Goldman Sachs chief credit strategist Lotfi Karoui departs after 18 years - Bloomberg

Introduction & Market Context

Atea ASA (OB:ATEA), the Nordic region’s leading IT infrastructure provider, reported record first-quarter operating profit in its Q1 2025 presentation held on April 29, 2025. The company achieved strong growth across all business lines and geographic regions, demonstrating resilience in a market where most companies are still in early stages of AI adoption and amid ongoing geopolitical concerns around public cloud services.

As shown in the following summary of key financial highlights, Atea delivered impressive year-over-year growth in multiple metrics:

Quarterly Performance Highlights

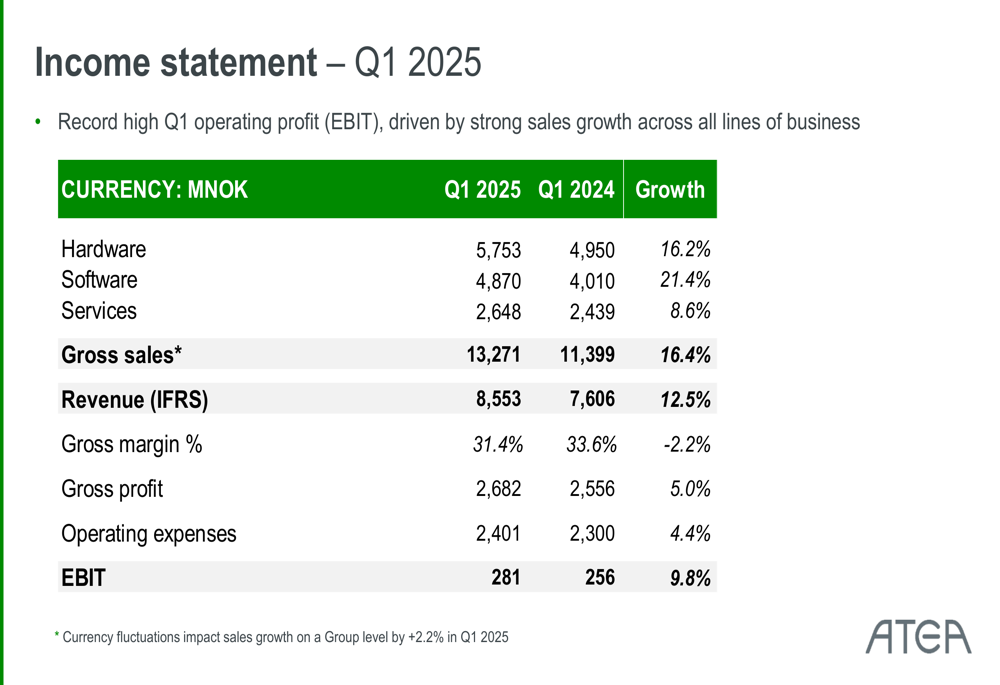

Atea reported gross sales of NOK 13.3 billion in Q1 2025, representing a 16.4% increase compared to the same period last year. Operating profit (EBIT) reached a record high of NOK 281 million, up 9.8% year-over-year, while revenue (IFRS) grew by 12.5% to NOK 8.6 billion.

The company’s financial performance was driven by strong growth across all business lines, with software sales leading the way at 21.4% growth, followed by hardware at 16.2% and services at 8.6%. Currency fluctuations had a positive impact of 2.2% on group-level sales growth during the quarter.

The detailed income statement reveals solid performance metrics despite a slight decrease in gross margin:

Detailed Financial Analysis

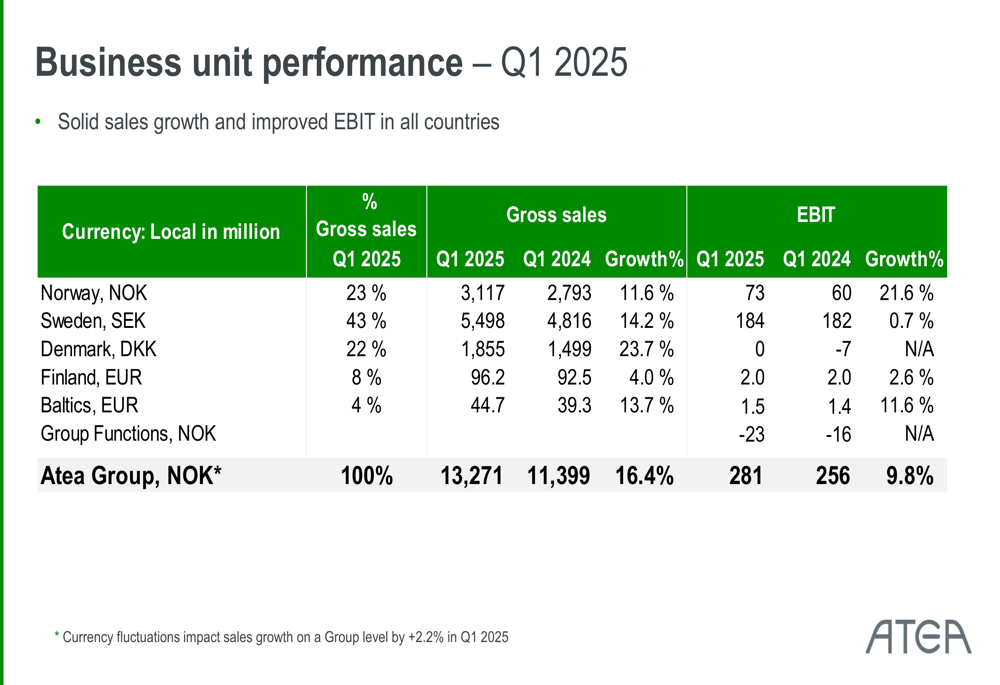

Atea’s business unit performance showed growth across all geographic regions, with particularly strong results in Denmark (23.7% sales growth) and Sweden (14.2% sales growth). Norway delivered 11.6% growth while improving EBIT by 21.6%. Denmark’s operations reached breakeven EBIT, improving from a loss in the previous year.

The following breakdown illustrates performance by business unit:

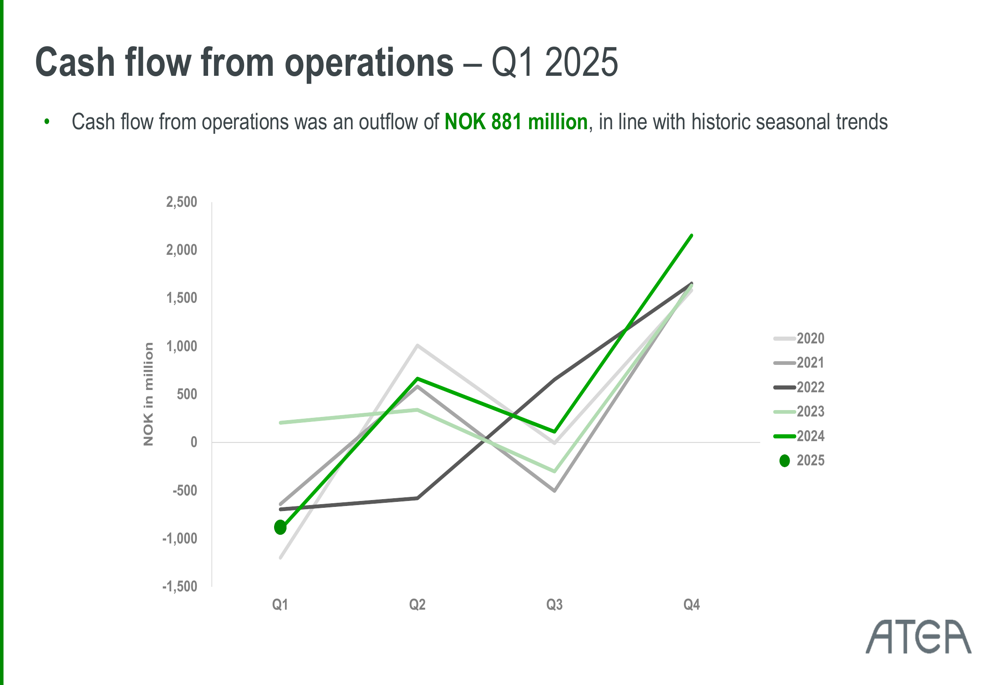

Despite strong operational results, Atea reported a cash outflow from operations of NOK 881 million, which the company noted was in line with historic seasonal trends. This pattern is visible in the following chart showing quarterly cash flow trends:

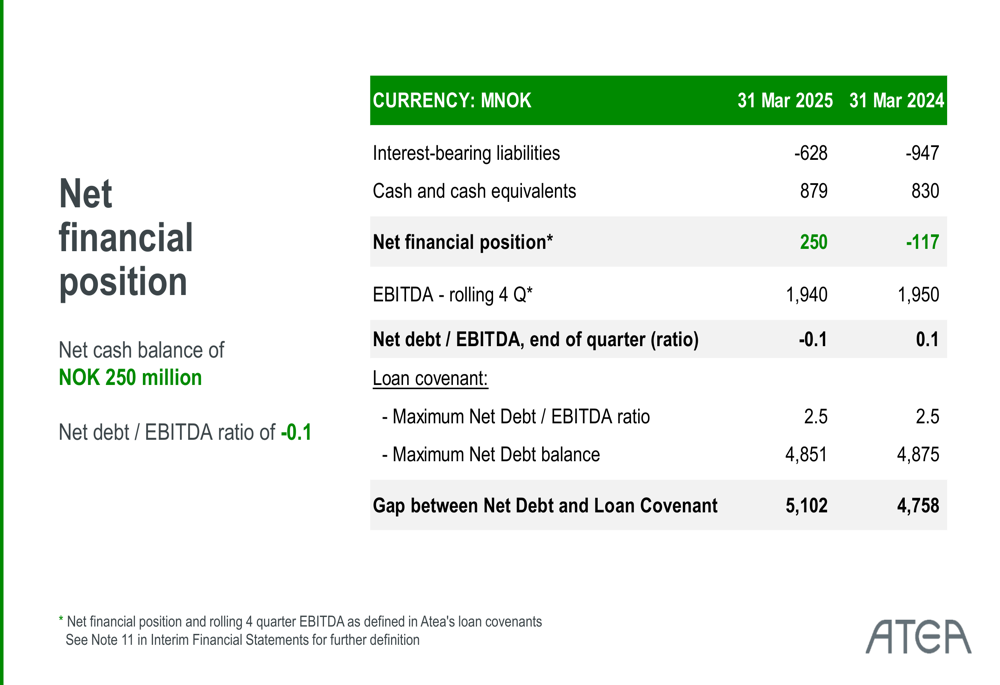

The company maintained a strong financial position with a net cash balance of NOK 250 million as of March 31, 2025, compared to a net debt position of NOK 117 million a year earlier. This represents an improvement of NOK 367 million year-over-year. Atea’s net debt to EBITDA ratio stands at -0.1, well below its maximum covenant of 2.5.

Strategic Initiatives & Growth Drivers

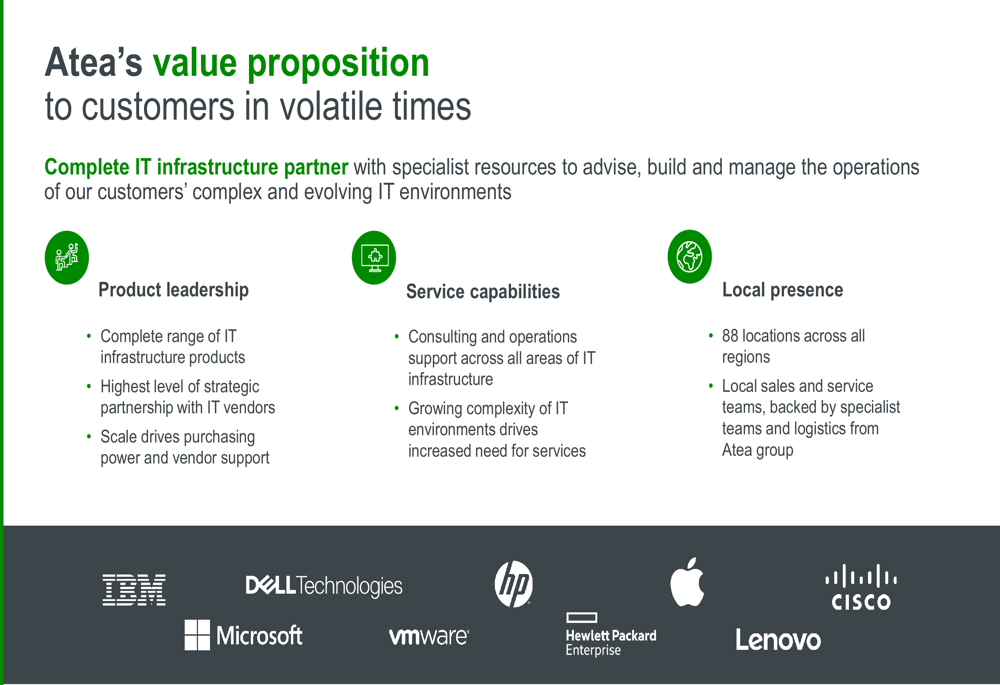

Atea’s strategic positioning as a complete IT infrastructure partner appears well-aligned with current market conditions. The company highlighted that 65-70% of its sales come from public sector customers, which are less influenced by economic cycles. Additionally, its highly fragmented customer base (with the largest customer representing only 2% of revenue) provides resilience against customer-specific risks.

The company is actively addressing the cautious approach many organizations are taking toward AI adoption. According to Boston Consulting Group research cited in the presentation, only 22% of companies have advanced beyond the proof-of-concept stage in AI implementation, and just 4% are creating substantial value. This presents both a challenge and an opportunity for Atea’s advisory and implementation services.

In response to geopolitical concerns around public cloud adoption, Atea is promoting a "hybrid" approach that allows customers to maintain flexibility in where their data and workloads reside. The company provides complete advisory and support services for customers seeking this hybrid data center model.

The following slide outlines Atea’s value proposition as a complete IT infrastructure partner with specialist resources:

Forward-Looking Statements

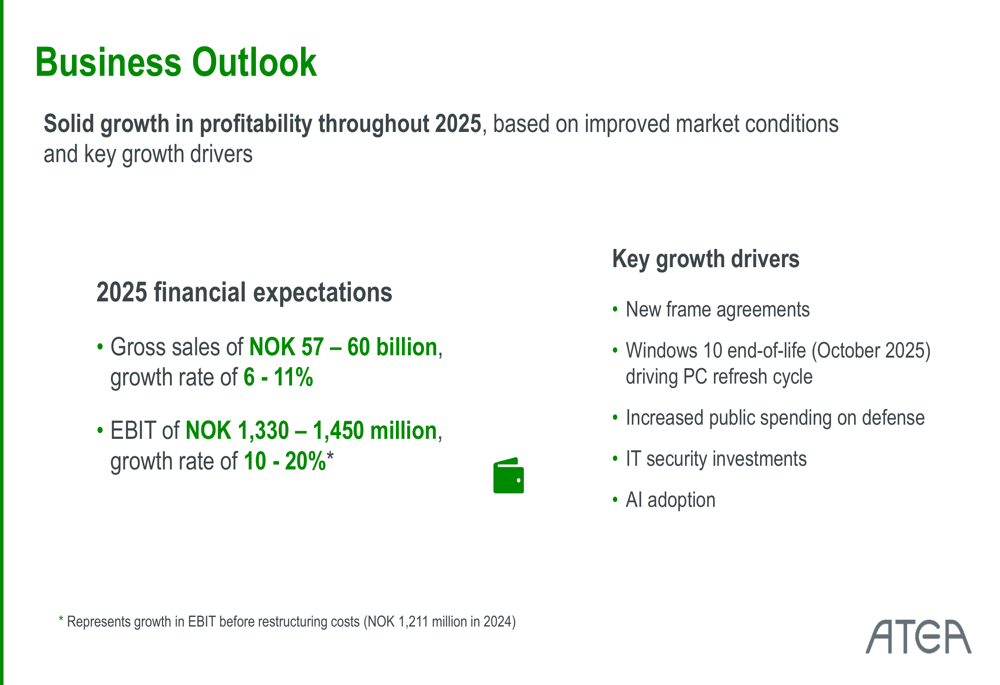

For the full year 2025, Atea provided an optimistic outlook based on improved market conditions and several key growth drivers. The company expects gross sales of NOK 57-60 billion, representing growth of 6-11%, and EBIT of NOK 1,330-1,450 million, reflecting growth of 10-20% compared to 2024’s EBIT before restructuring costs (NOK 1,211 million).

These projections are supported by several specific growth catalysts, including new frame agreements, the approaching end-of-life for Windows 10 in October 2025 (which is expected to drive a PC refresh cycle), increased public spending on defense, growing IT security investments, and the gradual adoption of AI technologies.

The following business outlook summarizes these expectations and growth drivers:

Atea’s strong Q1 2025 results and positive outlook for the full year suggest the company is well-positioned to capitalize on its market leadership in Nordic IT infrastructure while navigating macroeconomic uncertainties and evolving technology trends. The company’s diversified business model across regions and sectors, combined with its strong financial position, provides a solid foundation for continued growth.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.