Paul Tudor Jones sees potential market rally after late October

Introduction & Market Context

Arla Plast AB (ARPL) shares surged 10.23% to 58.2 on August 15, 2025, following the release of its Q2 2025 interim report showing significant margin improvement despite flat sales. The Swedish manufacturer of extruded sheets of thermoplastic materials has successfully leveraged its recent acquisition of Nudec S.A.U. to offset organic sales declines in its core markets.

The company’s transformation from a net debt to net cash position highlights its strengthened financial foundation, even as it navigates challenging market conditions including weak demand in several industrial sectors and increased price competition across Europe.

Quarterly Performance Highlights

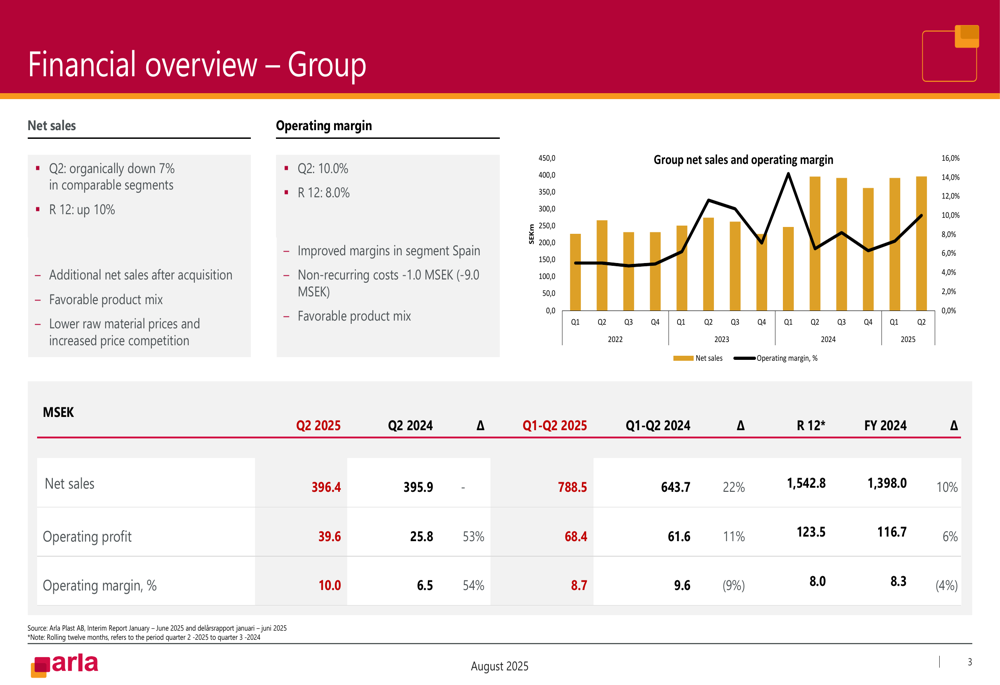

Arla Plast reported Q2 2025 net sales of 396.4 MSEK, virtually unchanged from 395.9 MSEK in Q2 2024. However, operating profit surged 53% to 39.6 MSEK, driving the operating margin to 10.0% compared to 6.5% in the same period last year.

The company’s performance reflects a successful balancing act between acquisition-driven growth and organic challenges, as shown in the following financial overview:

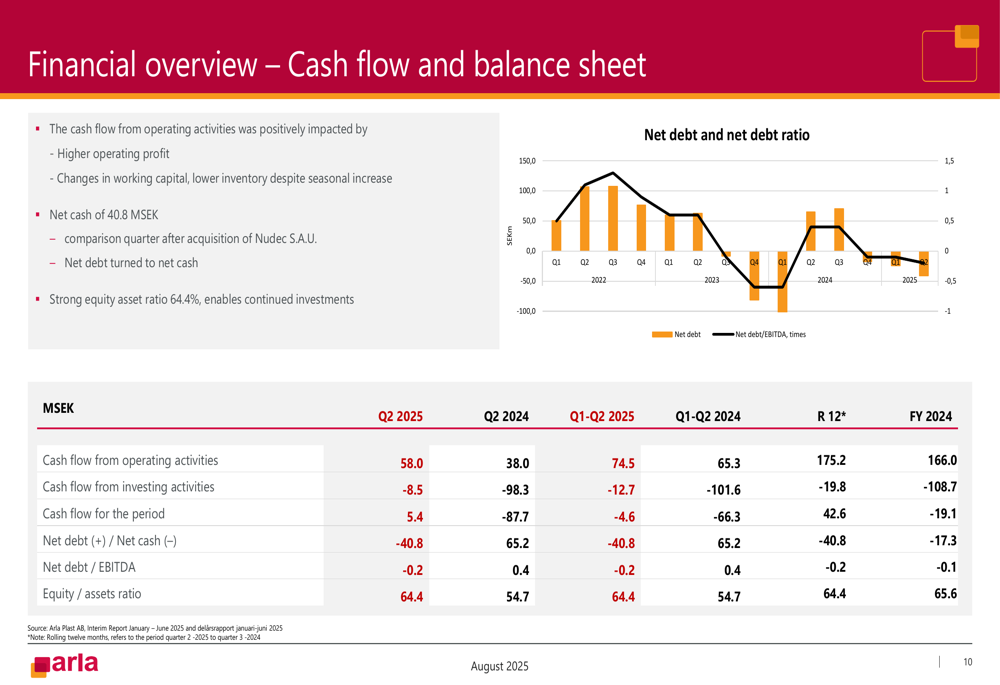

Cash flow from operating activities improved significantly to 58.0 MSEK, up from 38.0 MSEK in Q2 2024, driven by higher operating profit and efficient working capital management. The company has achieved a net cash position of 40.8 MSEK, compared to a net debt of 65.2 MSEK in the comparative quarter, while maintaining a strong equity/assets ratio of 64.4%.

Detailed Financial Analysis

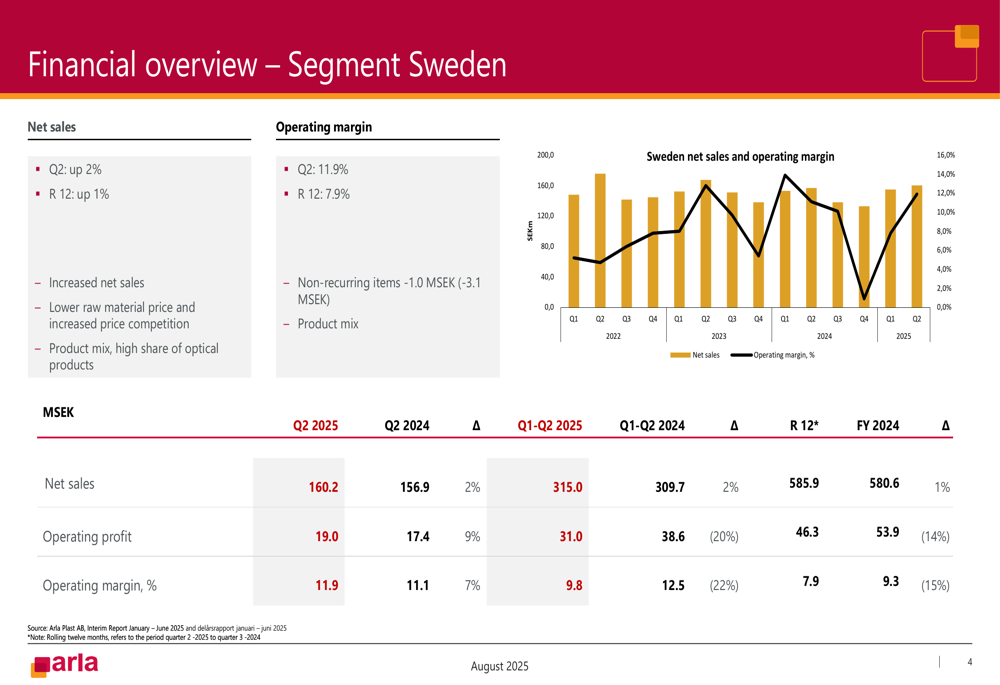

Arla Plast’s segment performance showed mixed results across its geographic footprint. The Swedish segment delivered 2% sales growth with an improved operating margin of 11.9%, benefiting from a favorable product mix with a high share of optical products.

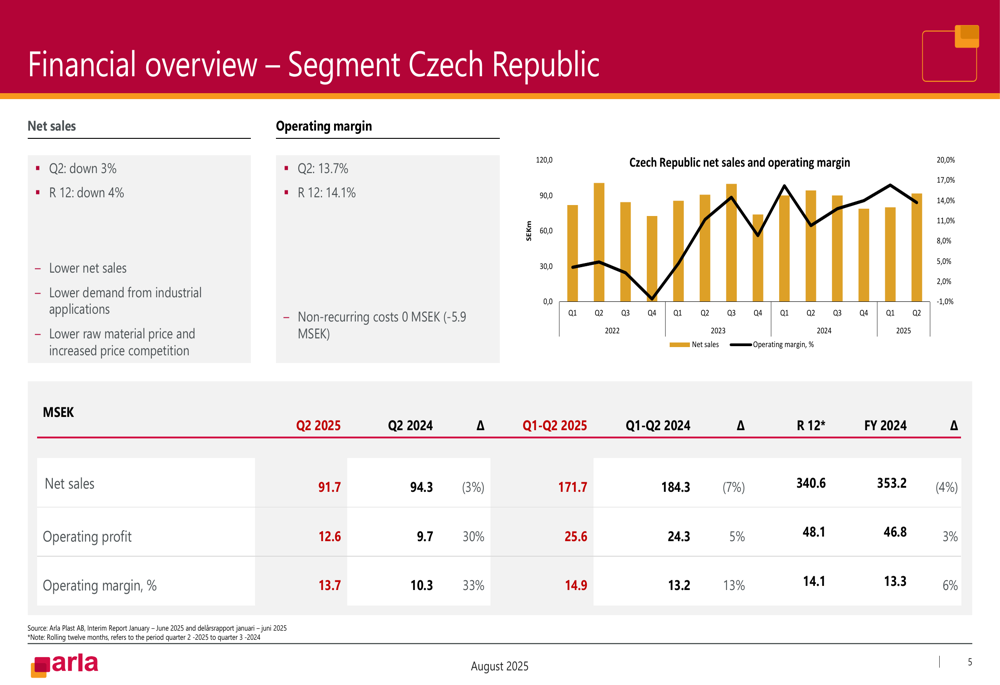

The Czech Republic segment faced headwinds with a 3% sales decline due to lower demand from industrial applications, but still managed to improve its operating margin to 13.7% from 10.3% in Q2 2024.

Germany experienced the most significant challenges with a 14% sales decline and operating margin contraction to 6.6% from 11.6%, reflecting weak demand and increased price competition in the region.

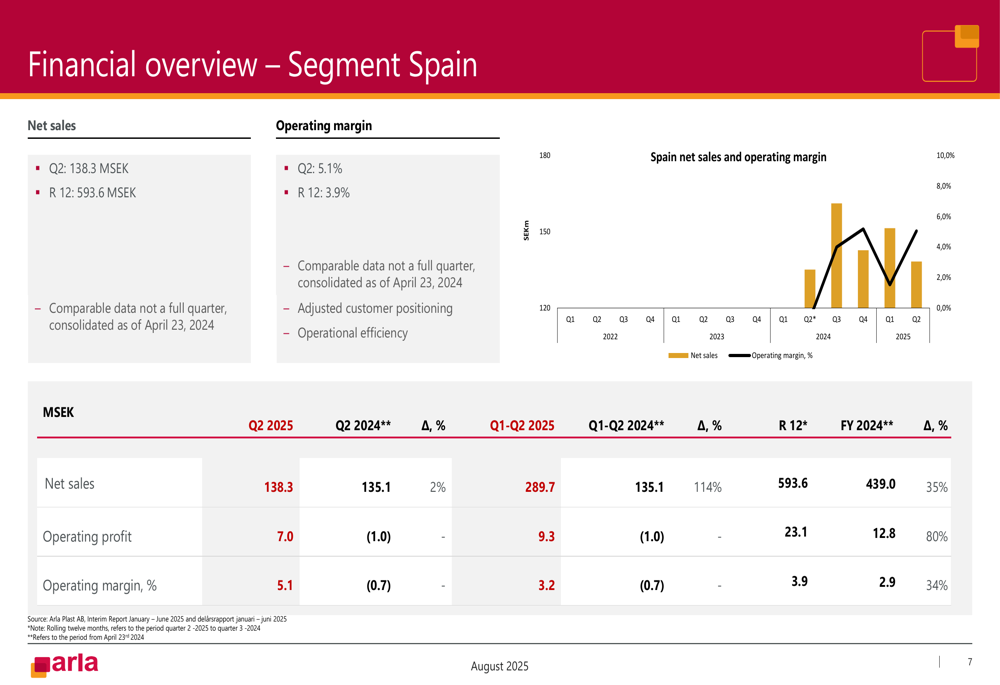

The newly acquired Spanish segment contributed 138.3 MSEK in net sales with a 5.1% operating margin, showing improvement from negative margins in the comparative period through adjusted customer positioning and operational efficiency initiatives.

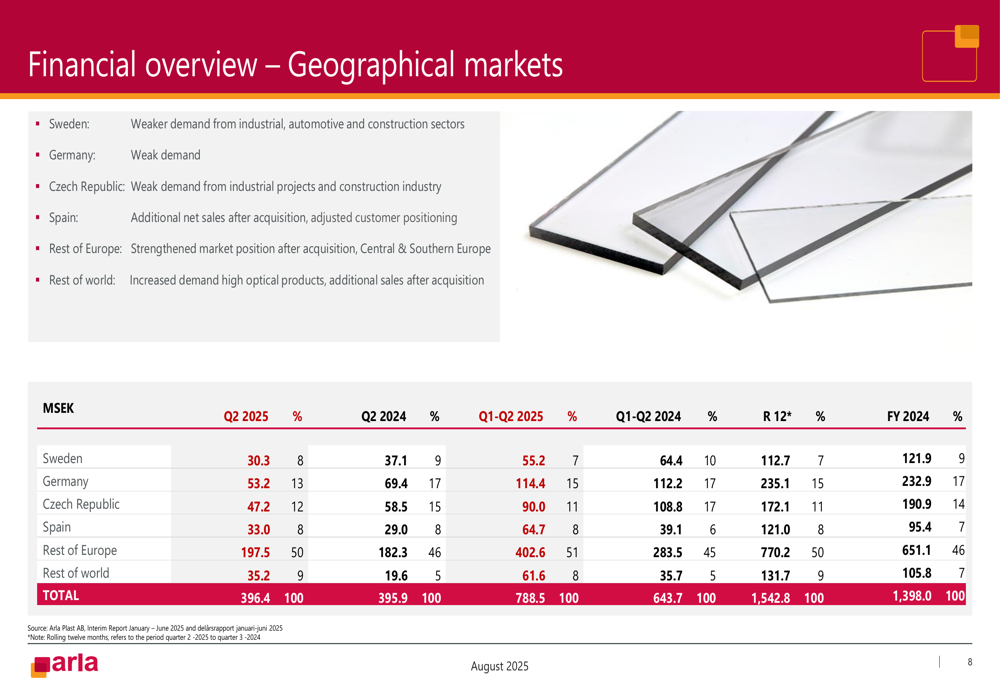

From a geographical perspective, Rest of Europe represents Arla Plast’s largest market at 50% of total sales, followed by Germany (13%), Czech Republic (12%), and growing contributions from Spain (8%) and Rest of World (9%).

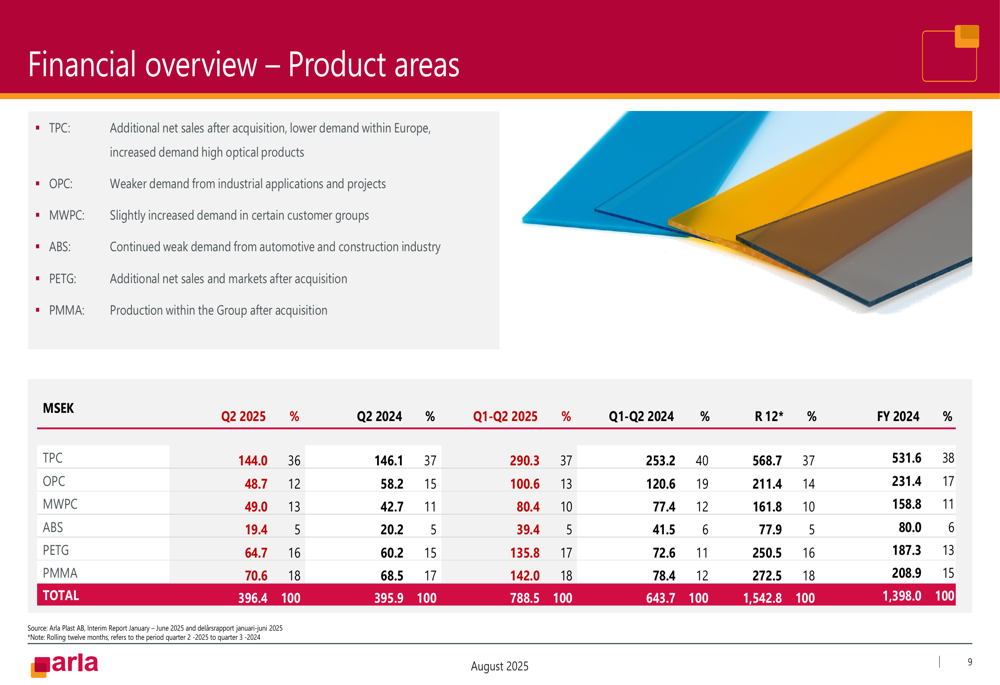

The company’s product portfolio has expanded following the Nudec acquisition, with Transparent Polycarbonate (TPC) remaining the largest category at 36% of sales, while PETG (16%) and PMMA (18%) have gained significance.

Strategic Initiatives

Arla Plast’s acquisition of Nudec S.A.U. has proven strategically important, contributing additional sales and expanding the company’s product portfolio and geographic reach. The integration appears to be progressing well, with the Spanish segment showing margin improvement.

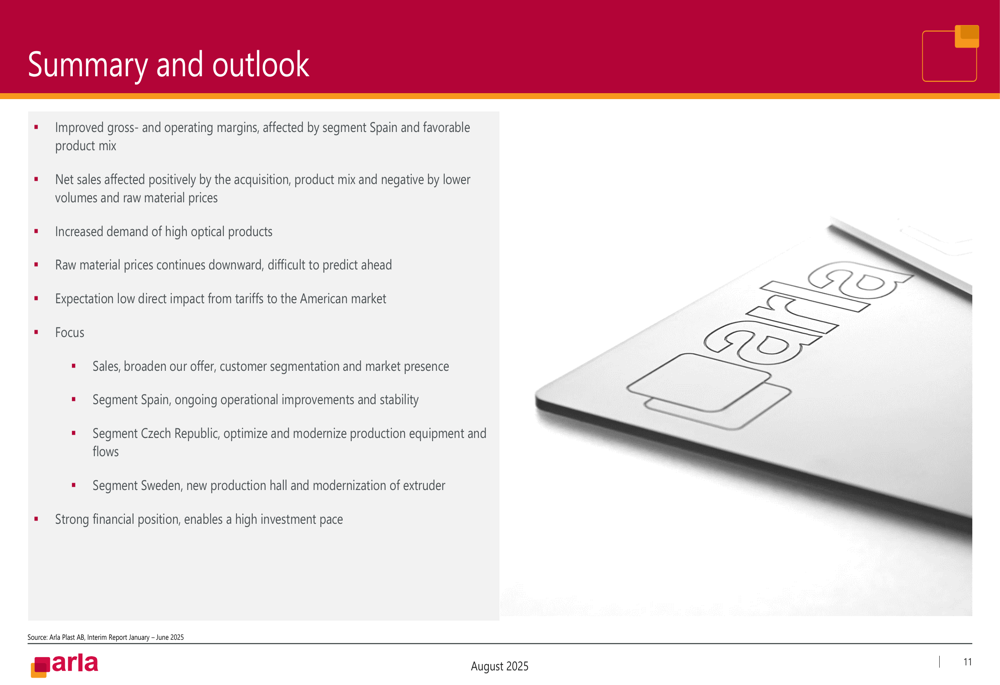

The company continues to invest in operational improvements, including a new production hall and modernization of extruder equipment in Sweden, optimization of production equipment and flows in the Czech Republic, and ongoing operational improvements in Spain.

These initiatives are supported by Arla Plast’s strong financial position, which enables a high investment pace while maintaining financial stability.

Forward-Looking Statements

Looking ahead, Arla Plast noted that raw material prices continue to trend downward, though future movements remain difficult to predict. The company expects low direct impact from tariffs to the American market.

Management emphasized its focus on broadening product offerings, customer segmentation, and market presence, while continuing to drive operational improvements across all segments. The increased demand for high optical products represents a bright spot amid generally challenging market conditions.

Despite organic sales challenges, Arla Plast’s significant margin improvement, strong cash flow generation, and successful integration of its Spanish acquisition position the company well for continued performance improvement, as reflected in the positive market reaction to its Q2 2025 results.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.