Wall St futures flat amid US-China trade jitters; bank earnings in focus

Introduction & Market Context

Arla Plast AB (STO:ARPL) reported a significant revenue increase in its Q1 2025 interim presentation on April 29, though profitability metrics showed pressure. The company’s stock fell 3.77% to 48.5 SEK following the announcement, suggesting investors focused on margin contraction rather than top-line growth.

The Swedish plastic sheet manufacturer’s results reflected broader European market weakness, with the company noting decreased volumes across the entire sector while maintaining its market share. The acquisition of Nudec S.A.U., completed in April 2024, substantially impacted financial results.

Quarterly Performance Highlights

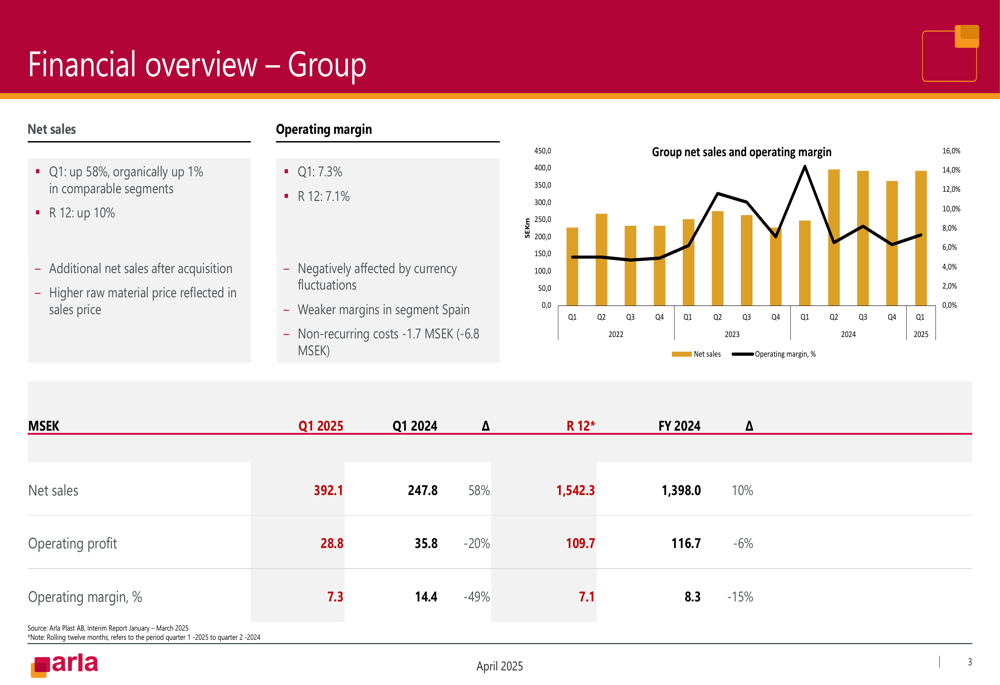

Arla Plast reported Q1 2025 net sales of 392.1 MSEK, a 58% increase from 247.8 MSEK in the same period last year. However, organic growth in comparable segments was just 1%, highlighting the acquisition’s dominant role in revenue expansion.

Operating profit decreased 20% to 28.8 MSEK (Q1 2024:35.8 MSEK), while operating margin contracted significantly to 7.3% from 14.4% in the prior-year period. The company attributed this decline to currency fluctuations, weaker margins in the Spain segment, and non-recurring costs of 1.7 MSEK.

As shown in the following chart of group financial performance:

Cash flow from operating activities remained positive at 16.5 MSEK but decreased from 27.3 MSEK in Q1 2024. The company maintained a strong financial position with a net cash position of 24.5 MSEK, though this was substantially lower than the 106.6 MSEK reported a year earlier, reflecting the Nudec acquisition investment.

Segment Performance Analysis

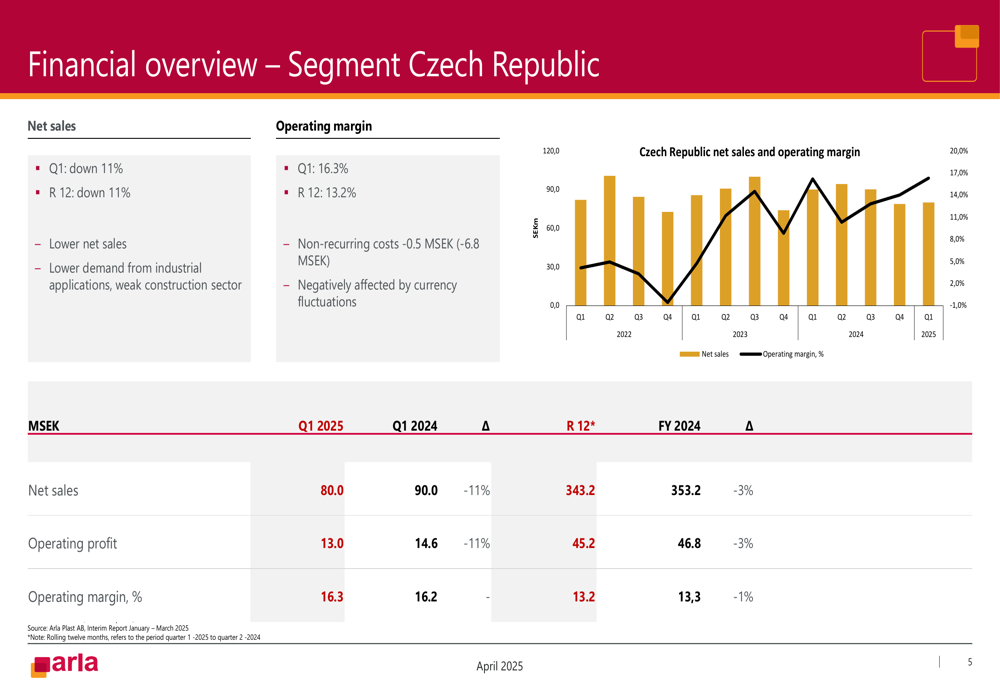

The Czech Republic segment continued to deliver the strongest profitability with a 16.3% operating margin, despite an 11% decline in net sales to 80.0 MSEK. Management cited lower demand from industrial applications and a weak construction sector as primary challenges.

The Sweden segment, which accounted for 39% of total sales, saw a modest 1% revenue increase to 154.8 MSEK, but operating profit fell 43% to 12.0 MSEK with margin declining to 7.8% from 13.9%. Currency fluctuations and non-recurring items of 1.2 MSEK negatively affected results.

The following chart illustrates the Czech Republic segment’s performance:

Germany emerged as a bright spot, with sales increasing 23% to 29.5 MSEK and operating margin improving dramatically to 7.8% from just 0.4% in Q1 2024. Management attributed this to a favorable product and customer mix, despite the weak German economy.

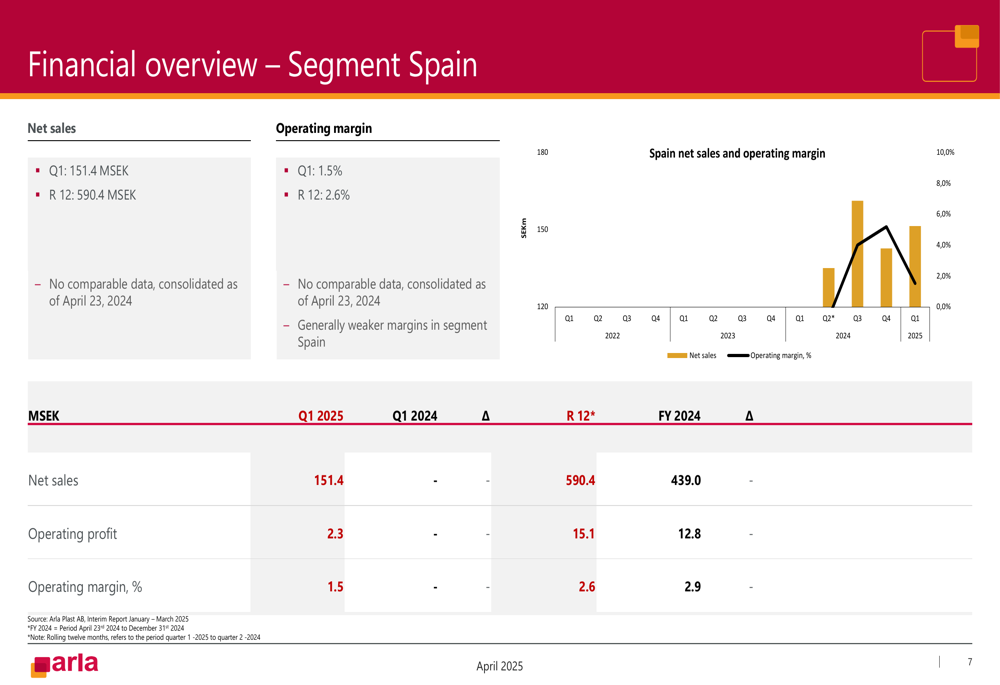

The newly acquired Spain segment contributed 151.4 MSEK in sales but delivered only a 1.5% operating margin, weighing on overall group profitability. The company noted "ongoing operational improvements" in this segment.

Geographic and Product Diversification

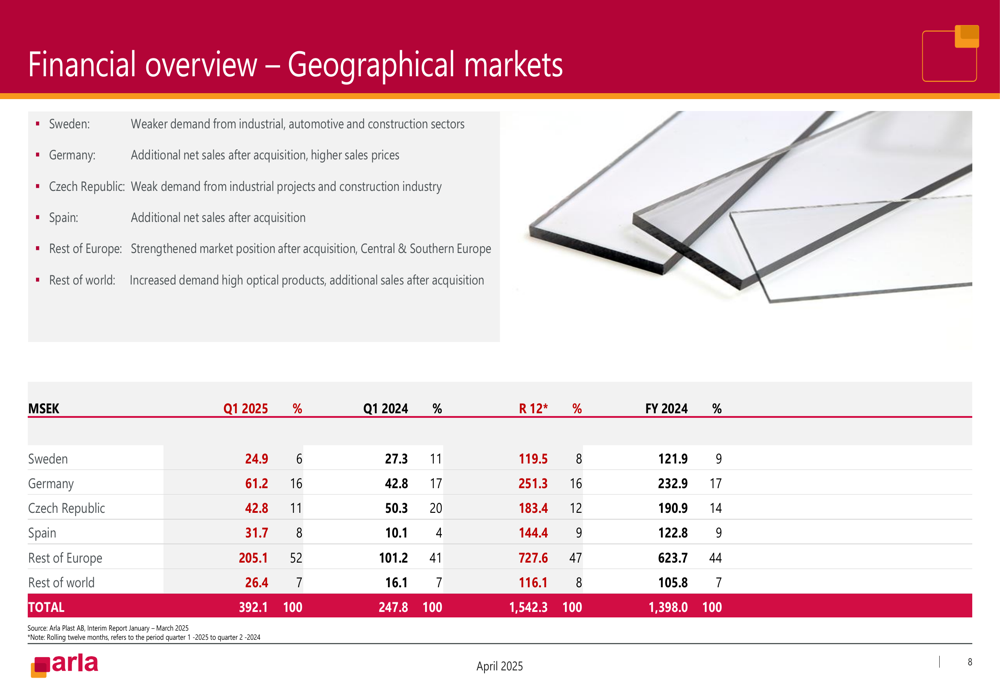

The Nudec acquisition has significantly altered Arla Plast’s geographic sales distribution. Rest of Europe now represents the largest market at 52% of sales (205.1 MSEK), up from 41% a year earlier. Germany, Spain, and Rest of World markets all gained importance in the sales mix.

The following geographical breakdown illustrates this shift:

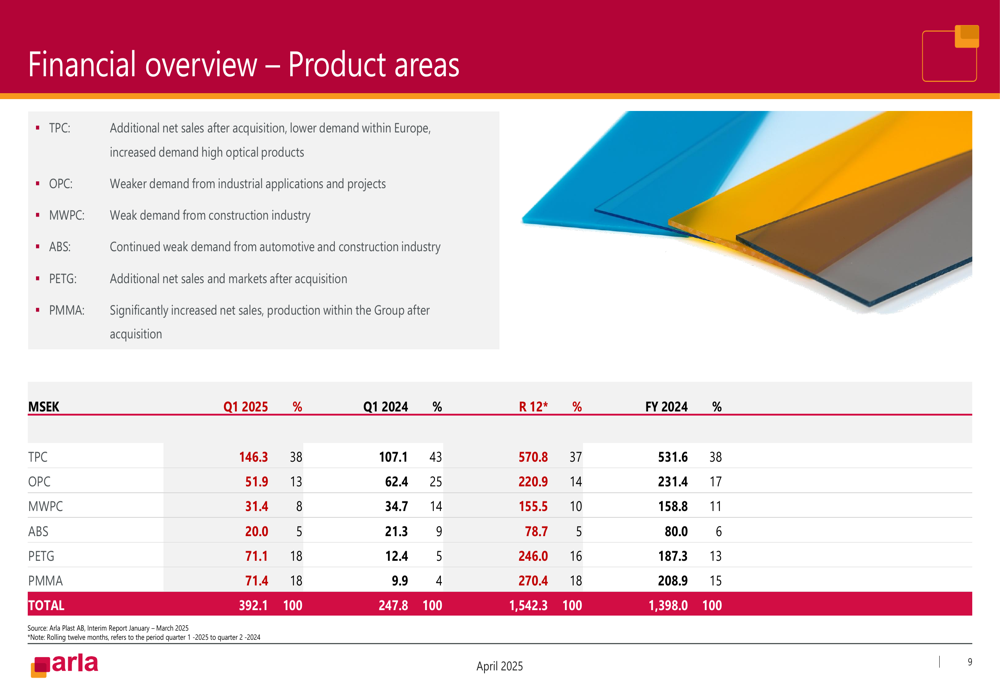

From a product perspective, the acquisition has diversified Arla Plast’s portfolio, with significant increases in PETG and PMMA product categories. While Transparent Polycarbonate (TPC) remains the largest product area at 38% of sales, its share has decreased from 43% a year earlier.

The product mix evolution is shown in this breakdown:

Forward-Looking Statements

Management provided a cautious outlook, noting that raw material prices showed a slight downward trend but remained difficult to predict. The company expects low direct impact from potential tariffs on the American market.

Arla Plast highlighted its strengthened position in Europe and broader product and customer portfolio through the Nudec acquisition. The company also noted increased demand for high optical products from North America as a positive trend.

Strategic initiatives include ongoing operational improvements in the Spain segment, optimization and modernization of production equipment in the Czech Republic, and preparation work for warehouse and production facilities in Sweden.

The company emphasized its strong financial position, which "enables a high investment pace" going forward, while acknowledging the challenging European market environment with decreased volumes and increased price competition.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.