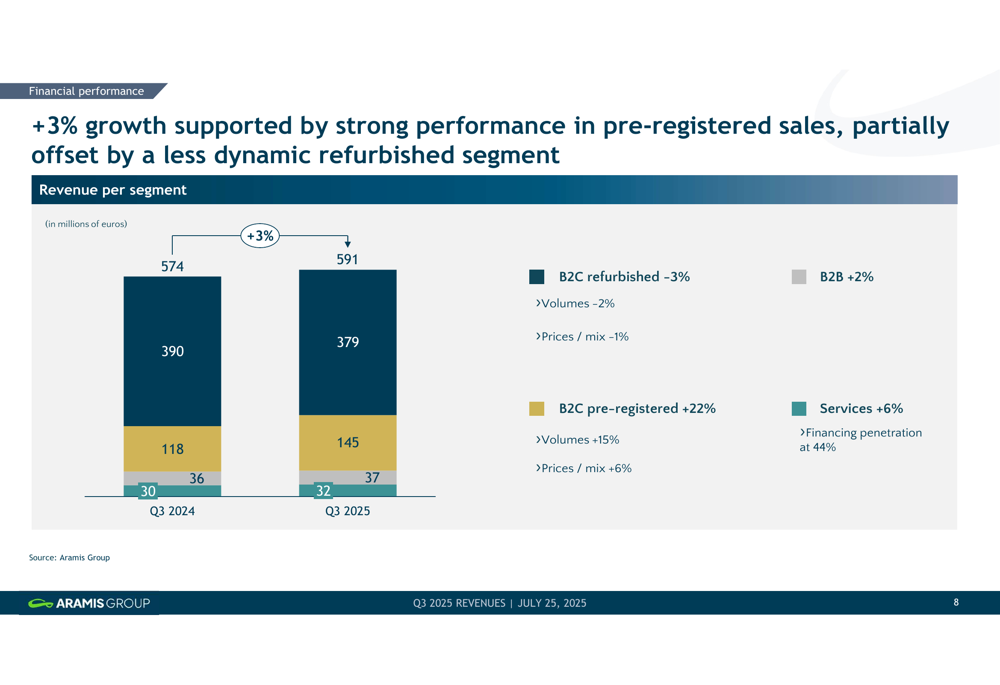

The company’s performance varied significantly across its business segments. While the B2C refurbished segment, which represents the core of Aramis Group’s business, experienced a 3% decline (with volumes down 2% and prices/mix down 1%), this was more than offset by strong growth in the B2C pre-registered segment, which surged 22% with volumes up 15% and prices/mix contributing an additional 6%. The B2B segment grew by 2%, while services increased by 6% with financing penetration reaching 44%.

This segment breakdown is illustrated in the following chart:

Detailed Financial Analysis

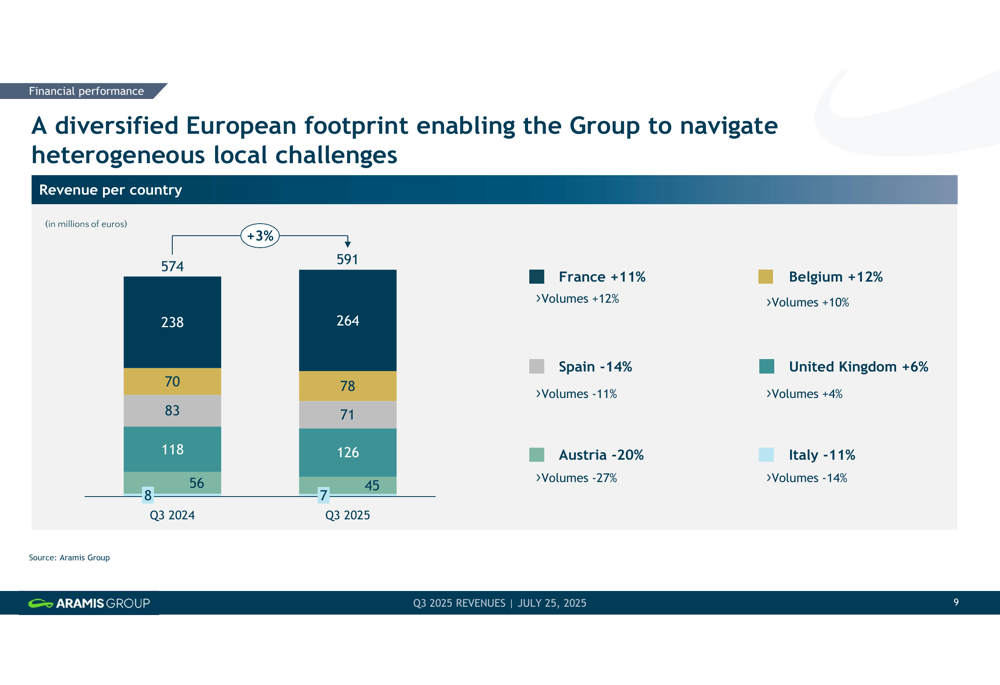

Geographically, Aramis Group’s performance revealed a tale of two markets. France and Belgium delivered robust double-digit growth, with revenues increasing by 11% and 12% respectively. However, this strong performance was partially offset by challenges in other markets, particularly Spain (-14%) and Austria (-20%).

The following chart provides a comprehensive breakdown of revenue by country:

The company provided additional context for its underperforming markets. In Austria, the negative performance was attributed to an exceptional 2024 due to earn-out context and management transitions, including the appointment of a new co-CEO in July 2024 and the planned departure of the founder in January 2025. The company is now focusing on consolidating its management team and diversifying sourcing channels in this market.

In the United Kingdom (TADAWUL:4280), Aramis Group is prioritizing unit profitability over volume growth in the short term. Despite this approach, the UK operation (CarSupermarket.com) achieved 15% B2C volume growth in H1 2025 compared to H1 2024, outpacing the group’s overall 10% growth. However, its EBITDA margin of 1.3% remains below the group average of 2.7%, highlighting the need for continued operational improvements.

Strategic Initiatives

Aramis Group’s strategy centers on profitable growth rather than pure volume expansion. This approach is particularly evident in markets like the UK and Italy, where the company is focusing on improving unit economics. The two-pillar strategy consists of:

1. Converging and leveraging the European platform to achieve economies of scale

2. "Raising the bar" by empowering customers and teams

The company’s investment case emphasizes its entrepreneurial vision, vast market potential, customer-centric value proposition, unique business model, and clear strategy for profitable growth:

Sustainability also features prominently in Aramis Group’s strategic positioning. The company frames its business model as providing affordable and lower-impact mobility options for customers, scalable solutions for ecological transition, meaningful work for employees, and measurable impact with long-term value for investors:

Forward-Looking Statements

For the remainder of 2025, Aramis Group expects moderate growth driven primarily by France and Belgium amid the continued market slowdown. The company is implementing targeted efforts to address operational challenges in Austria and Spain while maintaining its focus on unit profitability in the UK.

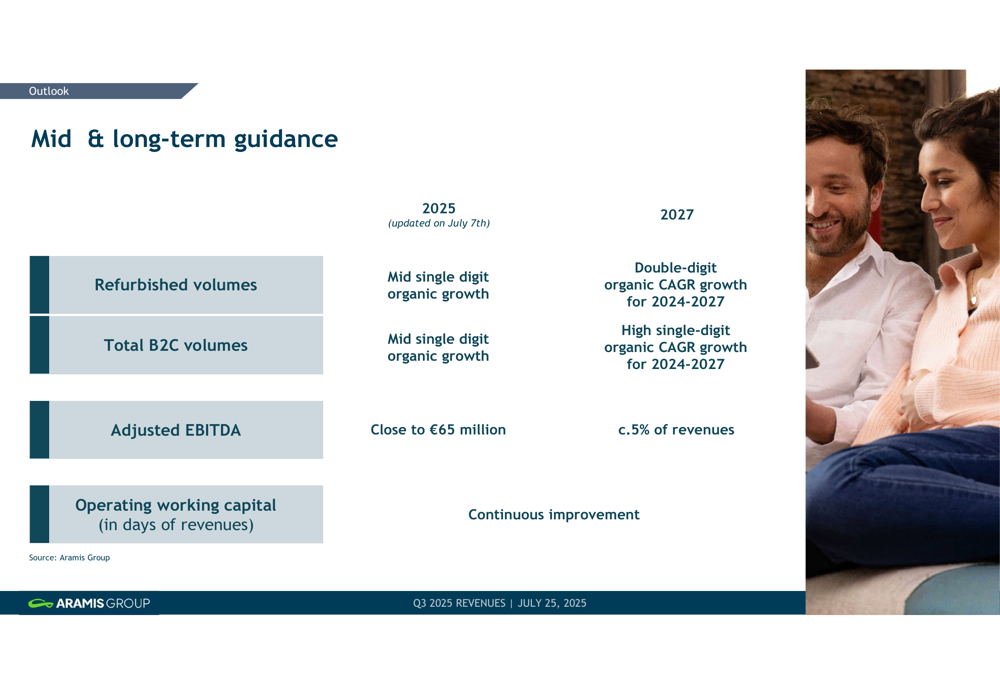

The company’s updated 2025 guidance calls for mid-single-digit organic growth in both refurbished volumes and total B2C volumes, with adjusted EBITDA expected to be close to €65 million. Looking further ahead to 2027, Aramis Group targets double-digit organic CAGR growth for 2024-2027 and aims to achieve an adjusted EBITDA margin of approximately 5% of revenues.

The following slide details these mid and long-term targets:

Aramis Group’s next financial communication is scheduled for November 26, 2025, when the company will release its full-year 2025 results.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.